CLAR - Clarus: Too Much Risk

2023-05-08 05:09:36 ET

Summary

- CLAR posted disappointing Q1 FY23 results.

- They look fundamentally and technically weak. In addition its valuation seems high.

- They have a huge debt and their revenue growth rate is poor.

- I assign a hold rating on CLAR stock.

Clarus Corporation ( CLAR ) manufactures and sells lifestyle products and outdoor equipment internationally. Their outdoor segment provides shells, midlayers, logo wear, protection devices, belay devices, ice climbing gears, trekking poles, ski poles, and probes. The precision sports segment manufactures ammunition products for hunting and law enforcement purposes, and in the adventure segment, they provide mounting systems, carriers, and engineered automotive roof racks. CLAR recently posted Q1 FY23 results. I will do their financial and technical analysis in this report. Their revenues and net income have declined significantly in Q1 FY23, and its valuation also seems high. Hence I assign a hold rating on CLAR.

Financial Analysis

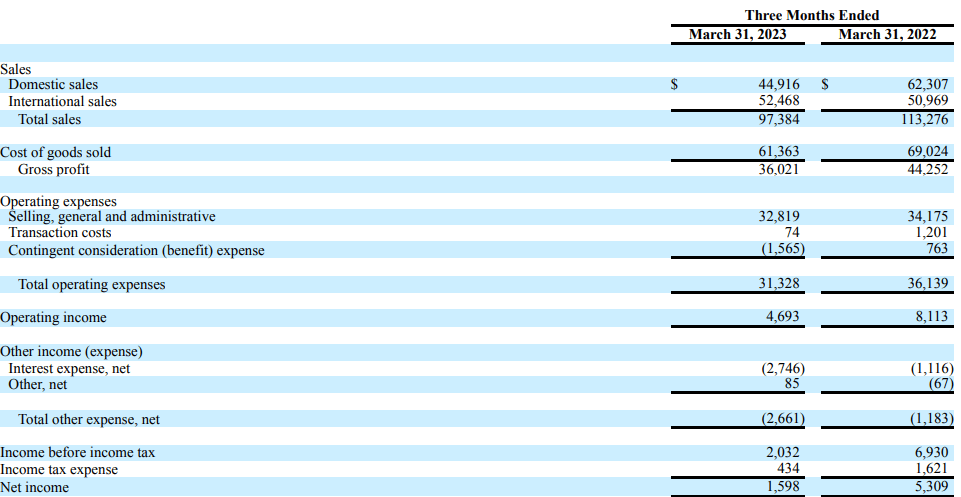

CLAR recently posted its Q1 FY23 results . The sales for Q1 FY23 were $97.3 million, a decline of 14% compared to Q1 FY22. I think the main reason behind the decline was underperformance in its precision sports and adventure segments. The precision sports and adventure segment sales were down by 18.1% and 38.8% in Q1 FY23 compared to Q1 FY22. I believe the decline in sales in the precision segment was due to supply chain issues that limited its ammo sales. The weakness in the Rhino-Rack North American market impacted sales in the adventure segment. The sales from the Rhino-Rack North American market were down by $5.7 million, and I think lower consumer demand and the difficult macro environment in North America and Australia were responsible for the decline. The gross profit margin for Q1 FY23 was 36.9% which was 39% in Q1 FY22. I think the main reason behind the decline was unfavorable FX and unfavorable product and channel mix.

{kind=link}

The net income for Q1 FY23 was $1.5 million, a decline of 70% compared to Q1 FY22. I believe the decline in sales in the precision sports and adventure segments and the $2.4 million headwind because of the strength in the U.S. dollar led to the decline in the net income in Q1 FY23. In my view, the financial performance of CLAR was quite disappointing in Q1 FY23; various factors impacted its business operations, due to which its revenues and net income declined significantly. Moreover, looking at the current market situation, I believe they might continue to struggle financially in the coming quarters.

