CLFD - Clearfield: Being Greedy When Others Are Fearful

2023-10-24 00:15:23 ET

Summary

- Clearfield experienced a significant run-up in stock price fueled by strong growth and optimistic guidance, but has since seen a steep decline.

- Despite the recent downturn, Clearfield's core business and offerings remain strong, with potential for growth in rural broadband and 5G markets.

- The company's management had executed a masterstroke by raising cash and beefing up its balance sheet at the right time.

- The stock is currently attractively priced, presenting a buying opportunity for investors who believe in the company's long-term potential.

- I present three ways an investor can warm up to the stock if there is any fear in the short-term price movement.

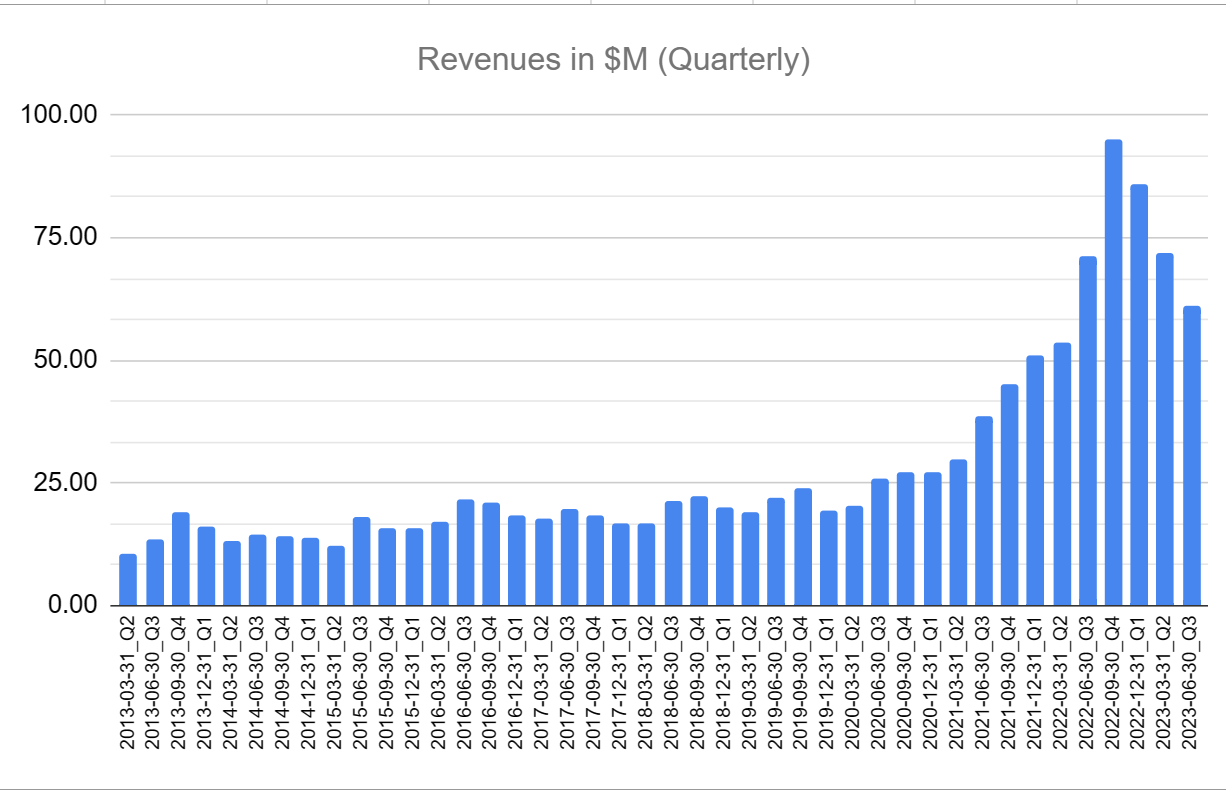

Clearfield ( CLFD ) had one of the wildest run-ups in recent history and I think it's a prime example of investors running ahead of the stock. The company's offerings were straightforward. It is a provider of communication equipment and was a big beneficiary of the optic fiber rollout. But its growth and guidance sent the investors into a frenzy. From early 2020 to late 2022, the stock moved approximately 900% while revenues grew around 200% .

Their guidance for 2023 was lofty at 40% which got investors even more excited about their prospects. Clearly, no heed was paid to valuation, pricing the stock for perfection.

As the year passed by the stock price cratered, with every quarter presenting a more humbling version of reality with sales not matching up with earlier expectations. The stock price was quickly catching up with the valuation and has fallen more than 80% from its highs presently. Investors who were too caught up with the future instead of valuing the company with the information available till then paid dearly.

