FMY - Closed-End Funds: Investment-Grade Corporate Fixed-Income Exposure To Consider

2023-12-03 02:34:21 ET

Summary

- Investment-grade corporate-focused closed-end funds offer attractive fixed-income options with higher yields in the current higher-rate environment.

- Leverage and discounts/premiums in CEFs add volatility to consider when investing in these funds, which would otherwise be for more conservative investors.

- Besides the higher yields, when rates decline investment-grade funds should see a significant rebound, adding a catalyst for potential upside and 'locking in' higher yields now.

Written by Nick Ackerman, co-produced by Stanford Chemist.

Several readers have been asking about investment-grade corporate-focused closed-end funds. In the CEF space, there aren't too many pure-play options, but there are a couple and a few offerings that also incorporate a tilt toward investment-grade quality. Fixed-income options are more attractive these days, with higher rates leading to higher yields.

Of course, heading through the last couple of years with a rising rate environment meant these funds saw meaningful losses. As yields rise, bond prices fall, leading to net asset value declines. That said, this is the other appealing aspect of investment-grade quality as this could now go in the reverse; if rates are set to decline in the next couple of years, there could be some potential upside, and we would be 'locking in' higher yields (assuming no distribution cuts, which isn't guaranteed as several funds are overpaying.)

In general, investment-grade fixed-income investments are attractive options for a more conservative investor. However, in the CEF space, leverage is often employed, so being aware that that adds additional volatility is important. On top of this, the discounts/premiums that CEFs can trade at add further volatility to consider.

Some Funds For Consideration

With that being said, I wanted to highlight several funds in the space that could be worth consideration. Those include Western Asset Premier Bond Fund ( WEA ), Western Asset Investment Grade Income Fund ( PAI ), Western Asset Investment Grade Defined Opportunity Trust ( IGI ), Western Asset Global Corporate Defined Opportunity Fund ( GDO ), BlackRock Core Bond Trust ( BHK ) and BlackRock Credit Allocation Income Trust IV ( BTZ ).

These CEFs represent funds that are either nearly entirely or tilting toward investment-grade exposure. That said, IGI and GDO are a bit unique pair as they were both launched in 2009 and were clearly a 'pair.' One being U.S.-focused specifically and the other global. That said, I would exclude those from today's discussion because they are term funds set to terminate on December 2, 2024. That means they might not even be around for too much longer.

Additionally, there are a couple of funds, such as BlackRock Enhanced Government ( EGF ), MFS Government Markets ( MGF ) and MFS Intermediate Income ( MIN ), which are going to be considered investment-grade but lean heavily toward U.S. Treasury debt or other U.S. Government exposure. These funds could be fine, but even with higher yields, the higher expense ratios that often come with closed-end funds don't generally justify these sorts of funds as being particularly attractive. If one wants to hold them for other more tactical purposes, that could be a different story. However, in those cases, I'd still probably lean toward ETFs instead.

That's similarly the case for funds such as First Trust Mortgage Income Fund ( FMY ) or BlackRock Income Trust ( BKT ), which are heavily invested in agency MBS. All could be worth considering, but not really what I'm leaning toward when looking at, more specifically, investment-grade corporate debt.

With that, here is a look at the portfolio allocations in terms of credit quality and whether they are leveraged for the remaining funds. As a reminder, anything BBB rated and higher is investment-grade and below that would be high-yield/below-investment-grade or "junk." The "not rated" category will be included in the high-yield allocation. The cash allocations are excluded from the weightings.

Additionally, this data is from each fund sponsor's website at the time of writing, so the data is accurate as of November 18, 2023.

| Ticker |

| IG Allocation |

| HY Allocation |

| Leverage |

| WEA |

| 69.97% |

| 28.61% |

| 28.11% |

| PAI |

| 92.19% |

| 6.88% |

| N/A |

| BHK |

| 88.56% |

| 29.95% |

| 37.31% |

| BTZ |

| 67.47% |

| 47.08% |

| 37.11% |

Here is a look at a small basket of funds and their performance for the last decade. I've also included the iShares iBoxx $ Investment Grade Corporate Bond ETF ( LQD ) for some. I've also included GDO and IGI for some historical context.

Ycharts

As we can see, each of the presented funds discussed today has outperformed the passively managed LQD. This could be because LQD actually carries a higher allocation to the upper side of the credit quality spectrum.

High yield during this time performed better, so even having a small amount of exposure for these CEFs could have been helpful for this outperformance. For high-yield exposure, we can use iShares iBoxx $ High Yield Corporate Bond ETF ( HYG ) for some context.

