RSG - Clean Harbors: My Bullish Assessment Unchanged

Summary

- Clean Harbors posted some robust financial figures since I last wrote about it, indicating that its health is still not an issue in this environment.

- Guidance revisions have been mixed, but shares still look cheaper than they would if we used data from 2021.

- On top of this, the stock is affordable compared to most of its peers and will likely fare well in the long run.

The fact of the matter is that there are some jobs some people just don't want to do. But for the right amount of money, you can get somebody to do some unsavory activities. A great example involves the ridding of both hazardous and non-hazardous waste. One company dedicated to precisely this type of activity is a firm called Clean Harbors ( CLH ). In addition to operating hazardous waste incinerators, landfills, and other similar environmental facilities, the company offers its customers certain industrial services such as industrial cleaning, specialty maintenance, and utilities services. You would think that in this current environment, customers would be looking for ways to cut back on costs such as these. But based on the data provided, the company is doing exceptionally well. Add on top of that how shares are priced at the moment, and I believe that the stock does offer some upside for investors from here.

Fundamentals are being ignored

The last article that I wrote about Clean Harbors was published in late October of 2022. At that time, I found myself impressed by how well the company was performing compared to the broader market. In addition to that, sales and profits were rising nicely. Add onto all of this the fact that shares of the company looked attractively priced at that time, and I believed then that shares should generate upside that exceeded with the broader market would achieve. This resulted in me rating the company a ‘buy’. In the short time that has passed since then, the market has not exactly cared about the fundamental condition or the pricing of the company. You see, while the S&P 500 is up 3%, shares of Clean Harbors have generated a loss for investors of 0.7%. Although this is disappointing, it should be mentioned that since my first bullish article on the company in November of 2021, shares of the business have achieved upside of 3.8% compared to the 13.6% decline the broader market experienced.

