CLFD - Clearfield: Mr. Market's Overreaction

2023-05-11 15:33:46 ET

Summary

- I believe the market has overreacted to recent guidance slashes, creating an attractive opportunity for long-term oriented investors.

- Clearfield’s near-term headwinds present risks but appear to be short-term in duration.

- Demand for fiber remains massive, supported by a significant pipeline of government investment in the coming years.

- Clearfield is led by ‘owner-operators’ with a proven ability to navigate the industry and create shareholder value.

Investment Thesis

Clearfield ( CLFD ) has fallen out of Mr. Market's favor so far this year. After recent guidance cuts in the Q2 earnings report, the stock fell over 20% and is now down 60% year-to-date. Despite near-term headwinds, Clearfield remains poised to capture the sizable long-term demand for fiber for several reasons:

- The company's recent demand slowdown presents a risk but appears to be short-term in nature.

- Long-term demand for fiber is massive, supported by ample government broadband investment yet to impact Clearfield's topline.

- Clearfield is led by 'owner-operators' with a proven ability to navigate the industry and create shareholder value.

Clearfield has been unduly punished by a short-term biased market in my view, presenting an attractive opportunity for prudent long-term investors.

1) Near-term Headwinds

Clearfield's Q2 revenue fell short of analyst estimates by $0.18M but still grew 34.2% YoY to $71.8M. The company also slashed its fiscal year revenue guidance by $120M and EPS by $2.45 per share. The company attributed these cuts to an unanticipated lull in demand driven by the following :

"… we have experienced order pushouts by several Large Regional Service Providers and some Multiple System Operators (MSOs or Cable TV providers) who had accumulated an excess inventory position during the pandemic period."

Essentially, the company failed to foresee a pause in orders from a handful of large customers due to over-purchasing inventory during the pandemic. These customers over-ordered in an attempt to capture surging demand and stay ahead of supply chain issues the past few years. This was shown in Clearfield's massive backlog number through '21 and '22. These customers have pushed out their new orders as they digest excess inventory. Clearfield has not lost any customers but is now facing short-term demand headwinds. Here are a few takeaways I have and risks that have been uncovered regarding this situation:

- The company fumbled the ball in not anticipating a scenario of its customers over-purchasing inventory. Leadership should have been aligned and in constant communication with its large buyers, which would have allowed for more accurate prior guidance for the fiscal year.

- Even so, management actions highlight their commitment to investor transparency. A few examples are increasing communications with large customers sometimes to a daily cadence, continuing to report backlog after investor feedback from last quarter, and adding a revenue breakout of large regional service providers in quarterly reports - as per the company's Q1 transcript. Clearfield also tracks large customer inventory position and plan, but relies heavily upon customers executing their plan.

- The issue highlights a major risk for Clearfield: significant customer buying power. Clearfield's performance relies heavily on customer ordering patterns within its regional service provider and MSO categories. Nonetheless, no customer makes up more than 10% of revenues and Community Broadband makes up a majority of revenues.

Community Broadband is comprised of smaller local carriers and is less of a risk to Clearfield in these areas. It also happens to be one of the company's fastest growing segments, climbing 72% YoY. Additionally, leadership has a focus on taking market share with smaller carriers as they tend to grow faster than other categories. Despite near-term uncertainty with ordering patterns, management expects a "strong return to broadband deployment in the latter half of the year". Investors should be aware of the risks associated with this issue but recognize they are short-term in nature. Clearfield's long-term opportunity within fiber deployment remains significant.

