CMSD - CMS Energy: Attractive Total Return Potential Valuation Make Strong Case

2023-03-30 17:24:08 ET

Summary

- CMS Energy Corporation is the largest natural gas and electric utility in the state of Michigan.

- CMS Energy enjoys remarkably stable annual operating cash flows, which is exactly the kind of thing that should prove attractive in today's economic environment.

- The company is positioned to give investors a 9% to 11% total return on average over the next five years.

- The balance sheet appears reasonable, but less debt would be nice.

- CMS Energy Corporation is trading at an attractive valuation relative to its peers.

CMS Energy Corporation ( CMS ) is the largest regulated electric and natural gas utility in the state of Michigan. The utility sector in general has long been one of the favorite places for conservative investors, such as many retirees, to park money. This is one reason why companies like CMS Energy are frequently called "widows and orphans" stocks, as they are boring companies that do not typically have substantial growth. CMS Energy does have remarkably stable cash flows over time, though, coupled with very reasonable growth prospects and a 3.19% yield at the current price. Overall, this company should be able to provide investors with an acceptable total return over the coming years. The company also has a very attractive valuation today.

Admittedly, the general thesis for CMS Energy has not really changed since the last time that we looked at the stock. It is still a solid utility company with long-term ambitions to achieve net-zero carbon emissions across its operations. However, a few months have passed since that time, and the company has released some new information and another quarter of financial results , so it deserves another look. Therefore, let us have a look at it and determine if the company could be a good fit for a portfolio today.

About CMS Energy Corporation

As stated in the introduction, CMS Energy Corporation is the largest regulated electric and natural gas utility in the state of Michigan. The company serves nearly all of the state, except for Detroit and the Upper Peninsula:

{kind=link}

This is a reasonably well-populated area, and CMS Energy has a total of 1.9 million electric and 1.8 million natural gas customers. That is, admittedly, fewer customers than fellow Michigan utility DTE Energy Company ( DTE ) serves, but CMS Energy's service territory is much larger. As I have pointed out in various previous articles, though, a utility's customer count is not really all that important, as it does not change the fact that utilities typically enjoy remarkably stable cash flows over time. We can see this by looking at CMS Energy's annual cash flow:

{kind=link}

As we can see above, with one or two exceptions, the company's operating cash flow was generally similar in each of the past ten years. The company did not give a reason for the reduced cash flows in 2022 in its annual report, but the company did pay significantly more money to purchase natural gas over the course of the year and there was a substantial difference in its change in accounts receivable compared to a typical year:

{kind=link}

This generally means that the timing of when customers paid their bills was very different. As I pointed out in a recent blog post , the high inflation is taking a serious toll on American consumers, so this could be a sign that the company's customers struggled to pay their utility bills on time over the course of the year.

The reason for the generally stable cash flows enjoyed by CMS Energy is the fact that its products are generally considered necessities for modern life. After all, how many people do not have electricity and heating in their homes and businesses? As such, most people will prioritize paying their electric and natural gas bills ahead of making discretionary expenses. This is especially important during periods like today, as the budget of the average household has been getting increasingly squeezed. It is likely that a company like CMS Energy will hold up much better than a company that makes items that people can do without in such an environment. As such, this is precisely the type of company that we want to be holding in our portfolios.