In the business world, the rearview mirror is always clearer than the windshield

-Warren Buffet

I think we have been provided with a second opportunity. We can consider all the previous excitement and letdowns as pure noise, view this company impartially based on how well they have done so far, and this time not value them for perfection but on a range of scenarios. Based on my analysis of the company's strength and their journey and what lies ahead for them, I believe this company is a Buy .

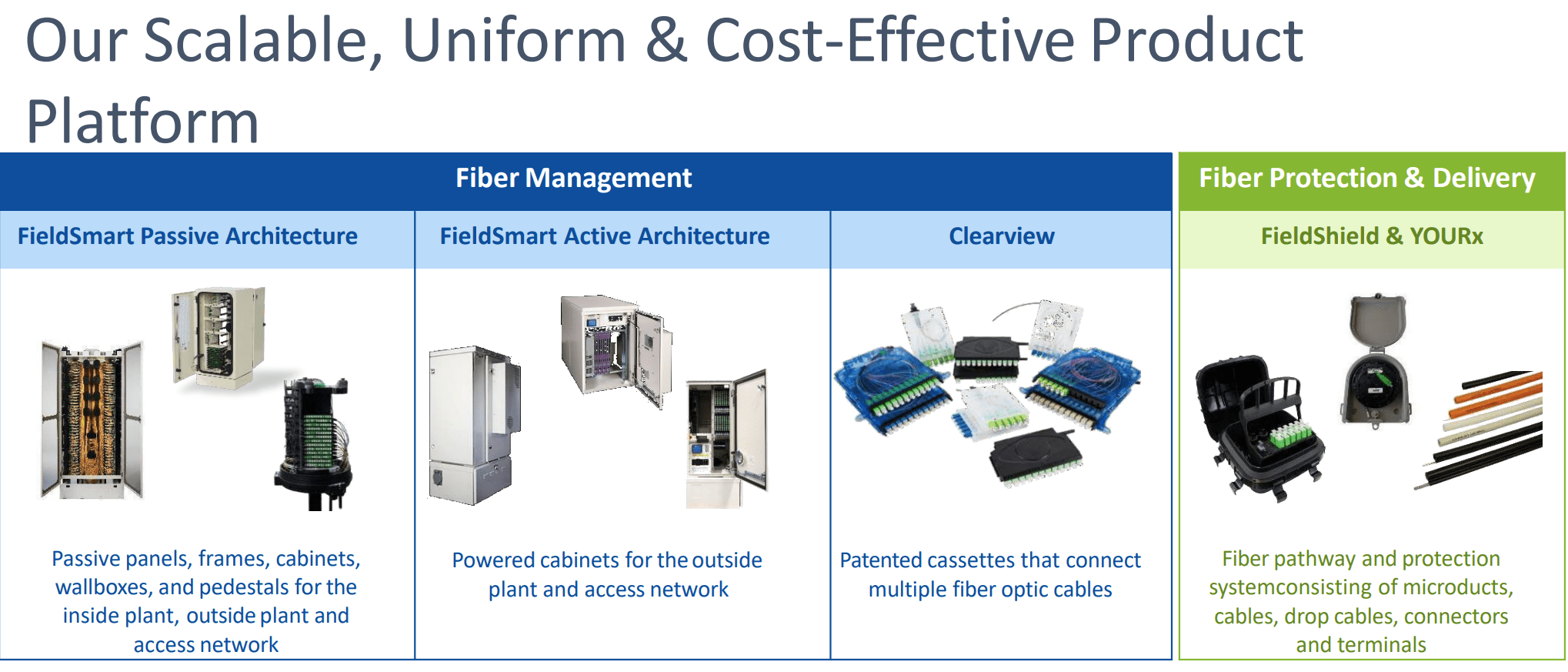

Clearfield's Business

Clearfield, Inc. is a company that specializes in fiber management and connectivity solutions for communications networks. Their business revolves around providing a wide range of products and services that enable network operators to efficiently deploy, manage, and expand fiber optic networks. Clearfield's solutions encompass fiber panels, cabinets, and optical components, designed to streamline fiber deployment and minimize the cost and complexity of fiber management. They cater to a variety of industries, including telecommunications, broadband, utilities, and more, offering vital infrastructure support to meet the growing demand for high-speed connectivity.

