CLX - Clorox: Cyberattack Compounds Existing Challenges

2023-10-10 10:17:53 ET

Summary

- Clorox benefited from COVID-19 but faced slowed growth, cyberattacks, despite their IGNITE strategy and tech investments.

- Clorox faces rising costs and recession fears, compounded by cyberattacks, but should show resilience thanks to a strong brand portfolio.

- After the cyberattack, Clorox's Q1 2024 outlook worsens; concerns arise over sustaining dividend aristocrat status.

- Assuming a moderate decline resulting from the recent cyberattack, Clorox’s current price suggests moderate returns.

Investment Thesis

I believe The Clorox Company ( CLX ) is a hold at its current position. The company, which saw a significant boost during the COVID-19 pandemic due to heightened demand for its products, is now navigating a series of challenges. Post-pandemic, Clorox's growth trajectory has decelerated notably. While their IGNITE strategy and tech investments were designed to fortify their market stance, the recent cyberattack underscores their vulnerability to digital threats. This setback is compounded by rising operational costs and potential economic downturns. Yet, Clorox's robust brand portfolio may offer some resilience amidst these adversities. The dampened outlook for Q1 2024, especially after the cyberattack, raises questions about their capability to uphold their dividend aristocrat status. Given the current stock price, projections suggest only moderate returns ahead. With the lingering uncertainties post-cyberattack, it's prudent to adopt a wait-and-see approach, thus making Clorox a hold in the near term.

Company Overview

The Clorox Company is a prominent multinational manufacturer and marketer of consumer and professional products, with a significant presence in over 25 countries or territories and distribution in over 100 markets. However, despite its global reach and a diverse portfolio of trusted consumer brands such as Clorox bleach, Pine-Sol cleaners, and Liquid-Plumr clog removers, the company recently faced a major cybersecurity attack that disrupted its operations. Clorox also caters to professional customers with its CloroxPro and Clorox Healthcare brands. Organized into segments like cleaning products, household items such as bags and wraps, and lifestyle products including food and water-filtration, Clorox typically markets its top brands in midsized categories, focusing on financial attractiveness.

Recent Innovations Not Enough To Prevent Cyber Attack

I believe Clorox was one of the companies that benefitted from the outbreak of COVID-19 pandemic. The unprecedented surge in demand for disinfecting products during the pandemic was a clear reflection of the global urgency to maintain hygiene and curb the spread of the virus. Brands like Clorox became household staples, almost overnight. We saw this reflected in their overall sales and income which increased during the pandemic years. However, over the past few years, as we have transitioned into a post-pandemic world, this heightened demand has subsided, and growth has slowed considerably which has the left the company in a position where management are seeking to revitalize growth and control expenses. Management is aiming to achieve this by continuing to invest into innovation which they mentioned throughout their most recent earnings call although this has been significantly set back following a recent cyber-attack .

