CLPR - Clipper Realty: How Sustainable Is The 7.7% Dividend Yield?

2023-12-19 04:12:46 ET

Summary

- Clipper Realty is currently paying out a 7.7% dividend yield.

- The most recent distribution was 158% covered by its third quarter adjusted FFO.

- Its long-dated maturity profile and high insider ownership have reduced the likelihood of a dividend reduction.

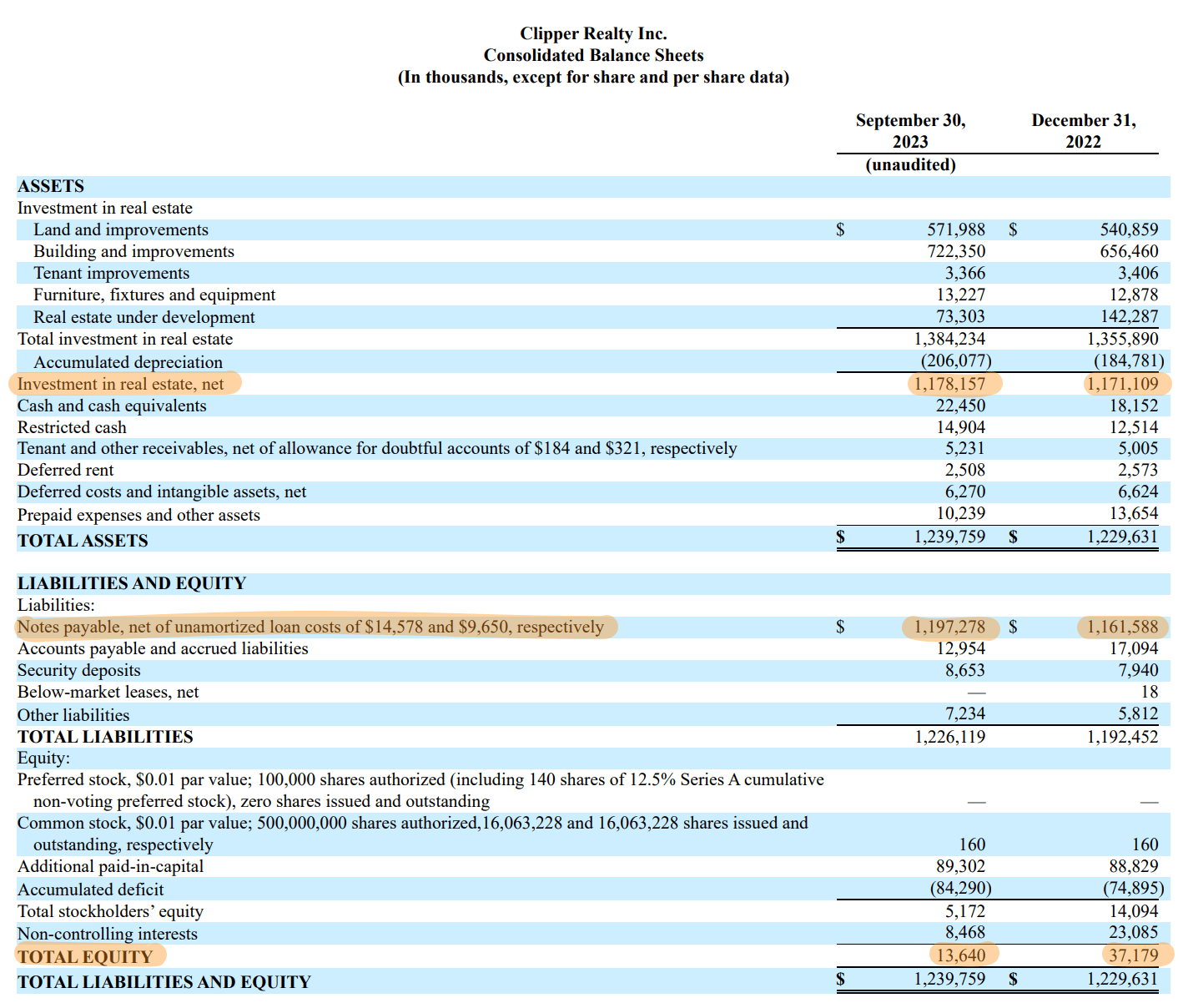

Clipper Realty's ( CLPR ) dividend has so far defied calls for a cut with the Brooklyn-based REIT last declaring a quarterly cash dividend of $0.095 per share , unchanged sequentially for what's currently a 7.7% annualized dividend yield. This is high and forms a near-record dividend yield for CLPR. The dividend is tempting but the REIT faces quite intense headwinds from an overleveraged balance sheet besieged by declining equity against an elevated interest rate environment. CLPR's total debt at the end of its recent third quarter stood at $1.2 billion with its market cap currently at $210 million. This drove a record quarterly interest payment during the quarter of $11.5 million, roughly 33% of total revenue.

CLPR's leverage is staggering with total shareholders' equity at just $13.6 million at the end of the third quarter. This figure has been in constant decline since the REIT went public and could flip negative. It has been the core factor driving the commons to ever lower levels. However, whilst CLPR is down 27% year-to-date, rate cuts could be coming to deliver a boost to adjusted FFO that came in at $0.15 per share during the third quarter. This meant the REIT covered its dividend by 158%.

Further mitigating the specter of a dividend cut is the extremely high 62% insider ownership. To be clear, the dividend is the only factor driving a realizable return for insiders whose stake has lost a significant amount of value since the pandemic.