{kind=link}

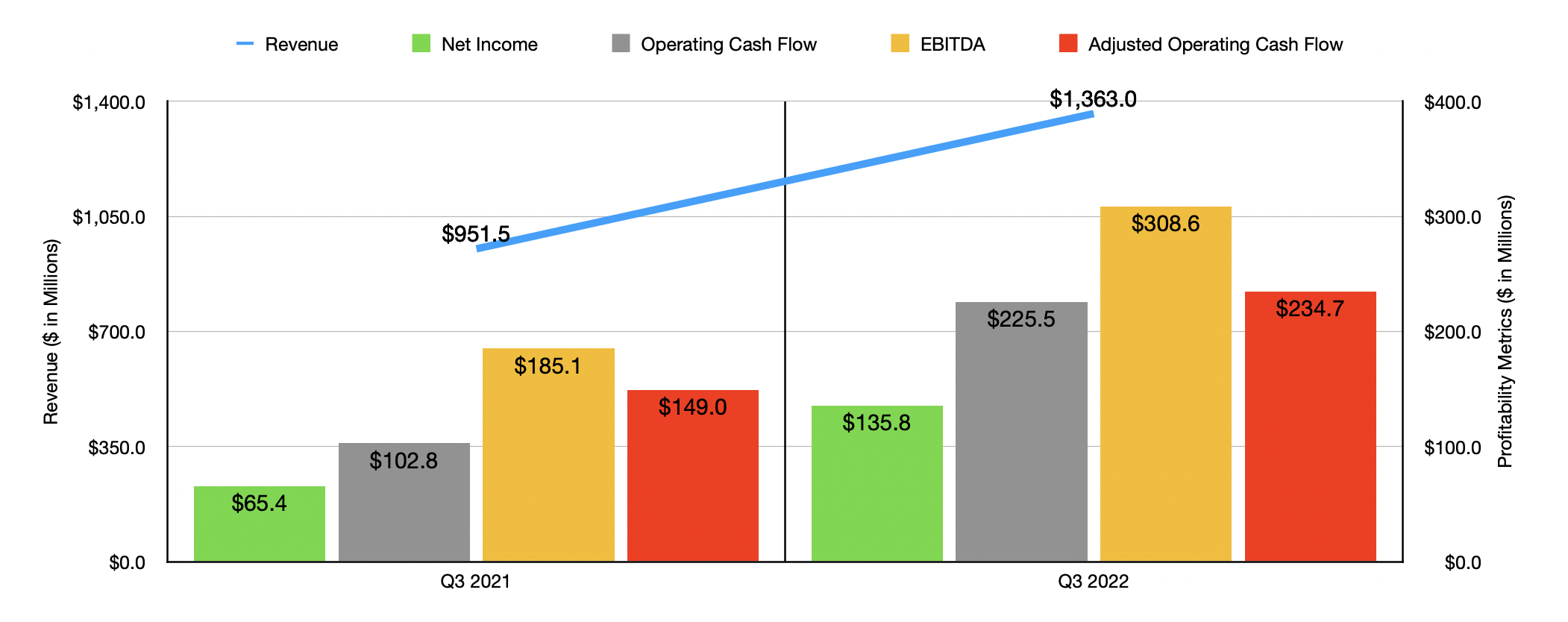

Interestingly, this return disparity since October has developed even at a time when fundamental performance achieved by the company has been very impressive. To see what I mean, we need only look at the third quarter of the company's 2022 fiscal year. This is the only quarter for which new data is available that was not available when I last wrote about the firm. During that time, sales came in at $1.36 billion. That's 43.2% higher than the $951.5 million reported the same time one year earlier. The primary driver behind this growth was the Environmental Services segment of the company, with revenue shooting up 45.7% year over year. According to management, this increase was driven mostly by the company's acquisition of HydroChemPSC. But this is not to say that all of its growth was driven by non-organic means. For instance, the company's technical services operations saw revenue jump 29.4% year over year, while its Safety-Kleen Environmental revenue stream increased 21.5%. The other segment the company has, called Safety-Kleen Sustainability Solutions, reported a 34.3% increase in sales, largely because of higher pricing of its base and blended oil products.