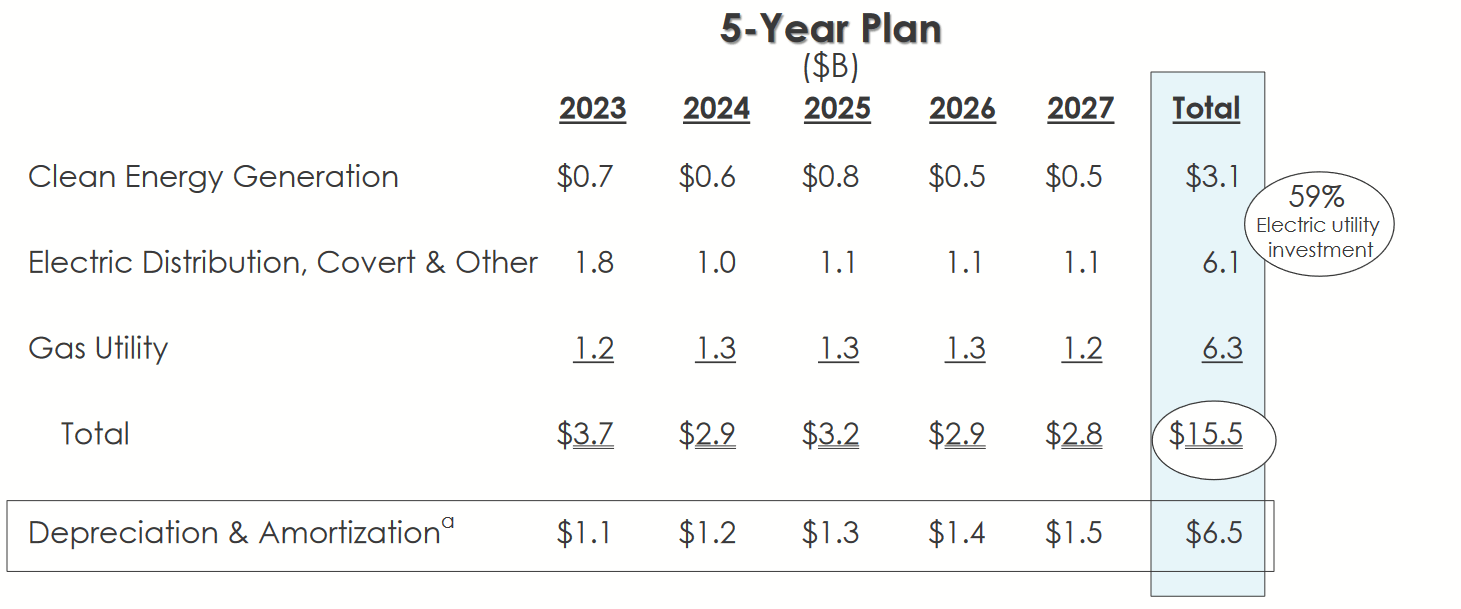

Naturally, as investors, we are unlikely to be satisfied with mere stability. We like to see every company in our portfolios grow and prosper. Fortunately, CMS Energy is well-positioned to do exactly this. The primary way through which the company will grow its profits is by expanding its rate base. The rate base is the value of the company's assets upon which regulators allow it to earn a specified rate of return. As this rate of return is a percentage, any increase to the rate base allows the company to increase the price that it charges its customers in order to earn that specified rate of return. The usual way that a company grows its rate base is by investing money into upgrading, modernizing, and potentially even expanding its utility-grade infrastructure. CMS Energy is planning to do exactly this, as the company recently unveiled a plan to invest $15.5 billion into its infrastructure network over the 2023 to 2027 period:

{kind=link}

This is a somewhat more recent plan than the 2022 to 2026 plan that we had the last time we discussed the company. This is nice because it gives us a bit more insight into CMS Energy's forward plans and long-term return potential. It is also in line with peers that have begun to release their own five-year plans for the same period. This plan should allow CMS Energy to grow its earnings per share at a 6% to 8% rate over the time period. When we combine this with the current dividend, investors should be looking at a 9% to 11% total average annual return, which is very reasonable and acceptable for a conservative utility stock.

Financial Considerations

It is important to have a look at how a company is financing its operations before making an investment in it. This is because debt is a riskier way to finance a company than equity because debt must be repaid at maturity. This is usually accomplished by issuing new debt to repay the maturing debt, as few companies have sufficient cash on hand to completely pay off their debt as it comes due. This can, unfortunately, cause a company's interest expenses to increase in certain market conditions. As the Federal Reserve has been raising interest rates steadily over the past year, this is something that could be a particularly big concern today as interest rates on brand-new debt are at a ten-year high. In addition to this risk, a company must make regular payments on its debt if it is to remain solvent. As such, an event that causes a company's cash flow to decline could push it into financial distress if it has too much debt. Although utilities like CMS Energy tend to enjoy remarkably stable cash flows, bankruptcies have occurred in the sector so this is not a risk that we should ignore.

One metric that we can use to evaluate a company's financial structure is the net debt-to-equity ratio. This ratio tells us the degree to which a company is financing its operations with debt as opposed to wholly-owned funds. It also tells us how well a company's equity can cover its debt obligations in the event of liquidation or bankruptcy, which is arguably more important.

As of December 31, 2022, CMS Energy had a net debt of $14.176 billion compared to $7.595 billion in shareholders' equity. This gives the company a net debt-to-equity ratio of 1.87 today. This is slightly higher than the 1.81 that the company had the last time that we reviewed it, but it is not completely out of line with its prior numbers. Here is how this compares with the company's peers:

| Company |

| Net Debt-to-Equity Ratio |

| CMS Energy |

| 1.87 |

| DTE Energy |

| 1.85 |

| Avista Corporation ( AVA ) |

| 1.25 |

| Eversource Energy ( ES ) |

| 1.45 |

| Entergy Corporation ( ETR ) |

| 2.02 |

As we can clearly see here, CMS Energy is quite a bit more heavily levered than its peers, although it is not completely out of line with the other companies here. In particular, both DTE Energy and Entergy Corporation have similar levels of leverage in their financial structures. This indicates that CMS Energy is probably not employing too much debt to finance its operations, so it is probably not exposing investors to undue amounts of risk. It would still be nice to see the company reduce its leverage somewhat, though, especially given the fact that interest rates are much higher now than they were just a few months ago.

