NEE - CMS Energy: This Michigan Utility Continues To Prove Its ESG Credentials

Summary

- CMS Energy Corporation boasts remarkable revenue stability that should help the company weather the coming difficulties in the economy.

- The company is positioned for growth and should be able to deliver a 9% to 11% total average annual return.

- CMS Energy recently set up a unit devoted to helping major corporations meet their renewable energy ambitions, which could turn the company into an ESG darling.

- The company's debt load has gotten worse since we last looked at it.

- CMS Energy Corporation boasts a fairly attractive valuation relative to its peers.

CMS Energy Corporation ( CMS ) is one of the largest regulated electric and natural gas utilities in the state of Michigan, serving nearly all of the state except for the city of Detroit and the Upper Peninsula. The utility sector in general has long been among the favorite investments for conservative investors, such as retirees. There are some very good reasons for this, as most utilities enjoy incredibly stable cash flows and pay out fairly high dividend yields.

CMS Energy Corporation is certainly no exception to this, as the company’s current 2.83% yield is higher than most other things in the market, although it is a bit lower than many of its utility peers. CMS Energy makes up for this though with its very attractive current valuation. As I pointed out in my last article on the company, CMS Energy does not have the lowest debt load in the industry, but it has been making some progress in improving this. That is something that we very much like to see in today’s rising interest rate environment. Overall, there are certainly some reasons to consider taking a position in CMS Energy today.

About CMS Energy

As stated in the introduction, CMS Energy Corporation is one of the largest regulated electric and natural gas utilities in the state of Michigan. The company serves all of the Lower Peninsula except for Detroit, an area that includes 6.8 million residents:

CMS Energy

The company is fairly well-balanced between the provision of electricity and natural gas. It has 1.9 million electric and 1.8 million natural gas customers. Note that this is less than the number of actual residents in its service area due to the fact that many households contain more than one person. The fact that it is balanced between electric and natural gas is something that is fairly nice to see because both utilities have a certain degree of seasonality to them. This is most evident with natural gas, which is most often used as fuel for space heating. It is only necessary to heat a home or business during the cold winter months so natural gas is more heavily consumed during the fourth and especially first quarters of the year.

Electricity, in contrast, is consumed all year round, but it does have somewhat higher consumption during the summer months due to the use of air conditioners. As a result, utilities will see their cash flows spike during certain periods in which electricity or natural gas is more heavily consumed. The fact that CMS Energy is fairly well balanced between the two provides a certain amount of stability and cash flow balance over the course of the entire year. We can actually see this by looking at the company’s quarterly revenues over time. Here they are over the past eleven quarters:

{kind=link}

As we can see, there is not really a huge amount of change from quarter to quarter in most cases. The first quarter of the year does tend to have higher revenue, though, because the surge in natural gas consumption during those months is much greater than the increase in electricity consumption that occurs during the summer. Overall, though, we can see a great deal of stability here.

The reason for this is that electricity and natural gas service is generally considered to be a necessity in the modern world, so most people will prioritize paying their utility bills ahead of discretionary expenses during times when money gets tight. In addition, people do not really increase their electric consumption during boom times when they have lots of money to spend. This quality can make utilities like CMS Energy quite attractive as investments when economic times are difficult. It is no real surprise to anyone reading this to learn that the incredibly high inflation that has been dominating the economy has strained the budgets of many households. In addition, the United States is widely projected to enter into a recession during the next year. Thus, we want our portfolios to include companies like CMS Energy that should be able to maintain business as usual in such an environment.

Naturally, as investors, we are not interested in mere stability. We like to see the companies that we own grow and prosper over time. CMS Energy is fortunately quite well-positioned to do this. The primary way that the company will do this is by increasing its rate base. The rate base is the value of the company’s assets upon which regulators allow it to earn a specified rate of return. As this rate of return is a percentage, any increase in the company’s rate base allows it to increase the price that it charges its customers in order to earn that specified rate of return.

