CLFD - Clearfield: European Expansion 5G And IoT Could Imply Undervaluation

2023-07-13 02:10:55 ET

Summary

- Clearfield Inc., a US-based telecommunications company, is expanding into Europe following its successful acquisition of Finnish company, Nestor Cable Ltd.

- The company anticipates growth in sales and business flow due to increasing digitization and the expected growth of the FTTH market in the US.

- Despite potential risks such as client concentration and increases in manufacturing costs and salaries, Clearfield seems undervalued and is expected to see further growth and expansion.

Clearfield, Inc. ( CLFD ) accumulated a lot of know-how in the telecommunications market in the United States, and recently commenced its expansion in Europe. I believe that the FTTH market growth, successful integration of the acquisition in Europe, and further headcount growth will most likely lead to FCF sales growth in the coming years. I do see risks from certain concentration of clients, increases in the price of manufacturing processes, or an increase in salaries. With that, I believe that CLFD trades undervalued.

Clearfield

With the largest number of its operations concentrated in the United States. Clearfield Inc offers design, development, and distribution services for the protection, management, and distribution of fiber networks for different industries, primarily for telecommunications, Wi-Fi network operating companies, and TV companies, along with the broadband services.

The company’s services are divided into a variety of proprietary products that it offers independently and in purchase packages, taking advantage of the needs in small points of its clients' networks as well as those who decide to move their network to the optical fiber.

Clearfield projects a growing demand in its sales and flow of business, taking advantage of the general trends in the market, with the budding digitization of internal communication modules at the business level, along with different alternatives storage and data management. In this regard, I believe that investors may want to have a look at the FTTH market, which is expected to have a cumulative 5G cycle spend by 2035 of close to $200 billion.

Source: Investor Presentation

In the last quarterly presentation delivered in June, the company noted impressive expectations about the number of FTTH homes marketed in the United States for the years 2023, 2024, 2025, and 2026. In my opinion, if the market grows as expected, Clearfield would most likely experience significant net sales growth.

Source: Investor Presentation

It is important to note that the company does not design or install the networks, but it is dedicated to the design and marketing of materials and devices that are part of this type of installation. A point in favor when it comes to the design of its products is the flexibility it offers to its customers, being able to make devices and artifacts according to the specific needs of each one of them.

If we refer to its main clients, during the years 2020 and 2021, two of these concentrated 28% and 30% of the annual profits. This number later dropped to 15% in 2022, which appears beneficial. In my view, further decrease in the concentration of sales would most likely interest market participants. The concentration of sales and commercial activities in specific clients - in this case broadband distributors - is a condition of great magnitude if we think about Clearfield's versatility when it comes to developing new investments, research, and agreements.

It is also worth noting that management does not expect annual sales to fall significantly in 2023. The forecast for the year 2023 includes $260-$275 million in sales and EPS close to $1.8-$2.1. In my view, management tried to be conservative, which I do appreciate. If the company delivers better than expected results in 2023, I would be expecting some demand for the stock.

Source: Investor Presentation

Solid Balance Sheet With Little Debt And A Small Amount Of Liabilities

As of March 31, 2023, the balance sheet delivered included cash and cash equivalents of about $137 million, with short-term investments close to $19 million, accounts receivables worth $39 million, and inventories of $100 million. The ratio of total current assets/total current liabilities stood at close to 7x-8x, so management may not have to deal with liquidity issues any time soon. Property, plant, and equipment stood at $21 million, with goodwill of $6 million, intangible assets worth $6 million, and right-of-use lease assets of about $11 million. Finally, total assets stand at $357 million, and the asset/liability ratio appears very solid.

Source: 10-Q

The liabilities include current portion of lease liability of $3 million, accounts payable of $16 million, accrued compensation of $6 million, accrued expenses worth $5 million, factoring liability of $8 million, long-term portion of lease liability of $8 million, and total liabilities of $51 million.

Source: 10-Q

Financial Model: The European Expansion, Growth Around The 5G Industry, And New IoT Technologies Would Imply Undervaluation

Under my financial model, I incorporated certain long-term catalysts highlighted by management in a recent presentation. I assumed that governments will offer beneficial financial packages or funding, which will most likely accelerate the number of actors in the industry, and may also enhance business growth.

Additionally, I believe that Clearfield will most likely enjoy 5G market growth driven by the development of new IoT solutions. Finally, if the company makes further investments in Europe, where public money is very important, in my view, management may receive further exposure to growing markets.

Source: Investor Presentation

In my view, more communication and information about the beneficial effects of Clearfield’s product in the financials of clients could bring more clients and more investors. It is worth noting that it removes barriers to wireless 4G/5G small cells, offering easier reconfiguration and less expensive networks. In my opinion, most market participants believe that 5G means faster networks. In this case, it may also mean FCF margin expansion.

