BILS - CLIP: T-Bills Remain The Best Game In Town

2023-11-04 10:28:26 ET

Summary

- The Q4 refunding announcement has relieved rate pressure across the Treasury curve.

- Yet, debt levels and funding needs remain very high in the face of an increasingly price-sensitive buyer.

- Given the inverted yield curve, low-cost T-bill ETFs like CLIP still offer the best risk/reward.

Government bond supply, rather than the Federal Reserve's policy rate path, has emerged as the key driver of Treasuries this year. If the market's reaction to this week's better-than-expected refunding announcement was anything to go by, this probably won't change anytime soon.

Not only did the Q4 refunding feature less overall issuance than consensus expectations (although not by much), but the continued focus on <12-month T-bills over longer duration/coupons also eased pressure across the rate complex. The Fed's dovish tone post-meeting didn't hurt either, indicating we're much closer to "done" than "one and done" at this juncture.

While longer-duration bonds have benefited the most from this week's developments, I still think going out in duration is risky. After all, deficit projections haven't eased (CBO's long-term projections are a sobering reminder for those who believe the current debt to GDP levels have peaked), and supply remains on a structurally higher path from here. At the same time, Treasuries are facing new demand headwinds in the face of quantitative tightening by the Fed and an increasingly price-sensitive foreign buyer.

With the short end of the Treasury curve offering the highest yields and suffering no demand shortfalls (so far), it's still hard to look past the risk/reward offered by low-cost T-bill ETFs like the Global X 1-3 Month T-Bill ETF (CLIP).

Fund Overview - Low-Cost Exposure to the Least Risky Part of the Curve

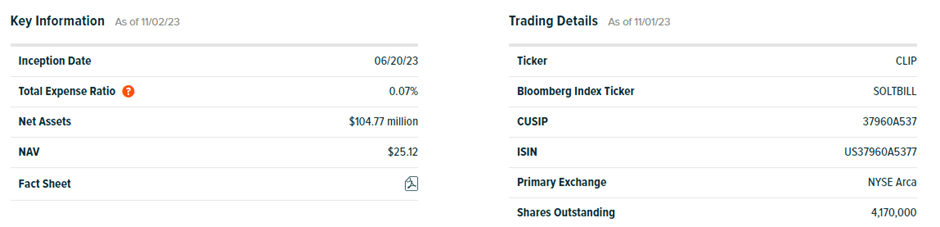

The US-listed Global X 1-3 Month T-Bill ETF offers investors access to a basket of US Treasury bills with a remaining maturity between one and three months by tracking (before fees and expenses) the Solactive 1–3-month US T-Bill Index. Having only been launched in June this year, CLIP is one of the smaller T-bill ETFs at ~$104.7m of assets under management at the time of writing.

CLIP makes up for its lack of a track record, though, with a very competitive 7bps expense ratio. By comparison, its key comparable, the iShares 0-3 Month Treasury Bond ETF (SGOV), charges 13bps gross (7bps net of temporary waivers), while T-bill ETFs targeting <12-month maturities like the SPDR® Bloomberg 3-12 Month T-Bill ETF ( BILS ) and the Goldman Sachs Access Treasury 0-1 Year ETF ( GBIL ) charge over 10bps.

{kind=link}

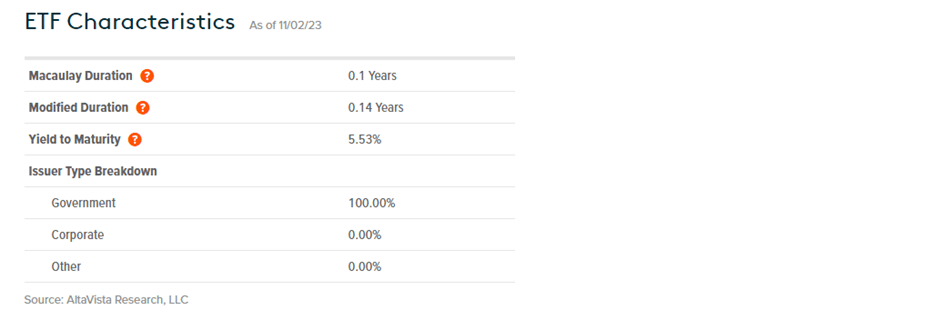

The fund is spread across 27 Treasury holdings, with a weighted average portfolio maturity of 0.1 years and an average yield to maturity of 5.5%. Specifically, the current portfolio composition is largely skewed toward December and January 2024 maturities, keeping the modified duration low at 0.14 years. Hence, CLIP has limited interest rate sensitivity (even vs. other short maturity T-bill ETFs), offering income while also shielding investors from rate fluctuations through the cycles. Distributions are made monthly and come with state and local tax exemptions.