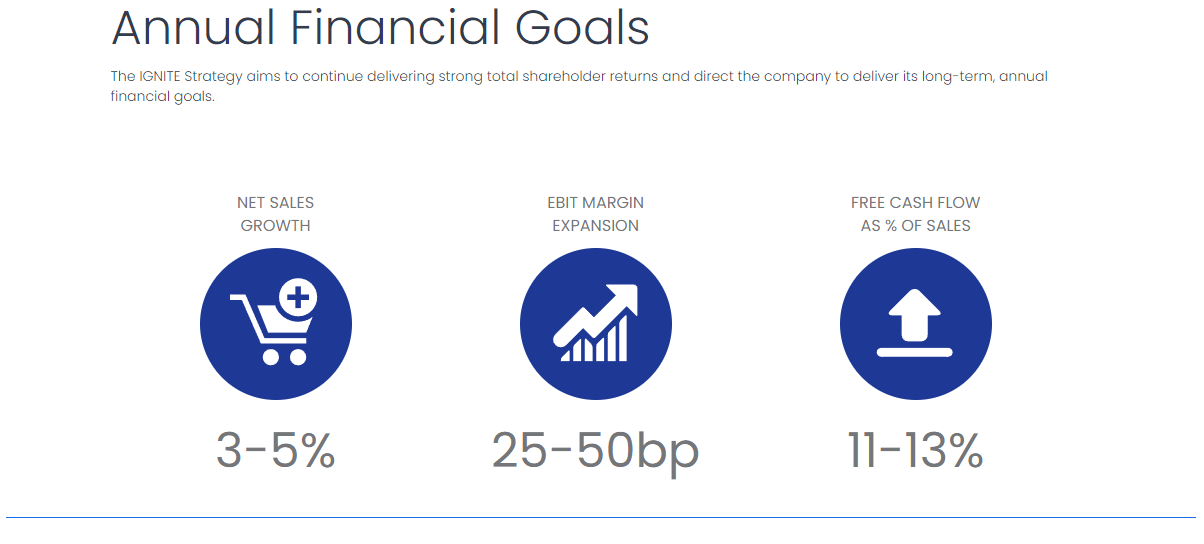

In 2019, Clorox introduced their IGNITE strategy which is designed to accelerate innovation in key areas of the business to drive growth and deliver value for all its stakeholders. The strategy is underpinned by Clorox's purpose and enduring values. The strategy focuses on four strategic choices, being to fuel long-term growth, innovate consumer experiences, reimagine how the company and its employees work, and continuously evolve the product portfolio.

CLX's Annual Financial Goals (The Clorox Company)

{kind=link}

As part of this strategy, Clorox announced in August 2021 to invest approximately $500 million over five years in transformative technologies. Beginning in fiscal year 2022, a significant portion of this investment is directed towards replacing the company's existing enterprise resource planning ((ERP)) system. Transitioning to a cloud-based platform is a strategic move, given the scalability, flexibility, and cost efficiencies cloud solutions typically offer. Yet despite this investment in their online infrastructure, the company failed to prevent a cyber-attack that has massively damaged the company.

The Clorox cyberattack highlights the vulnerability of even well-prepared companies in today's digital landscape. Despite a $500 million investment in IT and notable cybersecurity recognition, Clorox suffered a breach that disrupted operations and impacted its supply chain for weeks. This incident led to a significant 23-28% drop in quarterly sales, equating to over $500 million in lost revenue, and a substantial decline in stock value by over $3 billion.

In my opinion, what's concerning is the apparent lack of tech expertise in Clorox's board, emphasizing the need for companies to have tech-savvy leadership. I believe tools like X-Analytics are essential for boards to gauge and mitigate cyber risks effectively. Moreover, the focus should shift from merely preventing cyberattacks to managing their consequences. This cyber-attack is also occurred during a time in which Clorox was dealing with other significant challenges.

Rising Costs And Macroeconomic Uncertainty Persist

Outside of the recent attack, the company continues to be under pressure from rising costs as well as the uncertainty surrounding the macroeconomic situation continue to impact the business. In the most recent earnings, management mentioned they are anticipating a mild recession in the latter half of their fiscal year which they recognize will impact their top and bottom line of their business.

Even with a mild recession, the company anticipated a sales growth of up to 2 percent compared to the prior year which I think highlights the robust nature of the Clorox and its diverse portfolio of product offerings, although the company is expected to revise this down in the Q1 call given the recent cyber-attacks. Looking past the cyber-attacks however, which management believe they now have more control of , when reflecting on Clorox's performance during the Global Financial Crisis ((GFC)), it's evident that the company's resilience and adaptability have been hallmarks of its strategy, even during challenging economic times. During the GFC, Clorox saw an approximately 2% decline in sales whilst metrics such as earnings per share ((EPS)) saw a moderate increase of approximately 3%. It's worth noting that companies with strong brand portfolios, like Clorox, often have a competitive advantage during economic downturns. Trusted brands tend to retain customer loyalty, which can provide a buffer against declining sales. This was also reflected in the share price of CLX which only had a moderate decline during the GFC compared to other businesses which saw far greater declines, although during this period the company was not grappling with souring costs and a cyber-attack like it is now.