{kind=link}

Mean reverting growth

{kind=link}

2022 was a record year for multiple reasons (mostly short-term) and any revenue comparison from this quarter with 2022 will show us shrinking growth. I believe this comparison would be unfair as the demand for the company's products still exists and it has not lost any of its competitive advantage. So both their growth rate and profitability when looking at a longer time horizon should still be intact.

{kind=link}

2022 was a clear outlier as a lot of the demand was pulled forward and the stock price overshot to the upside. Now the overshot is to the downside but outside of the short-term correction to the demand, none of their key advantages have changed. In fact, their recent acquisition of Nestor Cables reaffirms their strategic outlook by optimizing their operations and mitigating supply chain risks. Their primary focus remains on providing a comprehensive solution that not only reduces installation costs and maintenance time but also enhances the total cost of ownership. Their trademarked FastPass approach has proven to cut the installation time required for homes by 50%, ensuring a swift, cost-effective, and hassle-free deployment.

So all in all, outside of the short-term macro headwinds, their core business and their offerings are still strong!

Where will the future growth come from?

The potential for future growth is large and the company can look at two main avenues to drive its growth.

Rural Broadband

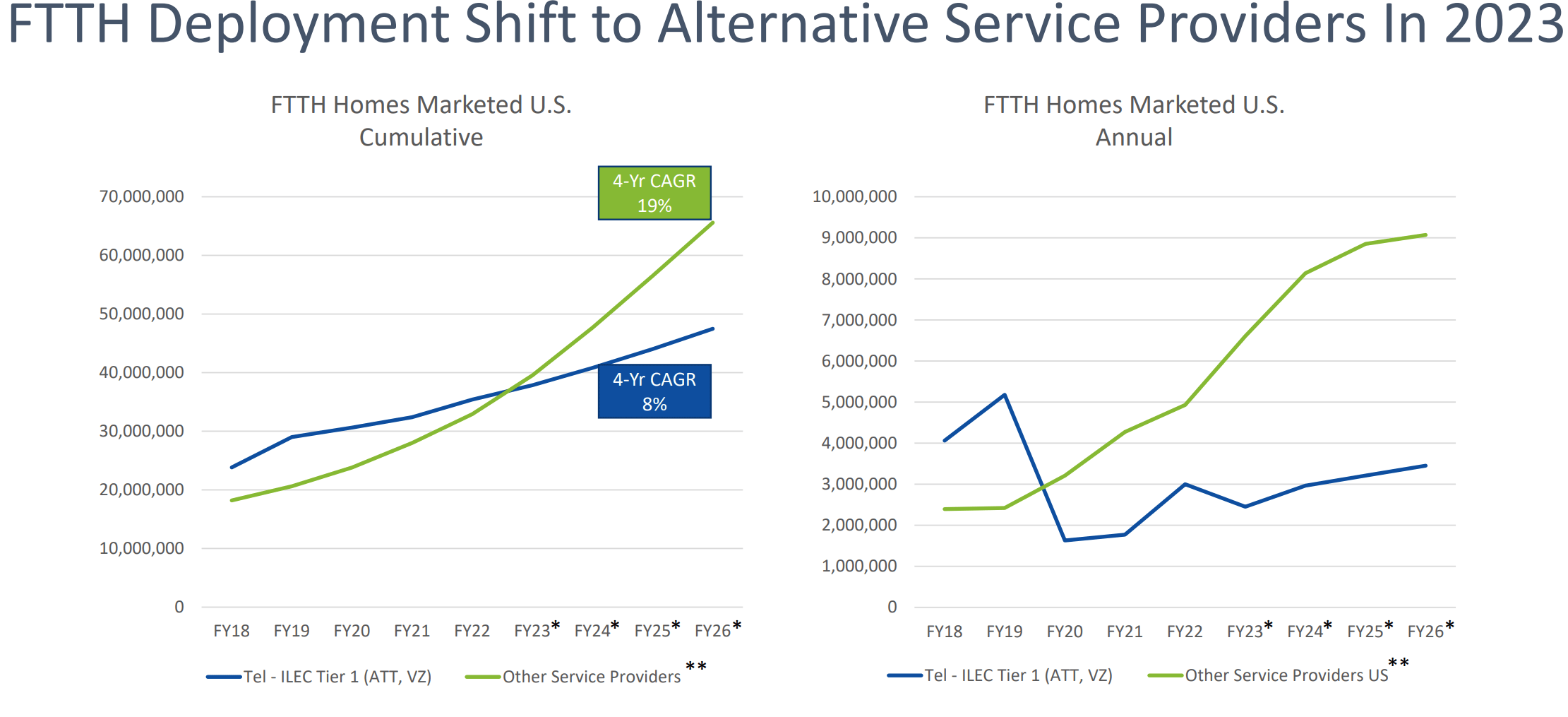

The US fiber-to-the-home (FTTH) market is anticipated to reach over $12.5B and there are commitments to pass roughly 55M homes with fiber by the year 2030. The Biden Infrastructure Package allocates a substantial 100 billion dollars for broadband initiatives, along with over 10 billion dollars in annual subsidies for broadband infrastructure over the next three years. The Biden Administration also aims for complete broadband coverage, targeting 100% across the nation by 2030. Its leadership position here makes it a prime candidate to capture an underserved rural broadband market.

