CLPR - Clipper Realty: Don't Be Allured By The High Yield

2023-12-19 14:30:09 ET

Summary

- Clipper Realty is a residential/retail REIT that owns and manages properties in the New York metropolitan area.

- The company has a concentrated portfolio, which may be unattractive for investors seeking broader exposure.

- Even though the discount to NAV appears large and the dividend yield is high, its financial health is concerning, with high leverage, low liquidity, and a potentially unsafe dividend.

Clipper Realty Inc. ( CLPR ), founded on July 7, 2015 and headquartered in Brooklyn, New York, is a residential/retail REIT that owns and manages multifamily and commercial properties in the New York metropolitan area, specifically in Manhattan and Brooklyn.

Though its shares are trading at a very steep discount and the dividend yield is high, the REIT is overleveraged and illiquid and is growing at a very slow pace, and the distribution doesn't appear safe. If you're interested in CLPR and are curious about the thesis in support of these statements, read on.

Portfolio

As of September 30, 2023, the REIT operates in two distinct segments: Residential Rental Properties and Commercial ones. Here is the breakdown of Commercial and Residential revenue for the third quarter of 2023:

10-Q

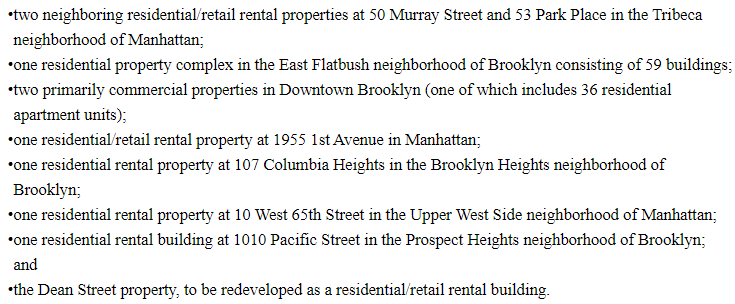

More specifically, these are the properties currently owned by Clipper:

{kind=link}

Obviously, this is not a very diversified portfolio, geographically speaking. Being confined in one corner of the country, no matter how populated, can be unattractive for investors who like residential REITs for a broader exposure to such assets.

Performance

At the end of the third quarter, Clipper averaged a 98% occupancy rate, showing exceptional efficiency in managing its assets. For context, consider that a much bigger residential REIT, Equity Residential ( EQR ), had an average 95.9% occupancy rate by the end of the third quarter.

However, though Clipper's revenue has been growing, its operating income and FFO haven't grown much since it was founded:

When it comes to more recent results, cash NOI and AFFO depict a more rapid growth, however. Below, I compare the figures from the last quarter on an annualized basis with the average annual figures from the past 3 fiscal years:

| Rental Revenue Growth |

| 12.31% |

| Cash NOI Growth |

| 22.84% |

| AFFO Growth |

| 45.48% |

With such a mixed picture related to its performance, it's not surprising that when it comes to CLPR's price, it has been a roller-coaster ride toward the low-single-digit:

If the operating results and a falling stock price were the only issues with Clipper, though...

Leverage

The worst problem with Clipper is the level of leverage it uses and how illiquid it appears in relation to both the amount and the cost of that debt. Its assets are 96.57% funded by debt, its debt-to-EBITDA ratio sits at 21.27x, and interest coverage is a dangerously low 0.62x.

As you can see from the charts above, leverage and liquidity only got worse as time went by. With such financial health, it's hard to appreciate the fact that there are no maturities in 2024 and that in 2025 only 6.6% of the total debt comes due.

