RSG - Clean Harbors: Shares Still Offer A Bit Of Upside Despite Its Massive Surge

2023-06-16 10:15:39 ET

Summary

- Clean Harbors, a facilities-related services provider, has experienced significant growth, with shares up 28.6% since January and 34.6% since November 2021.

- The company's Q1 2023 financial results show an 11.8% increase in sales, improved profitability, and strong performance in its Environmental Services operations.

- Despite an anticipated decline in some profitability metrics, Clean Harbors shares still appear undervalued, and the stock is considered a soft "buy" for those interested in the company and its industry.

One of the beautiful things about a company that is experiencing rapid growth is that, if shares were cheap previously, they might still be cheap after seeing a significant upside. A great example of this that I could point to is a company called Clean Harbors, Inc. ( CLH ). For those not familiar, the company provides a wide variety of facilities-related services such as industrial cleaning, specialty maintenance, and more. It also operates hazardous waste incinerators, landfills, and other similar environmental facilities. Even though this may not seem like a high growth area, management has done well to expand the company's top and bottom lines.

It is true that CLH stock is not quite as cheap as it was earlier this year. But in the grand scheme of things, I would argue that some additional upside is probably still on the table.

Great performance as of late

Back in the middle of January of this year, I found myself revisiting my bullish thesis on Clean Harbors. In that article , I talked about how the overall fundamental health of the company was continuing to impress me. Guidance revisions provided by management had been, unfortunately, mixed. But on the whole, shares looked cheap enough to warrant a degree of optimism. This led me to reassert my 'buy' rating on the stock, a rating that indicated my belief that shares should outperform the broader market for the foreseeable future.

Since then, things have gone remarkably well for CLH. Shares are up 28.6% compared to the 8.4% rise seen by the S&P 500 (SP500). And since I first rated the company a "buy" back in November 2021, shares have generated an upside of 34.6% compared to a 6.3% drop experienced by the S&P 500.