The usual way that a company will increase its rate base is by investing money into upgrading, modernizing, and even expanding its utility-grade infrastructure. CMS Energy intends to do exactly this as it has presented a plan to invest $14.3 billion over the 2022 to 2026 period into its infrastructure. Unfortunately, the company has not provided any more details than this so we do not know exactly how much it is planning to spend in each of the given years. This is rather disappointing since we are already into 2023, so any investments done in the first year of this program would already be behind us. Hopefully, the company will provide more details during its next earnings conference call as well as an updated investment figure that includes 2027.

We do know, however, that this program should allow the company to grow its earnings per share at a 6% to 8% rate over the period. When we combine this with the company’s current 2.83% dividend yield, CMS Energy should be able to deliver a 9% to 11% total average annual return to its investors through 2026. This is a bit higher than what we recently projected for peer utility Eversource Energy ( ES ), which does make CMS Energy a bit more attractive as an investment. It is worth noting that a 9% to 11% total average annual return is right about the same level as what the fastest-growing utilities are able to deliver so CMS Energy is certainly not a laggard here.

We did see this growth play out somewhat during the third quarter of 2022. CMS Energy reported earnings per share from continuing operations of $0.56 versus $0.54 in the year-ago quarter. This represents a 3.70% year-over-year increase, which is admittedly a bit less than the range that we just provided but it is still an increase. We also see an increase when we look at the trailing twelve-month period, which helps to balance out the fact that CMS Energy’s earnings are typically strongest during the winter for reasons that were already discussed:

{kind=link}

As we can clearly see, the company’s earnings per share have been climbing over time, exactly as projected. In the trailing twelve-month period that ended on September 30, 2022, the company had earnings per share from continuing operations of $2.67 versus $2.65 in the prior-year quarter. While that is only a 0.7% increase, the company’s basic earnings per share went up 48.34% year-over-year. The market generally looks at the headline earnings per share number, which as we can see is certainly delivering the kind of growth that we want to see from any company in our portfolio.