The escalating cost inflation Clorox has grappled with over the past few years is staggering. An $800 million hit in fiscal year '22, followed by $400 million, and now a projected $200 million for the current year paints a picture of a company under significant pressure. These inflating costs, driven by commodities and labor, are reflective of broader market trends. Many industries are feeling the pinch from rising raw material prices and labor costs, especially in the post-pandemic era. However, Clorox's situation is somewhat unique due to its diverse product portfolio, which ranges from cleaning supplies to charcoal with its Kingsford business, meaning the company must manage a complex network of diversified supply chains.

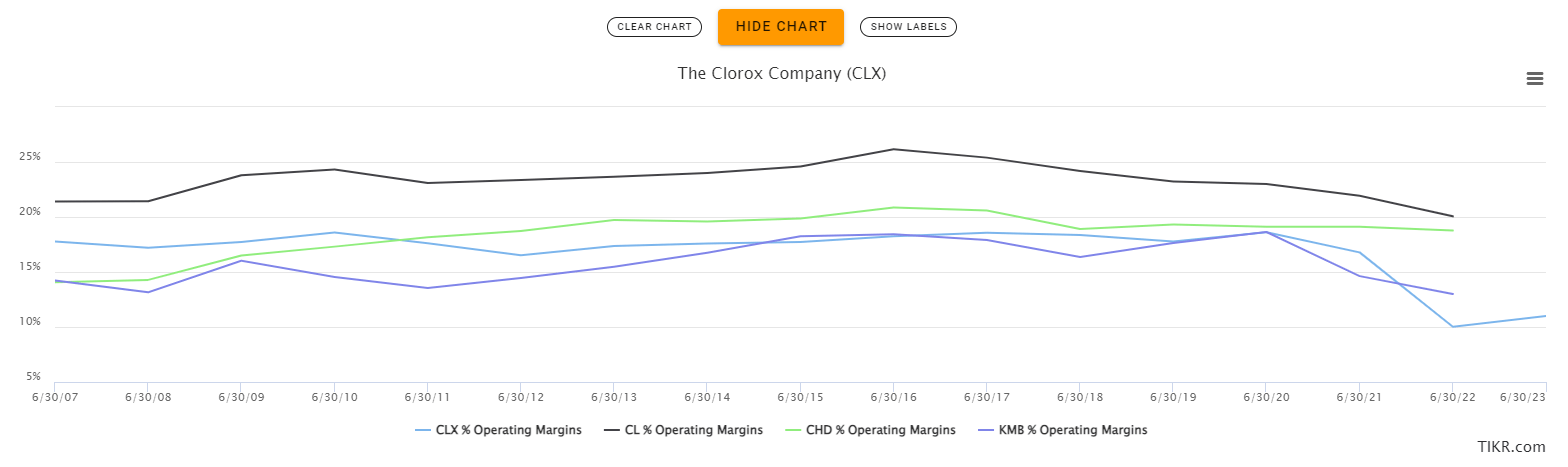

The rising costs, predominantly from commodities and labor, have inevitably squeezed Clorox's margins. With every uptick in raw material prices or wage rates, the company's profitability takes a hit. This decline in profitability, driven by shrinking margins, is concerning. Since the pandemic year of 2020, where operating margins were 18.6%, Clorox has seen a sharp decline of margins to 11% in 2023. A consistent decline could signal deeper structural issues or an inability to pass on rising costs to consumers. The company has attempted to counter these rising costs by increasing prices 4 times recently , however if Clorox cannot control costs and keep raising prices, consumers may begin to seek alternatives, and this is something that I will be following closely as this may impact the business profoundly especially given that their closest competitors have not seen margins decline as steeply. All of these concerns combine to present a tough short-term outlook for the company, which may present an opportunity for long-term investors.