{kind=link}

5G

Community broadband serves as the crucial infrastructure supporting 5G, capitalizing on the concept of One-Fiber for diverse deployments. Clearfield's current product range is strategically positioned to align with the substantial investment phase of 5G and there is an estimated cumulative spending of approximately 200 billion dollars on the 5G cycle by 2035. Their products can seamlessly extend into wireless networks for the implementation of 5G, effectively leveraging Clearfield's expertise in fiber management for this technology. Clearfield has a distinctive entry point into this landscape, with the next three years being pivotal for establishing a foothold in the 5G sector. This investment coincides with Clearfield's Now of Age Plan, which aims to eliminate barriers to integrating wireline and wireless networks.

Company Health and the management's masterstroke

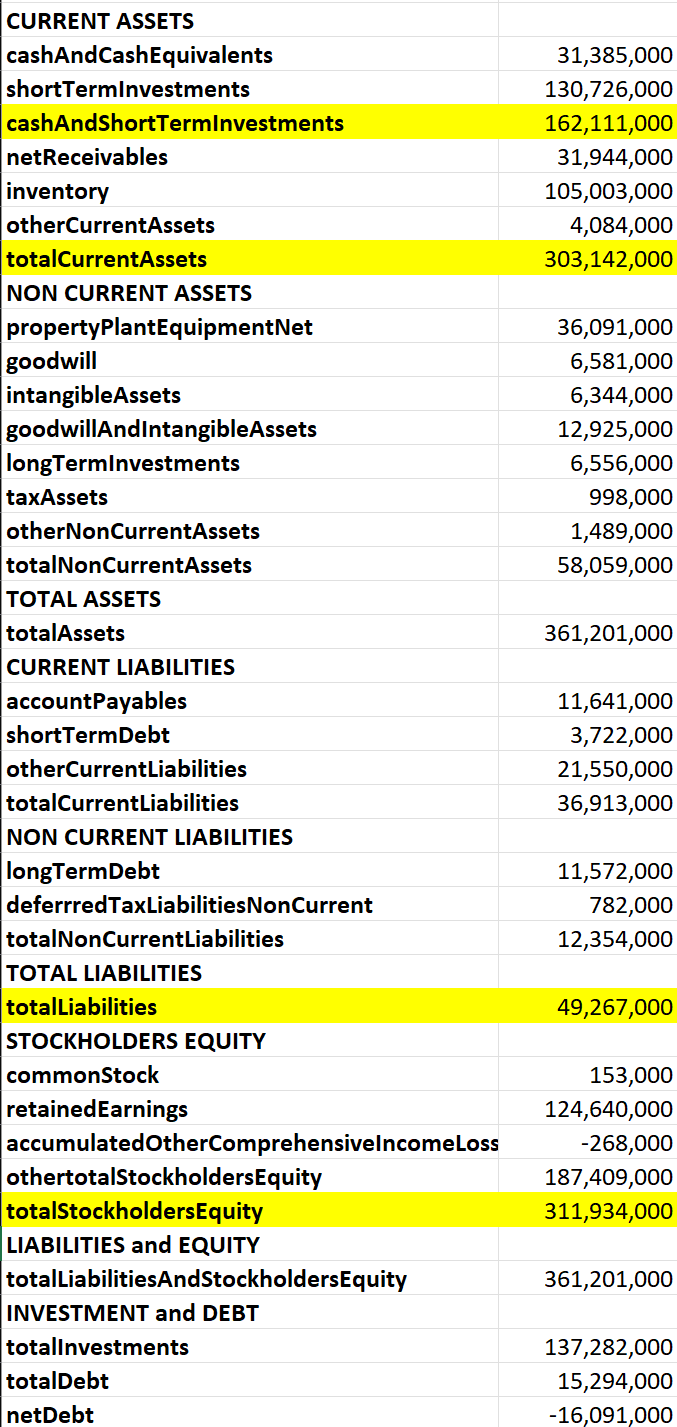

The way the stock price is tanking, it is easy to mix up this company with hundreds of other small caps that are struggling with their balance sheet. The company carries $160M of liquidity which completely covers all their liabilities. Since their debt is so low, we practically do not have to worry about their debt coverage from its cash flows. This is good for us due to their operational cash flows not being something to write home about until recently.