{kind=link}

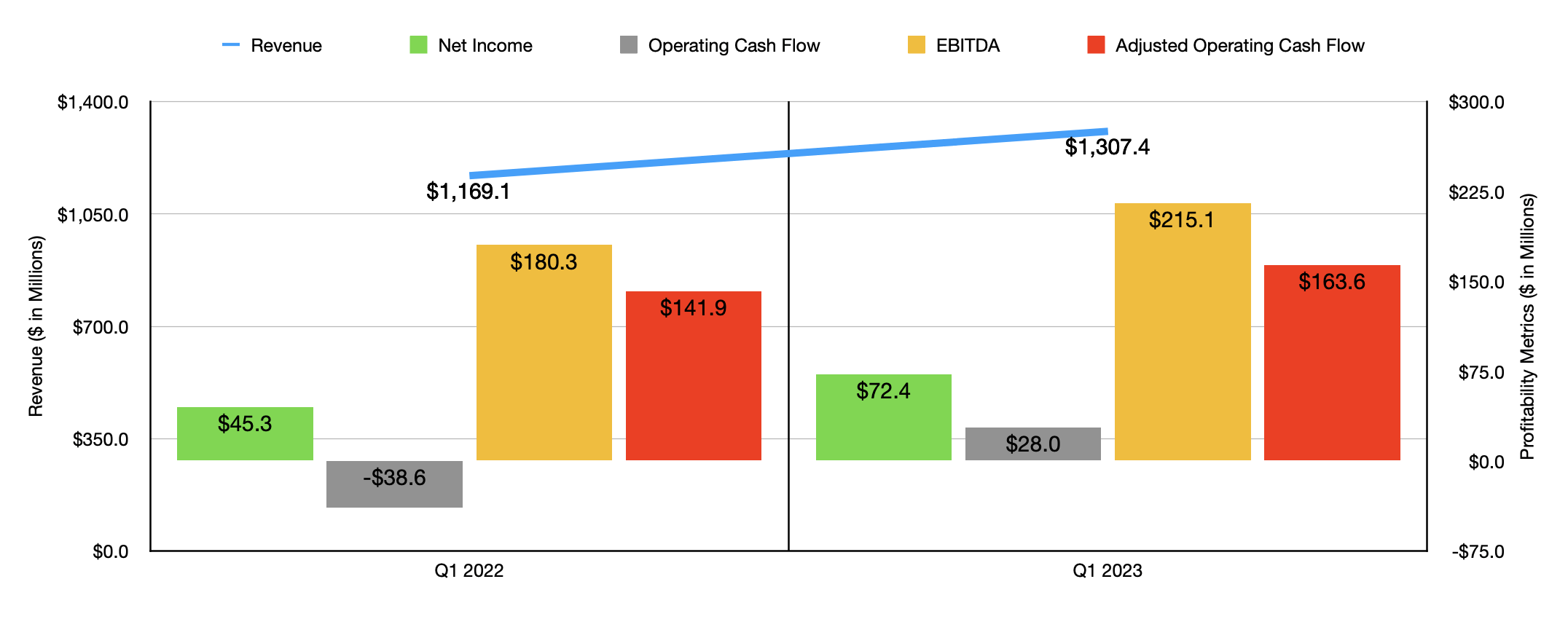

This return disparity is not, in my opinion, without cause. To see what I mean, we need only look at the most recent data covering the first quarter of the company's 2023 fiscal year. During that time, sales came in at $1.31 billion. That represents an increase of 11.8% over the $1.17 billion the company generated one year earlier. The most significant growth for the firm came from its Environmental Services operations. Revenue they are skyrocketed 13%, rising from $947.4 million to $1.07 billion. That increase, according to management, was driven largely by A $42.9 million rise associated with the technical services the company offers. Waste disposal facilities, driven by higher value waste streams and pricing initiatives implemented by management, were the big movers on this front. Results would have been even more impressive had it not been for certain unplanned outages at some of its incinerator and landfill facilities.

With the rise in revenue also came improved profitability. Net income of $72.4 million dwarfed the $45.3 million generated one year earlier. In addition to benefiting from the rise in revenue, the company also saw its overall cost of revenue grow rather modestly. Digging into the numbers, it saw environmental services cost of sales drop from 72.3% of their related revenue to 70.4%. Even though this may not sound like much, when applied to the amount of revenue the company generated in the first quarter, it translated to $20.3 million in additional pre-tax profits. Other profitability metrics followed suit. Operating cash flow, for instance, went from negative $38.6 million to positive $28 million. We would see this number rise from $141.9 million to $163.6 million if we adjust for changes in working capital. And finally, EBITDA for the company grew from $180.3 million to $215.1 million.

