CLPT - ClearPoint Neuro: I Continue To Rate The Stock A 'Buy'

2023-06-05 05:02:09 ET

Summary

- ClearPoint Neuro's progress on its four-pillar strategy continues despite a challenging operating environment, with an increasing number of partners and hospital sites featuring its equipment.

- The company has entered into pre-clinical work and milestone-based partnerships, such as its recent deal with UCB, a global biopharmaceutical leader.

- However, ClearPoint Neuro faces challenges with its cash position and increased cash burn, which may prevent current stockholders from benefiting financially from eventual profitability.

I began coverage of ClearPoint Neuro ( CLPT ) in July of 2022 with a "buy" rating (though noting that the "current valuation isn't compelling) and reiterated that verdict in January of this year. The stock has continued to trade down, but as I explain in today's article, I still believe that the stock will pay off in the longer term.

The poor performance to date mirrors that of most small cap biotech stocks over that timeframe; and during the most recent earnings call , the company mentioned three factors that have specifically been unexpectedly worse than originally forecast (with my emphasis):

Over the last couple of years, we have seen both the opportunity and the necessity to augment our strategy in light of dramatic changes to the cost of capital, supply chain constraints and volume of elective procedures . These strategic adjustments have included expanding preclinical services and capabilities for our pharma partners, entering the therapeutic device market with the Prism Laser Therapy System, and evolving our navigation platform beyond the MRI and into the operating room.

While the first factor is likely to be operative going forward, there is anecdotal evidence provided during many companies' earnings calls that supply chains are slowly normalizing. And it's unlikely that elective procedures will be put off indefinitely, so I personally believe we'll eventually see a return to pre Covid numbers on that front as well.

ClearPoint Neuro

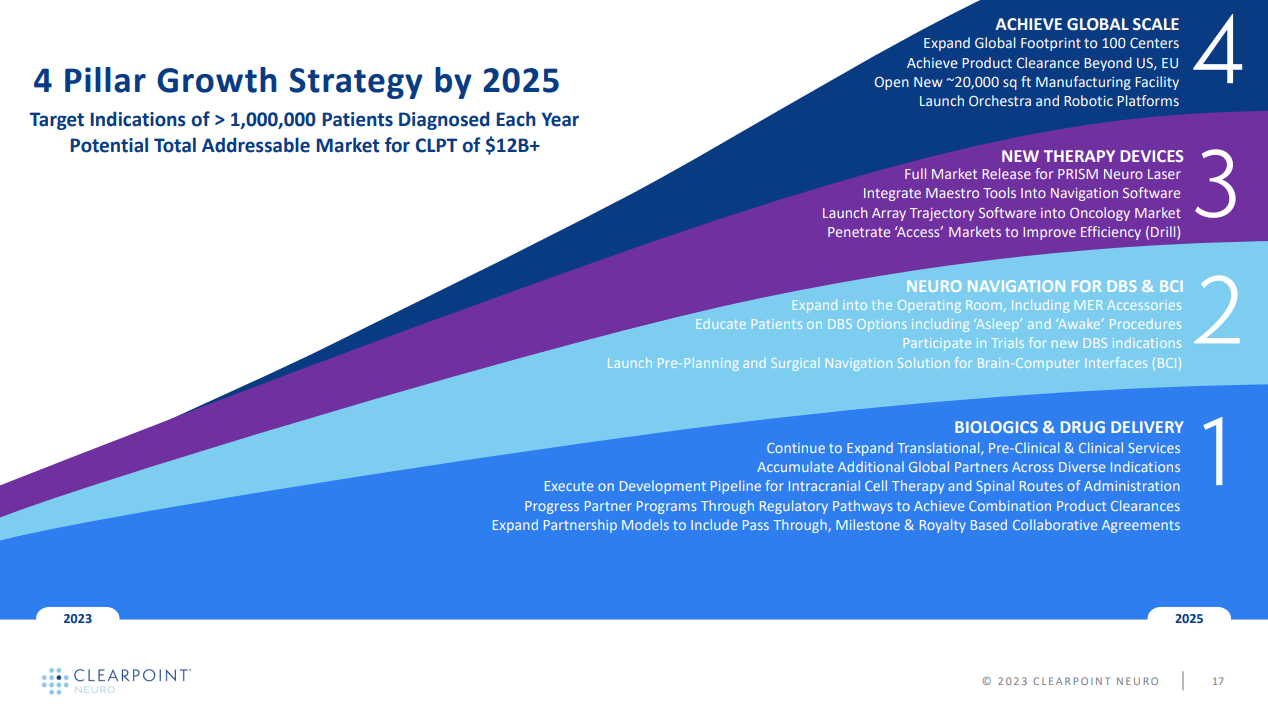

As I've discussed previously, CLPT has a "four pillar" strategy to convert its core competencies into commercially viable products.

