HFRO - Closed-End Funds: Misclassifications Can Lead To Misunderstanding

2023-03-09 15:14:17 ET

Summary

- Data aggregator websites such as Morningstar or CEFData are merely places to get initial ideas.

- With CEFs that can get rather niche and are actively managed, it becomes even more imperative as things change constantly.

- CEF misclassifications can lead to misunderstandings, which can lead to unexpected outcomes.

Written by Nick Ackerman, co-produced by Stanford Chemist. This article was originally published to members of the CEF/ETF Income Laboratory on February 22nd, 2023.

As I've said before, data aggregating websites such as Morningstar or CEFData are merely a place to get initial ideas; we have to look at the funds more in-depth before deciding if something is worth buying or not. Data feeds can have errors or not update as timely as material delivered directly from a fund sponsor. If there is a discrepancy between two data sets, going with the official data from the official source is always your best bet.

I'm not here to bash data aggregating websites since I obviously write on one of the best of them out there, Seeking Alpha. Seeking Alpha gets its data feed from S&P Market Intelligence, with real-time and delayed quotes from Xignite and IEX Cloud. What I do want to highlight is some of their shortfalls so investors can be better informed.

CEFConnect is a highly popular website sponsored by Nuveen. However, they get their data feed from Morningstar, so I'll be referring to Morningstar in this article, but what is applicable there is directly applicable to CEFConnect. As far as CEFData, I couldn't find the exact source of their information, but it sometimes varies from Morningstar - so I've assumed that it is fed from another source.

We've touched on distribution source characterizations being incorrect before. However, today, I wanted to touch on the misclassification of funds. Closed-end funds can get rather niche, then a data aggregator such as Morningstar tries to break it down into specific categories. This can lead to funds being misclassified. Since CEFs can change over time, this can also present another hurdle if the classification isn't switched.

Often, a closed-end fund sponsor will provide a benchmark that is blended from several different indexes. That provides better comparison results to their funds - but since the fund sponsors themselves select them, they could also come under scrutiny.

Examples Of Misclassifications

Highland Income Fund ( HFRO )

One such example of that is HFRO. It is still labeled in the category of "Bank Loan."

USD |All data based off of NAV except where noted| Investment (Price) as of Feb 21, 2023| Investment ((NAV)) as of Feb 21, 2023| Category: Bank Loan as of Feb 21, 2023| Index: Morningstar LSTA US LL TR USD as of Feb 21, 2023

On CEFConnect, it's actually still named Highland Floating Rate Opportunities Fund ( HFRO ), even though that was its former name. Along with that name change, the fund actually changed its investment policy as well to no longer be focused entirely on senior loans/bank loans.

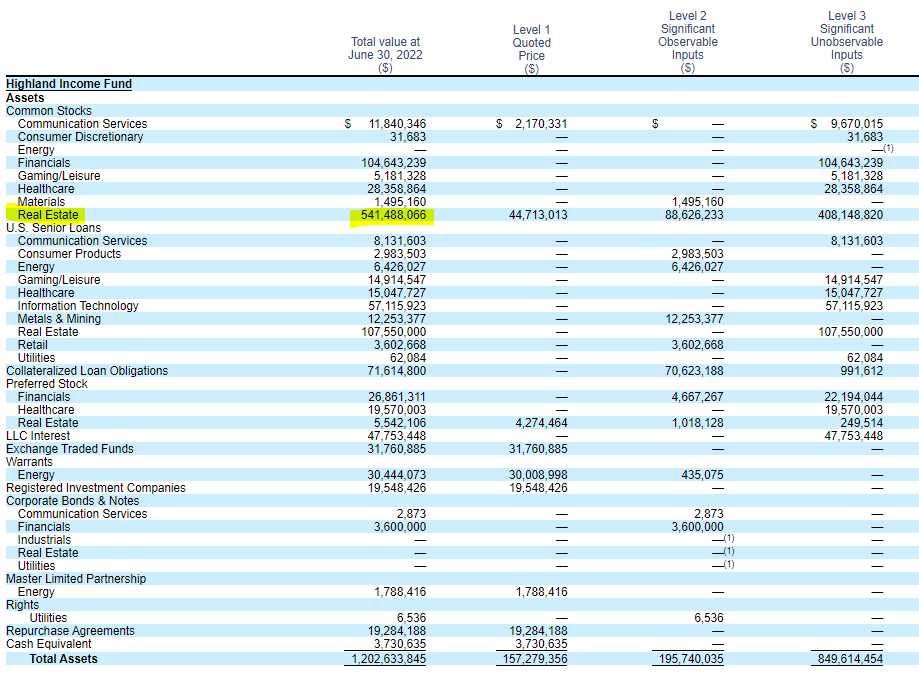

When we navigate over to the fund's last semi-annual report for the period ending June 30th, 2022 , it becomes very clear that the fund is heavily transformed. The largest allocation of the fund is to real estate equity positions. While the fund still carries a sizeable allocation to senior loans, it is no longer the main focus.