Ycharts

More specifically, we can give a look at the performance of these funds from the beginning of 2022 to today. This would encompass the rising rate environment we've been seeing. In this case, we've seen losses across the board as rates were rising. Of course, this was as expected, as these funds have pretty high durations, indicating that they are more interest rate-sensitive.

Ycharts

Once again, high-yield exposure performed better. We still saw losses, but being less interest-rate sensitive, this is to be expected.

Ycharts

BTZ And BHK

In terms of the BlackRock funds, BHK and BTZ, over the longer term, they've provided competitive results. BHK really started to diverge when rates started heading higher, which is surprising because it has the lowest duration currently at 5.97 years. The fund even has a decent discount relative to BTZ.

This highlights one of the bigger problems with BHK currently and what makes it not too attractive at this time. BHK is trading above its average discount, while BTZ is trading below this level.

Ycharts

Perhaps some would argue that it is justified due to better performance. It was the better performer over the last decade and beat out BTZ during the rising rate environment. That said, better historical performance is never guaranteed to happen going forward. Both the funds also carry a fairly elevated amount of leverage and come in with lower distribution coverage ratios.

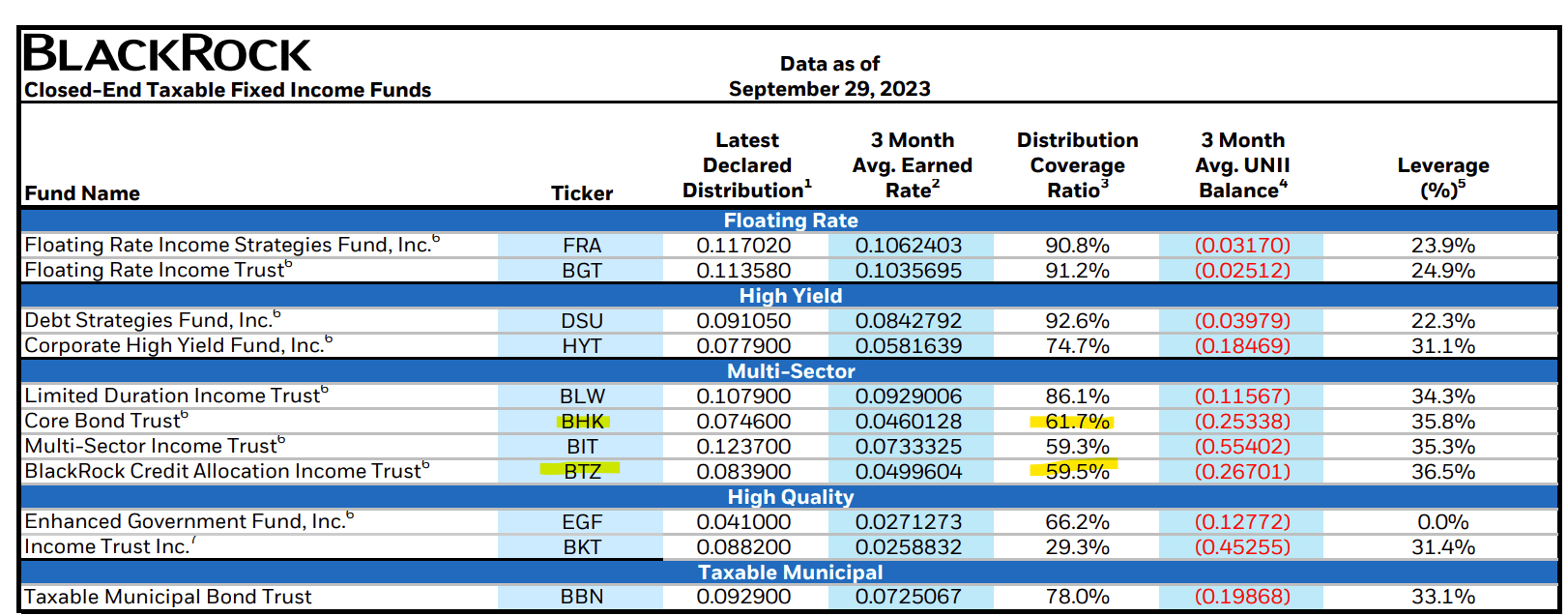

BlackRock UNII Report (BlackRock (highlights from author))

{kind=link}

However, it is true that if rates are cut, appreciation and higher leverage could see these funds perform quite strongly going forward. That appreciation could make up more than enough to cover the shortfall in distributions. Still, I'd have to say that WEA and PAI are more interesting names at this time, in my opinion.

WEA And PAI

WEA is leveraged and takes the approach of investing in some below-investment-grade debt holdings.

PAI, on the other hand, is an unleveraged fund with a portfolio that is almost entirely classified as investment-grade. That could make it the most conservative of the funds we touched on today.