As outlined in the slide below, these consist of:

- Biologics and Drug Delivery

- Navigation to Assist Deep Brain Stimulation and Brain-Computer Interfaces (think Elon Musk's Neuralink without all the hype)

- Neuro Laser and other new therapies

- Expand items 1 to 3 globally

{kind=link}

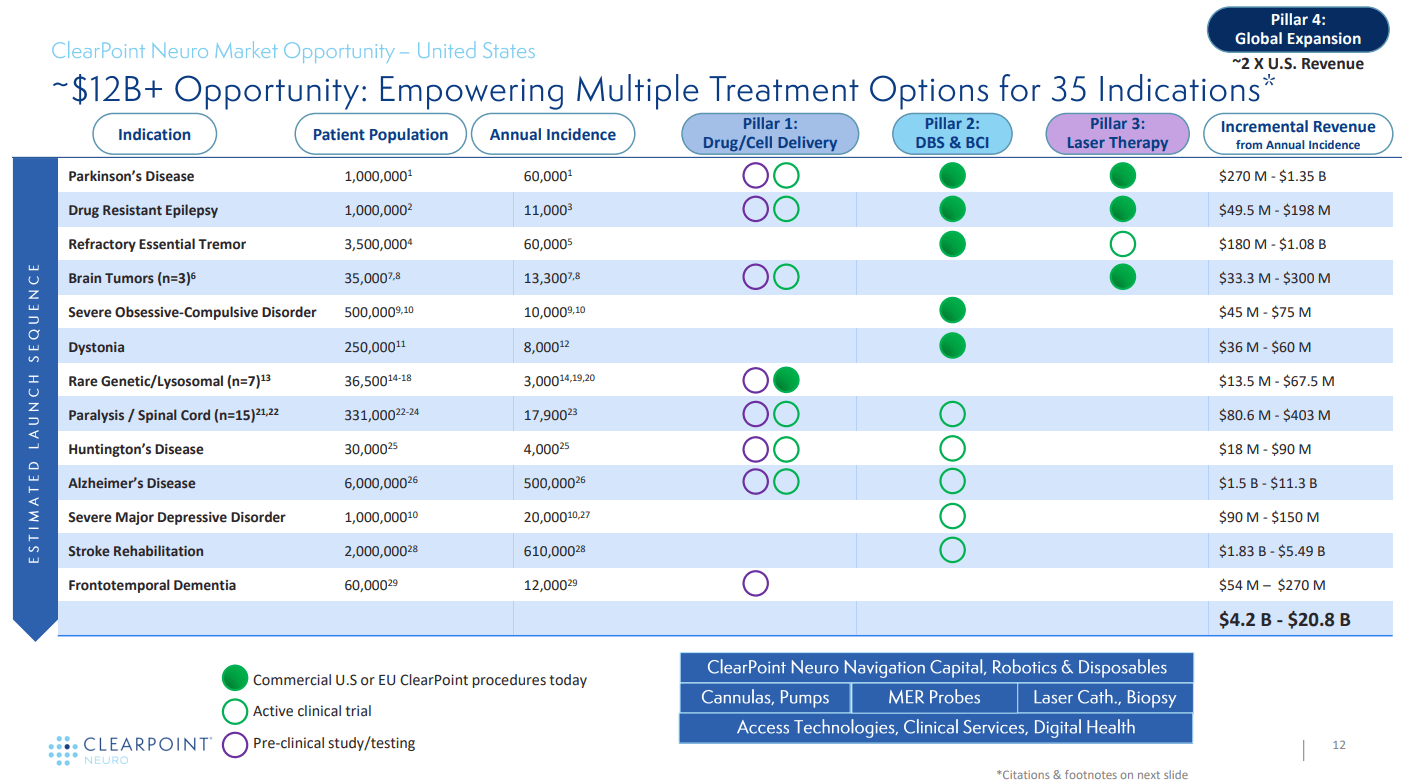

This slide identifies (some of) the target markets for each "pillar" as well as giving the status of clinical progress in each. As can be seen, the first three pillars have activity ranging from pre-clinical testing through to regulatory and commercially authorized procedures; and at least by that metric, the company has been making continued progress in developing its strategy.

{kind=link}

Razors / Razorblades

To me at least, the beauty of CLPT's approach is that it is built on a model by which revenues are mostly generated from the sale of disposables. That is, once a CLPT piece of equipment or technique has been accepted as part of a larger FDA approval, there are continuing revenues from disposables used in each and every procedure. And the moat for these continuing revenues is the FDA approval itself (which specifically includes the CLPT product, not some generic product category). See my previous articles for an elaboration of this thesis.