Balance Sheet for the latest quarter (FMP)

{kind=link}

So how did the company end up with so much cash? This is where the management executed its masterstroke . At its height of valuation (late 2022), the company raised serious cash ( $130M ) through the issuance of stock. In hindsight, the timing of the stock sale looks brilliant as the company was able to not only beef up its balance sheet but also pay down the debt from its acquisition of Nestor cables (The same move at any other time in the company's history would not have yielded the same results as it would have to issue a lot more stock to raise the same amount of cash). The same cash is also now earning interest income!

Net investment income for the nine months ended June 30, 2023, was $3,328,000 compared to $284,000 for the comparable quarter for fiscal 2022. The increase in interest income is due to higher interest rates earned and a higher average investment balance in the nine months ended June 30, 2023. The higher investment balance is a result of the Company’s capital raise of approximately $130,262,000 completed in the first fiscal quarter of 2023.

All of this means the company's health is not only rock-solid but also its moves at the peak of its stock price will continue to pay dividends in the future.

The value argument

As we mentioned earlier, the stock's deep correction means it is attractively priced now (PE of 8x). This is a big change from the high valuations that we were seeing just two years ago. Again, this was due to investors running ahead of the stock and pricing it for perfection.

Now that the growth is starting to normalize, I believe the market's reaction has provided us with an opportunity to get in at a much better price. Certainly, if you liked this business then, you will love this business now!