{kind=link}

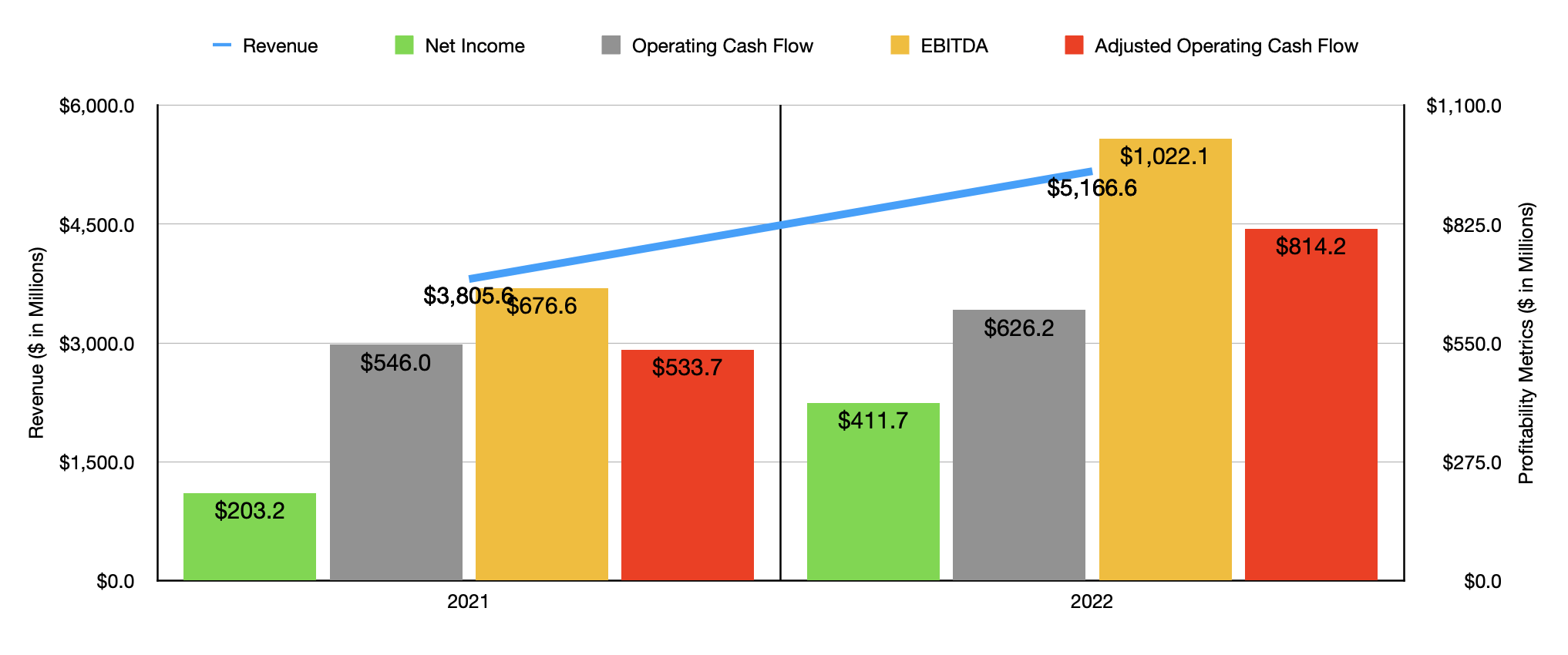

As you can see in the chart above, financial results for the first quarter of 2023 relative to the same time one year earlier were not a one-time event. Results in 2022 were, by every measure, substantially higher than with the company reported for 2021. But this doesn't necessarily mean that results will continue to be strong this year. Consider current guidance for 2023. At present, management is forecasting EBITDA of between $1.02 billion and $1.06 billion. This is slightly higher, at the midpoint, than the $1.02 billion reported for 2022. But unfortunately, other profitability metrics are expected to show signs of weakening. Net income, for instance, should come in at between $364 million and $400 million. Meanwhile, operating cash flow should be between $705 million and $765 million. Using midpoint figures, these estimates translate to $382 million and $735 million, respectively.

