CLW - Clearwater Paper: Stealth Accumulation And Cheapest Valuation In 13 Years

Summary

- Clearwater has dramatically reduced debt and total liabilities by 30% since 2019, as prices for pulp and paperboard climb, playing catch-up to lumber gains during COVID.

- Record EPS and cash flow per share are forecast for 2023-24 by analysts.

- A stagnate share price for years has failed to acknowledge the improvement in operations, bringing a 13-year low valuation.

- Technical trading indicators are highlighting accumulation of the stock in early 2023, setting up the chance for a truly bullish year for owners.

Clearwater Paper Corp. ( CLW ) is preparing to have a terrific year financially in 2023, largely on the back of higher market pricing for commodity paper products. The enterprise manufactures pulp, bleached paperboard, and consumer tissues from wood. However, Wall Street is only starting to wake up to the bullish setup in January-February. My research suggests now is the best time to own a position since 2010 from a valuation standpoint. In the end, very strong underlying trading momentum and accumulation trends of late could be hinting at meaningful “outperformance” of the S&P 500 index soon.

Company Website - February 26th, 2023

{kind=link}

After several years during the pandemic of pulp and paperboard prices lagging the giant upmove in lumber, a more normal equilibrium between raw and processed wood items in 2023 (on top of tight cost controls by management) should lead to a sizable and sustainable jump in revenue and income. And, if another round of money printing later this year is the Federal Reserve’s reaction to a recession, wood and paper quotes could be stuck in rising trends for years to come. So, the pricing power outlook for the company is excellent.

Below are graphs of basic price trends in pulp, paperboard, and lumber over 5-year and 50-year time periods.

YCharts - Pulp, Paperboard & Lumber Prices, Percentage Changes, Since 2018 YCharts - Pulp, Paperboard & Lumber Prices, Percentage Changes, Since 1976

According to the company’s Q4 2022 press release on February 14th, 2023,

Paperboard average net selling price increased 23% to $1,429 per ton for the fourth quarter of 2022, compared to $1,164 per ton in the fourth quarter of 2021. Paperboard average net selling price increased 25% to $1,356 per ton for the year ended 2022, compared to $1,088 per ton for the year ended 2021.

Wall Street analysts are projecting the expanded late-2022 spread for profit and cash flow generation will continue in 2023-24, after subtracting high/rising selling prices from slower growing net costs to process paper products.

Seeking Alpha Table, Clearwater Paper, Analyst Estimates for 2023-24, Made February 26th, 2023

Appealing Valuation Story

You would think investors would be more excited about Clearwater Paper’s share price and valuation. However, this company is smaller ($700 million equity capitalization) and only thinly followed by both analysts and the average investor. Today, you can buy the company at essentially the same price as 2018 or even 2012! The marketplace for the stock seems to be disconnected from the positive operating business growth taking place.

You would also think a lower valuation lines up with extra debt holdings or lower margins. Nope, cash generation on sales and total debt are not depressed, and should tick up strongly in 2023, if analyst estimates are met.

YCharts - Clearwater Paper, Cash Flow vs. Sales & Debt, 10 Years

When you review all kinds of data points, it becomes apparent today’s valuation is actually at its lowest point using fundamental ratio analysis since 2010, just after the company and manufactured-paper marketplace rebounded from the Great Recession.

The forward P/E projection of 6x is quite inexpensive vs. a cyclical history all over the statistical board. Excluding years where operating losses took place, the average P/E is closer to 12x since 2009. When you include them with an arbitrary 30x reading (for argument's sake), the average rises to 15x.

YCharts - Clearwater Paper, Price to Earnings, Since 2009

Another super-bullish positive for me is the company has aggressively reduced debt and long-term liabilities since 2019. Over the last 3 years, total debt has been slashed by $320 million and total long-term liabilities by a whopping 30%. So, the sharp 2022 increase in interest rates has been very manageable, with no real debt maturing until 2025.

From my investing experience over many decades, this makes the stock quote trading near book value (1.1x tangible BV) even more attractive as an owner. Considering cost accounting and inflationary effects on hard asset values since 2009, it would likely cost a considerably greater sum than the current stock capitalization at $38 per share to reconstruct, replace, and build similar assets (especially if borrowing at higher interest rates in 2023 was involved).