The Balance Sheet

{kind=link}

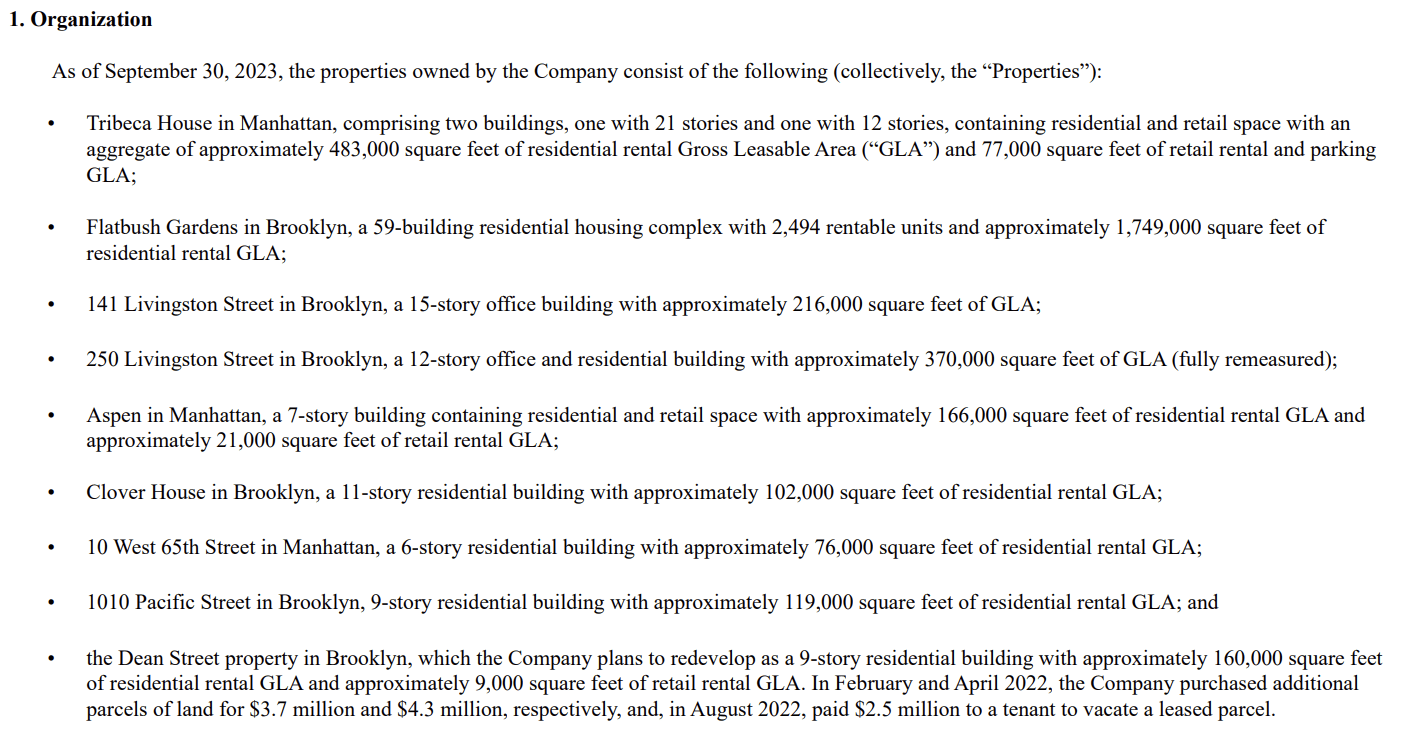

CLPR owns a mix of commercial and residential properties in New York City including Flatbush Gardens in Brooklyn, a 59-building housing complex with 2,494 rentable units, and a 15-story office building 141 Livingston Street which has 216,000 square feet of GLA. These drove total revenue of $35.1 million for the third quarter, up 7% over its year-ago comp but a miss of $1.62 million on consensus estimates. Residential properties contributed 73% of total third-quarter revenue and 59% of income from operations.

{kind=link}

The market is looking at the balance sheet for direction with total equity dipping by $23.54 million since the end of 2022. Hence, assuming the same $7.85 million per quarter decline in total equity is realized in future quarters, CLPR would see this figure come in negative by its fiscal 2024 first quarter. Such a negative inversion would be close to placing the commons in uninvestable territory.

{kind=link}