{kind=link}

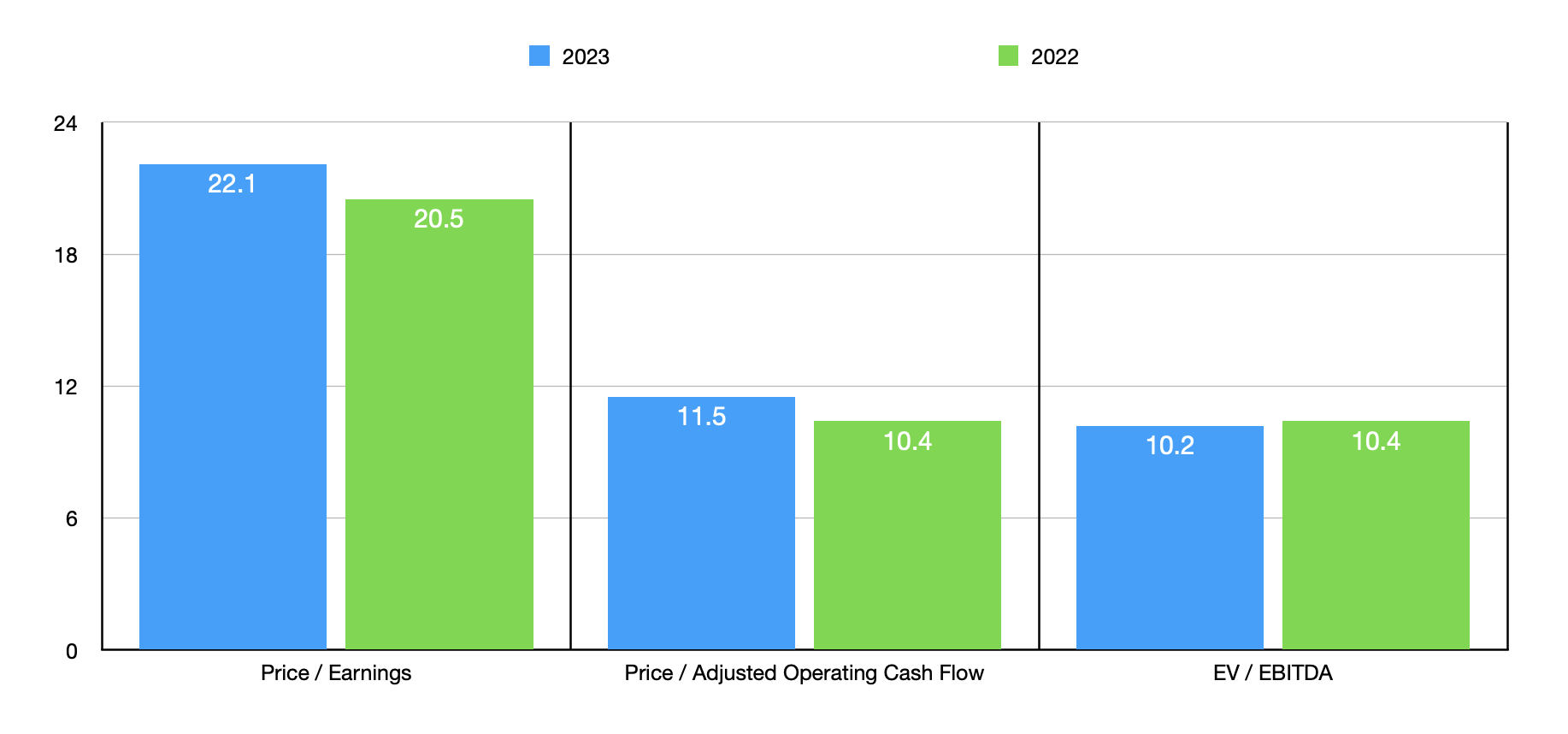

Even with this anticipated decline, shares of the business do not look pricey. In the chart above, you can see how shares are priced using the forward estimates for 2023. You can also see how the company is priced using data from 2022 as well. Using two of the three valuation approaches, the stock does look to be a bit more expensive. But in the grand scheme of things, I would argue that shares might still be a bit undervalued at this time. This is true also relative to similar firms. In the table below, you can see how I priced the company relative to five similar firms. On a price to earnings basis, two of the four companies with positive results were cheaper than Clean Harbors. And when it comes to the price to operating cash flow approach and the EV to EBITDA approach, two of the five companies ended up being cheaper than our target.

| Company |

| Price/Earnings |

| Price/Operating Cash Flow |

| EV/EBITDA |

| Clean Harbors |

| 22.1 |

| 11.5 |

| 10.2 |

| Quest Resource Holding Corporation ( QRHC ) |

| N/A |

| 115.7 |

| 13.7 |

| Heritage-Crystal Clean ( HCCI ) |

| 9.9 |

| 9.3 |

| 5.7 |

| SP Plus ( SP ) |

| 18.8 |

| 10.7 |

| 9.8 |

| Republic Services ( RSG ) |

| 30.0 |

| 14.4 |

| 15.0 |

| Tetra Tech ( TTEK ) |

| 27.9 |

| 31.0 |

| 19.2 |

Takeaway

From all that I can see right now, things are going quite well for Clean Harbors and its shareholders. Management has done a great job growing the company on both the top and bottom lines. This is especially true when you consider how strong 2022 was and, by definition, how difficult it should be to top such a strong year. Interestingly, management does seem to think that bottom line figures for this year will end up mixed relative to what the company saw last year. But even if that does come to pass, shares look attractively priced on a forward basis. They also, I would argue, look perhaps slightly undervalued relative to similar enterprises.

This is not to say that I expect another significant outperformance from Clean Harbors stock relative to the broader market. Rather, I would argue that upside from this point is more limited than it was earlier this year. But for those interested in this company and in this space, I would say that Clean Harbors, Inc. stock is still cheap enough to warrant a soft "buy" at this time.

For further details see:

Clean Harbors: Shares Still Offer A Bit Of Upside Despite Its Massive Surge