DE - CNH Is Looking Cheaper Than Ever Using DCF Valuation

2023-10-25 13:33:59 ET

Summary

- CNH Industrial appears undervalued using a CFROI based DCF valuation tool.

- The macroeconomic outlook for farm income is less favorable, leading to lower spending in farm equipment, but still higher than pre-COVID times.

- CNH is making investments in technology and sustainable products, positioning itself for long-term growth in the agricultural equipment market.

We are initiating CNH Industrial N.V. ( CNHI ) with a buy rating. It is looking significantly undervalued using Cash Flow Returns On Investment DCF valuation tools.

Using the same parameters, we would also like to see how CNH stacks up against its peers, Deere & Company ( DE ) and AGCO Corporation ( AGCO ).

CNH Industrial is predominantly an agricultural equipment supplier, along with 15% of revenues from construction equipment. CNH is trading 38% below its year high of $17.98 and continues to fall. Investors are faced with the choice of buying now or waiting in the hope of a better entry point. For direction, investors are also eying Q3 results expected on 7 November 2023.

The macroeconomic outlook for farm income is less favorable than it has been over the last couple of years. According to the Food & Agricultural Policy Research Institute, University of Missouri , higher commodity prices saw net farm income at record levels of $183bn during 2022. Due to lower receipts and higher production expenses, income is expected to decline to $143bn for 2023, and further again to $140.4bn in 2024. Projected growth beyond 2024 is flat to slightly negative. Similar projections are made for Europe where farm income growth is expected to be very modest. These two geographies account for about 70% of revenues from its agriculture segment. Despite lower growth, revenues are expected to remain above pre-covid levels.

Higher farm income coupled with post-COVID pent-up demand resulted in higher spending for farm equipment in 2022. CNH's overall revenues increased 20.8% in 2022. The company outlook for 2023 expects revenue to be up 8% to 11% (including currency translation effects). Consensus sees no growth for 2024 and this is consistent with reduced forecasted farm income. Lower farm income translates to less disposable income and lower investments in farm equipment.

Construction is expected to be more resilient going forward, as can be seen in CNH's Q2 results . Revenue from agriculture is seen increasing 4% over Q2 2023 compared to the same period last year, whereas construction increased 19%. Consolidated gross margins also improved 300 bps from 22% to 25%. Along with higher price realization of its products, management has been working to control costs and improve operating performance.

Over the longer term, increasing population and limited farmland will increase the need for more efficient and precision farming equipment. Food security will also be a concern, given the current turmoil around the world. CNH is making inroads to elevate some of these concerns with the introduction of sustainable construction and agricultural products, including methane tractors and electric mini excavators. This is a result of higher R&D expenditure towards new product development and digital components for precision agriculture. In 2020, R&D expenditure was $493m, this increased to $642m in 2021 and again to $866m during 2022. CNH has recently acquired a global satellite navigation technology provider, Hemisphere GNSS for $175m, adding to its commitment to investment in technology. It is becoming more focused on agricultural equipment.

Financial Analysis

Over the last two years, and since the disposal of its trucks, commercial vehicles, buses, and specialty vehicles segment, IVECO, margins have risen.