YCharts - Clearwater Paper, Price to Tangible Book Value, Since 2009

The company appears still cheaper when you add total debt to equity capitalization and subtract cash holdings, the enterprise value calculation. On EV to projected sales or EBITDA (earnings before interest, taxes, depreciation and amortization), Clearwater stands out as the cheapest since late 2010.

YCharts - Clearwater Paper, EV to Revenues, Since 2009

YCharts - Clearwater Paper, EV to EBITDA, Since 2009

EV to final accounting cash flow is also on the low end of the spectrum, and should approach 2009-10 levels if analyst estimates prove correct.

YCharts - Clearwater Paper, EV to Cash Flow, Since 2009

Technical Momentum Sorts

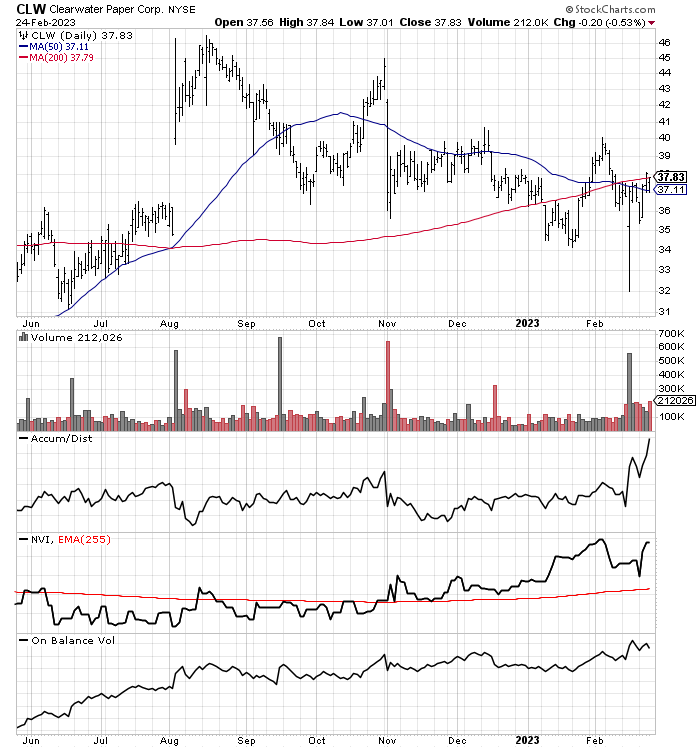

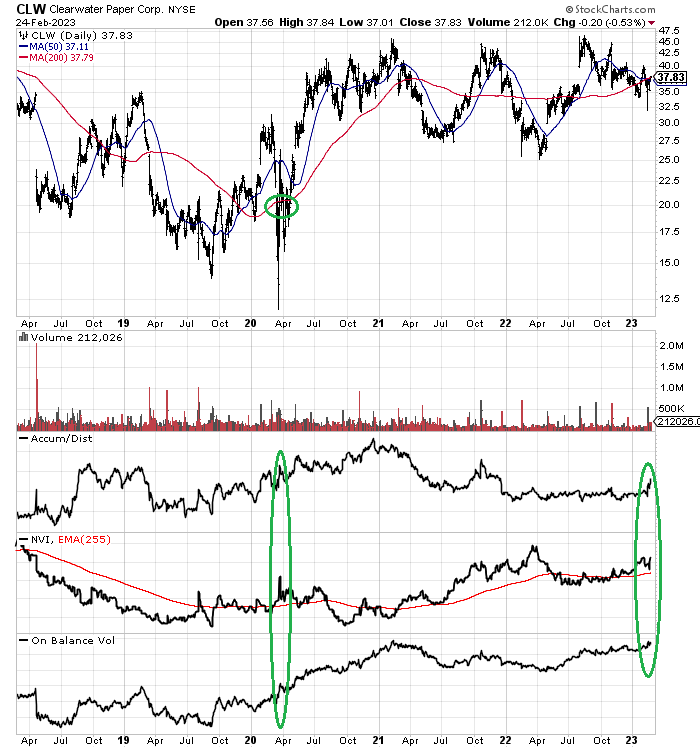

But that’s not all the bullish news for Clearwater shareholders. Despite some operating issues at its paper mills (that have mostly been resolved) during the last few months of 2022, trading patterns in the stock are showing signs of accumulation. My quant sorting research has actually detected a rather strong surge in foundational momentum during January and February.