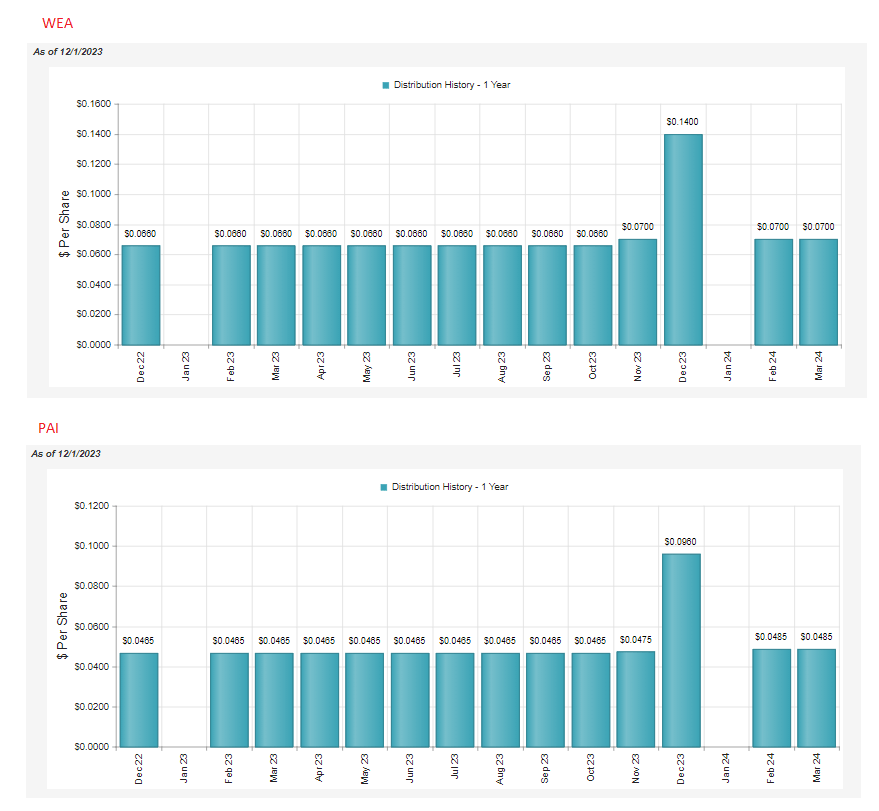

That generally means that it is also going to be the lowest yielding of the group, and we can see that is definitely the case when put up against WEA. WEA currently sports a distribution rate of 7.99%, and PAI is at 5%. They've also both just recently seen their distributions increase, with PAI even more recently boosting it a touch for a second time.

WEA/PAI 1 Year Distribution History (CEFConnect)

{kind=link}

WEA's distribution coverage stands at nearly 90.5% based on its last quarterly report and the latest distribution announced. For PAI, their last quarterly report would put the distribution coverage at 103%. They are the best of the bunch, as they don't have to deal with the headwinds of higher interest rate costs on their borrowings.

At the same time, PAI is also the most attractively priced, too. At least relative to their historical level, which showed the fund traded at premiums on a regular basis prior to the last couple of years. WEA isn't too richly priced, which also makes it a solid candidate to consider. Although it just recently appeared to have spiked higher after it was attractively priced.

Ycharts

This is one of the catalysts that looks like it could play in favor of PAI. PAI carries the lowest distribution rate (with the best coverage), but more upside could come from discount contraction as well as when we see the Fed pivot. When lower rates come, PAI should provide further upside, so that's what makes the ~5% distribution rate quite appealing at this time. It isn't just the yield itself but the potential upside from two different angles.

Having strong coverage also means they aren't seeing assets potentially erode away as BHK and BTZ will. Those two funds need rates to come down sooner rather than later so they can start making capital gains to cover their payouts to investors rather than simply focusing on paying out the income generated from the underlying portfolio. That means for as long as rates remain "higher for longer," that's bad news for those funds.

Conclusion

Overall, of this group discussed, I'd lean more toward PAI - which I hold - and WEA, with their stronger distribution coverage and decent valuations. For investors who are more optimistic about rates going lower sooner, BTZ offers a tempting choice. This would be due to the elevated leverage that should see it rebound harder, as well as attractive discounts. Of course, that cuts both ways; higher leverage does mean higher risk. The lack of distribution coverage is another area of concern that should be considered for BTZ. This is why BHK appears to be the worst choice at this time for this small group: unattractive valuation and lack of distribution coverage are two areas of main concern.

For further details see:

Closed-End Funds: Investment-Grade Corporate Fixed-Income Exposure To Consider