On the earnings call, the company updated its rollout of regional sites that do or will feature CLPT equipment. The numbers look good for continued revenue expansion and cash flow positivity by the end of 2025 (run rate). With my emphasis:

[O]ur functional neurosurgery navigation business added new sites to our installed base in the quarter and we continue to expect more than 10 site installations in 2023. This is keeping us on pace to achieve an installed base goal of 100 individual customers by the end of 2025 . As a reminder, our strategy is not to install ClearPoint at every local hospital but rather treat these patients with chronic conditions at regional therapy centers that have the benefit of scale and experience. Just 100 centers doing two procedures a week could potentially deliver $100 million in revenue to the company. At present, we have more than 50 hospitals active in our acquisition funnel, meaning we need just a 20% closure rate this year to achieve our 2023 goal.

Moving into Pre Clinical Work and Milestone-Based Partnerships

As its been working with clinical partners, CLPT has realized that it can provide value in pre-clinical work as well. Not only does this provide earlier revenues, but more importantly, it secures CLPT's involvement from the very get-go of new therapies and approaches. The company elaborated on this aspect during its earnings call (with my emphasis):

Importantly, our extension into preclinical services has transformed our relationship and duration of partnership, allowing us to work alongside pharma well before the first patient is enrolled. We have now signed our first milestone based agreement with a pharma partner whereby ClearPoint is able to share within the success of important development and regulatory milestones with the drug sponsor. We expect this deal to become the blueprint for future agreements with our pharma partners and allow us to form more creative and sophisticated methods of collaboration that better value the unique support that we believe we offer in drug development .

The first such deal was announced with partner UCB ( OTCPK:UCBJY ), a Belgian biopharmaceutical with 8,400 employees and an EV of $18.8B.

Here's a summary of this deal announced on May 24th (again with my emphasis):

[CLPT] announced that it has entered into a multi-year license agreement with UCB (EURONEXT BRUSSELS: UCB), a global biopharmaceutical leader, to partner on drug delivery platforms for UCB’s gene therapy portfolio.

“We are extremely excited to partner with UCB, a global biopharmaceutical leader, with a focus on innovating through the adoption of next generation science and new technologies,” stated Jeremy Stigall, Executive Vice President and General Manager of Biologics and Drug Delivery at ClearPoint Neuro. “Over the past year, we have invested heavily in expanding our Biologics and Drug Delivery team, as well as our product and services portfolio to attract partners of UCB’s caliber. UCB sought comprehensive tools to empower a seamless transition from benchtop testing to commercial success, and that’s precisely what our team can deliver today. ”

Under the terms of the license agreement, UCB will utilize ClearPoint Neuro’s proprietary technology and services in connection with the development and commercialization of UCB’s gene therapy products. ClearPoint Neuro will receive success-based milestone payments .

Hopefully, this is the first of many such deals!

Financial Performance

While CLPT has been steadily increasing its revenues, it has also been burning more cash in its operations. This of course isn't good, but I cut the company some slack due to its expansion on several fronts (see discussion of four pillars above) as well as the tougher post-Covid environment. Nonetheless, I won't be upping my "Buy" rating to "Strong Buy" until we see cash flow from operations approach breakeven or better.