2) Outlook for Fiber

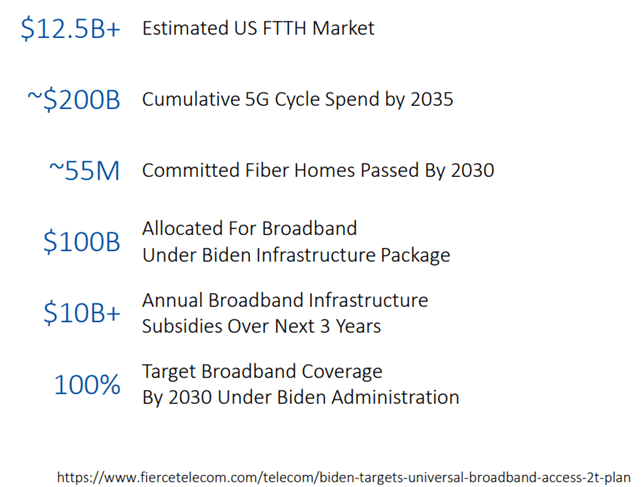

Fiber optics is the backbone of broadband infrastructure, which is what allows for the trillions of connections and transmissions of data every single day. Almost all modern-day industries rely on high-speed internet connection and the ability to transfer data. In addition, as technology advances, so does the need for faster internet and greater bandwidth. Emerging technology industries such as 5G, Cloud & Edge Computing, and Internet of Things ('IoT') all heavily rely on the build-out of fiber architecture, as touched on in my previous article . Even Artificial Intelligence indirectly relies on fiber which connects the massive data centers supporting its development. The global fiber management systems market is expected to grow 13.3% annually through 2030, with North America comprising one-third of the market. This report also highlighted the major opportunity within rural, underserved areas, which happens to be Clearfield's strategic focus. Adding to this, the pipeline of government funding for broadband remains massive. Specifically for rural areas with less coverage.

{kind=link}

3) Management Execution & Operational Excellence

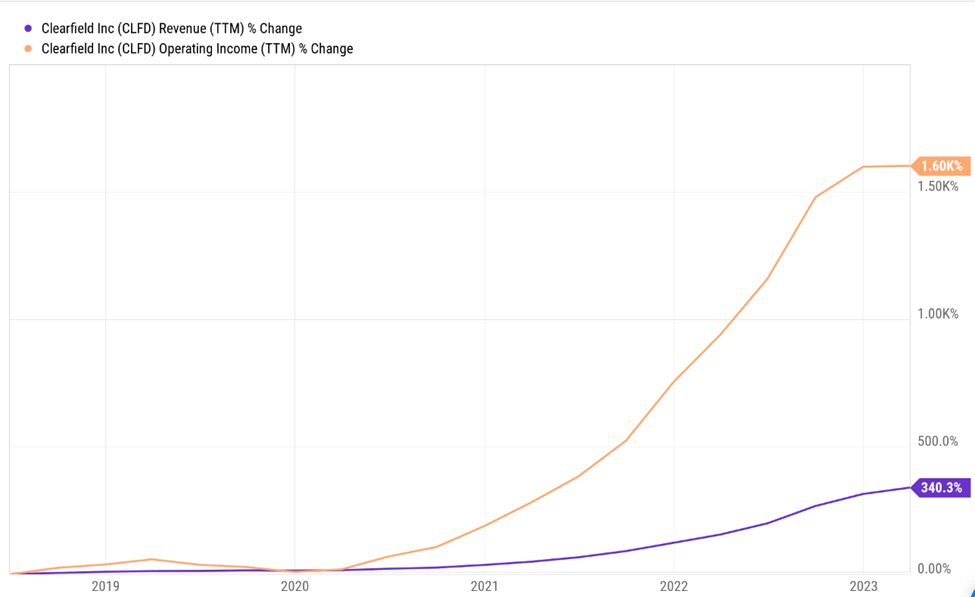

Clearfield's management has led the company to over a decade of profitability and positive returns on capital. Leadership's capital allocation ability is their primary strength. They've structured Clearfield to create value for shareholders even when topline growth wavers. The past five years were characterized by a surge in pandemic-driven demand of which Clearfield was able to meaningfully capture. The company grew revenues over 30% annually the past five years and demonstrated structural operating leverage while using almost zero debt.

