CLM - CLM: One Cut Down Several To Go

2023-12-05 13:25:43 ET

Summary

- CLM's distribution strategy relies heavily on divestitures of its asset base, making it unsustainable.

- The recent dividend cut did not significantly improve CLM's prospects, as the forward annualized dividend yield is still overly aggressive.

- CLM's reliance on capital gains and paid-in capital to cover its dividend creates several areas of concern, making it a speculative investment.

- Given that the underlying equity portfolio of CLM is already richly valued and the CLM's NAV premium has been compressed, it seems very likely that CLM will be forced to revise its dividend policy again.

About three months ago I issued an article on Cornerstone Strategic Value Fund ( CLM ) indicating that the Fund is a structural value trap.

Among the numerous reasons, the key driver behind my assumption that CLM is a value trap was founded on the mechanics of how CLM distributes cash flows to its shareholders.

CLM's strategy is to provide high yielding dividend in order to attract a base of investors, who prefer notable streams of current income and are willing to sacrifice the capital gains component for it.

However, in this case specifically, we are talking about a considerable disconnect between the dividend and the net investment income. For example, the annual net investment income constitutes less than 1% of the total NAV, while the current distribution level is close to 20%. This means that in order to cover the massive yield (i.e., close the gap between net investment income and distribution level), CLM has to rely heavily on the divestitures of its asset base.

In my opinion, that was and still is an unsustainable strategy.

About a month ago, CLM was forced to cut its dividend by ~12% to eliminate some of the pressure on the NAV base.

{kind=link}

YCharts

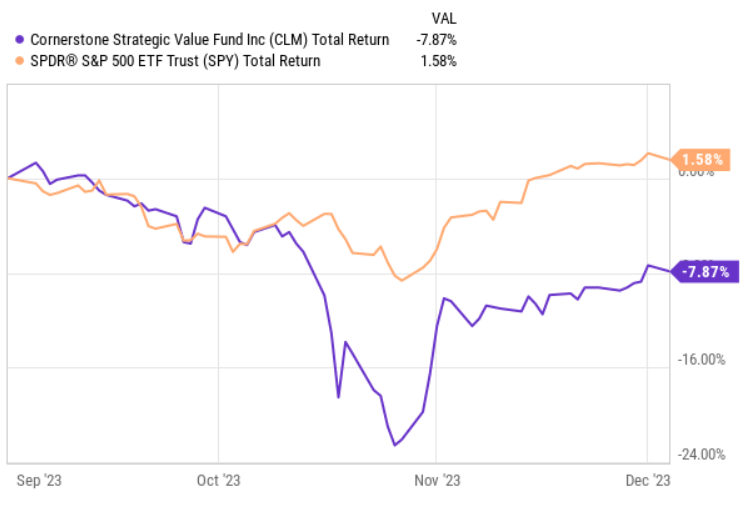

As a result, since the publication of my article, CLM has clearly underperformed the market registering a negative return of ~8% (on a total return basis).

Again, this is not a huge surprise and is only a natural consequence stemming from an aggressive distribution policy; just as outlined in my previous article :

While CLM's dividend distribution policy might seem attractive, given that a heavy portion of the distributions are funded by selling part of the existing asset base, it becomes a constant battle with NAV erosion.

Thesis update

Let's now take a look whether CLM's prospects have improved after the relatively recent dividend cut.

Currently, the forward annualized dividend yield lands at 19.9% (even after the dividend cut), which already seems overly aggressive.

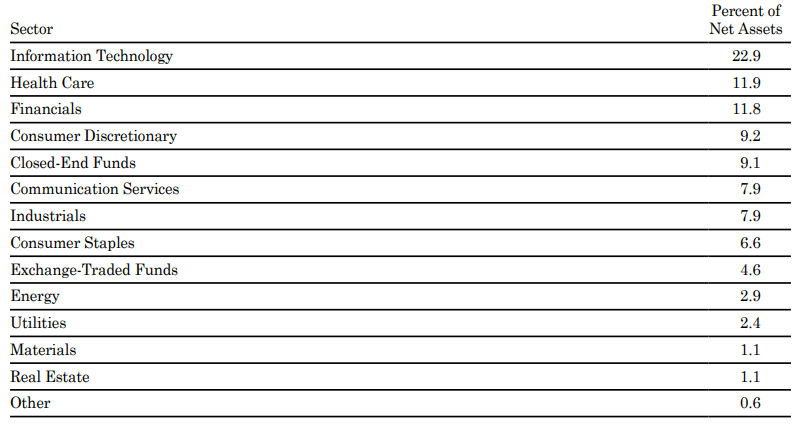

At the same time, the breakdown of net assets does not indicate any notable positions in sectors or asset classes, which inherently generate attractive dividends that could potentially reduce the delta between CLM's dividend and net investment income.