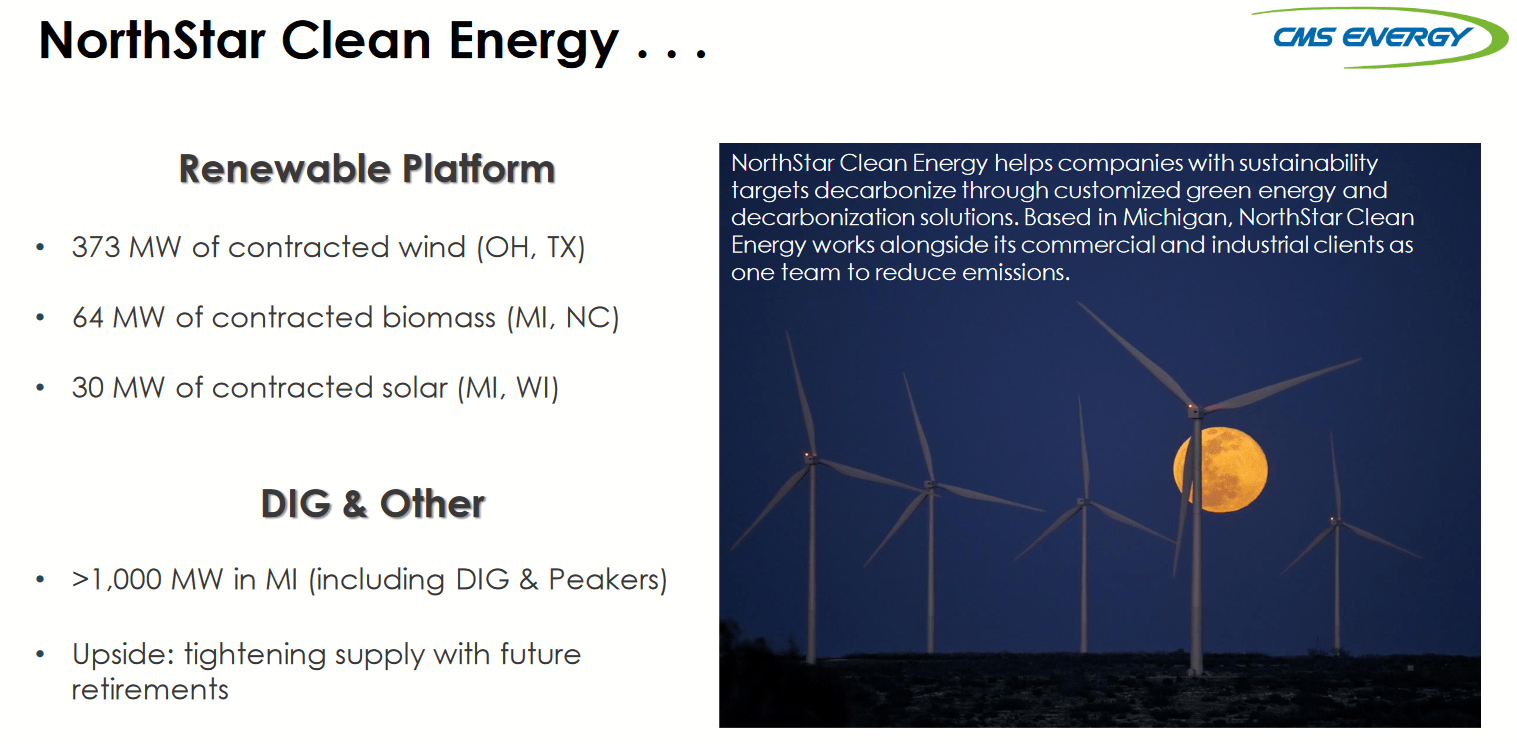

NorthStar Clean Energy

One of CMS Energy’s more interesting projects is its nationwide renewable energy company. In November 2022, the company renamed CMS Enterprises to NorthStar Clean Energy. This venture is designed to act as a partner for large companies that have somewhat ambitious clean energy goals. For example, General Motors ( GM ) had the goal of powering all of its factories in the United States with renewable energy by 2025. The company achieved that by sourcing power from four of NorthStar Energy’s generation facilities in three states.

CMS Energy is now looking to assist other companies in accomplishing the same feat with the NorthStar Energy subsidiary.

{kind=link}

In some ways, this is similar to NextEra Energy’s ( NEE ) green energy subsidiary which has made that company something of a darling in the environmental, social, and governance investing community. NorthStar Clean Energy basically constructs renewable energy facilities around the country and then enters into power purchase agreements with major industrial and commercial consumers of electricity. The purchasing power agreements help to fix one of the major problems with renewables, which is their intermittent nature. These contracts basically have the customer purchasing a set amount of power every month from the renewable facility, despite the fact that the renewable facility will not be producing at its peak capacity constantly. These agreements protect CMS Energy from the revenue fluctuations that would otherwise accompany these renewable facilities if the company was only able to earn money when they were actually producing. Thus, the company is able to maintain the general revenue stability that we appreciate from it while still constructing intermittent and unreliable renewable energy sources.

In my previous article on CMS Energy (linked in the introduction), I discussed how the company’s intense focus on improving the sustainability of its operations and deploying renewable solutions for its customers could attract interest from very wealthy environmental, social, and governance funds. The creation of NorthStar Clean Energy furthers that thesis. Ultimately, this could serve as a bullish catalyst for the stock should the company begin to attract more corporate clients and continue its expansion across the nation.

Financial Considerations

It is always a good idea to look at the way that a company is financing its operations before making an investment in it. This is because debt is a riskier way to finance a company than equity because debt must be repaid at maturity. This is usually accomplished by the company issuing new debt to repay its maturing debt, which can cause the company’s interest expenses to increase following the rollover depending on the conditions in the market.

As I have pointed out in a variety of previous articles, the Federal Reserve has been aggressively raising interest rates over the past year, so this is something that could prove to be a risk today. In addition to this risk, though, a company must make regular payments on its debt if it is to remain solvent. Thus, an event that causes a company’s cash flows to decline could push it into financial distress if it has too much debt. Although utilities tend to have remarkably stable cash flows, bankruptcies have occurred in the sector so this is still a risk that we should consider.