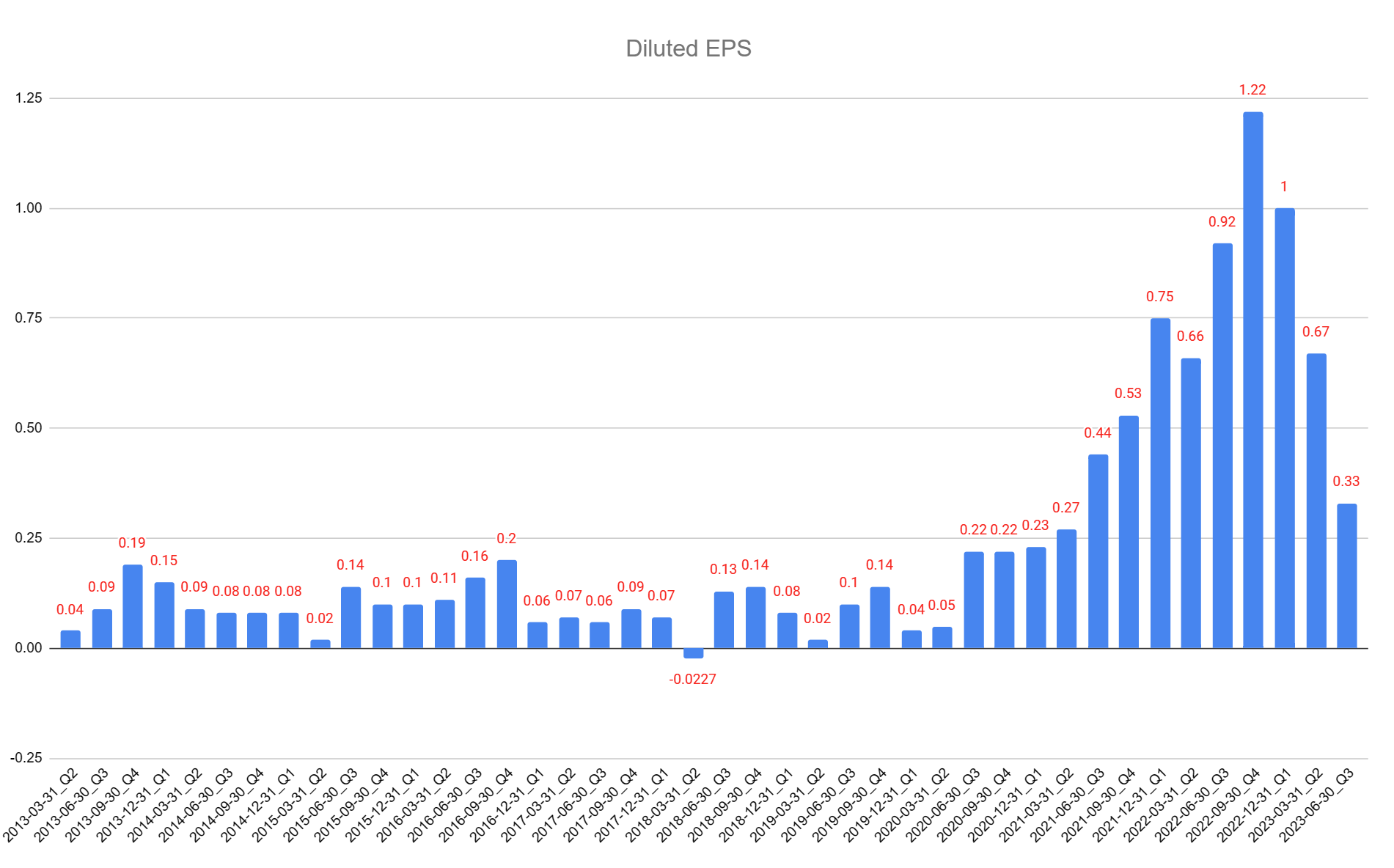

But what does the future look like? For FY23 it has guided EPS of $2.05 - $2.15 which is massively down from FY22 ($3.55). But this is still showing an increase from 2021 which came in at $1.47. Will it show growth in 2024? If we do believe their potential for growth will come from underserved rural broadband areas, 5G technology, and their expansion into Europe (helped by their Nestor cables acquisition) we are dealing with multiple factors that can boost both the top and bottom line.

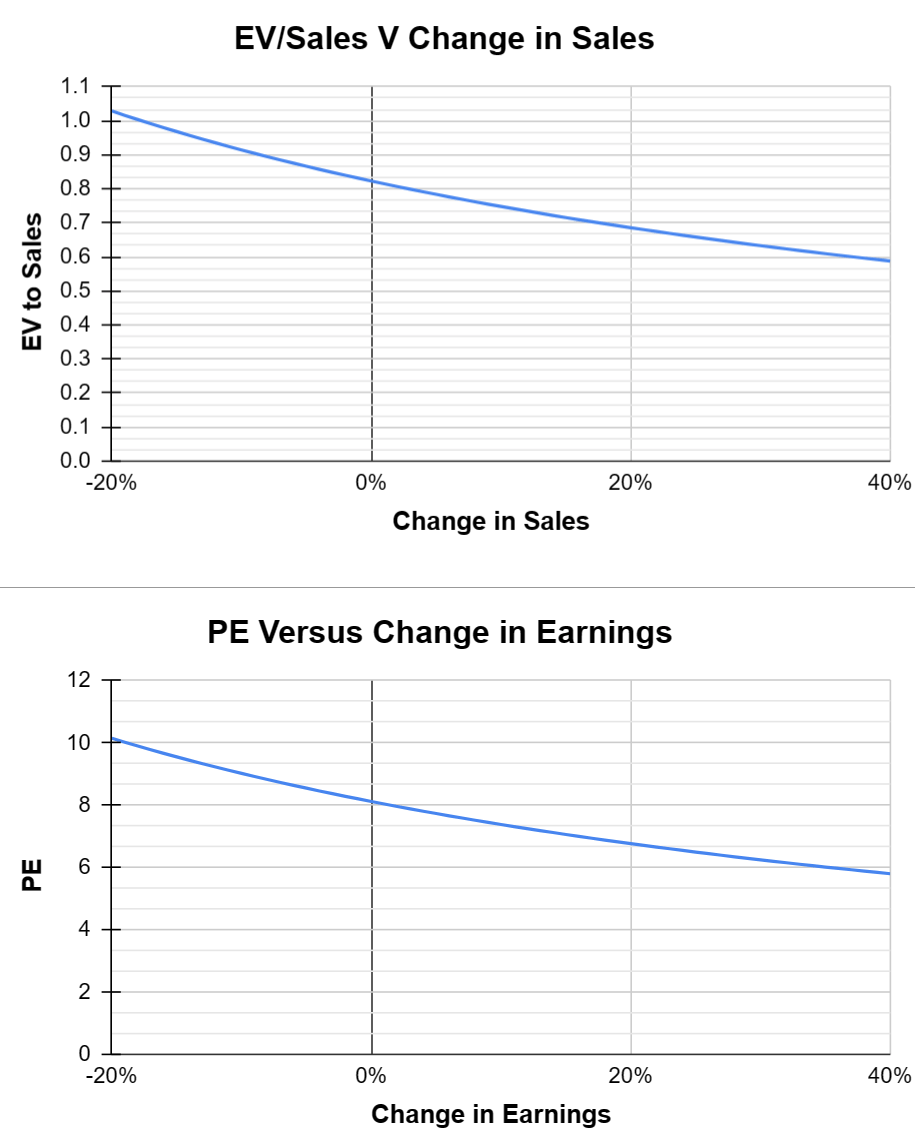

Scenario based Forward Valuations (Author Computed from Company Data)