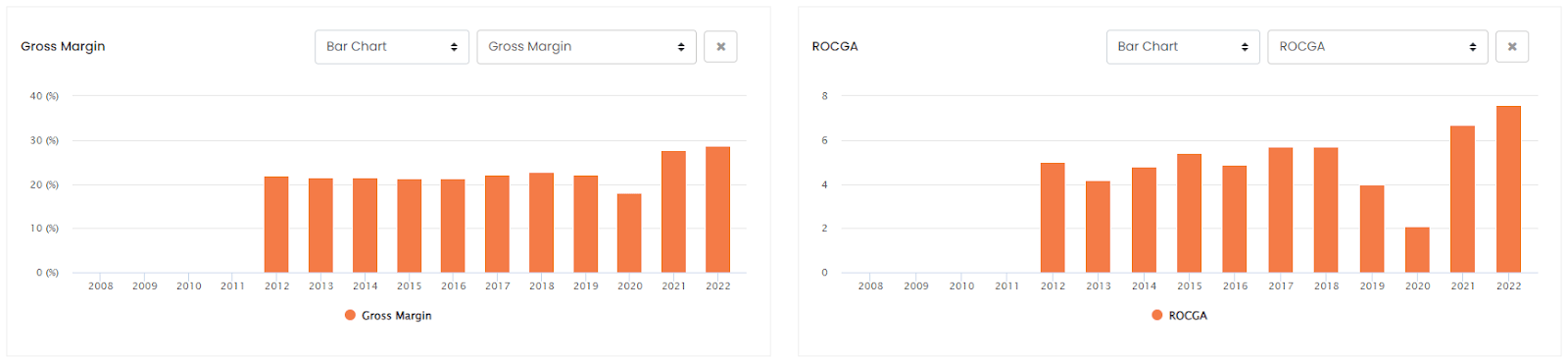

Gross Margins & Returns on Cash Generating Assets (ROCGA Research)

{kind=link}

This has resulted in higher Returns on Cash Generating Assets, a methodology of calculating returns similar to Cash Flow Returns on Investments.

More information on how ROCGA is calculated including gross assets, gross cash, and Cash Flow Returns on Investments can be found in Bartley Madden's paper " The CFROI Life Cycle ". Bartley Madden has been a significant contributor to the Cash Flow Returns on Investment methodology.

We will later see how this plays into the valuation of CNH.

In comparison to its peers, CNH has some positives and is showing some financial weakness, in particular its higher leverage. It has the highest debt to EBITDA of the three. In July 2023, management embarked on a $300m share buyback program indicating comfort in its liquidity.

CNH Peer Comparisons (ROCGA Research)

{kind=link}

On conventional valuation matrices, it stands roughly at par with AECO and these two seem to be undervalued in comparison to Deere. Looking forward Deere is trading at 11.4x PE for FY24, AGCO at 7.6x, and CNH at 6.3x. CNH is not only looking the cheapest in comparison to its peers but also across its own historical averages. Deere also enjoys the highest margins, whereas AGCO has the lowest.

Cash Flow Returns On Investments Valuation

To value a company, we use our affiliate ROCGA Research's quantitative and systematic Cash Flow Returns On Investments based on DCF valuation and modeling tools. The first step involves modeling the company, back-testing the valuation for correlation with the historical share prices, and using that same model to forecast forward.