Dividend & Valuation

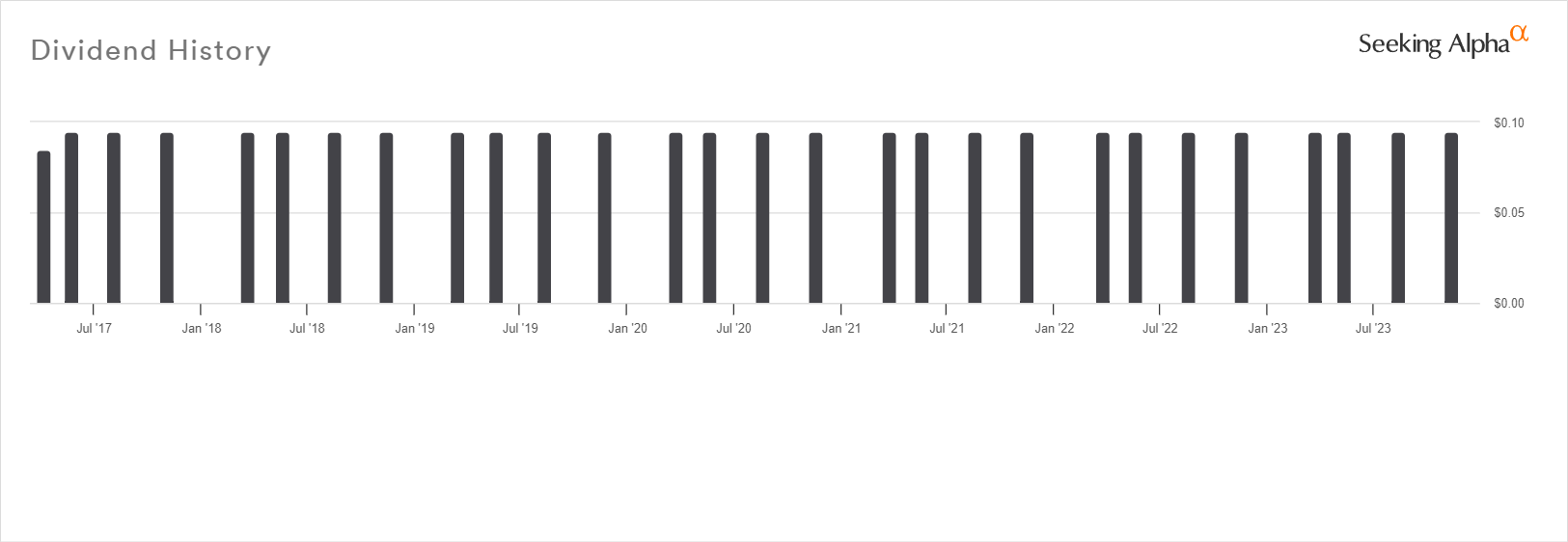

Clipper currently pays a $0.10 dividend per share, which suggests an 8.08% forward yield. Although the yield is high, even if the problems I mentioned above weren't present, I would be reluctant to capture it. Though the 67.70% payout ratio (based on last quarter's AFFO annualized) suggests that the current distribution is safe from a suspension or cut, the REIT doesn't have a long operating history, and the same applies to its dividend payment record which depicts almost no growth:

{kind=link}

Now, I have to admit that CLPR is pretty cheap right now, trading at a 6.13% implied cap rate. Using a 5% cap rate here is more appropriate, considering the median implied cap rate for residential REITs and the market average cap rate for multifamily properties. Using that then, NAV comes at $11.89 per share, which implies a 58.38% discount to NAV and a 140.28% upside from the current price if it ever reaches fair value.

But as we've seen above, there are multiple reasons why that large discount is justified. And it's time to sum them up.

Risks

First of all, there is a concentration risk as all of Clipper's assets are in New York. Though the markets it operates in are far from unattractive, other REITs with properties across multiple states can hedge some of the risk that comes from market rent changes, unemployment rate, population, etc.

There is also a lot of debt that this REIT carries, and its low liquidity presents dangers. It's also very difficult to become a CLPR shareholder without worrying about your capital being at risk when the company's leverage keeps rising and its liquidity keeps drying up.

Further, I don't trust that the dividend is safe even when the payout ratio leaves a good margin of safety. The yield is very attractive, but the company doesn't seem intent on ever raising the dividend, and it's been about 8 years now. It's likely that the REIT cannot afford to. And if that is so, then it's also likely this is as high as they can keep it for now; should profitability worsen, a suspension or cut is possible.

Though the discount that the market offers here is very generous, the upside may never be realized if there are no drivers in place to change the market's perceptions. And frankly, I don't see why the market should change its mind.

But even if the upside is realized, how much time will this take? Can investors afford the opportunity cost they might incur in the meantime? As long as Clipper doesn't give a good reason, the answer is probably "no".

Verdict

That is why I am assigning a hold rating for CLPR and recommend investors consider other opportunities. Clipper will need to become more profitable, decrease its leverage, start expanding in more markets, and commit to increasing its dividend before it's worthy of another look.

At some point above, I mentioned Equity Residential, which I happened to cover not long ago here . You may want to take a look at that REIT if you're looking for residential real estate exposure. Though the stock price has increased 13.29% since I published it, the margin of safety remains attractive.

What are your thoughts? Do you own CLPR or intend to? Why or why not? Let me know below, and I'll get back to you as soon as I can. Thanks for reading!

For further details see:

Clipper Realty: Don't Be Allured By The High Yield