ERNXY - CME Group: Owning The House Is Not Cheap

Summary

- CME Group Inc. primarily operates future and options markets across several products.

- CME has grown consistently over its historical trading period due to greater volume in financial markets. The business is able to grow during positive and negative market movements.

- FCF yield is an impressive 42%, with CME distributing almost all of its cash flows as dividends.

- When compared to its financial services peers, CME Group Inc. is fairly valued in our view, with an upside of only 5%. We rate the stock a hold for only this reason, with a positive outlook on the business long-term.

Company overview:

CME Group Inc. ( CME ) operates markets for the trading of futures and options on contracts worldwide.

CME's product offerings include:

- Futures and options - They offer futures and options products linked to interest rates, equity futures, foreign exchange, agric. commodities, energy, and metals, as well as fixed income products.

- Clearing services - This involves clearing, settling, and guaranteeing futures and options contracts, and cleared swaps products traded through its exchanges.

- Market data - This includes real-time and historical data services.

CME's revenue split is heavily weighted towards future and options, as this is their primary operations. Interest rates are the largest derivative traded, given their importance in global markets as a hedging / liquidity tool. This is generally a sticky service for this reason, with a great amount of the trading stemming from SOFR (And other LIBOR successors) and U.S. treasuries.

CME revenue breakdown (Q3 investor pack)

Investors who have owned CME Group Inc. for any extend period of time have been handsomely rewarded, with continued and sustained gains into 2022. With the business essentially being the "market" (or at least a part of it), this is a reflection of greater market and corporate activity over time.

An interest factor to consider with CME is that they make their money from trades, which means the business has the potential to be a great hedge as markets decline. The reason for this is that volatility generally increases, which means more trading. This is what initially sparked our interest and will be an important part of this analysis. We will look to consider the quality of the business' current and forecast financial performance, alongside our view of current market conditions and any other factors impacting the exchange industry. Finally, we will look at CME's relative performance against its peers, to assess if it is an attractive investment today.

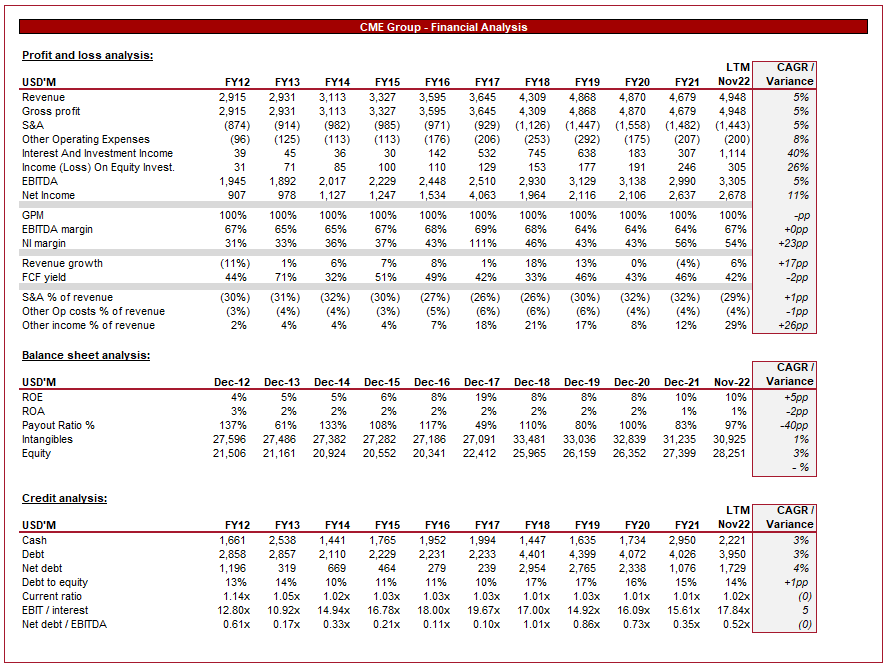

Financials:

CME - Financial performance (Tikr Terminal)

{kind=link}

CME's financial performance has been very strong across the last ten-years, with total revenue growing at a CAGR of 5%. The primary driving factor for this is greater average daily volume over the period. Interest rate and equity indexes are the primary growth area.

Avg. daily volume by product type (Annual accounts)

{kind=link}

Our only concern is that their rate per contract ((RPC)) has been gradually falling in recent quarters. Management attributes this to a change in product mix and it could act as a drag on revenue should it continue. It has yet to be seen if this will continue or not.

Market data revenue is up 6% on the prior year's quarter, as CME has been able to increase pricing. Although this revenue stream is far less significant, it is positive to see inflationary pressures are not impacting margins here.

CME's income from "other" sources has increased substantially, especially investment income. They are now 29% of revenue. This is driven in large part by strategic investments in businesses, earning dividends and (un)realized gains. Although this is great, it is non-trading and in many cases, one-off in nature, thus has the ability to distort net income.