One metric that we can use to evaluate a company’s financial structure is the net debt-to-equity ratio. This ratio tells us the degree to which a company is financing its operations with debt as opposed to wholly-owned funds. It also tells us how well the company's equity will cover its debt obligations in the event of a bankruptcy or liquidation event, which is arguably more important.

As of September 30, 2022, CMS Energy had a net debt of $13.587 billion compared to $7.504 billion of shareholders’ equity. This gives the company a net debt-to-equity ratio of 1.81. This is substantially higher than the 1.65 ratio that the company had at the end of the second quarter and is quite disappointing since it is clearly heading in the wrong direction. It is a real shame because the company had actually been making pretty good progress at improving this ratio over most of 2022. Here is how that compares to some of the company’s peers:

| Company |

| Net Debt-to-Equity Ratio |

| CMS Energy |

| 1.81 |

| DTE Energy ( DTE ) |

| 2.22 |

| Avista Corporation ( AVA ) |

| 1.22 |

| Eversource Energy |

| 1.41 |

| Entergy Corporation ( ETR ) |

| 2.14 |

I used the same companies here as the last time that I reported on the company in order to provide an accurate point of comparison. Over the course of the third quarter, DTE Energy improved its ratio slightly while CMS Energy, Avista, and Entergy all got worse. CMS Energy remains the midpoint, however, which is not unexpected as it is pretty rare for a utility to substantially increase its debt over the course of a single quarter. As CMS Energy is still the midpoint in this comparison, the company is probably not using too much debt in its financial structure. I will admit though that the sharp increase in the company’s net debt does worry me and we should watch it going forward to ensure that the company begins making progress at decreasing this figure once again.

Dividend Analysis

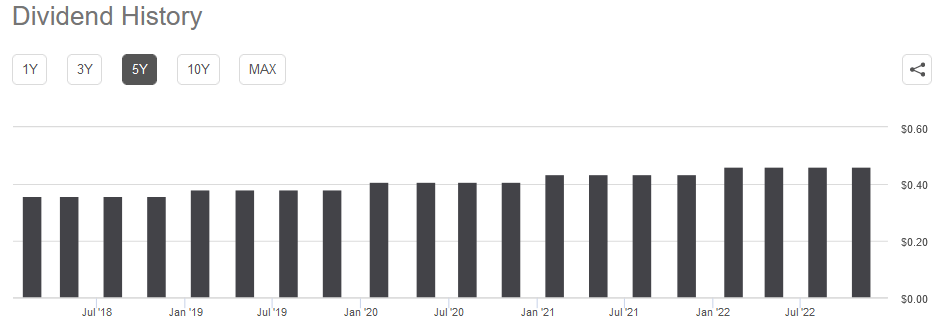

As stated in the introduction, one of the reasons why many conservative investors purchase shares of utilities like CMS Energy is because of the fairly high dividend yields that they tend to pay out. The biggest reason for these high yields is that these companies do not grow particularly quickly so they pay out a significant percentage of their earnings to the investors in order to provide a competitive total return. CMS Energy currently yields 2.83%, which is certainly better than the 1.63% yield of the S&P 500 Index ( SPY ) but is hardly jaw-dropping. Fortunately, CMS Energy has a long history of raising its dividend on an annual basis:

{kind=link}

The company will likely raise its dividend in the near future alongside the presentation of its full-year 2022 earnings results. Thus, someone buying today will likely see their yield-on-cost increase very quickly. That would be particularly true after a few years since it will undoubtedly keep increasing the dividend. The fact that the company keeps increasing its dividend over time is something that is fairly nice to see during inflationary times, such as today. The reason for this is that inflation is constantly reducing the number of goods and services that can be purchased with the dividend that you receive from the company. As a result, it can feel as if you are getting progressively poorer and poorer. The fact that the company will give you more money with each passing year helps to overcome this effect and helps to maintain the purchasing power of the dividend.

As is always the case, though, it is critical that we ensure that the company can actually afford the dividend that it pays out. After all, we do not want to be the bag-holders if the company is forced to reverse course and cut the dividend since that would reduce our incomes and almost certainly cause the share price to decline.

