CLH - Clean Harbors Missed Out Big On Heritage-Crystal Clean

2023-08-29 11:14:43 ET

Summary

- Heritage-Crystal Clean is being acquired by J.F. Lehman & Company for $1.2 billion, after no other companies made a better offer during the "go-shop" period.

- Clean Harbors, a potential suitor, missed out on the opportunity to acquire Heritage-Crystal Clean, despite similarities and potential synergies.

- Heritage-Crystal Clean's growth and profitability make it an attractive investment, but the buyout price leaves minimal upside for shareholders.

It's awfully tempting and even, in some respects, encouraged, to think about companies as efficiently run organizations that always or usually always succeed in optimizing shareholder value. But the more you come to understand about the companies that are out in the market, the more you realize just how far off the mark this view is. One really great example that I could point to involves the recently announced acquisition of Heritage-Crystal Clean ( HCCI ). There was some hope that the enterprise would be acquired for an even higher price than what was initially agreed upon. And some analysts even pointed out Clean Harbors ( CLH ) as a valid suitor. And yet, a large number of firms managed to pass up on what could have been considered the deal of a lifetime. This is bad for all parties involved, though it doesn't necessarily mean that shareholders should shortchange the companies when looking at the long-term picture.

A big disappointment

The last article that I wrote about Heritage-Crystal Clean was published in April of this year. In that article, I took a rather bullish stance on the firm. Attractive growth on both the top and bottom lines drew me to the company. However, I was also impressed by how cheap shares were and the overall growth potential of the enterprise moving forward. At the end of the day, these factors led me to rate the business a ‘buy’. And that is a call that has so far proven to be great. Shares are up 26.4% since the publication of that article. That compares to the 8.5% upside seen by the S&P 500.

To be perfectly clear, the lion’s share of this upside was driven by news that broke in July of this year that Heritage-Crystal Clean had agreed to be acquired by J.F. Lehman & Company in a deal valued at approximately $1.2 billion. In exchange for the stock of the business, the acquirer would pay each shareholder of Heritage-Crystal Clean $45.50 per share in cash for each unit said shareholder owned. This translated to a 24.9% premium over the 60-day volume weighted average price of the company leading up to the date of the announcement.

Normally in instances like this, the suitor wants to lock down the deal so that a bidding war does not erupt. But in some cases, the seller has the negotiating power to permit for what is called a ‘go-shop’ period. This is a window of time during which the company that has agreed to be acquired can shop around for more attractive offers. In this particular case, the ‘go-shop’ period for Heritage-Crystal Clean was set at 35 days, with midnight on August 23 representing the expiration date that Heritage-Crystal Clean had to get a better offer. Well, sure enough, on August 24, the management team at the enterprise announced that they failed to get a better offer.

This does not mean that management did not try to market the firm. According to the business, the company engaged with or actively solicited alternative proposals from no fewer than 53 ‘potentially interested’ parties. But at the end of the day, J.F. Lehman & Company ended up surviving unopposed. Upon hearing this, I was very surprised. Because as I discussed in my aforementioned article, shares of the business did look very cheap. In particular, I was shocked that competitor Clean Harbors did not step up to the plate and take a swing of the bat. I don't think I was the only one. After the news broke of the acquisition and the ‘go-shop’ period, an analyst at Baird expressed that Clean Harbors would be a ‘natural buyer’ of Heritage-Crystal Clean.

There are multiple reasons why I believe Clean Harbors missed out on a fantastic opportunity. For starters, the companies do have a lot in common. Admittedly, Clean Harbors is a significantly larger enterprise with a market capitalization of $9.28 billion and an enterprise value of $11.26 billion. However, they do operate in the same space. For starters, they are both players in the waste business. As of the end of the most recent quarter , Clean Harbors controls over 100 waste management facilities, including nine incinerators, nine landfill sites, 33 treatment, storage, and disposal facilities, eight solvent recycling facilities, and 10 wastewater treatment operations. It also has eight re-refineries, and over 15,000 company vehicles at its disposal. It truly is a massive player with operations spread across the US and parts of Canada.