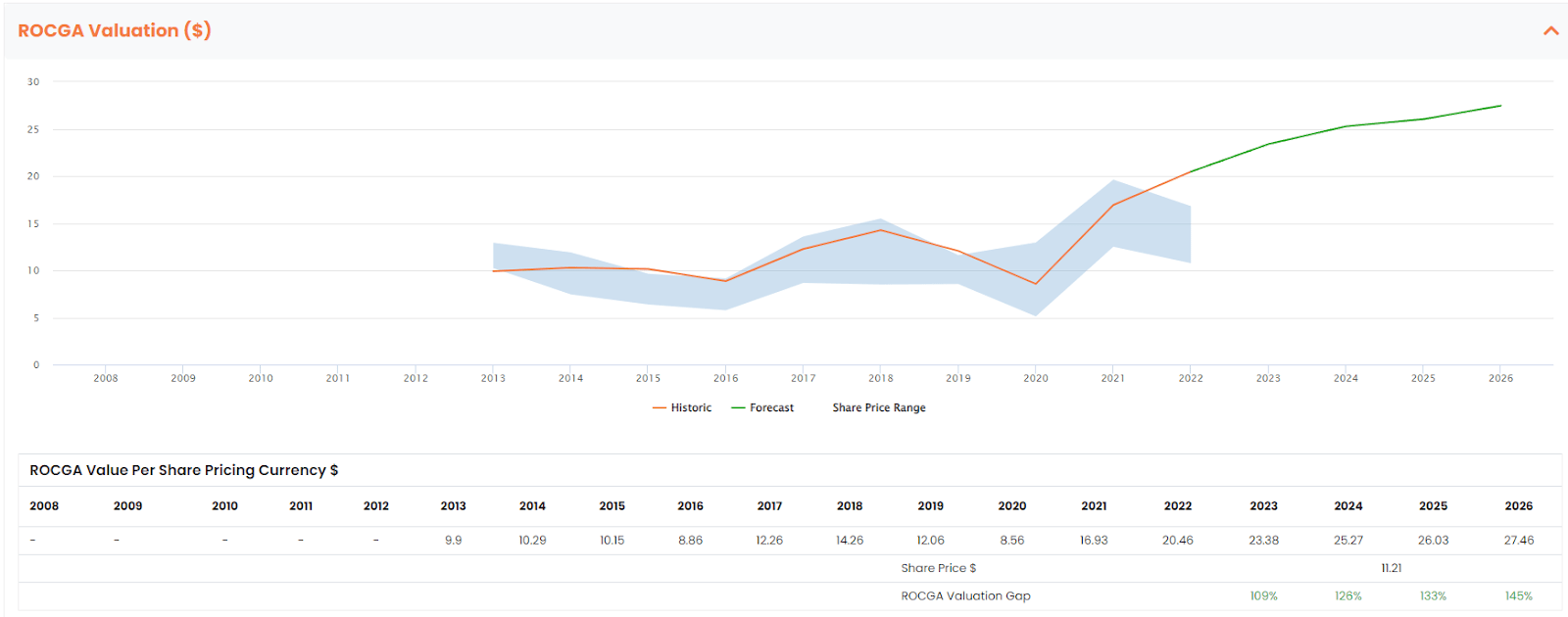

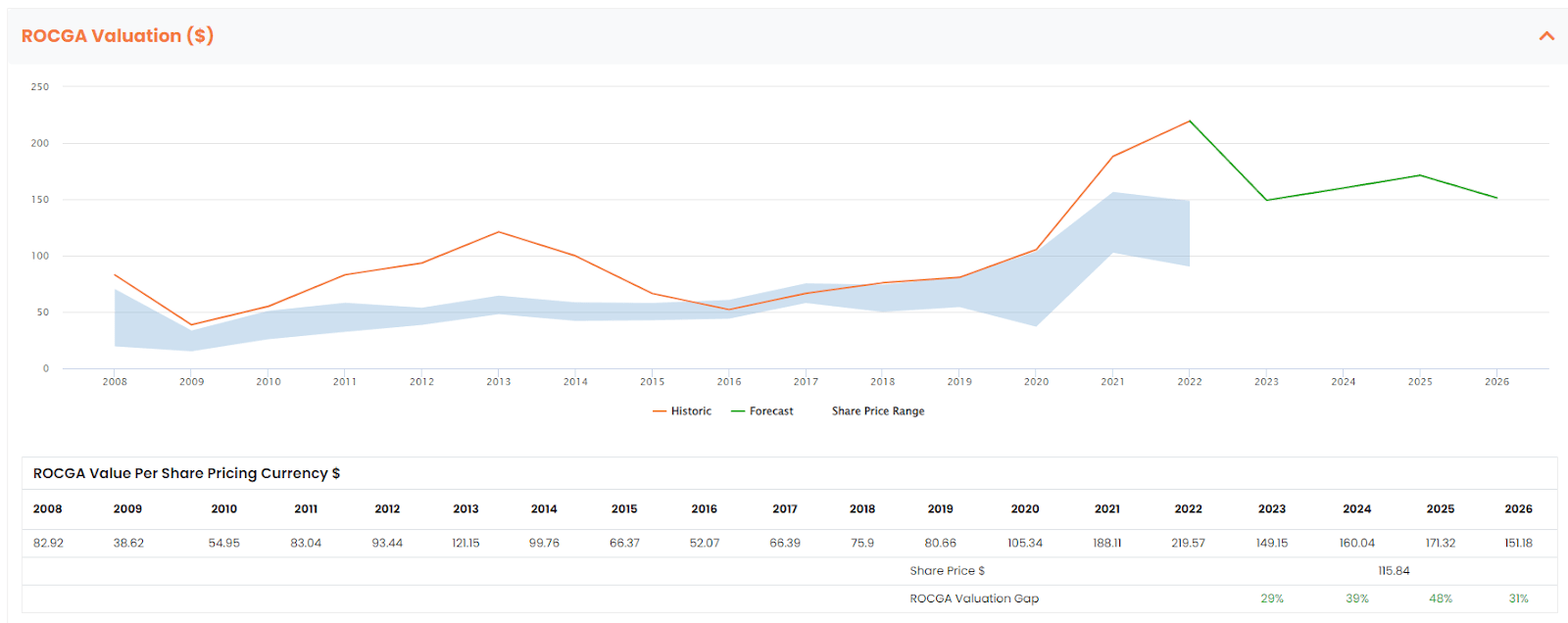

CNH Default ROCGA Valuation (Valuation chart created by the author using ROCGA Research Platform)

{kind=link}

Value is a function of returns and growth in cash-generating assets. The total value of the company takes into account the present value of existing assets and the present value of growth. The blue band above represents the share price highs and lows for the year, and the orange line is the DCF model-driven historic valuation. The green line is the forecast warranted value derived using the same model along with consensus earnings and default self-sustainable organic growth.