Comparison of Operating Margins for CLX and its Competitors (TIKR)

{kind=link}

Financial Analysis

As of 2023, The Clorox Company has demonstrated commendable financial performance. The rise in revenue over the past year is noteworthy, achieving 4% growth from $7.11 billion in 2022 to $7.39 billion in 2023.

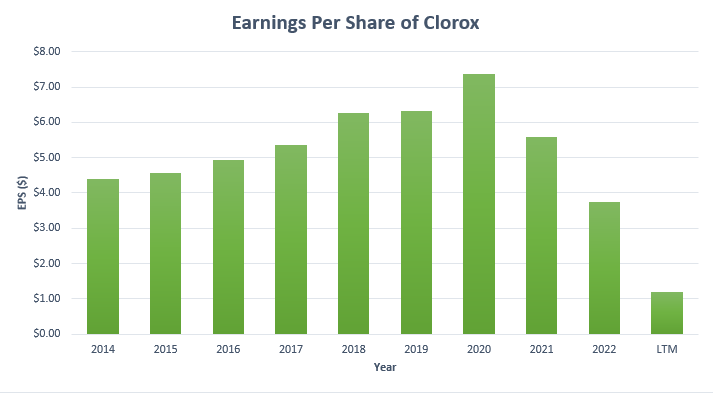

The EPS for Clorox stands at $1.20. It's essential to consider the broader context when evaluating this figure, especially given a large portion of the decrease was due to the noncash impairment charges on assets related to the Vitamins, Minerals and Supplements ((VMS)) business. That being said, when not factoring in the VMS impairment, there has still been a significant decline from the EPS of $6.26 five years ago. .

{kind=link}

The balance sheet of Clorox has struggled in recent years, characterized by rising liabilities and declining shareholder’s equity. The company's Book Value Per Share ((BVPS)) has also seen a sharp decline since in the past 3 years, from $7.20 in 2020 to $1.78 in 2023. This indicates that Clorox has not been effective in building its intrinsic value and highlights the company’s struggles to manage costs and liabilities in recent years.

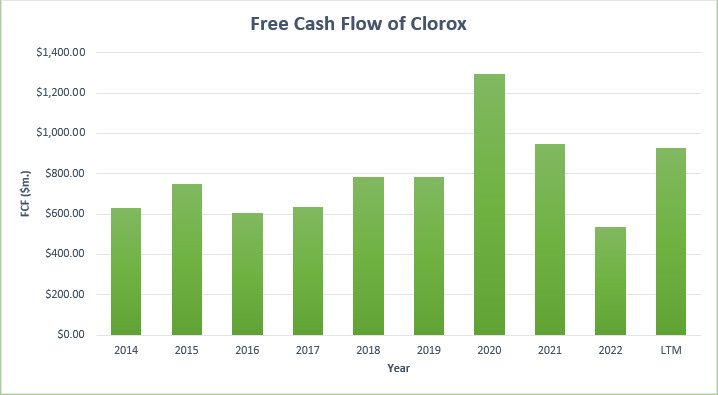

Despite that, the management team at Clorox has shown financial responsibility, especially in their approach to managing debt, which has steadily declined since 2020. Given Clorox's cash and cash equivalents of $367 million and their free cash flow ((FCF)) of $930 million 2023 and their proven track record of solid FCF yields, I am not too concerned with the company’s debt levels and believe they are in a solid position to meet its short-term obligations.

{kind=link}

In the aftermath of a significant cybersecurity attack, Clorox has released preliminary financial data for Q1 of fiscal 2024 . Net sales are expected to drop by 23% to 28% year-over-year, with organic sales decreasing by 21% to 26%. This decline is largely due to disruptions from the August cyberattack. The company's gross margin is also anticipated to decline, and diluted EPS could range between a loss of $0.75 to $0.35. Clorox foresees operational challenges in the next quarter but expects improvements as operations normalize. A detailed outlook will be presented in their November earnings call. This outlook is far worse than what the company was initially anticipating prior to the cyber-attack which I think highlights just how damaging they were.