Heritage-Crystal Clean is no slouch either. The company operates over 10 non-hazardous waste processing facilities, largely centered around waste water treatment and non-hazardous solids. This is on top of five antifreeze recycling centers and a single solvent recycling facility. It actually operates as the second largest full-service parts cleaning company in the country, and its operations include an oil business that engages in the collection of oil, oil filter disposal, re-refining, and other similar activities. In fact, according to management, the company is the second largest oil collector and re refiner in North America, with annual base oil capacity of 50 million gallons.

Buying up Heritage-Crystal Clean would make perfect sense for Clean Harbors, not only because it would expand the company's footprint further, but also because it could capture some synergies. It's unclear how much we are talking about. But it wouldn't be unthinkable that the business might achieve hundreds of millions of dollars of synergies per annum. Outside of the companies having similarities, there are other reasons why an offer seemed obvious.

{kind=link}

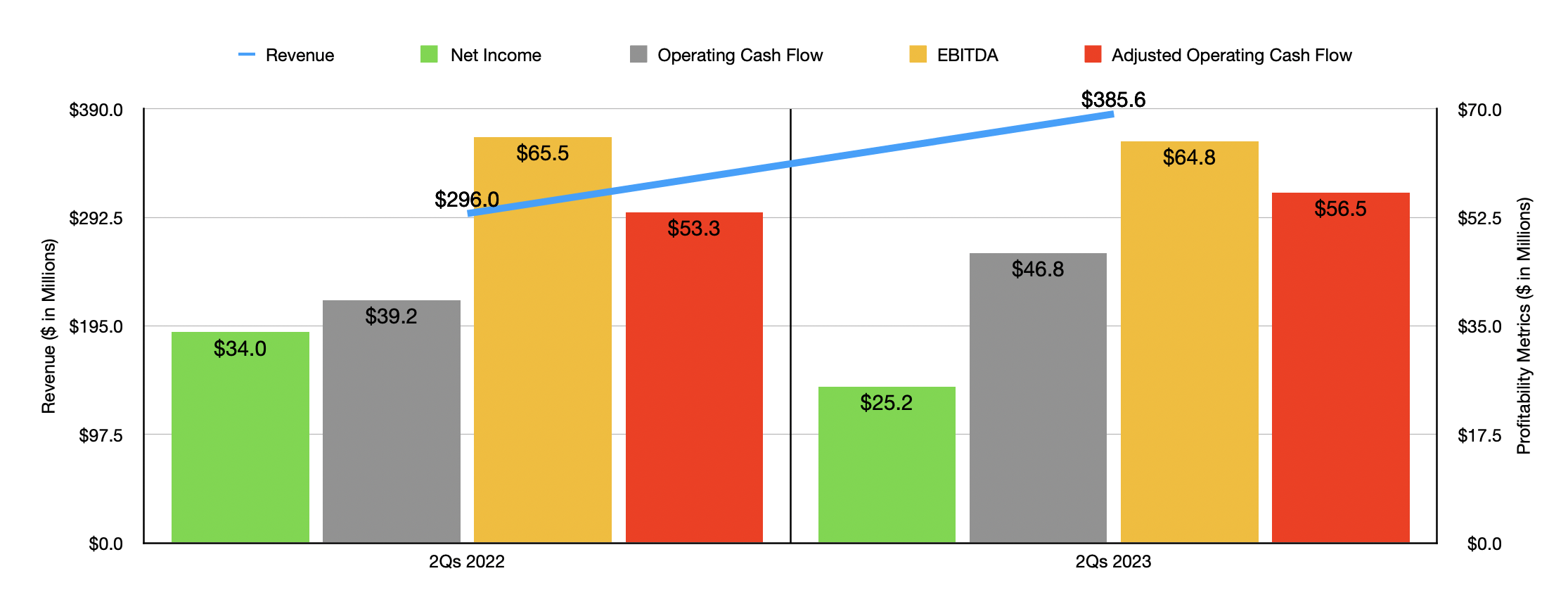

First and foremost, Heritage-Crystal Clean continues to grow at a nice clip. Management just announced financial results covering the second quarter of the company's 2023 fiscal year. For the first half of the year , revenue came in at $385.6 million. That's 30.3% higher than the $296 million reported one year earlier. It is true that net profits fell from $34 million to $25.2 million. But other profitability metrics were more stable. Operating cash flow, for instance, shot up from $39.2 million to $46.8 million. On an adjusted basis, it rose from $53.3 million to $56.5 million, while EBITDA declined from $65.5 million to $64.8 million.

