XLF - CNO-A Is Deeply Undervalued To The OTC Debt Of CNO Financial Group

2023-06-14 07:00:00 ET

Summary

- This article discusses the deeply undervalued junior bond of CNO Financial Group.

- Common stock and senior debt indicate no credit worsening of the company.

- We see possible 30% capital appreciation for CNO-A.

We usually post our articles to members of our service one week before we publish them to the public. This article was first published on June 9, 2023.

Overview of the trade idea

As we are on a constant search for the mythical "alpha," with this short article we would like to present you our latest trading idea, which allows the investors to exploit to their benefit the mispricing between the products issued by CNO Financial Group, Inc. ( CNO ). The main idea behind this kind of trade is that a particular product's yield deviates without some sound financial logic from its benchmark and from the yields of the products of the same issuer.

The particular fixed-income investment vehicle of interest to us today is CNO-A - a CNO Financial Group, Inc 5.125% Subordinated Debentures Due 2060. Its credit rating is Ba1 by Moody's and BB by S&P. At the moment of writing this article, CNO-A is trading with 9.1% YTM (XIRR calculated).

{kind=link}

We will try to defend the thesis that CNO-A is a "solid buy" on a relative basis, compared with the OTC traded debt of the company. Albeit being the lowest in the debt structure of CNO, CNO-A has widened unreasonably its credit risk spread, while its OTC-traded brother bonds have narrowed theirs. At the same time, the common stock of the company is trading with no signs of weakness. According to us, there is no sustained financial logic in CNO-A trading as if it is debt issued by a troubled company when both the higher and the lower segments of the capital structure of CNO do not recognize such a risk. So let us dive into some analysis.

The common stock

CNO belongs to the big family of financial companies:

{kind=link}

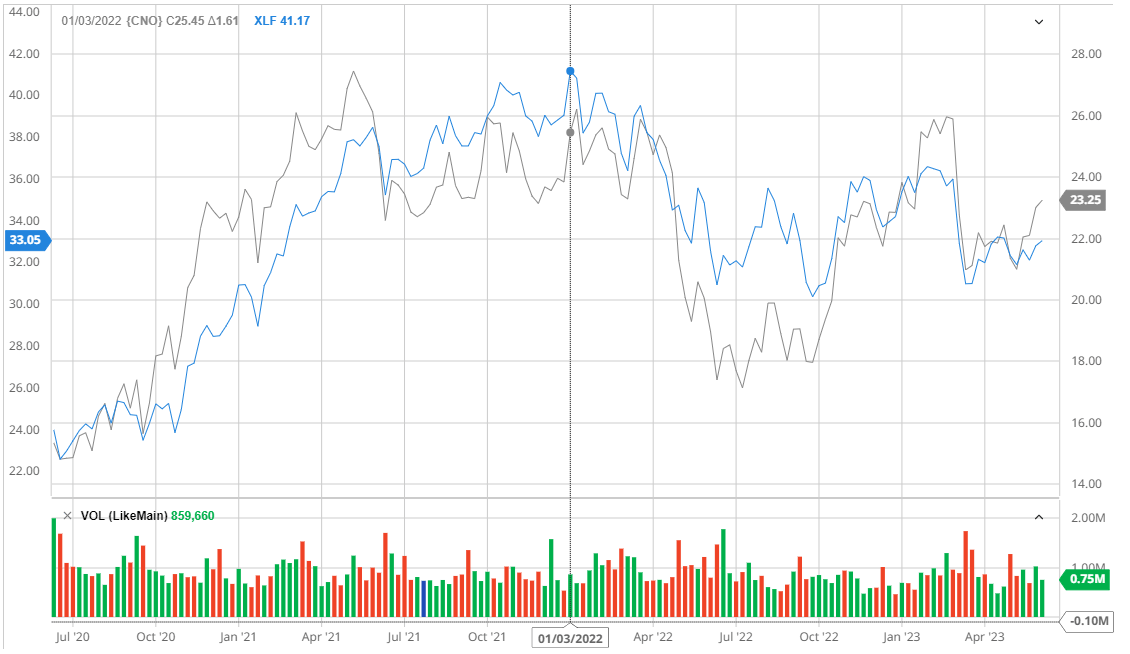

The performance of the common stock for the last three years suggests that the market sees no particular danger when pricing the company. When comparing the price action of CNO with the average for the financial sector, we do not observe some extraordinary long-term deviations on the downside that the company cannot compensate for. In the chart below we are comparing CNO with XLF - The Financial Select Sector SPDR ETF.