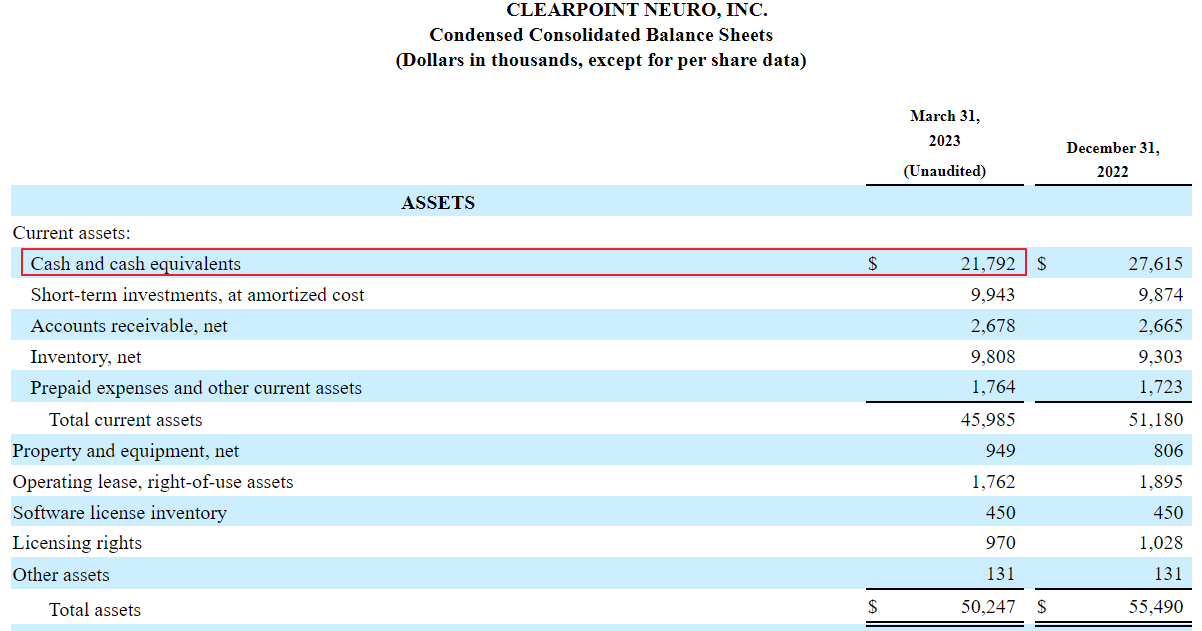

Cash on Hand and Cash Burn

The company currently has about $21M in cash on hand. Given that it's burning more than $5M per quarter (using the latest quarter's run rate), there's a good chance the company will need to raise money in the next six months or so. I won't be adding to my position until the cash position is improved.

{kind=link}

The company itself is a little more sanguine on this topic, but I prefer to be conservative when it comes to cash on hand. From the latest earnings call (my emphasis):

From a cash standpoint, we continue to perform in line with our expectations with more than $30 million in cash and equivalents at the end of the quarter, primarily in short term US treasuries. We feel like we have the vast majority of our team already in place to achieve operational cash breakeven and expect future hiring to be focused on scalable personnel in operations and clinical specialists . Although, we have allowed our inventory and prepaid expenses to expand in order to navigate supply chain challenges, as those supply risks start to wane, we expect to bring down that inventory level to more historical days on hands targets and further reduce our operational burn. We believe that as we approach the end of 2023 and move into 2024, we plan to hit an inflection point and expect to see sales growth outpace expense growth, especially when the new facility is up and running in 2024 .

Valuation

As a development stage company, CLPT doesn't yet have many meaningful metrics, but here is the valuation summary provided by Seeking Alpha just for thoroughness (with the stock trading at $7.77):

Seeking Alpha

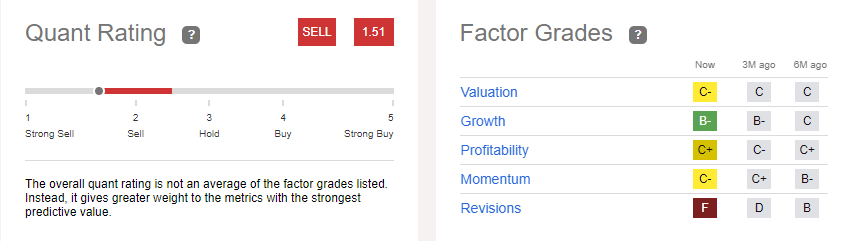

Quant Ratings

Similarly, here are Seeking Alpha's quant rating and factor grades, both of which will take on more importance once the company's commercial activities have progressed to reach cash flow breakeven.

{kind=link}

Options

CLPT trades options, but currently they are quite illiquid. However it's good to know about them in case there is ever a short term spike in price which could then be used to write covered calls against one's position (which I have done on occasion).

{kind=link}

Risks

CLPT is a development stage company that may never become profitable, hence any position in the company should be commensurate with a speculative situation.

The bigger risk, however, is that even if the company eventually becomes profitable, the number of cash raises, and hence stockholder dilution, may prevent current owners from ever benefiting financially from profitability. I, for one, won't be adding to my small position until the company has both 18 months of cash on hand and a cash burn approaching zero.

Summary

CLPT has made progress on all four pillars of its strategy despite a tougher operating environment. The number of partners and hospital sites featuring its equipment continues to grow, feeding the razorblade model. Moreover, the company is now working with large biopharmaceuticals from very early pre-clinical stages, as evidenced by the recent deal with UCB.

The downside, however, is that the company is running low on cash, while its cash burn has increased despite increasing revenues. I won't be adding to my position, nor up-rating my recommendation to "Strong Buy" until the cash and cash burn issues are clearly behind the company.

For further details see:

ClearPoint Neuro: I Continue To Rate The Stock A 'Buy'