For CNH, due to the macroeconomic environment, we know growth is going to be substantially subdued. Our default valuation model is showing a potential upside of +100%. We derive an adjusted valuation where we reduce growth to zero for the near term and add a 2% risk premium to the cost of capital.

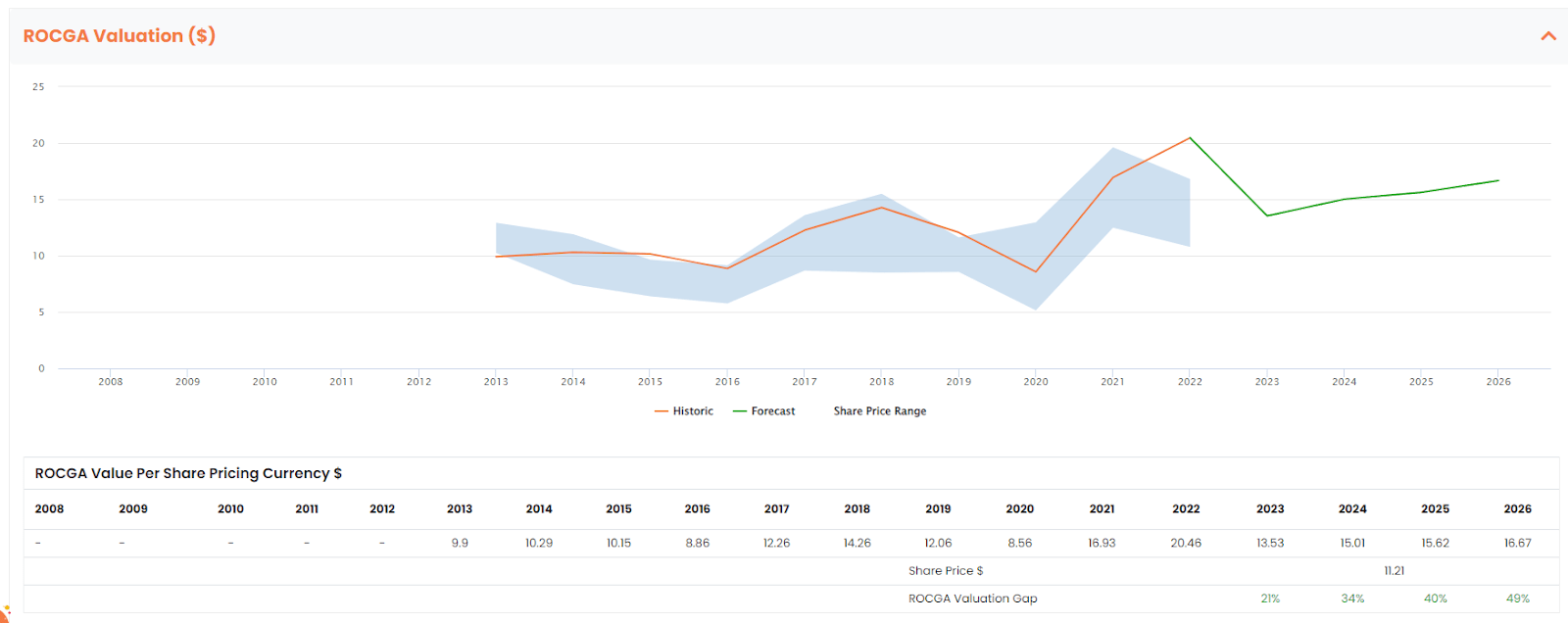

CNH Adjusted ROCGA Valuation (Valuation chart created by the author using ROCGA Research Platform)

{kind=link}

The valuation derived from stress testing is still pointing to a potential upside of 34% for FY24.