The usual way that we judge a company’s ability to pay its dividend is by looking at its free cash flow. The free cash flow is the amount of money that was generated by the company’s ordinary operations and is left over after it pays all of its bills and makes all necessary capital expenditures. This is the money that the company can use for things that benefit the shareholders, such as reducing debt, buying back stock, or paying a dividend. During the third quarter of 2022, CMS Energy had a negative levered free cash flow of $1.0173 billion. This is certainly not enough money to pay any dividends but CMS Energy still paid out $137 million in dividends during the period. At first glance, this will likely be concerning since the company is failing to generate the cash that is needed to cover the dividend.

However, it is common for a utility to finance its capital expenditures through the issuance of both equity and debt while paying its dividend out of operating cash flow. This is mostly because of the incredibly high costs involved in constructing and maintaining a utility-grade infrastructure network over a wide geographic area. During the third quarter of 2022, CMS Energy had a negative operating cash flow of $392 million. Obviously, this is not sufficient to pay any dividend either. However, the company typically posts a much better operating cash flow. The third quarter is usually rather bad for CMS Energy in terms of cash flow because it has to stockpile natural gas to get through the winter heating season.

Thus, it would make more sense to look at the company’s operating cash flow over the first nine months of 2022 in order to smooth out the effects of this. During that period, CMS Energy reported an operating cash flow of $667 million but only paid out $410 million in dividends. Thus, the company is certainly covering its dividend with some money left over. The coverage is admittedly not as strong as I would like, but I had the same complaint about the company when I reported on it following the third quarter of 2021 so that is just something that we have to learn to live with when it comes to this company.

Valuation

It is always critical that we do not pay for any asset in our portfolios. This is because overpaying for any asset is a sure-fire way to generate a suboptimal return on that asset. In the case of a utility like CMS Energy, we can value it by looking at the price-to-earnings growth ratio. This is a modified version of the familiar price-to-earnings ratio that takes a company’s earnings per share growth into account. A price-to-earnings growth ratio of less than 1.0 is a sign that the stock may be undervalued relative to its forward earnings growth and vice versa. In today’s richly valued market, there are admittedly very few companies that have such a low price-to-earnings growth ratio. That is especially true in the fairly low-growth utility sector. Thus, the best way to use this ratio is to compare CMS Energy with some of its peers in order to determine which company has the most attractive relative valuation.

According to Zacks Investment Research , CMS Energy will grow its earnings per share at an 8.18% rate over the next three to five years. This is in the same ballpark as the figure that we used earlier to project the total return so it seems pretty solid. This gives the company a price-to-earnings growth ratio of 2.54 at the current price. This is not as attractive as the valuation that the company had when we last looked at it, but it is still very reasonable. Here is how CMS Energy compares to its peer group:

| Company |

| PEG Ratio |

| CMS Energy |

| 2.54 |

| DTE Energy |

| 3.20 |

| Avista Corporation |

| 3.56 |

| Eversource Energy |

| 3.01 |

| Entergy Corporation |

| 2.68 |

This is certainly nice to see today. CMS Energy appears to offer the most attractive valuation of any of its peers today, which is actually an improvement from the last time. In my previous article, Entergy actually had a more attractive valuation. CMS Energy Corporation overall still offers its investors a reasonably attractive price here that, while it is a bit more expensive than when we last looked at the company, it is substantially better than the 3.0+ level that most utilities had a year ago. Overall, CMS Energy Corporation might be worth considering at the current price.

Conclusion

In conclusion, there is a lot to like about CMS Energy today. The company’s overall financial stability should serve investors quite well given the economic weakness that is likely to set in over the next year. It also continues to prove its merits to those that are excited about the transition to a “green” economy, and ultimately this could prove to be a net positive for the stock given the amount of money that is invested in this theme.

Unfortunately, CMS Energy Corporation’s debt has been getting somewhat worse, and CMS stock has gotten a bit more expensive. Neither of these things looks particularly terrible relative to the company’s peers, though, so it still might be worth investing in today.

For further details see:

CMS Energy: This Michigan Utility Continues To Prove Its ESG Credentials