This is where the argument for dividend cuts comes from. However, the REIT is currently only paying out roughly $4 million every quarter as a dividend. This really won't make a substantial dent in debt repayments and the resulting selloff from a dividend cut would be destructive as it would counter the only other reason for holding the commons. I have some confidence that the dividend will be maintained against the high insider ownership, strong coverage, and the limited benefits of a dividend reduction.

Debt Maturities And Impact Of Interest Rate Cuts

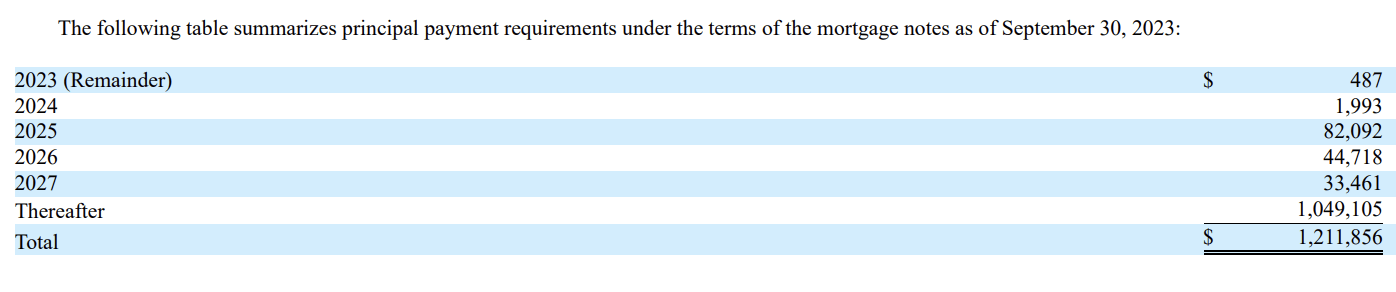

CLPR's balance sheet is its enemy. The REIT held cash and equivalents including restricted cash of $37.4 million at the end of its third quarter. This figure sits at its lowest level since the pandemic but the dip on the back of rising interest payments has moderated. It was up by $6.4 million sequentially and from $35.5 million in the year-ago comp on the back of new debt. The criticality of what's a broadly constrained liquidity position is mitigated by CLPR's healthy and long-dated debt maturity profile.