{kind=link}

CORNERSTONE STRATEGIC VALUE FUND, INC

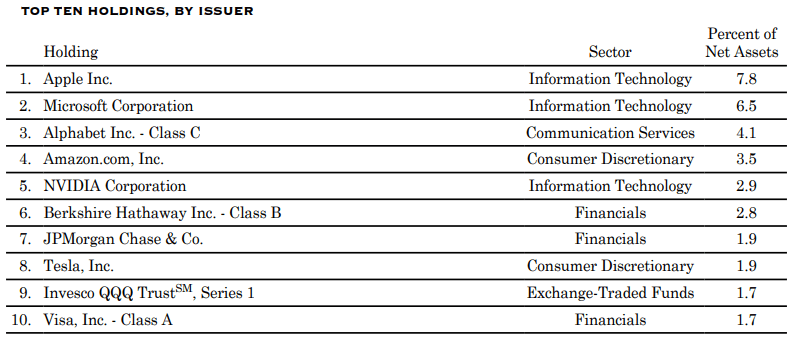

We can confirm this by looking at the Top 10 holdings.

{kind=link}

CORNERSTONE STRATEGIC VALUE FUND, INC

Almost none of the Top 10 positions provide attractive yields. Instead, we can see that there is a heavy skew towards large cap growth names, where CLM has to rely on the corresponding capital gains component to fund its ~20% dividend.

{kind=link}

Cornerstone Strategic Value Fund, Inc

The most recent distribution that was made in November was supported by a combination of net investment income, net realized capital gains and paid-in capital.

Net investment income in this case accounted for ~5% of the total dividend. If we based this calculus on the post-cut dividend, the relevant percentage would increase to ~6%.

Hence, investors have to understand that the revised dividend does not in any shape or form move the needle. CLM is still dependent on capital gains (or price appreciation) of the underlying equity investment portfolio.

Plus, what is rather CLM specific is that the shareholders carry an option of replacing their dividends with additional shares, thereby supporting the NAV base at CLM. This is a major source for CLM since after net investment income and capital gains there is still ~61% left of the dividend amount that has to be covered by paid-in capital.

All of this translates to several areas of concern that, in my opinion, should justify the argument of avoiding CLM:

- Unsustainable distribution strategy - the fact that even after the dividend cut CLM still has to rely heavily on the inherently more volatile source of funding (i.e., capital gains) does not send comforting signs for the overall sustainability of the dividend.

- Volatile equity positions - despite the embedded dependency on capital gains, the underlying equity portfolio entails a pure exposure towards beta risk. The breakdown of sectors and top holdings largely resemble the S&P 500, which currently is very close to the all-time highs. So, the combination of a lack of any risk mitigating strategy on the beta factor, and the market near all-time highs, creates an unfavorable basis from which to continue the reliance on future capital gains.

- Unpredictable paid-in capital - as stated earlier CLM supports its massive yield to a large extent via the distribution of the paid-in capital. This, in turn, implies an unpleasant risks, where in case new flows and/or dividend reinvestments decrease to a level, where CLM has to divest parts of its equity portfolio, investors should be fully ready to accept further dividend cuts. Alternatively, CLM could decide to embark on a more speculative approach by keeping the dividend unchanged and instead selling equity positions. Yet, if markets do not recover and there are still no changes in the net flows, CLM will have to inevitably make material revisions in its distribution policy.

The bottom line

All in all, despite the revised dividend level, CLM still remains a speculative vehicle. In my opinion, investors should factor in a notable probability of experiencing incremental dividend cuts because of the current dynamics in the S&P 500 in conjunction with a dependency on further capital appreciation to at least partially narrow the gap between dividends and the generated returns.

Finally, given that ~60% of the dividends are funded by the paid-in capital, CLM has to have positive net flows and a premium on its NAV. Now, when CLM is down it seems that the premium is getting smaller making the strategy unsustainable. The fact that CLM had to decide on a decreased dividend is a clear indication of that, where supporting the juicy yield was not possible with the existing levels of net income, capital gains and paid-in capital.

With that being said, I would not feel comfortable shorting CLM either because in that case investors would be to a large extent short the S&P 500, which in the event of additional gains could provide support for CLM in the form of more ample capital gains component that could help CLM protect its dividend for some time.

For further details see:

CLM: One Cut Down, Several To Go