{kind=link}

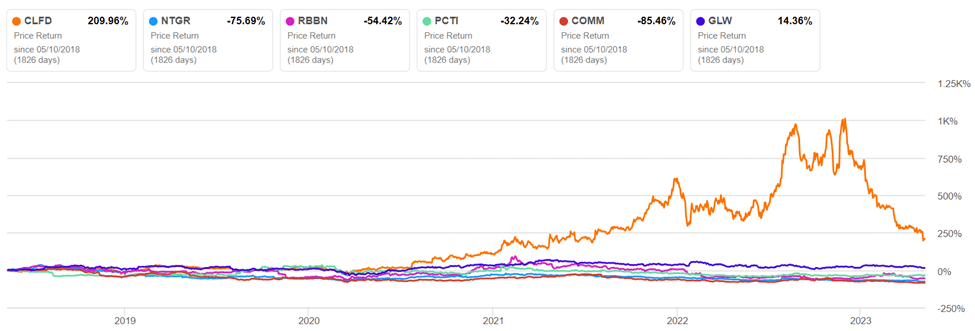

Additionally, management raised capital via stock issuance when shares were near their peak of $130. This boosted the company's liquidity and gave them more flexibility to handle the current near-term demand uncertainty. Leadership has effectively balanced profitability with investment in growth. The result has been market-beating returns for investors. Even after last year's sell-off, CLFD has beaten the S&P 500 by over 150% and peers by even more in the past 5 years.

{kind=link}

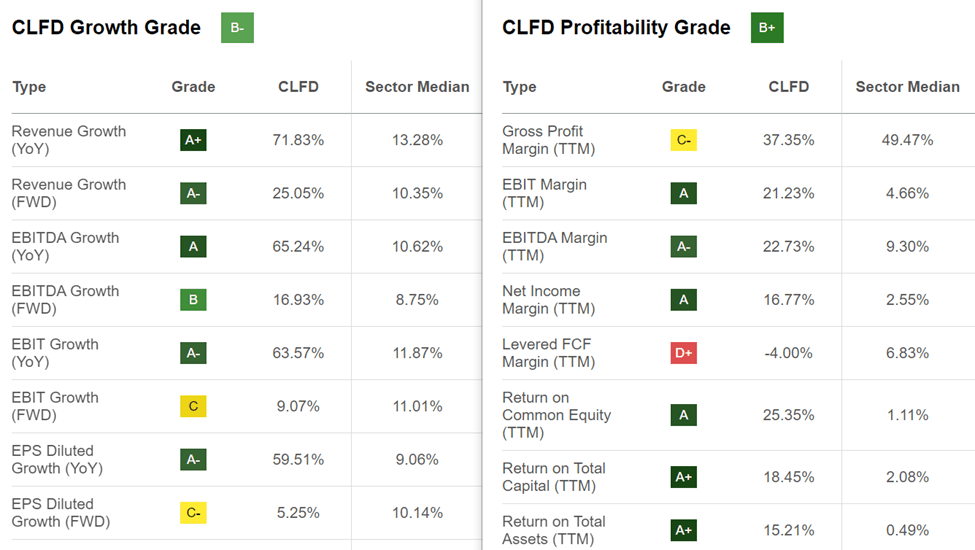

The difference is even more stark when looking at financial performance. Clearfield outpaces its sector median (peer group) on the majority of metrics measured by Seeking Alpha.

{kind=link}

It's much easier to have confidence in the face of uncertainty with this management's track record. Especially given their 'skin in the game', with insiders owning over 15% of outstanding shares.

Despite strong operating performance, Clearfield has a number of financial risks investors should be aware of. Gross margins and cash flow are clear areas of weakness for the company. Gross margins fell over 10% YoY to 32%, driven by unused capacity from order pushouts and the contribution of Nestor Cable's lower gross margin business. Gross margins are expected to recover to 40% as demand comes back online and Nestor Cables is restructured. But lower gross margins have a ripple effect down the income statement, damaging returns on capital and free cash flow. This is no doubt a concern for investors, especially combined with the current economic environment of higher input costs and inflationary pressures.

Clearfield's free cash flow and cash from operations have been historically lackluster despite a strong overall cash position on the balance sheet. The main culprits are excess inventory purchases and capital expenditures to build out capacity in the company's manufacturing facilities. Similar to gross margins, when demand returns this inventory should be digested and cash flow should improve. A positive note is Clearfield's preference to use cash rather than debt for operations and investment as it mitigates interest rate exposure.

