CLAR - Clarus: Promising Initiatives But Risks Still Present

2023-10-09 02:04:22 ET

Summary

- The company's revenue decreased by 27.2%, and the operating loss (% of revenue) reached 0.3%.

- Declining real consumer incomes, price investments, and high industry inventories continue to have a negative impact on business financial performance.

- I believe that financial performance may take longer to recover, so my recommendation is hold.

Introduction

Shares of Clarus (CLAR) have fallen 20% YTD. Despite the fact that the company's management is quite optimistic about the future performance of the business, I believe that it is still not the best time to open a long position in the company's shares. In my article, I would like to analyze current trading trends and share my own opinions on the future financial performance of the business and current valuation.

Investment thesis

Despite significant pressure on both revenue growth and operating margins, management is fairly optimistic for the second half of 2023, but I believe the company's financials will continue to be under pressure in the next quarter, while shares are still not cheaply priced. In addition, the improvement in profitability is largely due to the recovery of gross margin in the Precision Sports segment, which, in my personal opinion, is associated with additional risks.

Company overview

Clarus designs, develops, and manufactures outdoor equipment and products. The main business segments are Outdoor (48% of revenue), Precision Sports (31% of revenue) and Adventure (21% of revenue). The company makes sales both in the domestic market (56% of revenue) and in the international market (44% of revenue). The company was founded in 1957.

2Q 2023 Earnings Review

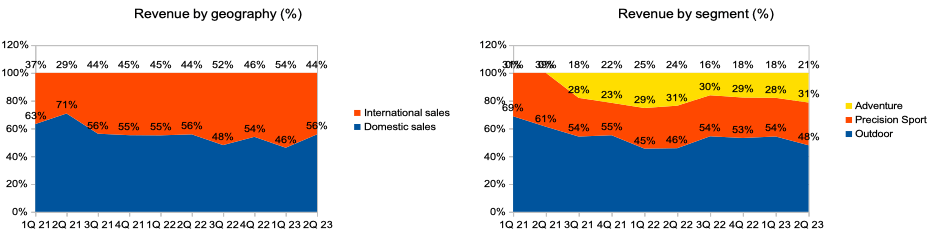

The company reported worse than investors expected . The company's revenue decreased by 27.2% YoY . Domestic sales were down 27.2% YoY and international sales were down 27.1% YoY. In terms of business segments, the largest contribution to the decline in revenue was made by the Outdoor segment, where revenue decreased by 23.8% YoY, while in the Precision Sports and Adventure segments sales decreased by 26.7% YoY and 34.2 % YoY, respectively. You can see the details of the revenue mix changes in the graph below.

Revenue by geography (%) and revenue by segment (%) (Company's information)

{kind=link}

Gross profit margin decreased from 38.0% in Q2 2022 to 36.7% in Q2 2023 due to unfavourable changes in product mix and unfavourable FX. Separately, I would like to note the change in gross profit margin for each of the segments. Thus, we see the greatest decrease in the Precision Sports segment, where gross profit margin decreased from 44.9% to 31.7% due to the need to reduce prices due to high inventory levels in the industry, and in the Outdoor and Adventure segments, gross profit margin increased from 33.1% to 37.5% and from 38.5% to 42.2%, respectively. SGA expenses (% of revenue) increased from 30.8% in Q2 2022 to 36.1% in Q2 2023.

Gross profit margin and SGA (% of revenue) (Company's information)

{kind=link}

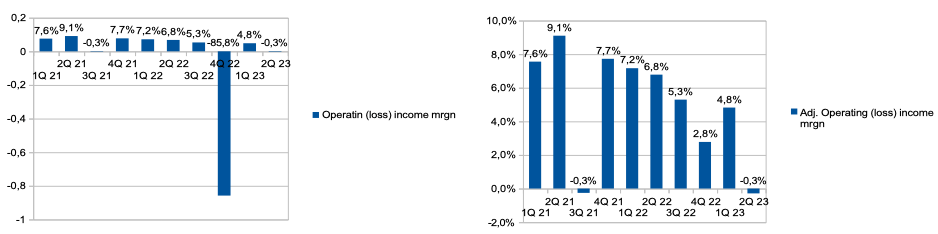

Operating margin decreased from 6.8% in 2Q 2022 to -0.3% in 2Q 2023. In the graph below, I would also like to demonstrate adjusted operating income, because in the 4th quarter of 2022, the company faced one-time expenses for impairment of goodwill and indefinitely-lived intangible assets in the amount of $92.3 million.

{kind=link}

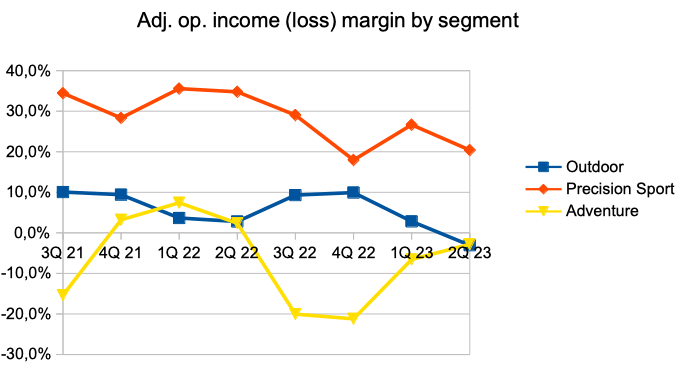

If we pay attention to the operating margin by business segment, we see that profitability continues to decline in all segments. Thus, operating margin in the Outdoor segment decreased from 2.8% to -3.1%, and in the "Precision Sports" and "Adventure" from 34.8% to 20.4% and from 2.4% to -2.8%, respectively.

adj. op. income (loss) margin by segment (Company's information)

{kind=link}

In addition, the company published guidance for 2023. Thus, management expects that in the second half of the year the company will show a decrease in revenue growth rates in the range from 0.5% to 7.3%, and the adjusted EBITDA margin will improve to 20.6%-22.8%.