{kind=link}

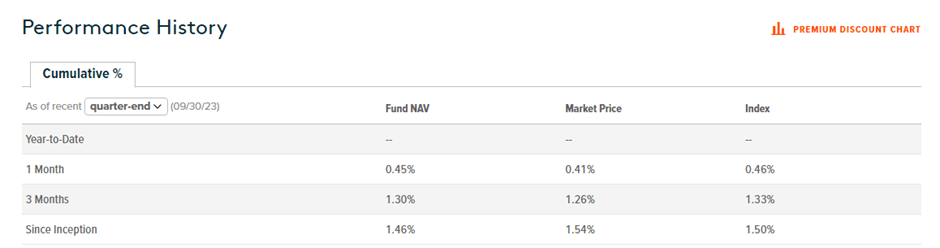

Performance-wise, CLIP's June inception means there isn't a lot to go on. Over the last quarter, however, the fund has appreciated a cumulative +1.5% in NAV and market price terms, slightly ahead of key comparable SGOV (+1.3%). Expect performance numbers to converge with comparable front-end funds over time, though the high >5% T-bill yields should boost CLIP's total return figures for now. While T-bills don't offer the kind of upside potential offered by equities and corporate bonds, CLIP's balance of income and principal protection is hard to match in the current environment of volatility, uncertainty, and un-inverting yield curves.

{kind=link}

Q4 Refunding Offers (Temporary) Relief

November's quarterly refunding is officially in the rearview mirror. For the most part, it was status quo, with the Treasury announcing another consecutive quarter of increased auction sizes up to the two-to-seven-year maturities. The surprise, though, was its decision to pare back new issuances at the longer end (i.e., the ten to thirty-year maturities), likely in reaction to rising term premiums in recent weeks.

{kind=link}

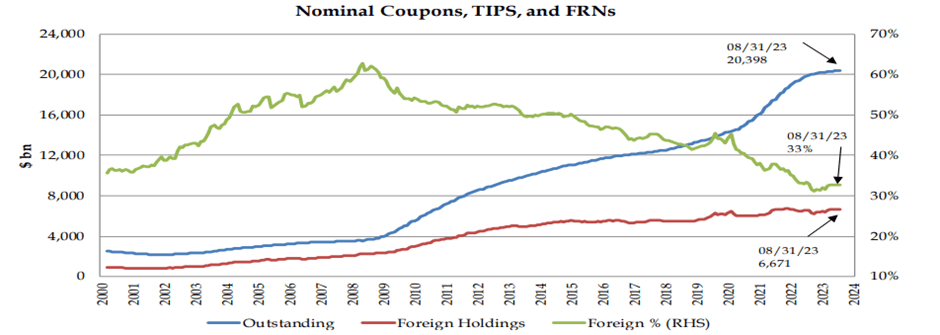

Importantly, we aren't yet out of the woods on auction size increases - the Treasury's guidance pointed to another quarterly increase in Q1 next year before pulling back in Q2 ( "increases beyond Q2 FY2024 may not be required" ). This seems optimistic, given funding needs aren't slowing down near-term - an ongoing high-single digits % YoY decline in receipts will likely bite once the elevated "Treasury General Account" (i.e., the US Treasury's checking account) balance runs down. And over the mid to long term, hopes that demand for additional supply will remain well-supported despite headwinds from banks (post-Basel Endgame) and foreign investors (particularly China) leaves little margin for error.

{kind=link}

Evidence from recent auctions supports the case that demand for >5% yielding T-bills is well-supported. Thus far, dealer bill holdings have remained in check in the face of a surge in recent bill supply, implying robust real money demand for these issuances. The same can't be said for longer maturity auctions , where dealer holdings have been on the rise, indicating an increasing price-sensitive buyer. Thus, expect bill supply to remain well above the recommended 15-20% range (as a % of debt outstanding), in turn, keeping the yield curve inverted for a while. Pending evidence that the Treasury can tap into the longer maturities without giving up some yield, I would stick to higher-yielding T-bills for now.

T-Bills Remain the Best Game in Town

The US Treasury's Q4 refunding announcement brought some much-needed relief to Treasuries, as a lower planned issuance schedule and continued emphasis on T-bill issuances (vs longer maturity Treasury bonds) kept a lid on yields at the long end. I'm not convinced it's time to take on duration risk, though, as the structural path for Treasury supply is still higher based on the CBO's long-term projections (vs an already elevated 120% debt to GDP currently). The Fed, while more dovish than usual thanks to the recent yield spike, is also a long way off cuts, particularly with the economy showing no signs of entering a recession. Plus, there's still plenty of demand uncertainty further across the curve, complicating the path to the Treasury's <20% T-Bill supply target (as a % of debt outstanding). Given the higher yields and better principal protection at the shorter end of the curve, CLIP screens attractively as an investment vehicle in the current backdrop.

For further details see:

CLIP: T-Bills Remain The Best Game In Town