{kind=link}

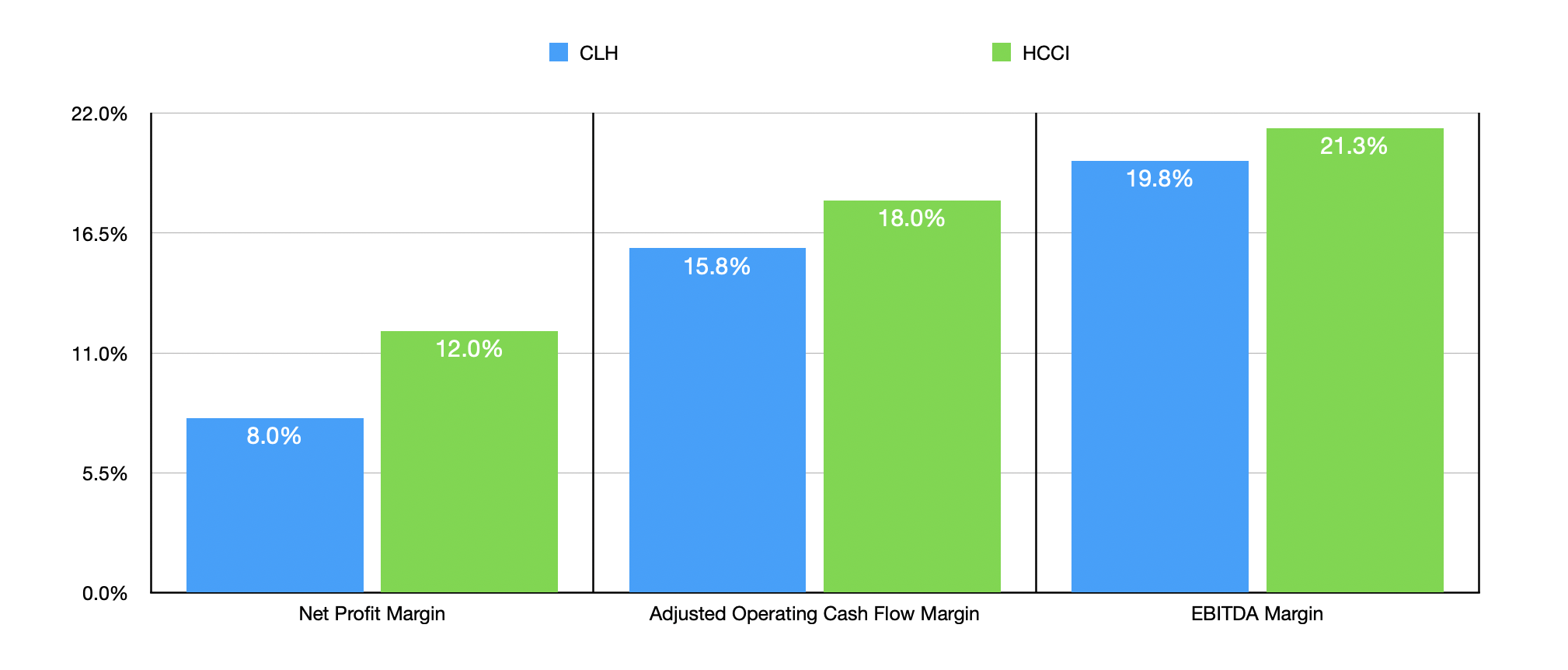

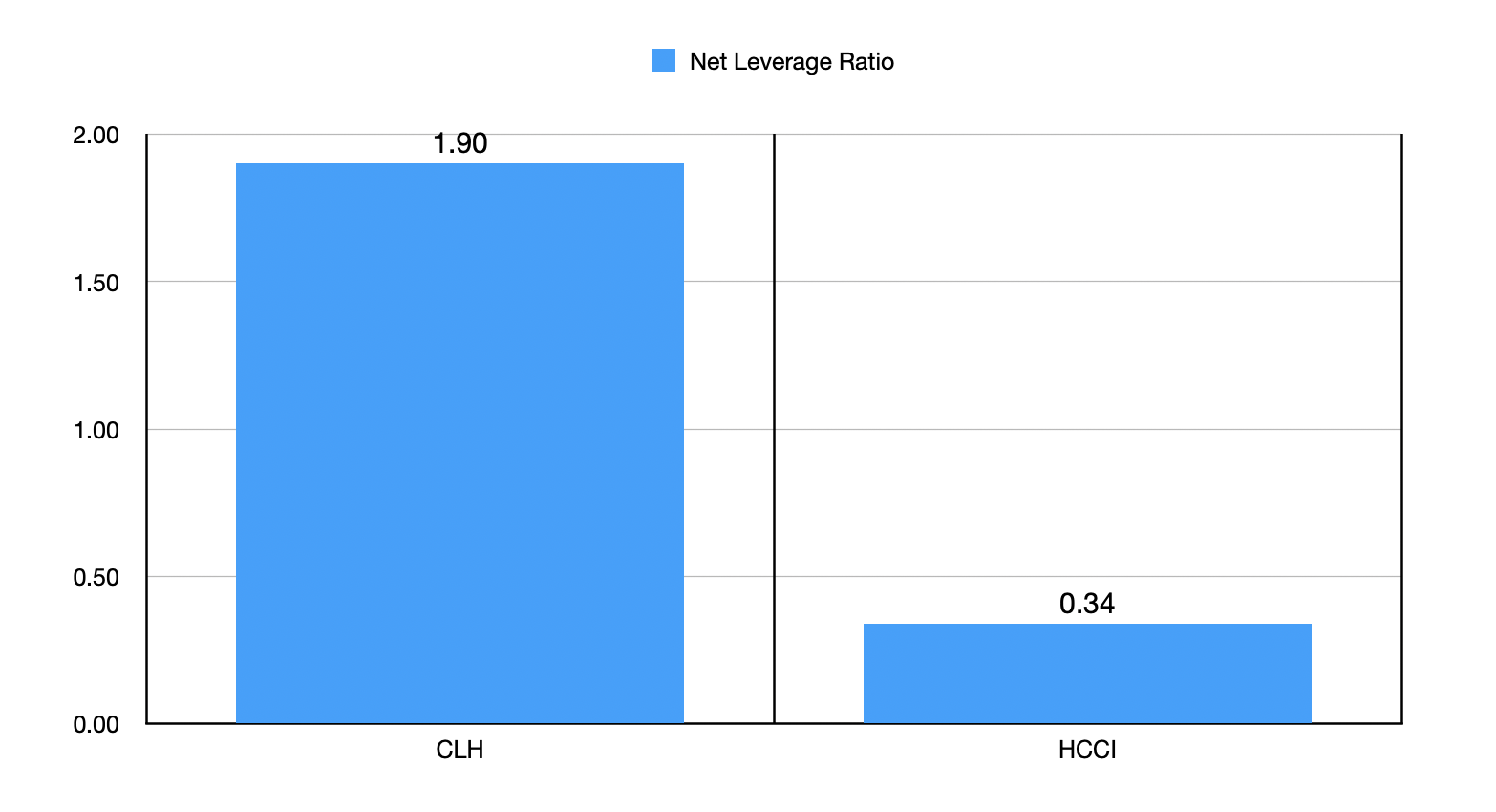

Although Heritage-Crystal Clean is a much smaller business than its rival, it is also far more profitable from a margin perspective. Using data from the most recent completed fiscal year, I was able to create the chart above. In every respect, Heritage-Crystal Clean achieved stronger margins than what Clean Harbors did. On top of this, the company is also significantly less leveraged. The net leverage ratio of it is 0.34 compared to the 1.90 that Clean Harbors posts. And this brings me into another reason why such a transaction would have been fantastic for shareholders of Clean Harbors.