Long term investments disclosure (1/2) (2021 FS) Long term investments disclosure (2/2) (2021 FS)

{kind=link}

{kind=link}

Margins are very impressive and translate straight into free cash flow ("FCF"). In the LTM period, FCF yield stands at an eye-watering 42%. Management's policy is to pay a normal dividend, alongside a special dividend to the extent that all unrequired cash is distributed. Thus, investors are rewarded by both dividends and capital appreciation.

Dividend declared (Q3 Investor pack)

ROE is an attractive 10%, with much of their equity value now represented by intangibles. This is not a concern as the business does not require a significant asset base as part of its operations.

The business is moderately leveraged with any debt issued repaid when possible. This gives the business scope for M&A / greenfield expansion should the opportunity arise. We like that the business has not been tempted into funding large dividend payments with debt, which many mature businesses like to do. With debt at 0.5x EBITDA, there is no real reason to reduce this further and with little in the way of capex commitments, dividends are an appropriate use of capital.

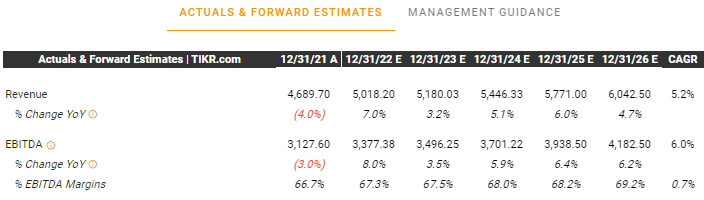

Looking forward, 2022 is likely to come at around $5BN in revenue, which representing 7% growth Y/Y. Markets have been fairly volatile during 2022, contributing to greater ADV. Beyond this, we believe the business can continue to grow at 3-5% indefinitely, with margins remaining consistent. The business is a market leader in the options/futures space and the barriers to entry are very high. CME can likely maintain this growth with just their current suite of products due to their importance to investors. Analyst forecasts support these assumptions.

Analyst estimates (Tikr Terminal)

{kind=link}

Product innovation:

As we mentioned previously, CME could easily continue its current offerings only and be highly successful. However, no sane Management would and so the business is looking to expand and develop its product offering. This includes:

- Development to e-mini weekly options

- Greater e-mini sector coverage

- Ether options and Euro-denominated Bitcoin and Ether futures

- Euro short-term rate

- TBA MBSs

- Event contracts.

These cover all forms of development, from incremental improvements such as the e-mini contacts to new products such as Event contracts. This allows CME to maintain its market leading status product wise, while also looking to find solutions for current problems.

Mortgage and interest rates have increased significantly in 2022 and Cryptocurrencies have reached new peaks in popularity. CME expanding their offerings in these areas is a great way to align their products with areas of importance in today's market.

Event contracts are more streamlined ways of accessing key futures markets globally. CME has seen strong engagement with these contracts and are attracting investors who otherwise would not use futures. This is an opportunity to increase their total addressable market and target new audiences.

Macro considerations:

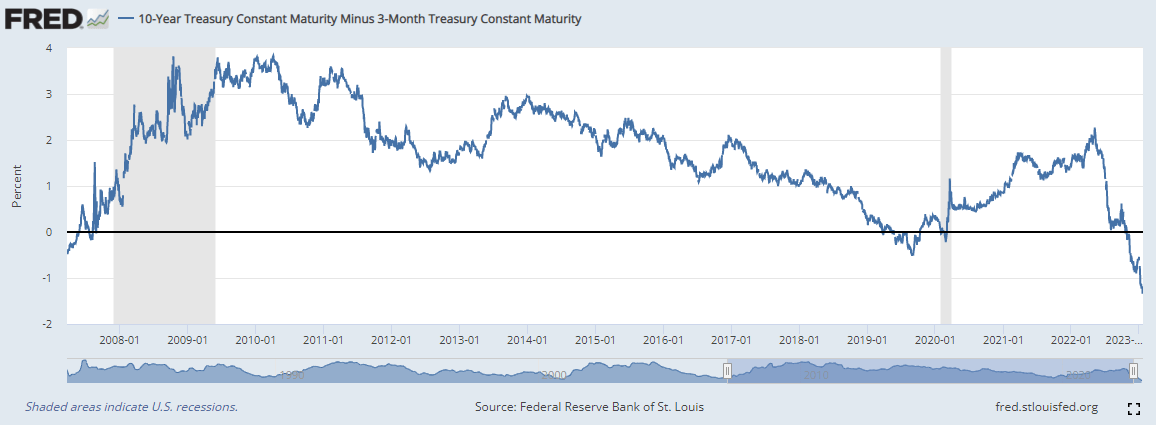

Inflationary pressure had caused economic conditions to reverse in late 2021 / early 2022. Interest rates began to be lifted following a decade of record low levels. This was initiated in order to cool demand and ease inflation. A large portion of this inflation is derived from energy prices, which is a market materially disrupted by the Russian invasion of Ukraine. For this reason, interest rates have been slow to dampening inflation. With inflation >5% in most western nations, it is likely that rates will continue to rise, with a normalization to sustainable levels in early 2024. The 10-year / 3-month yield curve inverted in Nov22 and remains so. At these levels, a recession is looks likely.