HFRO Asset Breakdown (Highland)

{kind=link}

Additionally, note the amount of level 3 assets here. That adds some skepticism to the valuation of the underlying portfolio as well. Here is the definition of level 3 assets.

Level 3 - significant unobservable inputs (including the Trust's own assumptions in determining the fair value of investments)

Barings Corporate Investors ( MCI )

Another great example of this that was brought up to me recently is the MCI. This was actually what spurred me to write this article in the first place.

This fund has performed incredibly well, like outstandingly well, against the high-yield bond category that it gets assigned to it.

USD |All data based off of NAV except where noted| Investment (Price) as of Feb 21, 2023| Investment ((NAV)) as of Feb 21, 2023| Category: High Yield Bond as of Feb 21, 2023| Index: Morningstar US HY Bd TR USD as of Feb 21, 2023

Taking a look at the total NAV returns of the last five years against a basket of high-yield bond CEFs, we can see just how well the fund has done.

Ycharts

Instead of being impressed, my initial reaction was one of skepticism. There had to be a data error or something about the quarterly update of the NAV throwing something off here. There just couldn't that much pull away in the fund relative to the sector. If there was, this is the best high-yield bond fund ever, and investors need not look elsewhere except MCI for all of our investing dollars.

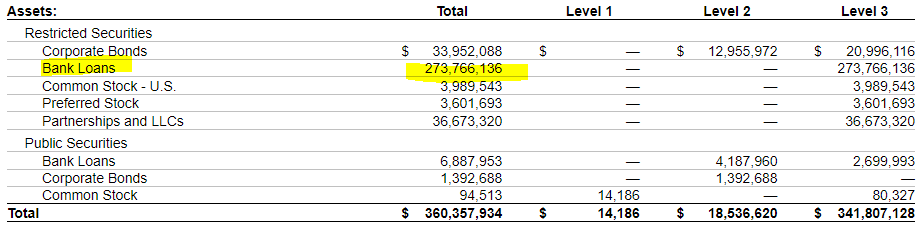

However, it became quite clear when looking at the portfolio from their annual report. It should have also been a tip-off that it initially started near the end of 2021 when the fund started diverging away from the rest of these 'peer' funds. And here is what I would have initially missed based on just looking at the Morningstar classification, this fund is heaviest in bank loans. This was as of the end of June 30th, 2022 .

MCI Asset Breakdown (Barings (highlights from author))

{kind=link}

MCI, similar to HFRO, carries a significant amount of level 3 assets. In fact, nearly 95% of the portfolio was in level 3 assets - which is primarily the fund's main focus of privately placed debt investments.

Bank loans are based on floating rates so that this fund could be considered more accurately as a senior loan fund and categorized as such, with nearly 76% of its portfolio invested in these bank loans. When looking at the total NAV performance of the last year, the fund's end result is much more similar to senior loan peers that I've included. The quarterly NAV updates, of course, are going to be less consistent.

Ycharts

As an ETF, Invesco Senior Loan ETF ( BKLN ) doesn't have to contend with discounts/premiums as the CEFs do. Additionally, it is non-leveraged.

When looking at the total share price return, we see that it is much more consistent with the rest of the peers in the last year.

Ycharts

If we look back at the end of 2020 , that annual report showed ~63% allocated to bank loans. So they can shift their portfolio around to take advantage of different situations - but seem to carry a higher allocation to bank loans rather than high-yield bonds.

In their defense, they don't say anything about being a high-yield bond fund either. They simply state that the "fund invests principally in privately placed, below-investment grade, long-term debt obligations and often accompanied by equity features, purchased directly from their issuers and sourced through Barings extensive deal network of private equity sponsors."

All that being said, MCI has still been a solid performer over the longer term. Perhaps it's the "accompanied by equity features," private investment prowess or adaptability to environmental changes since the fund's inception in 1971, but whatever it is, they have delivered against both senior loan and high-yield bond funds.

The longer-term total share price return results were much more comparable to the high-yield bond category - while we saw above, the shorter-term results were similar to the strong senior loan space due to rising rates. Giving outstanding results while minimizing the downside is truly a rare feat.