Overall, it’s clear that Clorox has some substantial challenges in the short to medium term which have been exacerbated by the recent cyber-attacks. The company has a history of stability during economic downturns and has shown a dedication to its shareholders in the form of a strong dividend which has established them firmly as a dividend aristocrat . I am however, concerned as to whether Clorox will be able to sustainably maintain this title in the next year given their most recent payout ratio was 391% and that I anticipate their earnings to get worse next year.

Valuation

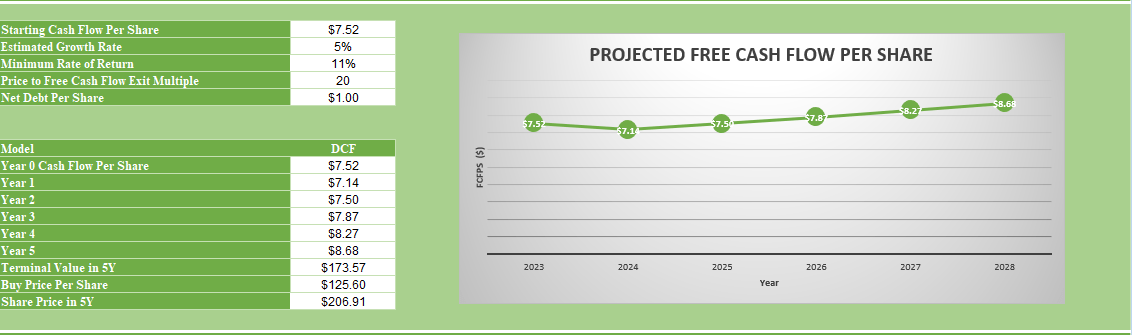

In my view, a company's valuation should reflect a balance between its market capitalization and the foundational business metrics, especially projected earnings. A tool I often lean on to gauge this is the discounted cash flow ((DCF)) methodology. As of the most recent quarter, CLX’s FCF per share was $7.52. Given its recent challenges like the cybersecurity attack, I anticipate the company to fall approximately 5% this year and FCF annual growth rate of 5% in the years following that. Taking this growth into account, the projected cash flow for Clorox by the end of the 5 year period would be at $8.68.

Using an exit multiple of 20, which is approximately where I anticipate the company to trade at over the next 5 years, the estimated price target for the stock in five years would be $206.91. Therefore, if you invest in Clorox at its current share price, the expected Compound Annual Growth Rate ((CAGR)) would be 10.5% over the next five years, based on these calculations. This is assuming the company experiences moderate declines resulting from this cyber-attack, the damage of which will not be known until the company discusses further in their Q1 earnings call. Based on the projected return without any margin of safety, and the uncertainty surrounding recent events, I believe CLX is a hold currently.

{kind=link}

Conclusion

Clorox, which initially benefited from the COVID-19 pandemic, has recently faced a series of challenges. Although Clorox experienced an initial surge in demand due to the pandemic, it now faces a transition phase marked by decelerated growth and emerging challenges. Their IGNITE strategy and significant investments in technology were aimed at bolstering the company's position, but they were not immune to cyber threats, as evidenced by the recent cyberattack. This comes at a time when Clorox is grappling with rising costs and looming recession fears. However, the strength of their brand portfolio suggests potential resilience in these challenging times. Their Q1 2024 outlook, post-cyberattack, has dampened, raising concerns about their ability to maintain their esteemed dividend aristocrat status. While the company's current stock price indicates moderate returns in the future, the full impact of the cyberattack remains to be seen, making the company's trajectory uncertain in the near term.

For further details see:

Clorox: Cyberattack Compounds Existing Challenges