{kind=link}

In the worst-case scenario where their earnings and sales tank by up to 20%, we see EV/Sales and PE multiple inflate to 1x and 10x approximately. This still puts our ratio far below sector medians. We could narrow our comparison down to just its components within the same industry (Communications equipment) for better comparisons.

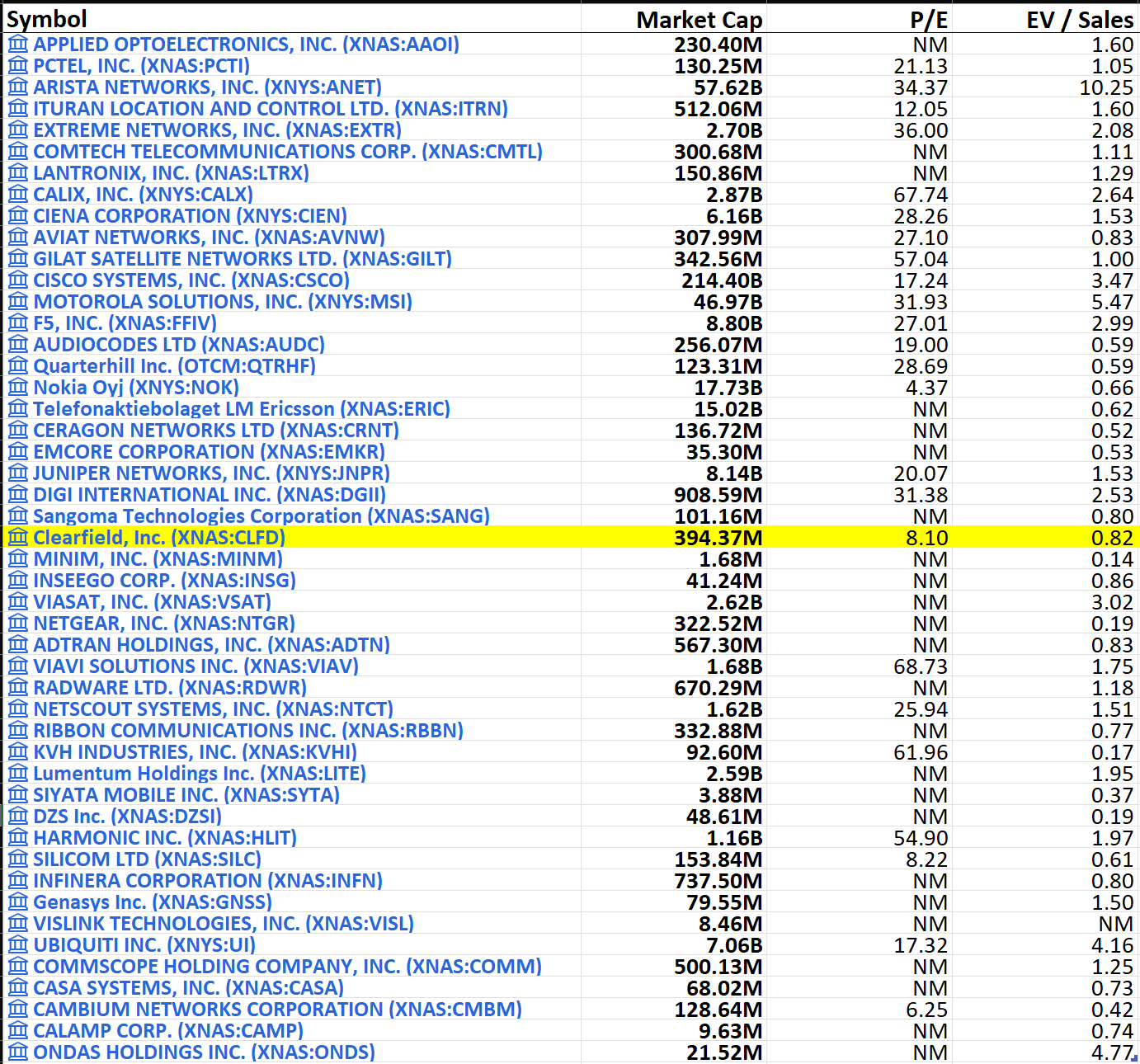

Valuation of Communications Equipment Industry Components (Seeking Alpha)

{kind=link}

It is clear from the above list that many of the components in this industry are not even profitable. However, even among the profitable ones, Clearfield fares quite favorably not only in the present but also in the worst-case scenario in the future. A similar observation can be made for EV/Sales where the median of the industry is 1.05x and the average is 1.62x.