Ycharts

One thing that is still worth touching is what we see for the total NAV return results. Once again, my skepticism warning light is flashing. How could it not when the fund's total NAV returns suggest that COVID was a mild downturn? Although COVID was such a short-lived event, this is where quarterly reporting wouldn't have really reflected such a quick event that was there and gone between reporting periods.

Given the results below, MCI should be trading at a massive discount.

Ycharts

The discount for MCI is indeed massive as the fund's NAV results were much better than the share price results. Based on the last reported NAV and price in the last quarter on September 30th, 2022, the discount stood at 21.94%. However, since the price has risen since then, the current discount would be suggested to be closer to 12%. Although we know the NAV is likely to have moved during this time too. With quarterly reporting, it can lead to this sort of ambiguity compared to daily NAV reporting.

MCI Assets And Discount (Barings)

Author Note: Since the original publication, the new annual report is out, reflecting a NAV per share of $16.37 for the quarter ending December 2022. That suggests the latest discount comes out to 13.7%.

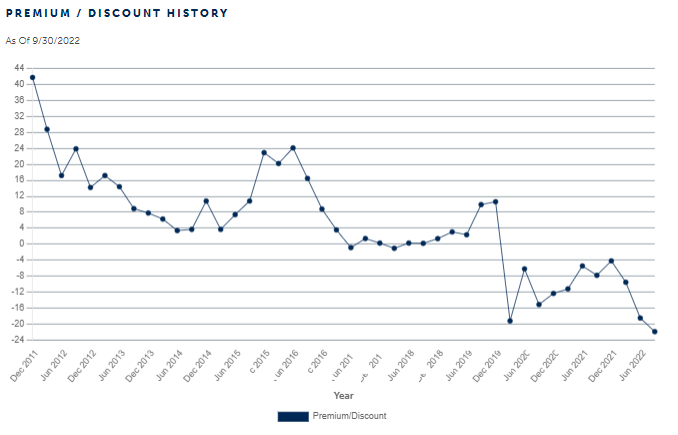

The fund had traded at a sizeable premium for most of its years. It's been more recently in the last several years where a discount has been present.

MCI Discount/Premium (Barings)

{kind=link}

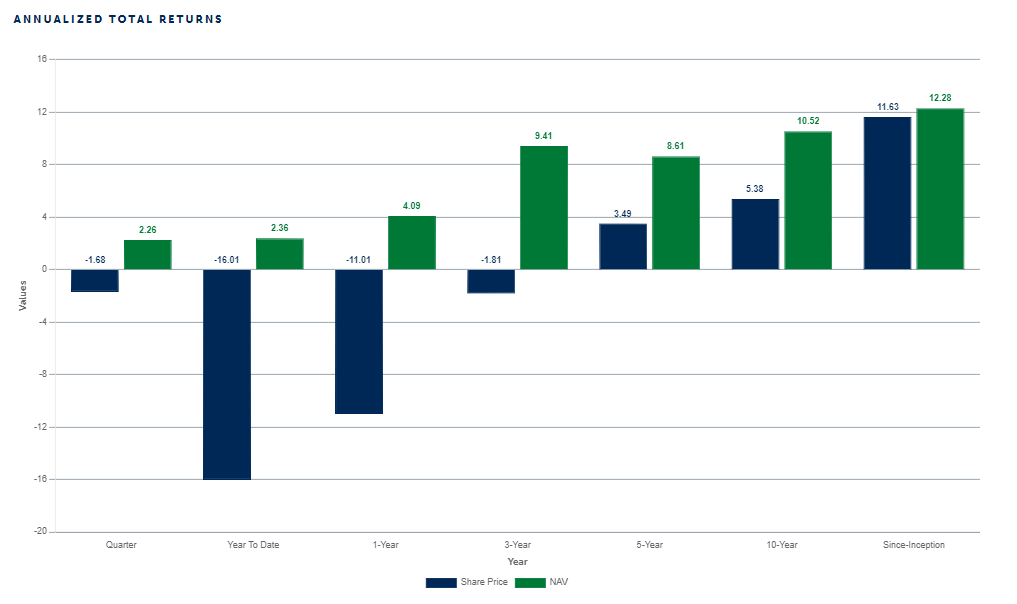

Here's a look at the annualized returns.

MCI Annualized Results (Barings)

{kind=link}

Conclusion

With data we get from outside sources other than fund sponsor official data, if it is sometimes too good to be true, one better takes a deeper look. Misclassifications on funds, especially with closed-end funds that can get niche, are actively managed and can change investment policy, need to be given extra time when comparing against 'peers.' Looking at their portfolio, what might be categorized as a peer at first glance isn't always so.

For further details see:

Closed-End Funds: Misclassifications Can Lead To Misunderstanding