Our products help make business services more profitable through faster building access, easier reconfiguration and quicker services turn-up. Finally, Clearfield is removing barriers to wireless 4G/5G small cell, Cloud Radio Access Network, and distributed antenna system deployments through better fiber management, test access, and fiber protection. Source: 10-Q

In July 2022, Clearfield acquired Nestor Cable Ltd, a provider of similar services in Finland, with its sights set on developing its business globally, first achieving a position in European territory. Due to this acquisition, the company began to operate with two business segments, for its operations in the United States and Finland. Hence, Clearfield is in the process of integrating the Finnish acquisition into the development of its historic US-based segment. In my view, if the integration is executed successfully, the market or debt investors may offer more financing for further acquisitions in Europe. With this in mind, even if management does not seem to have a lot of expertise in the M&A markets, I would be expecting further inorganic growth in the coming years.

Considering the state of the balance sheet, the training programs for manufacturing offered, and overall collaborative working environment disclosed in the last 10-k, I would expect further headcount growth. Over the last 10 years, the company noted headcount growth of close to 12%. I would expect similar growth in the coming years. More employees would most likely enhance net sales growth and FCF margin.

Source: Ycharts

We invest significant management attention, time and resources to attract, engage, develop and retain our employees, particularly for positions that require technical knowledge or expertise. For this reason, we offer rigorous training programs for manufacturing and other technical employees to allow them to develop the necessary skillset for their roles and promote career development. To date, our training programs and overall collaborative working environment have allowed us to be successful in attracting and retaining qualified technical personnel for these positions. Source: 10-K

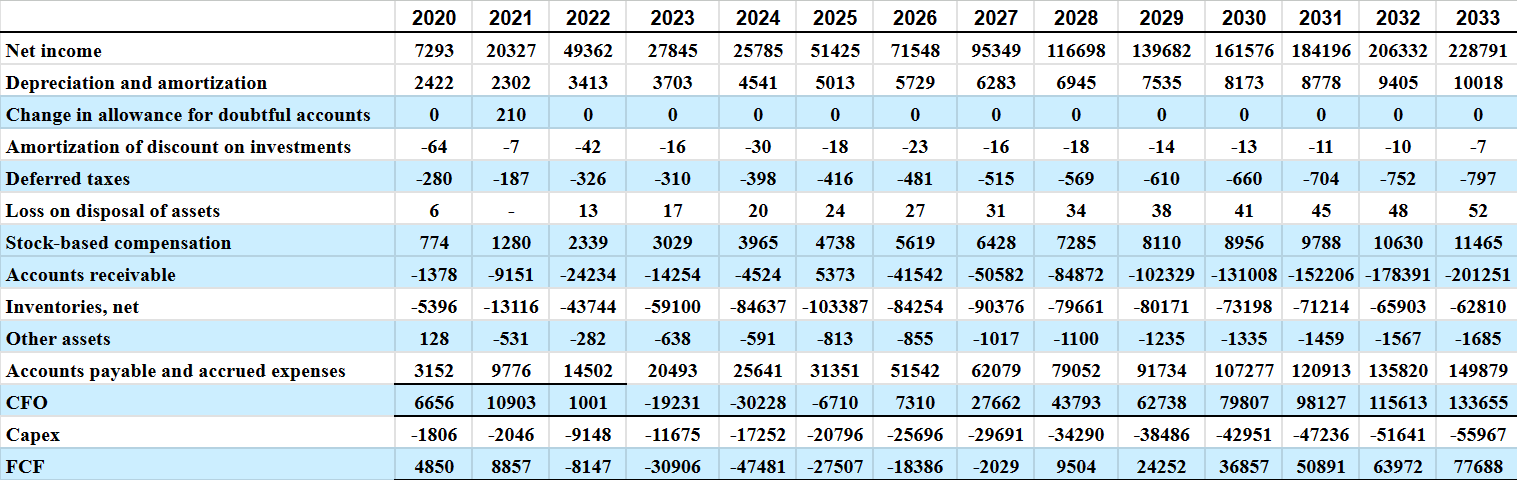

My DCF model included 2033 net income of about $228 million, 2033 depreciation and amortization worth $10 million, 2033 stock-based compensation of $11 million, and changes in accounts receivable of close to -$202 million.

Besides, with 2033 changes in inventories worth -$63 million and changes in accounts payable and accrued expenses worth $149 million, 2033 CFO would be close to $133 million. If we also assume 2033 capex of -$56 million, 2033 FCF would be about $77 million.