Guidance (Company's information)

My expectations

On the one hand, I am impressed by the current management initiatives (transforming our product development and innovation process, improving customer service and digital transformation), which are aimed at restoring business revenue growth rates and improving profitability.

While we are experiencing a challenging retail landscape, the changes we have made through the first half of this year and the further cost-outs and savings initiatives we expect to make in the next 6 months are foundational to our growth strategies.

However, on the other hand, in my personal opinion, the operational and financial performance may take longer to recover, so I expect the company's financial performance to continue to be under pressure in the coming quarters. First, I think pressure on sales in the Outdoor segment (48% of revenue) will continue in the second half of 2023 because I do not expect a quick recovery in consumer spending, even if we see a slowdown in inflation, because consumers will continue to face increased day-to-day costs. If we look at management's comments during the Earnings Call following the earnings release, we can see that management is talking about similar trends.

However, as we head into Q3, we are starting to see retail purchasing habits normalize, but we do expect it will take until year-end before the market approaches equilibrium. Somewhat offsetting this weakness was a 28% increase in our direct-to-consumer business, which we believe shows the strength of the Black Diamond brand despite the broader retail environment.

In addition, the company published strong guidance, which implies a recovery in growth rates and profitability, however, if we look at the guidance in more detail, we can see that the main recovery is associated only with the 4th quarter of 2023, while in the next quarter (3Q 23) the pace Sales growth will continue to be under significant pressure.

Guidance (Company's information)

I would also like to note that the restoration of profitability is associated with an improvement in gross margin in the Precision Sports segment, where the company experienced the largest decline. However, it is my personal opinion that high inventory levels in the industry, consumer pressure from macro headwinds, and a decrease in the amount of time people choose to spend outside the home will continue to put pressure on profitability in the segment. So I think the current guidance looks optimistic, but the financials are still quite uncertain.

Moreover, I think that additional pressure on profitability may be exerted by the deleverage effect due to a decrease in the scale of the business because part of the operating expenses (salaries, distribution) is fixed.

Risks

Revenue: lower consumer spending, high industry inventory levels, and a decline in the amount of time people choose to spend outside the home could put pressure on revenue growth rates in the coming quarters.

Margin: investments in prices, unfavourable product mix, unfavourable changes in FX, increased marketing costs, and deleverage effects due to reduced economies of scale may have a negative impact on the operating profitability of the business.

Drivers

Revenue: launch of new products, simplification of the cooperation model with partners, and expansion of the e-commerce platform for B2B and B2C sales may contribute to revenue growth in the future.

Margin: recovery of gross margin in the Precision Sports segment due to the normalization of supply and demand before the hunting season can provide significant support to the operating profitability of the business.

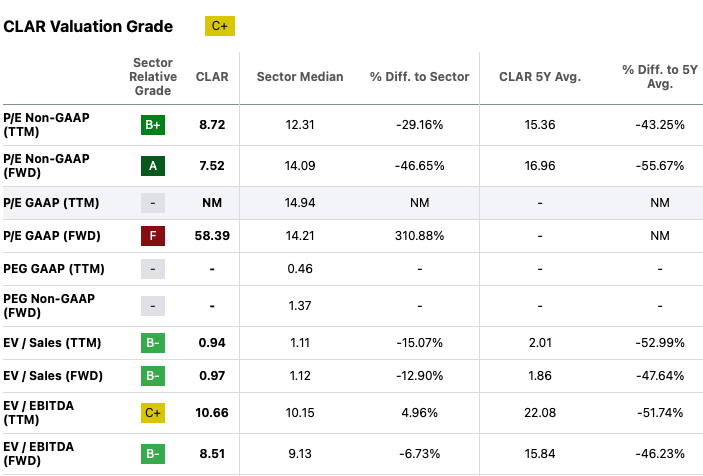

Valuation

Valuation Grade is C+. In accordance with the P/E ((FWD)) and EV/EBITDA ((FWD)) multiples, the company's shares are trading at 7.5x and 8.5x, respectively, which implies a discount to the sector median of about 47% and 7%, respectively. Despite the fact that the stock doesn't look expensive, I believe investors need to wait for the next quarter's financial results before making a purchase decision because: 1) I believe the company deserves a discount based on the size of the business 2 ) shares may trade at relatively low prices for long periods of time in the absence of clear growth drivers/catalysts (revenue growth, improved profitability).

{kind=link}

Conclusion

Thus, at the moment my recommendation is hold. I believe that pressure on both revenue growth and profitability may continue in the coming quarters, while the shares are still not cheaply priced. I will be happy to change my recommendation to buy if I see that the company is able to demonstrate stable and sustainable improvements in financial performance in both domestic and international markets.

For further details see:

Clarus: Promising Initiatives, But Risks Still Present