How about optimistic scenarios? In my view, this could be more likely as the long-term growth can remain intact because of the opportunities that we saw with rural broadband, 5G, and Europe expansion. 5Y average growth rate is at 36% and forward growth is seen at 20%. As we saw in our scenario-based valuations, we can compute the valuation for a range of growth rates but at 20% growth (conservatively optimistic) we would see EV/Sales at 0.67x and PE at 6.5x (approximately)

Growth (Average and Forward) (Seeking Alpha)

This is where I believe things would start getting even more interesting. Even though the SPY and NASDAQ are up significantly for the year (10% and 30% respectively), the breadth/participation of the market remains low as small-cap stocks are getting crushed. It could be that a lot of the recent performance of Clearfield stock is attributed to this phenomenon and has less to do with its business performance. And why could this argument be valid? It's because the stock's market cap is at late 2020/early 2021 levels even as the revenue, profitability, and equity have tripled. While I believe market excesses being trimmed is a good sign, in Clearfield's case it could be the market doing the proverbial "throwing the baby out with the bathwater".

So what would happen if this continues to beat the stock price down? Currently, the book value per share is $20.44 and we may see a scenario where the stock starts trading below its book value per share (Current P/B is 1.26x). This combined with even modest growth rates would be the cherry on top for our valuation argument.

Key Risks

The company's business model revolves around the manufacturing of materials and thus it opens it up to a variety of risks regarding inflationary pressures on raw components, sourcing materials from suppliers, and any disruptions in the supply chain. The company could get ahead of the problem by increasing its stock of materials but any change in ordering patterns from its customers would leave it with high inventory. There is already clear evidence of this happening when you look at their balance sheet and how inventory has evolved over the last several time periods.

Inventory levels (Seeking Alpha)

{kind=link}

This shows that the company would always be walking a tightrope and is a risk that would be ever-present for them.

A less major risk is what I see regarding their customer concentration. In 2022, one customer represented 14% of their sales, whereas in 2021 and 2020, two customers made up 28% and 30% of sales, respectively. Since these customers are distributors and there are no obligations for future purchases they could easily switch to a competitor affecting the company's operations. This means that Clearfield has to remain competitive in its offerings and any slip-up would affect its financial position.

Wrapping up

I am rating Clearfield as a Buy and believe the market is severely mispricing the stock again. While on its way up the market gave no room for error and now on its way down the market is severely undervaluing its potential as its business model remains intact and its addressable market remains bright. This could be a good example of long-term investors needing to be greedy while others are fearful. The management was also clever in making use of the explosive increase in stock price by issuing stock and beefing up its balance sheet. The same cash will continue to earn interest income or can be used towards another acquisition should an opportunity present itself (Another interesting twist would be if the company's business remains strong and they decide to use the cash to buy back their own stock if the market continues to value them lower. Essentially, this would be Sell High and Buy Lower !)

But it has to be mentioned that investors should be ready for further downward movement in its stock price as indicators for small-cap stocks are currently pointing that we are heading towards another bear market for small-cap stocks (IWM is approximately 30% off its all-time high and has dropped 15% in the last 3 months alone).

Savvy investors can reduce their entry price by following one of the many options below -

- Initiate a starter position now and dollar cost average till the maximum position size is reached.

- Sell puts at a price you would be more comfortable getting in (below its book value?)

- Initiate a covered call

Personally, I am comfortable with the way the company is looking at the present including its valuation, and will be initiating a starter position. I will also be closely monitoring this position and the company's earnings. If I do not see a threat to the company's business model and the valuation continues to get attractive, I will be dollar-cost averaging into the position till I reach my maximum threshold.

Editor's Note: This article was submitted as part of Seeking Alpha's Best Value Idea investment competition , which runs through October 25. With cash prizes, this competition -- open to all contributors -- is one you don't want to miss. If you are interested in becoming a contributor and taking part in the competition, click here to find out more and submit your article today!

For further details see:

Clearfield: Being Greedy When Others Are Fearful