{kind=link}

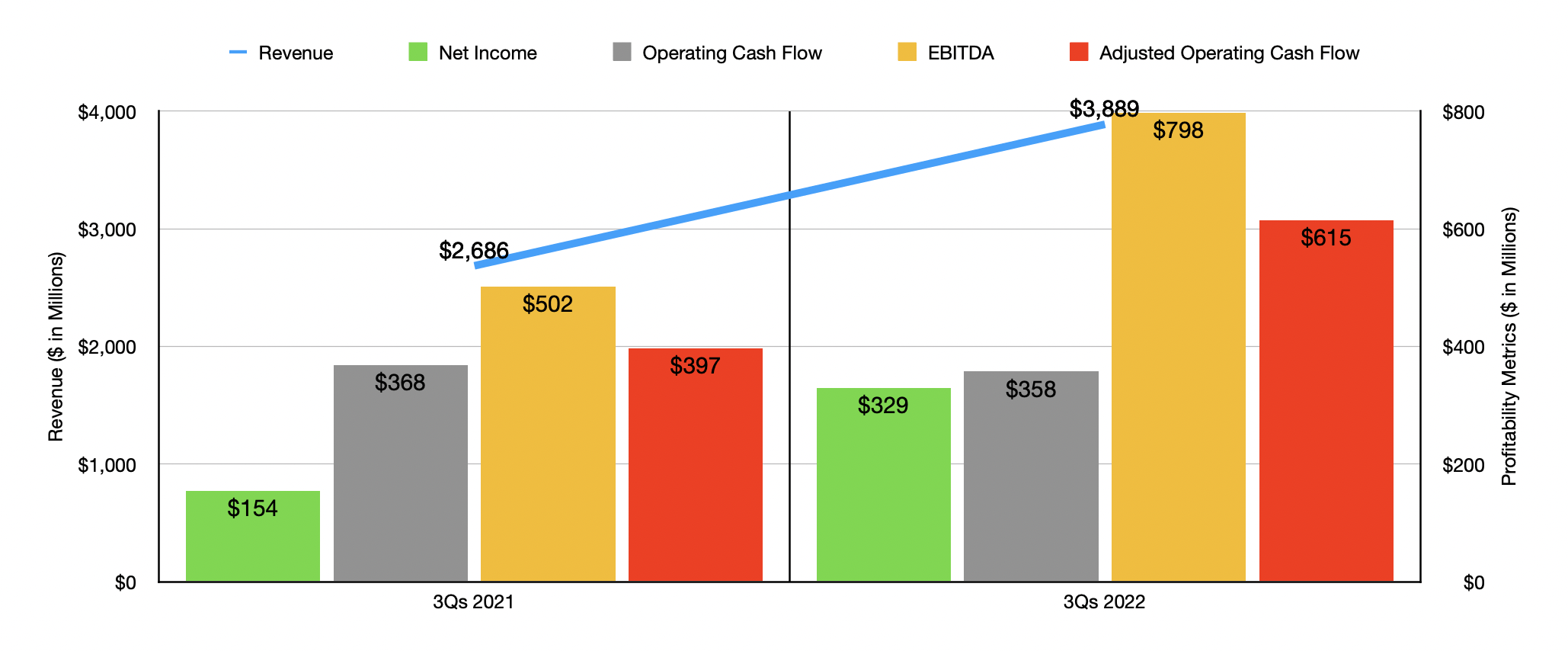

This increase in revenue brought with it drastically improved profitability. Net income more than doubled from $65.4 million to $135.8 million. Operating cash flow followed suit, shooting up from $102.8 million to $225.5 million, while this figure adjusted for changes in working capital grew from $149 million to $234.7 million. Another metric that also fared well during this time was EBITDA. Based on the data provided, it increased year over year, climbing from $185.1 million to $308.6 million. Thanks to the strong performance in the third quarter, results for the first nine months of 2022 as a whole remained strong compared to what they were one year earlier. Revenue of $3.89 billion beat out the $2.69 billion reported for the first nine months of 2021. Net income more than doubled from $154.3 million to $329.3 million. Operating cash flow actually did worsen, dropping from $368.2 million to $357.5 million. But if we adjust for changes in working capital, it would have risen from $396.6 million to $614.9 million, while EBITDA expanded from $502.3 million to $797.9 million.