{kind=link}

{kind=link}

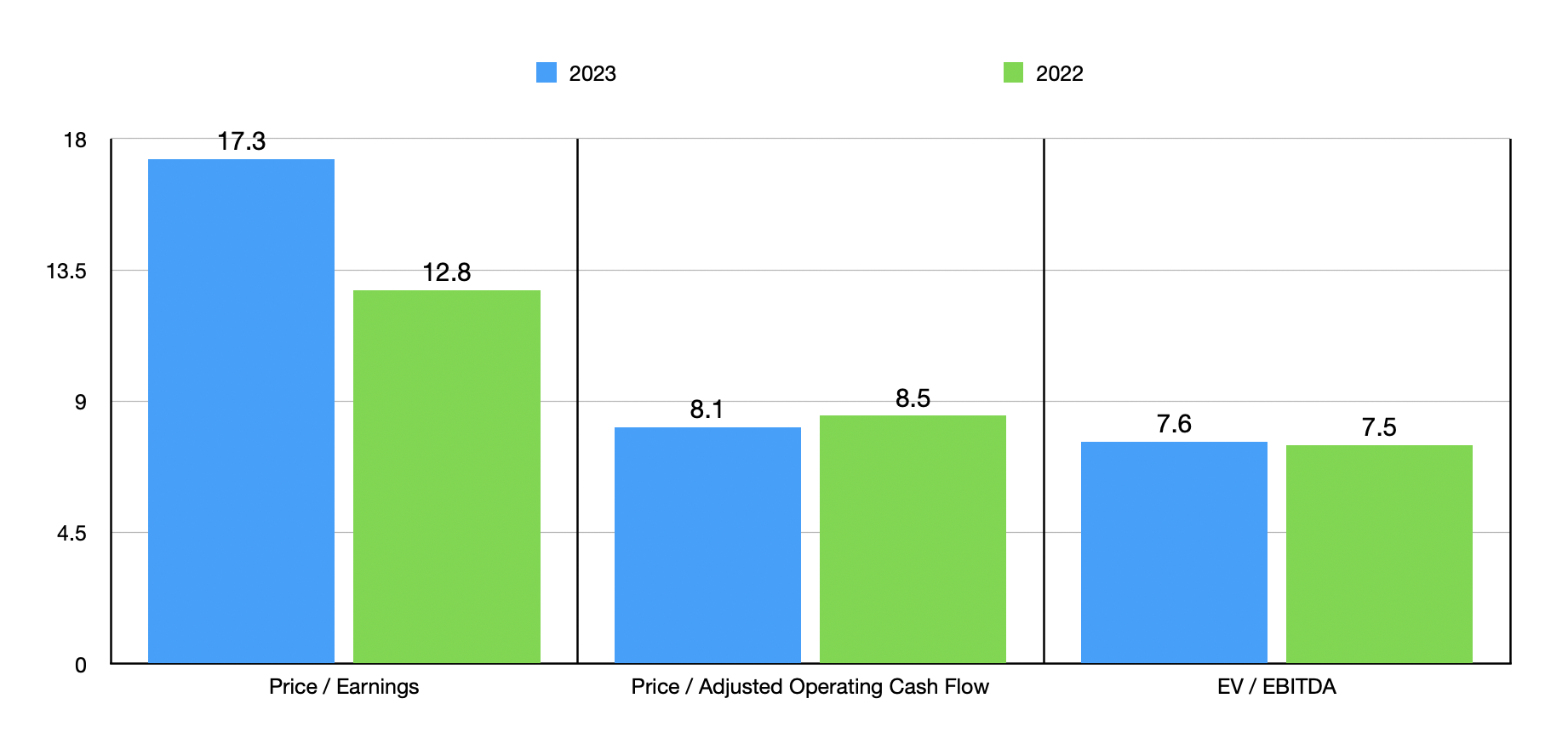

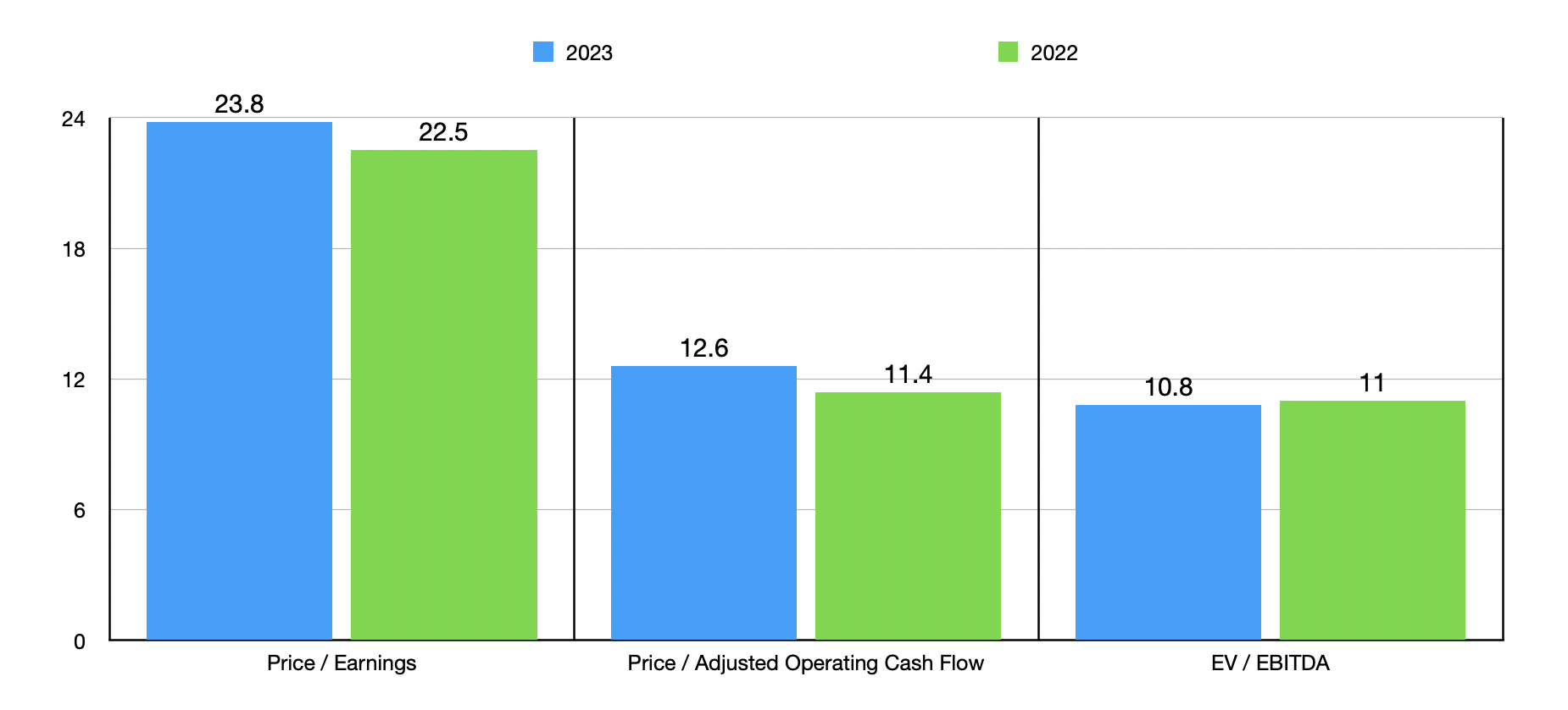

One could argue that Clean Harbors may not have wanted to take on the debt, given its net leverage ratio, to make a transaction happen. But the fact of the matter is that while Clean Harbors is fundamentally attractive from a valuation perspective, as indicated in the chart above, it is significantly more expensive than the buyout price for Heritage-Crystal Clean. In the chart below, I put just how cheap Heritage-Crystal Clean happens to be. Had Heritage-Crystal Clean elected to use all stock in its transaction, it would be essentially using more expensive shares to purchase cheaper shares. And to keep things simple, even if we just prioritize the price to earnings multiple for the 2023 fiscal year as forecasted, Clean Harbors could have put in a bid up to 37.6% above what J.F. Lehman & Company struck a deal to purchase the business for before it would be paying the same amount as what its own shares are trading at. And this ignores the prospect of synergies, so additional wiggle room could have been on the table.

{kind=link}

Takeaway

In my view, it was a major mistake for Clean Harbors not to make an all-stock bid on Heritage-Crystal Clean. The company had plenty of incentive to make such a transaction. Shares of Heritage-Crystal Clean are cheaper, the company is more profitable, and it is less leveraged than Clean Harbors happens to be. So long as the premium would not have been outrageous, shareholders of Clean Harbors almost certainly would have benefited. This doesn't change my previous bullish view on Clean Harbors, but it does dent my perception of management's capabilities. As for Heritage-Crystal Clean, the fact that the ‘go-shop’ period has come and gone now means that the $45.50 buyout price is what will ultimately happen. Compared to where shares are as of this writing, that leaves upside for holding the stock of only 1%. And considering that the transaction will not occur until sometime in the fourth quarter, I would argue that there are better places for shareholders in the company to put their money at this time.

For further details see:

Clean Harbors Missed Out Big On Heritage-Crystal Clean