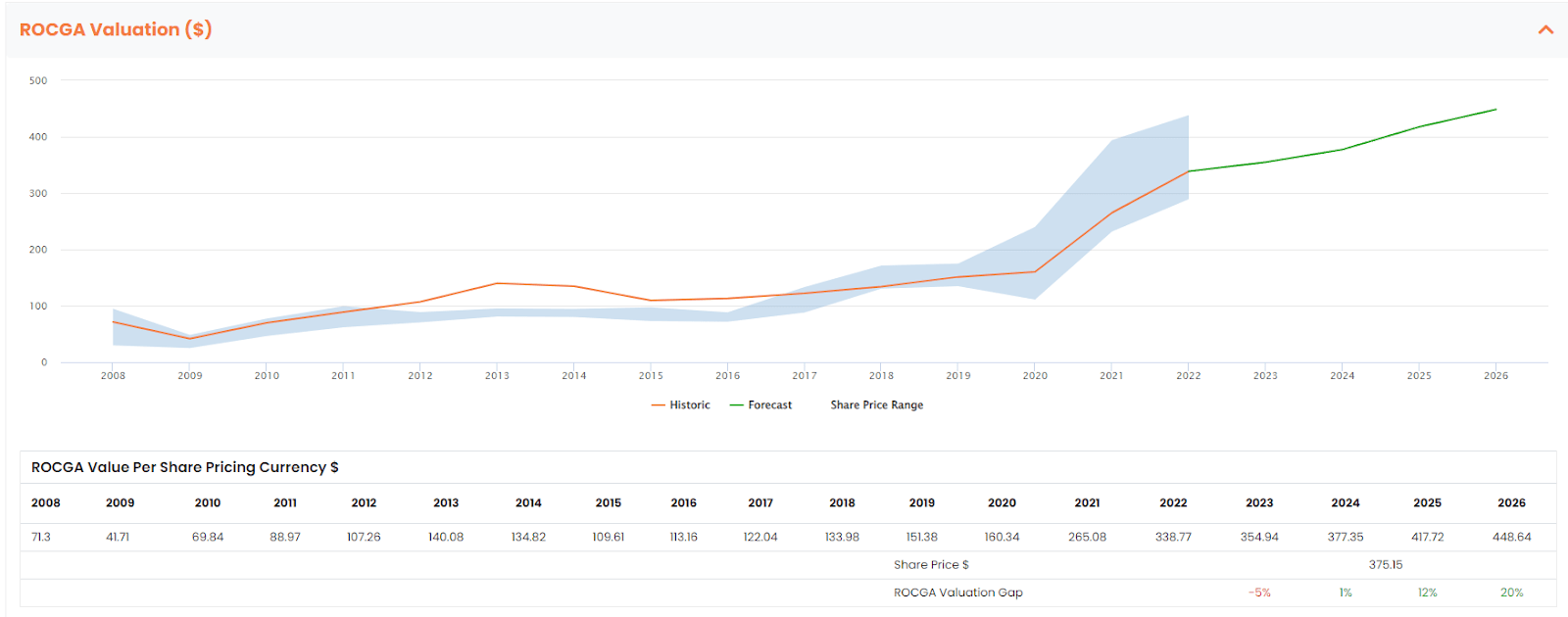

The same default scenario applied to Deere points to the downside of 21% for FY24. Since Deere has better growth and a stronger balance sheet, for our stress testing for Deere we reduce growth to 2% and add a 1% risk premium. This is our preferred adjusted value where Deere is trading at fair value.

Deere Adjusted ROCGA Valuation (Valuation chart created by the author using ROCGA Research Platform)

{kind=link}

Similar growth and risk adjustments to AGCO point to a potential upside of 39% for FY24.

AGCO Adjusted ROCGA Valuation (Valuation chart created by the author using ROCGA Research Platform)

{kind=link}

Given that AGCO has gained the most of a post-COVID bounce, it is potentially the most at risk among the three. Out of the three, our choice would be CNH.

Risks

The main risk faced by the agriculture equipment makers is the income of farmers. Lower food inflation will affect farmer's income and in turn lower demand for new equipment. This coupled with higher wage inflation for the workforce in the US and Europe, competition from Chinese manufacturers, and a higher interest rate environment could prove challenging going forward. Higher interest rates would affect CNH more as it has the higher leverage among the three we have looked at.

Conclusion

CNH is trading at a discount to its warranted value, even when we adjust for lower growth and higher risks.

The current share price is downward trending and investors are faced with the choice of buying now or waiting in the hope of a better entry point. At FY24 PE of 6.3x, there isn't a lot of room for the prices to fall further in our view, buy.

For further details see:

CNH Is Looking Cheaper Than Ever Using DCF Valuation