CLFD - Clearfield: Attractive Valuation With A Great Growth Story

- The acquisition of Nestor Cables to be a growth driver for CLFD in FY22.

- CLFD reported a solid Q2 2022, with a strong future outlook in terms of revenue growth and profit margin expansion.

- CLFD is currently undervalued on the basis of PEG ratio analysis and has a huge upside potential from current price level.

- I assign a buy rating for CLFD, with a target price of $95.

Investment Thesis

Clearfield, Inc. ( CLFD ) is a manufacturer of passive connectivity products. The company has recently acquired one Finnish company. I will be analyzing the effect of this acquisition on the operations and earnings of the company. I believe this acquisition will be a primary growth factor for the company as it will help the company to strengthen its position in the European market and make its operation efficient in North America. The company has also shown accelerated growth in the past year. I will also be analyzing the sustainability of high growth rates in future with this acquisition.

Company Overview

Clearfield, Inc. is a manufacturer and distributor of fiber protection, fiber delivery and fiber management products and services which are used to provide fast gigabit-speed bandwidth to residential houses, companies, and network infrastructure. The company is currently targeting five markets: Fiber to the Home (FTTH), Business Services, Wireless, Multiple Dwelling Units (MDUs) and Multiple Tenant Units (MTUs).

{kind=link}

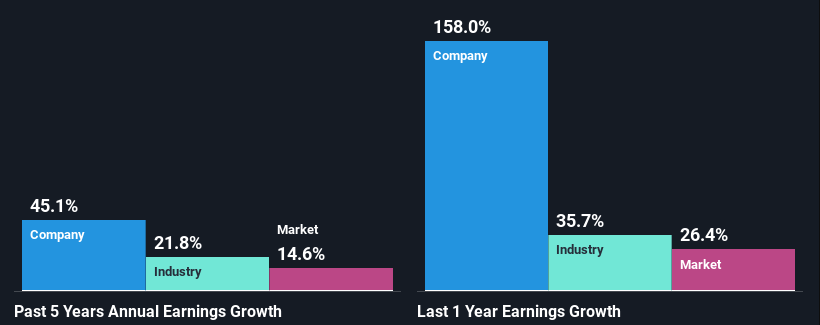

The company has been able to grow its revenue at 45.1% CAGR in the last five years when the communication industry's earnings have only increased by 21.8%. Last year, the company accelerated growth by exceeding its 5-year average growth (45.1%) with a robust growth rate of 158%. The company has given a 26.9% return on equity which is almost double as compared to the industry average of 13.9%. It has also achieved a strong return of capital employed ratio of 31.2%. I believe the company will be able to keep this growth spree in the coming years with the acquisition of Nestor Cables, as it will strengthen the position of the company in the European market. This acquisition will also add a revenue stream of $31.8 million to the company's financials.

Acquisition of Nestor Cables

Recently, the company announced the acquisition of Finnish company Nestor Cables Oy, a fiber optic cable producer. As a provider of optical fiber cabling, Nestor possesses a strong market position in Finland. The company also exports a large number of its goods to Europe, which accounts for about 30% of its annual sales. With customers in more than 50 countries, Nestor runs two production sites. In FY2021, Nestor generated $31.8 million in revenue, and CLFD bought it for $23 million, which is 0.72x of its net sales. I believe 0.72x is a very low sales multiple, making this deal very cheap for CLFD. This was about the financial rationale of the agreement; now, let's discuss qualitative information about the deal.

CLFD will be able to vertically integrate the supply of its fiber optic cables thanks to this strategic acquisition in order to fulfil rising client demand. Additionally, the company expects to increase the supply of FieldShield fiber in the North American market by utilizing the Nestor team's extensive technical know-how and decades of optical experience. The company anticipates starting optical cable production in North America in the first quarter of FY2023 and opening optical fiber production in its facility in Mexico. I think this deal will optimize the company's operations in North America and help the company increase its presence in the European market. I also believe this deal will act as a strong growth factor for the company's earnings in FY2022 and FY2023.

Cheri Beranek, President and CEO CLFD, stated -

The acquisition of Nestor is a significant milestone for Clearfield. Nestor has been a wonderful company to work with over the last 10 years, and we are thrilled to be adding them to our team. Nestor's focus on providing its customers with reliable and flexible deliveries, quick reaction times, and operational efficiency is entirely aligned with Clearfield's company culture. We are excited for the potential opportunities afforded by this acquisition, namely the ability to leverage their fiber optic cable expertise in our own manufacturing facility in Mexico and, in the longer term, evaluate the opportunity to enter the European market with our fiber management solutions.

Financials

SEC:10Q CLFD

CLFD reported Q2 2022 net sales at $ 53.49 million , a significant 80% jump as compared to Q2 2021 net sales of $29.69. The main revenue driver was a 94% increase in the community broadband revenue as compared to Q2 2021. The gross profit margins were stable at 43.3% of the net sales. The gross margins remained stable despite rising inflation due to a compelling product mix and gradual price rise. The company reported a net income of $9.23, an astounding 153.7% increase compared to $3.64 million in the year-ago period. The diluted EPS for Q2 2022 was $0.66 compared to $0.27 in the corresponding quarter last year. I believe this overall growth in all segments will continue in the rest of FY22 with the latest acquisition. The company has also provided a robust future outlook, with estimated FY22 net sales revenue in the range of $204-$218 million, an effective growth of 45%-55% as compared to FY21. As per my analysis, the net could be even higher and touch $225 million, with a revenue boost from the acquisition of Nestor Cable and a strong order pipeline.