{kind=link}

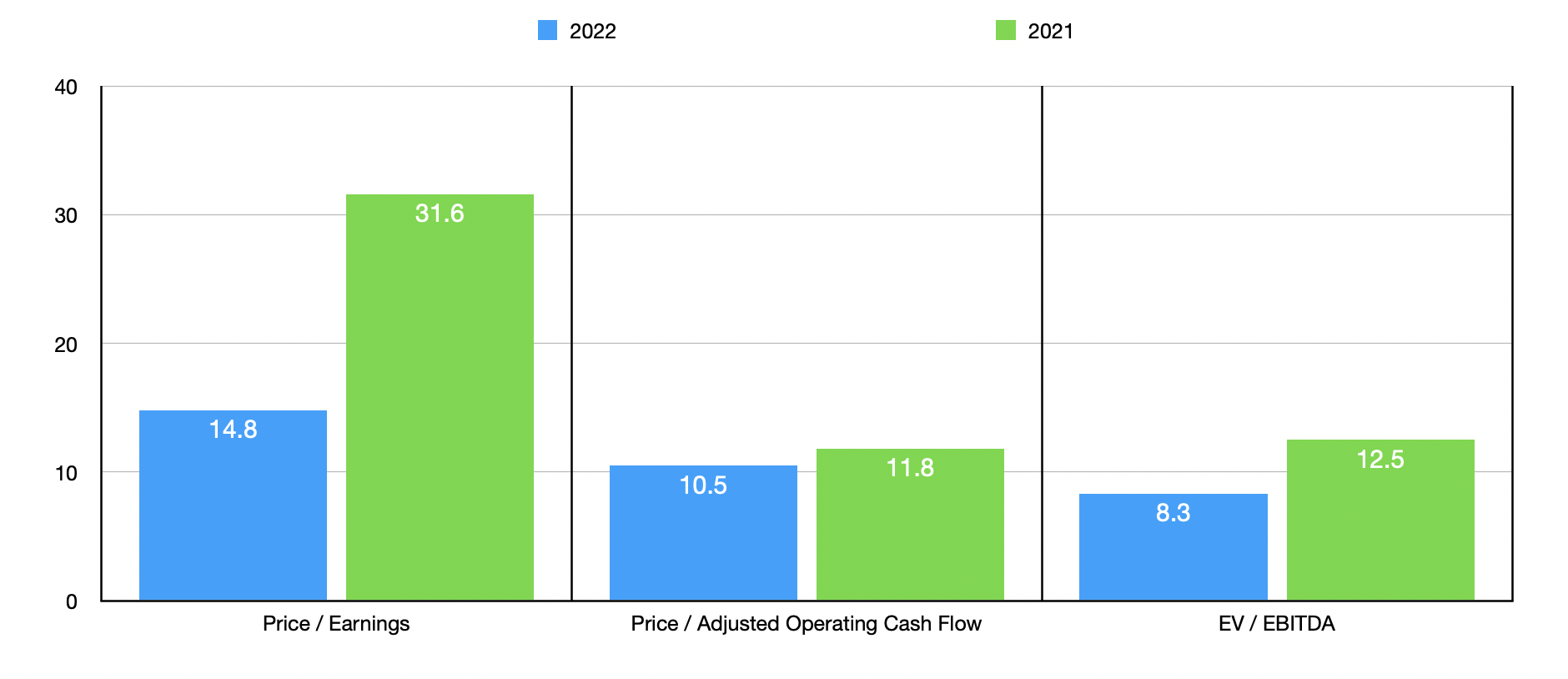

When it comes to the 2022 fiscal year in its entirety, management has said that operating cash flow should be between $585 million and $635 million. Unfortunately, this is lower than their prior expected range of between $630 million and $690 million. On the other hand, the expectations for EBITDA improved, with the metric now forecasted to come in at between $1.01 billion and $1.03 billion. No guidance was given when it came to net income. But if we annualize results experienced so far, we would anticipate a reading of $433.7 million for the year. Based on this estimate, the company would be trading at a price-to-earnings multiple of 14.8. That's down considerably from the 31.6 reading that we get using data from 2021. The price to operating cash flow multiple should drop from 11.8 using data from 2021 to 10.5 using our current forecasts for 2022. Meanwhile, the EV to EBITDA Multiple should drop from 12.5 to 8.3. As part of my analysis, I also compared the company to five similar firms. These are companies either engaged in waste disposal or firms that provide other facilities services. On a price-to-earnings basis, these companies ranged from a low of 10.7 to a high of 77.5. And when it comes to the EV to EBITDA approach, the range should be from 6.8 to 20. In both of these cases, only one of the five companies was cheaper than our prospect. And finally, when it comes to the price to operating cash flow approach, the range should be from 8 to 49.6, with two of the firms being cheaper than Clean Harbors.

| Company |

| Price / Earnings |

| Price / Operating Cash Flow |

| EV / EBITDA |

| Clean Harbors |

| 14.8 |

| 10.5 |

| 8.3 |

| Quest Resource Holding Corp ( QRHC ) |

| 77.5 |

| 49.6 |

| 14.9 |

| Heritage-Crystal Clean ( HCCI ) |

| 10.7 |

| 9.3 |

| 6.8 |

| SP Plus Corporation ( SP ) |

| 16.0 |

| 8.0 |

| 9.9 |

| Republic Services ( RSG ) |

| 27.0 |

| 12.9 |

| 14.5 |

| Tetra Tech ( TTEK ) |

| 30.3 |

| 23.7 |

| 20.0 |

Takeaway

From what I can see, Clean Harbors remains a solid prospect that is doing quite well for itself. Thanks to both organic growth and the aforementioned acquisition the company engaged in, revenue, profits, and cash flows have all been rising nicely. Shares are not the cheapest I have seen. But they are still cheap enough, in my opinion, for the firm to be rated a ‘buy’ at this time.

For further details see:

Clean Harbors: My Bullish Assessment Unchanged