Dividend Analysis

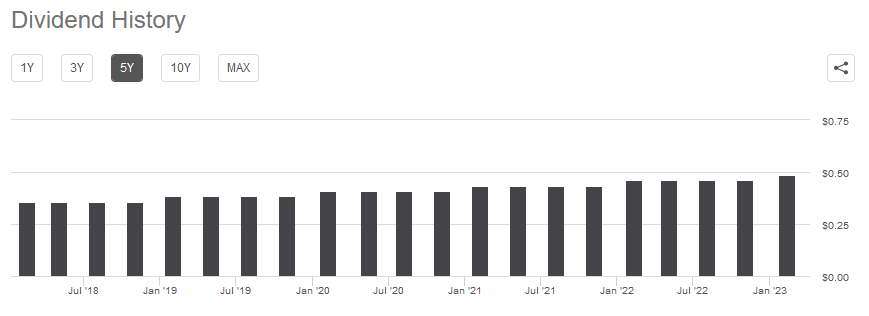

One of the reasons why investors tend to like utility companies is that they have higher yields than many other things in the market. This comes from the fact that they usually have slow growth and reasonable multiples, so they aim to deliver a large portion of their total return in the form of direct payments to investors as opposed to relying on capital gains. CMS Energy is certainly not an exception to this as the stock yields 3.19% at the current price. This is significantly higher than the 1.61% yield of the S&P 500 Index ( SP500 ) as well as the 2.53% current yield of the U.S. Utilities Index ( IDU ). CMS Energy has a long history of raising its dividend annually:

{kind=link}

The company has stated that it intends to continue to raise its dividend at a 6% to 8% rate annually in order to match the projected earnings growth that we discussed earlier. Thus, anyone purchasing the stock today should have a much higher yield on cost in a few short years. It is always nice to see a company grow its dividend over time, particularly during periods of inflation. This is because inflation is constantly reducing the number of goods and services that we can purchase with the dividend that the company pays out. This phenomenon can make it feel as though we are getting poorer and poorer with the passage of time. The fact that the company increases its dividend every year helps to offset this impact and ensures that the dividend retains its purchasing power.

As is always the case, though, it is critical that we ensure that the company can actually afford its dividend. After all, we do not want it to be forced to reverse course and cut the payout, since that would reduce our incomes and almost surely cause the stock price to decline.

The usual way that we judge a company's ability to afford its dividend is by looking at its free cash flow. The free cash flow is the money that is generated by a company's ordinary operations and is left over after it pays all its bills and makes all necessary capital expenditures. This is, therefore, the money that can be used for things such as buying back stock, reducing debt, or paying a dividend. During the full-year period that ended on December 31, 2022, CMS Energy had a negative levered free cash flow of $1.7055 billion. That is obviously not enough to pay any dividend, let alone the $546.0 million that the company actually paid out during the period. At first glance, this is certain to be concerning.

However, it is common for utilities to finance their capital expenditures through the issuance of debt and equity. These companies will then pay their dividends out of operating cash flow. This is because the incredibly high costs involved in constructing and maintaining utility-grade infrastructure over a wide geographic area would otherwise prohibit most utilities from ever paying a dividend. During the most recent trailing twelve-month period, CMS Energy reported an operating cash flow of $855.0 million. This is certainly enough to cover the $546.0 million dividend with money left over for other expenses. Overall, the company's dividend is probably reasonably safe.

Valuation

It is always critical that we do not overpay for any asset in our portfolios. This is because overpaying for any asset is a surefire way to generate a suboptimal return on that asset. In the case of a utility like CMS Energy, we can value it by looking at its price-to-earnings growth ratio. This is a modified version of the familiar price-to-earnings ratio that takes a company's forward earnings per share into account. A price-to-earnings growth ratio of less than 1.0 is a sign that the company may be undervalued relative to its forward earnings per share growth and vice versa. However, there are very few companies that have such a low ratio in today's richly-valued market. As such, the best way to use this ratio is to compare CMS Energy's valuation to that of its peers in order to determine which company offers the most attractive relative valuation.

According to Zacks Investment Research , CMS Energy will grow its earnings per share at an 8.04% rate over the next three to five years. This is on the high side of what we used earlier in this article to project the company's total return, but it is not overly optimistic based on the company's rate base growth. This growth rate gives the company a price-to-earnings growth ratio of 2.45 at the current stock price. Here is how that compares to the company's peers:

| Company |

| PEG Ratio |

| CMS Energy |

| 2.45 |

| DTE Energy |

| 2.89 |

| Avista Corporation |

| 3.51 |

| Eversource Energy |

| 2.73 |

| Entergy Corporation |

| 2.65 |

This looks pretty good for CMS Energy. As we can clearly see, the company appears to be quite cheap compared to its peers. When we combine this with the company's very reasonable balance sheet, it is presenting a solid investment thesis today.

Conclusion

In conclusion, CMS Energy Corporation has continued to deliver the relative stability that we have come to expect from it in the most recent quarter. The company continues to have fairly strong growth prospects and a high and growing dividend yield that overall makes a great investment case. The only real downside here is that the company's debt is a bit high, but it is not out of line with its peers so overall we probably do not have to worry about it. CMS Energy Corporation appears to be a worthy purchase today.

For further details see:

CMS Energy: Attractive Total Return Potential, Valuation Make Strong Case