{kind=link}

CLPR only has $490,000 of debt left to pay down this year and another $2 million coming due in 2024. 2025 will see $92 million come due but interest rate cuts should have been well realized by then with the Fed's December dot plot setting out at least 3 cuts of 75 basis points through 2024. There could be 2x this amount according to the CME's FedWatch Tool with current market expectations majority leaning towards interest rates exiting 2024 at 3.75% to 4.00% .

{kind=link}

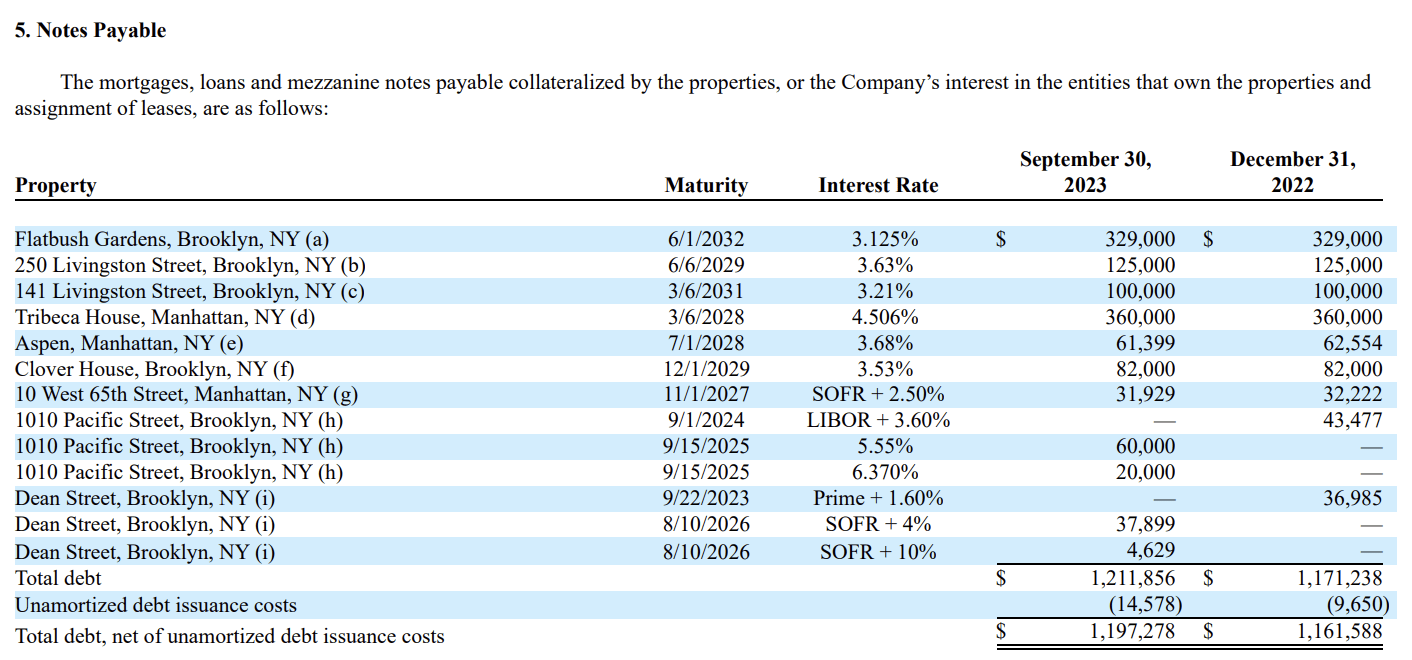

The REIT's debt is all secured on its underlying properties with the largest of its properties having largely fixed-rate debt. Hence, whilst its interest expenses have risen, the highly fixed-rate nature of its balance has meant that CLPR has been somewhat shielded from the Fed's fight with inflation. Do I think the common shares are a buy? No. However, the dividend seems to be more sticky than implied by the yield. I'm not a buyer here but this is a hold.

For further details see:

Clipper Realty: How Sustainable Is The 7.7% Dividend Yield?