Technical Analysis

{kind=link}

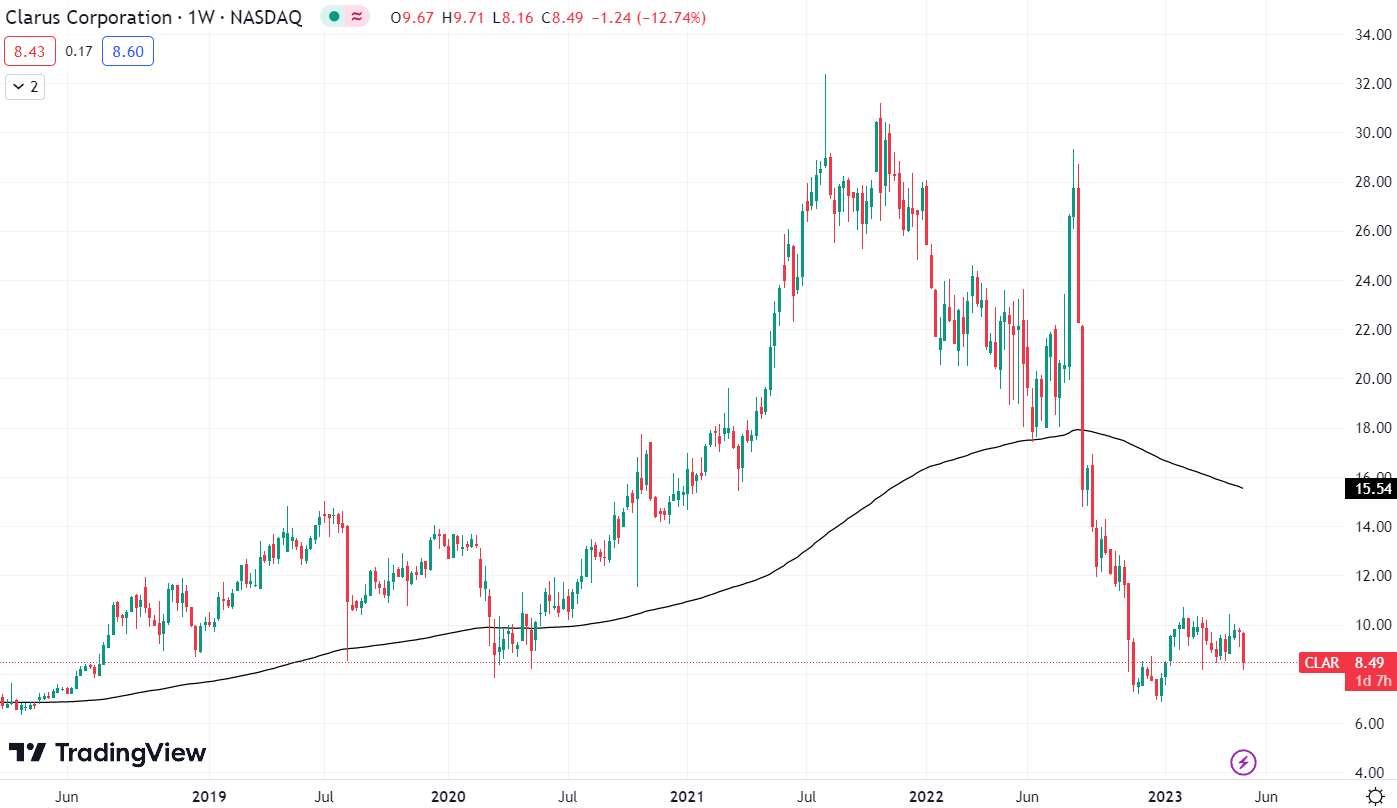

The stock has crashed more than 65% since August 2022, and now the stock is trading at the level of $8. It is very risky to trade in the stock now because it is currently at a crucial level; if it breaks the $8 level, it can fall to $6.5, and looking at the recent price action, I think there is a high chance of it happening. The stock looks bearish, and I think it is best to avoid it right now. One can only think of buying when it gives a strong candle closing above $11; if it breaks $11, it can reach $15. But until then, it is best to avoid the stock.

Should One Invest In CLAR?

CLAR is looking both technically and fundamentally weak. They posted poor quarterly results, and I believe they might continue struggling in the coming quarters. I am saying this because of headwinds they are facing, like supply chain issues, which have affected their sales in the precision segment. The management expects that they might continue to face supply chain challenges in 2023 which might affect their sales in FY23. Not only supply chain challenges, but they are also facing difficulties like imbalanced inventory levels and lesser consumer demand in North America and Europe, where they generate the majority of their revenue. I believe they might continue to face soft consumer demand in the U.S. and Europe markets due to adverse macroeconomic challenges that the U.S. and Europe might face in the second half of 2023, like the recession. In addition, the consumer spending trend is below historical averages, which suggests that consumers are not willing to spend as much as they were in pre-pandemic levels, due to which I believe they are facing inventory overhang challenges and looking at the current market situation, I think it would at least take six months for consumer spending trend to return to the historical average. Therefore I think the challenges in the U.S. and Europe markets might affect its sales to a large extent, and the management’s revenue estimate suggests the same. They have provided a revenue estimate for FY23, which is around $420 million , which is 6.2% less than FY22 revenue. So I believe one should not make any investment decision in the company in 2023. In addition, with a market capitalization of $322 million, they have a total debt of $137 million which is huge, and looking at the poor revenue growth of the company, the debt becomes a matter of concern.

Now talking about their valuation. I will use EV / EBIT and EV / Sales ratios to judge its valuation. CLAR has an EV / EBIT ((TTM)) ratio of 21.47x compared to the sector ratio of 13.28x. CLAR has an EV / Sales ((FWD)) ratio of 1.12x compared to the sector ratio of 1.11x. After looking at both ratios, I believe it is overvalued, and I have come to the conclusion that currently, there are more red flags than green flags in the company. They are looking fundamentally and technically weak, and the future growth estimates are also poor. Hence I believe there is no reason to invest in it, so I assign a hold rating on CLAR.

Risk

Due to several unfavorable events, such as general, domestic, and international market fluctuations, the price and availability of raw materials for their businesses can fluctuate greatly. The state of the global economy includes wage prices, output levels, levels of competition, consumer demand, import levies and tariffs, and exchange rates. This volatility can significantly affect the price and availability of raw materials, adversely affecting the company's operations. In addition, a supply shortage or fluctuations in the availability of a certain raw material could stop production or raise the cost of producing products. Therefore, changes in the availability and cost of raw materials could harm the company and its financial results.

Bottom Line

There are several red flags in the company. They are struggling financially and have a huge debt, and the technical chart looks weak. In addition, their valuation seems high, so I think one should avoid the stock in 2023. Hence I assign a hold rating on CLAR.

For further details see:

Clarus: Too Much Risk