CLFD President and CEO Cheri Beranek, stated,

Clearfield continues to execute in an environment in which demand is accelerating. This quarter we both achieved record revenue and increased our order backlog. With the current visibility into our substantial order backlog, the majority of which is scheduled to ship in the next six months, and the pipeline behind it, we are raising our fiscal year 2022 net sales guidance from a range of $177 to $183 million to a range of $204 million to $218 million.

{kind=link}

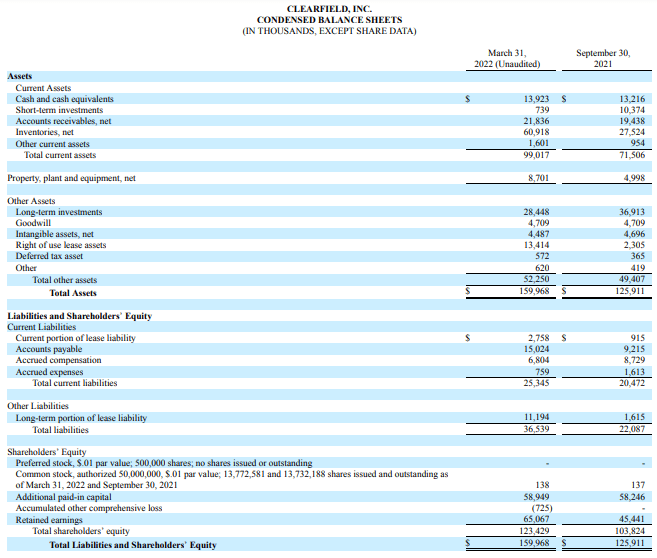

The company has cash and cash equivalents of $13.9 million as of 31st March 2022. The inventory saw a steep spike from $27.5 million to $60.8 million. The main reason behind this is the robust demand and a strong order pipeline that the company plans to execute. The company doesn't have any long-term debt, making the balance sheet solid. The company has the scope of raising funds in future in the form of debt without putting much stress on its balance sheet.

Overall, I believe the company posted a strong quarterly result, and the growth will likely continue for the rest of FY22. As per my analysis, the company has a really strong balance sheet and future scope for raising funds to continue this growth trajectory.

Risk Factor

Limited Source Suppliers: The company relies on third-party suppliers for some of its most essential components like injected molded parts, cables and connectors. These third-party suppliers are mostly single source or limited source suppliers. This makes the company highly dependent on these suppliers, as even if a single supplier is unable to supply a particular component, the operations are seriously affected. In case of a supply chain disruption that the company faced in FY21, the cost of acquiring the components increased drastically, putting pressure on the firm's profit margins. The company has been successful in managing this risk till now, but it is important for the firm to increase its supplier options to safeguard itself from supply issues in future.

Quant Ratings and Valuation

Seeking Alpha

The Quant Ratings of a strong buy on CLFD align with my thesis and recommendation of a buy on the company. I want to highlight the industry ranking of 2 out of 52 companies. This reflects that CLFD is one of the best opportunities in the communication equipment space. Wall Street is also bullish on the stock with a strong buy rating. All these factors further strengthen my thesis of a huge growth opportunity for CLFD from current levels.

{kind=link}

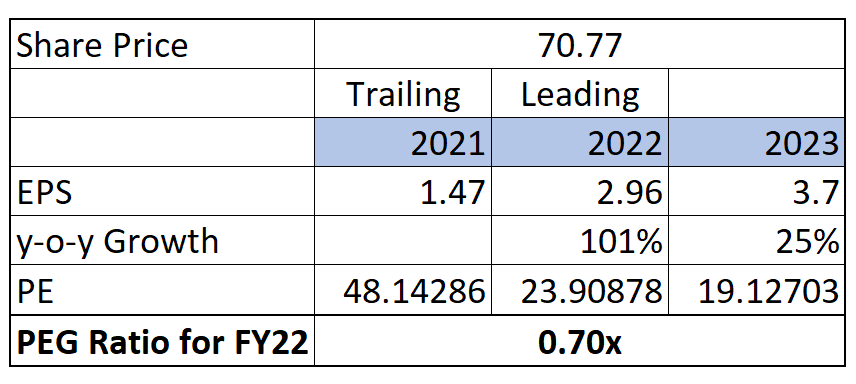

CLFD has a market cap of $996.52 million. The stock is currently trading at $70.77, a YTD decline of 11.84%. The company is trading at a leading PE multiple of 23.9x with the EPS estimate of FY22 at $2.96. The company might seem expensive in terms of PE multiple, but if we calculate the PEG ratio for the stock, we realize that the company is undervalued with a PEG ratio of 0.70x. A PEG multiple of 1x or lower for growth companies is considered good and reflects that the company is undervalued. I believe the company has a 34% upside potential from current levels with a PE estimate of 32x and a target price of $95.

Conclusion

CLFD has shown significant growth in FY22 in terms of revenue and profit margins. I believe going ahead, we will see the impact of the Nestor Cable acquisition that will maintain the growth trajectory of the firm in the near future. The company is undervalued in terms of PEG multiple, and I think we will see a significant upside from current price levels in the future. After analyzing the firm's financial statements and considering all the growth and risk factors, I assign a buy rating for CLFD.

For further details see:

Clearfield: Attractive Valuation With A Great Growth Story