{kind=link}

With the cost of capital increasing, valuations have contracted. Further, businesses are posting weaker LTM numbers, many of which suffering margin contractions due to supply chain issues. This has caused a re-rating in global markets, with the S&P 500 down c.20% in 2022 for example.

This is neither significantly good nor bad for CME, the house wins regardless. If we look back at Q1 or Q2 2020, the peak of market hysteria during the initial days of COVID-19 in the west, CME posted better quarterly results than the year prior. If we look back at the '08 Financial Crisis, we observe a similar thing, revenues and NI up Y/Y (45% in 08', 2% in '09 and 15% in '10). With interest rates as high as they are, we are likely seeing above average levels of hedging. This is likely one of the key drivers of growth in the LTM period. For this reason, we are comfortable that CME will perform well in 2023, despite weakening market conditions. The only downside risk is if volume falls due to a stagnation in markets, but this should be mitigated by the interest rate segment of their services.

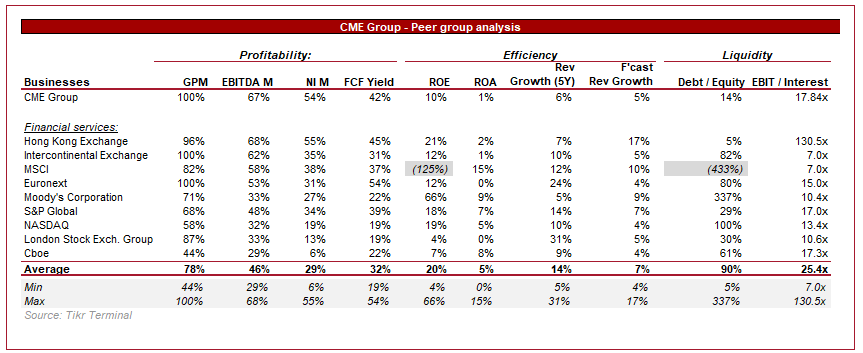

Peer group analysis:

Peer group analysis (Tikr Terminal)

{kind=link}

CME's peers are other exchanges, such as HKE, ICE and LSEG, as well as other financial services businesses.

As a general observation, we see high levels of profits and general market leading economics. There are multiple reasons for this including:

- The marginal benefit from extra investor / volume is very high as the associated cost is low. These businesses have built liquid markets through volume, which drives credibility and further users.

- These businesses operate in the same overarching industry but generally specialize in their own area (e.g., LDNXF in the UK equity market). This allows for the development of barriers to entry and aggressive pricing.

From a profitability perspective, CME performs extremely well, exceeding the average of the peer group. Only HKE ( HKXCF ) and Euronext ( EUXTF ) exceeds CME on a FCF basis but lack the geographical diversification.

Historic growth is difficult to compare, as many of CME's competitors have been acquisitive at much larger levels, such as LSEG with Refinitiv ($27BN) . Forward-looking data suggests CME is slightly below market average.

Based on this data, CME is a leading market participate. We would hesitate to suggest that they are the premier business in this group, as slightly lower margins combined with greater growth can be superior. With the strategy Management have maintained to date, sustainable moderate growth will continue.

Valuation:

Peer group valuation (Tikr Terminal)

With attractive economics these businesses bring, it is unsurprising that they are trading at high multiples. The average is 19x / 37x, with CME slightly above average at an EBITDA level and low on a PE level.

CME's dividends are only marginally higher than the average of their peers, with the optionality of a special dividend. This is a fairly attractive proposition for long-term holders looking for exposure in this market.

In order to determine our fair value for CME, we considered the relative position of CME v. each of the peer group, applying a discount or premium individual. In culmination, this gives us a 20x multiple. At this level, we see an upside of around 5%. Generally, we apply a 5% margin of error and so the upside is not sufficient enough to suggest this stock is a buy at its current level.

CME Group Inc. stock has seen very little in the way of re-rating during the last 10-years, meaning it could be very difficult to pick this one up at a discount. For this reason, investors seeking to hold long term can certainly achieve alpha at this price, but today, it is difficult to suggest there is a buy opportunity here.

Conclusion:

From a commercial perspective, CME is a fantastic business. It has cornered an incredibly large market, which is vital to global operations and will consistently grow into the long-term. Despite this, the business is showing innovation and sequential improvements. From a financial perspective, CME is incredibly disciplined. They have grown well, even during downturns, and have complete control over expenses to ensure profitability. Payouts only reflect what the business is able to distribute, with debt being a non-issue. This is clearly a fantastic choice as a low-risk component of a diversified portfolio.

The problem is that a company with all these characteristics is rarely cheap, and CME Group Inc. investors today are required to pay a fair price. We rate this stock a hold for that reason but believe in its long-term growth.

With market conditions weakening further, general sentiment could bring CME Group Inc. stock down into undervalued territory, regardless of performance, which is what we are banking on.

For further details see:

CME Group: Owning The House Is Not Cheap