Investors seem to be looking ahead to a great 2023, perhaps a record year for cash flow and EPS income. While price has not zigzagged higher YET, movements in tandem by the Accumulation/Distribution Line , Negative Volume Index , and On Balance Volume to 6-month highs is noteworthy. Usually, such action is part of a major price upswing on the charts. For Clearwater specifically, the last time all three were moving up together over 6 months was April 2020 (circled in green below). Following this circumstance, Clearwater doubled its pandemic panic selloff price in quick order.

StockCharts.com - Clearwater Paper, 9 Months of Daily Price & Volume Changes StockCharts.com - Clearwater Paper, 5 Years of Daily Price & Volume Changes, Author Reference Points

{kind=link}

{kind=link}

I prefer to find stocks experiencing a rise in at least 2 of the 3 indicators (ADX, NVI, OBV) as a record of healthy momentum. This 6-month Trifecta move out of 4000+ equities scanned on Friday (February 24th) revealed only 132 stocks were sitting in a similarly positive position. Honestly, far fewer have experienced a “stealth” move in these underlying momentum indicators masked by a flat stock quote.

Out of the 132 names, a few I have mentioned in past articles since summertime were included. BorgWarner ( BWA ) in January here and L.S. Starrett ( SCX ) in August here are both trading nicely above my article suggestion levels.

Final Thoughts

I guesstimate the combination of a 13-year low valuation crossed with well above-average momentum is part of the investment setup of just 5 or 10 names on Wall Street today [I wish I could produce a concrete list easily, buy my quant-sorting system utilizes a technical trading-focused database containing only a few fundamental readouts from each company]. To say Clearwater is in a rare and select group in late February is an understatement.

What could go wrong? The biggest risk is a deep recession could bring pulp and paperboard prices down, similar to the dip in lumber last year on souring demand for new home construction. However, this risk may be limited in duration, as a recession should encourage new money printing and an eventual aggressive easing policy by the Fed. Without new monetary efforts, we risk a major depression from rising defaults on near-record aggregate debt in the U.S. economy vs. GDP output.

If you give bankers, Wall Street traders, economists, and even the common man on the street a choice between 4% inflation and 15% unemployment, they will all choose slightly higher than normal inflation rates. I personally don’t know if our political divisions can handle 15% unemployment without riots, violence and possibly calls for a revolution by large swaths of American society.

If/when the Fed relents and pivots soon on interest rate policy, commodities like wood and paper will likely see an oversized price bump on speculative demand and inventory building. So, the long-term outlook for pulp and paperboard pricing is quite positive, in my opinion. If you are searching for hard asset, commodity-like investments to hedge inflation in future years, Clearwater Paper may be an excellent choice when already mispriced vs. current economic realities.

Does a cheap valuation guarantee a big upmove for the stock this year? No. Does robust trading momentum in January-February guarantee higher prices are right around the corner? No. But having both circumstances on your side does statistically improve your odds of success. I currently rate Clearwater a Buy , with odds of approximately 75% this name will “outperform” the U.S. equity market represented by the S&P 500 during 2023.

Seeking Alpha's Quant Ranking system also puts a bullish score on shares currently with a Top 5% listing out of a universe of 4,750 equities.

Seeking Alpha Table - Clearwater Paper, Quant Rank, February 26th, 2023

If pulp and paperboard prices remain elevated or rise further during 2023-24, I am projecting a $50 to $60 share price is well within reach. Using long-term average ratios of 0.75x sales, 8x EBITDA, and 2x tangible book value, a prolonged period of high paper prices could support a share price above $70, roughly DOUBLE the current level.

For a worst-case scenario over the next 12 months, a severe recession and sliding paper/lumber prices could push CLW shares under $30 to as low as $25 (in a stock market crash outcome). That works out to -35% total return loss risk on your investment (Clearwater does not pay a dividend). My best-case outlook is a mild recession (or soft landing) helps interest rates to decline and commodity price to react in a bullish manner in the second half, possibly generating a 12-month performance gain of +70% to $65 per share.

Thanks for reading. Please consider this article a first step in your due diligence process. Consulting with a registered and experienced investment advisor is recommended before making any trade.

For further details see:

Clearwater Paper: Stealth Accumulation And Cheapest Valuation In 13 Years