Valuation

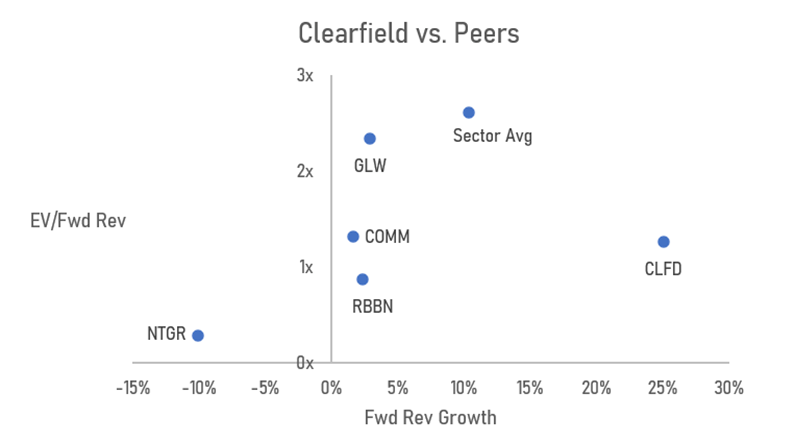

Crashing investor sentiment has driven CLFD valuation multiples to near record lows. Their price to sales ratio for example has fallen from near 8x in 2022 to 1.5x. The stock's valuation grade, which compares the stock's valuation to its sector, on Seeking Alpha has gone from a C- to an A- in 6 months. Compared to peers using forward revenue growth and EV/forward revenue, Clearfield looks like a steal despite the short-term revenue outlook dropping.

{kind=link}

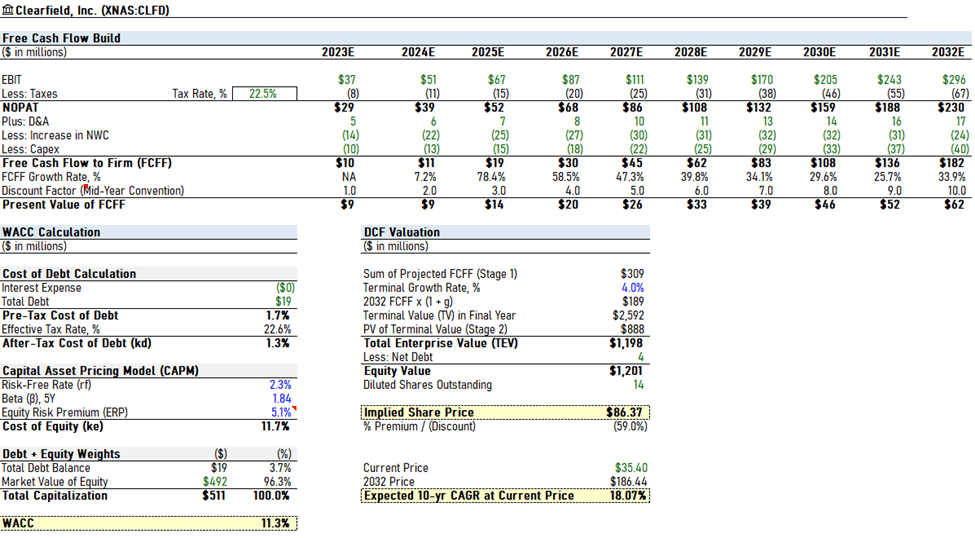

From a future free cash flow perspective, Clearfield also looks severely undervalued. I purposely used conservative assumptions in my base case for DCF analysis given the near-term uncertainty. Here are my assumptions:

- Revenue CAGR of 10% for 10 years (basically growing with the market).

- Gross margins starting at 30% and expanding to 40% over 10 years (most likely will recover to 40% in a shorter-time frame than assumed).

- SG&A margin hovering in the high teens (they cut operating expenses 16% YoY and are operationally efficient).

- EBIT margins then drop to low teens this year and recover to the low 20%s at the end of the forecast period.

- Depreciation, Net Working Capital, and CapEx staying relatively consistent.

- A discount rate ('WACC') near 11% driven by a fairly high beta.

The result was an intrinsic value per share of $85.34 representing a margin of safety of 59%. To put this in perspective, buying at the current share price of about $35 would yield an annual return of over 18% for the next 10 years, based on my conservative assumptions. That's quite the upside.

{kind=link}

Conclusion

When a company falls out of favor with the market, it can be a curse or a blessing depending on the investor's perspective. Short-term overreactions are far too common but can be an avenue of alpha generation for investors willing to zoom out. In my opinion, Clearfield fits this category. Near-term issues and post-pandemic realignment has the market overreacting to the downside, overlooking the tremendous long-term opportunity I believe the company has.

For further details see:

Clearfield: Mr. Market's Overreaction