{kind=link}

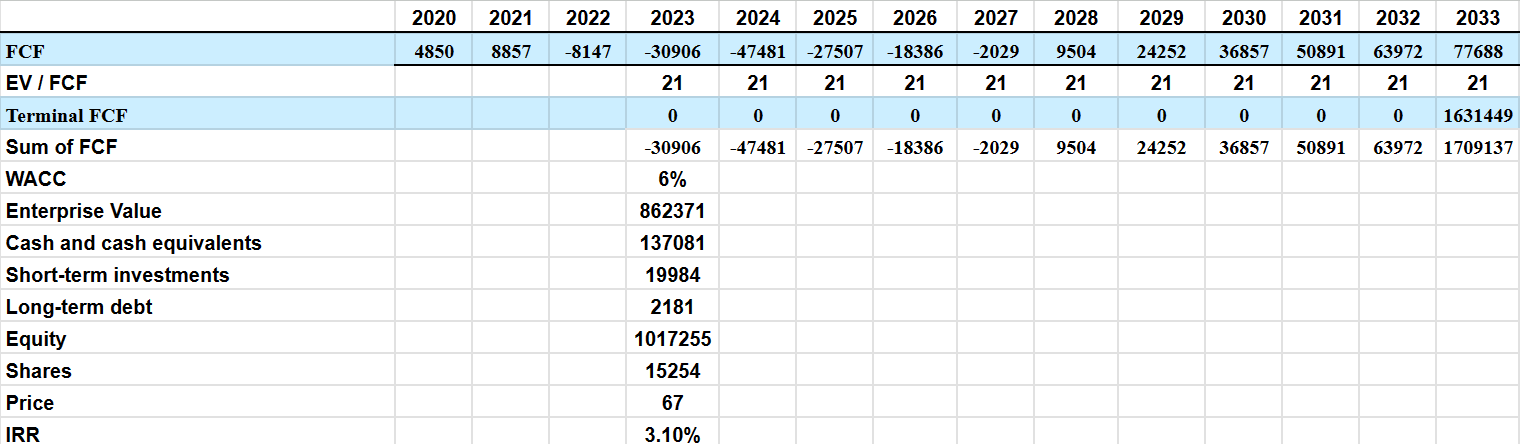

If we assume EV/FCF of close to 21x and a WACC of 6%, the implied enterprise value would be $862 million. The EV/ FCF 3 Years, 5 Years, 7 Years, and 10 Years median stand between 28x and 43x, hence I believe that my terminal EV/FCF of 21x appears conservative.

Source: Ycharts

It is also worth noting that the company appears to be paying an interest rate of close to 4.36% for the debt. With this in mind, I believe that my discount of 6.5% is very appropriate.

As of September 30, 2022, the Company had combined consolidated balances of cash, cash equivalents, short term and long-term investments of $45,199,000 compared to $60,503,000 as of September 30, 2021. As of September 30, 2022, our principal sources of liquidity were our cash and cash equivalents and short-term investments. The line of credit matures on April 27, 2025 and borrowed amounts will bear interest at a variable rate of the CME Group one-month term Secured Overnight Financing Rate (“SOFR”) plus 1.85%, but not less than 1.80% per annum. As of September 30, 2022, the interest rate was 4.36%. Source: 10-k

Adding cash and cash equivalents of close to $137 million, short-term investments worth $19 million, and long-term debt of about $2 million, the implied equity valuation would be $1.017 million, and the implied price would be $66-$67 per share with an IRR of close to 3.1%.

{kind=link}

Competitors

In a highly competitive market such as the management, design, and distribution of fiber materials and devices, the differential factors are the efficiency of the networks, the low cost of the products, quality, ease of installation, and support teams for the clients. In this sense, Clearfield competes in the positioning of its products with larger companies and small companies dedicated exclusively to the design of certain products. Some of the companies that stand out are Nokia (NOK), Fujikura Ltd, or Amphenol (APH).

Risks

Clearfield currently faces the challenge of successfully integrating its two business segments, allowing aligned operations between the United States and Europe. Just as a challenge deserves a correct reading of the landscape, so does the development of new products, since the inability to design products that serve future customers could directly affect the operations of the company.

Clearfield may suffer from certain concentration of clients. This produces a state of fragility as any change of supplier by contracting companies could spell a disastrous year for Clearfield's development ambitions, both nationally and internationally.

Finally, I believe that changes in the price of certain raw materials, inflation, and increases in the price of manufacturing processes could destroy Clearfield’s FCF margins. Besides, management may have to pay more salaries to new employees, which may also reduce FCF growth potential. In this regard, management provided some commentaries.

Rising costs, including wages, logistics, components, and commodity prices, are negatively impacting our profitability. We are subject to market risk from fluctuating market prices of certain purchased commodities and raw materials such as fiber cable and other components, which has outpaced our ability to reduce the cost structure and manufacturability or increase prices. We do not hedge commodity prices. Source: 10-Q

Conclusion

With know-how accumulated for many years in the United States, Clearfield Inc recently decided to acquire a company in Europe. In my opinion, if the transaction is successful, and management benefits from 5G expansion in Europe, we may see further acquisitions. I believe that the balance sheet would most likely allow further inorganic growth. Additionally, I think that the company may continue to deliver headcount growth close to 12%, which would most likely enhance future sales growth. I do see risks from increase in the price of manufacturing, inflation, acquisition integration, and concentration of clients, however the stock does appear a bit undervalued.

For further details see:

Clearfield: European Expansion, 5G, And IoT Could Imply Undervaluation