{kind=link}

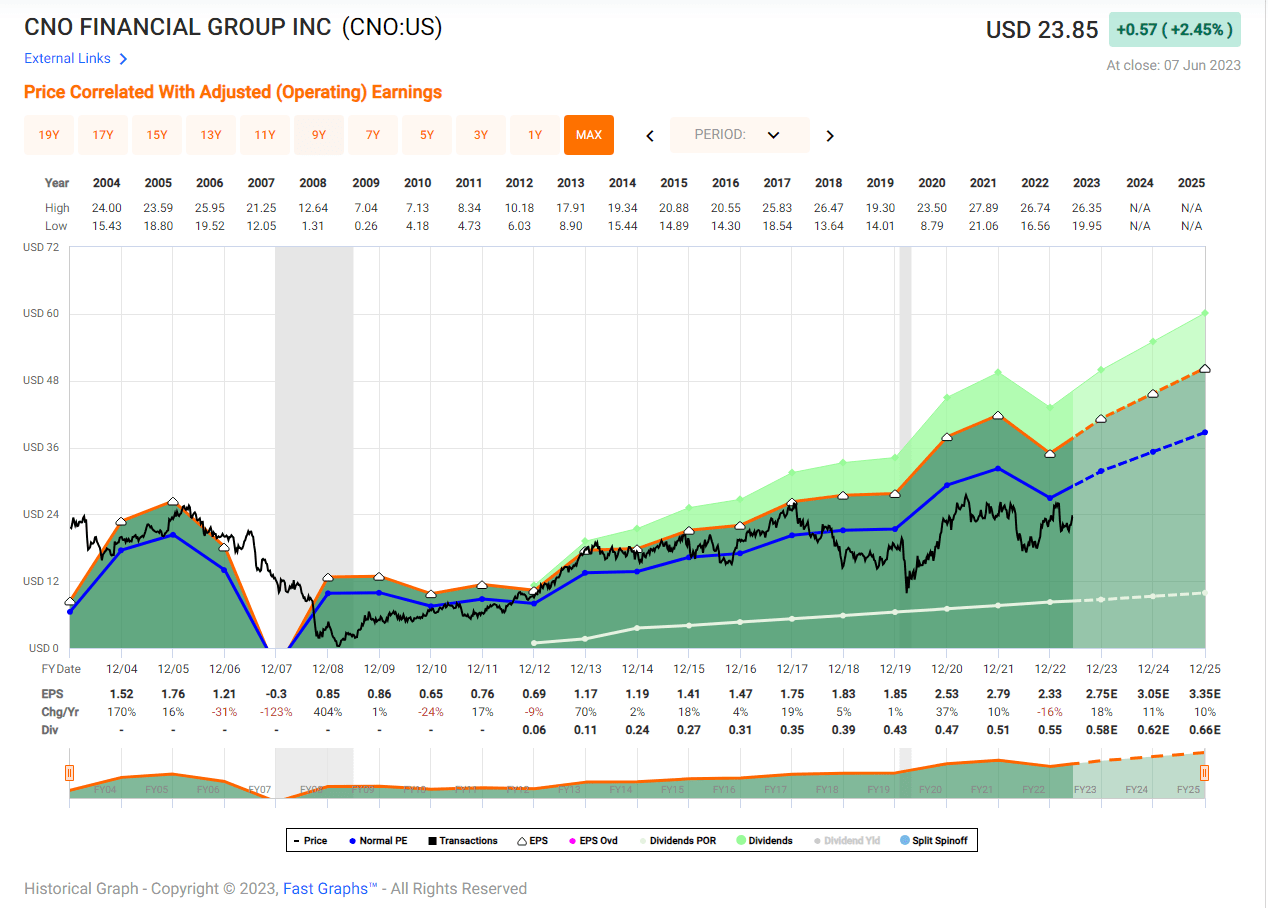

The P/E ratio of the company does not indicate some worsening, on the contrary - after the Financial Crisis in March 2020 CNO restored quite fast its pre-crisis values of P/E ratio. That indicates a stable business model that the general public trusts.

{kind=link}

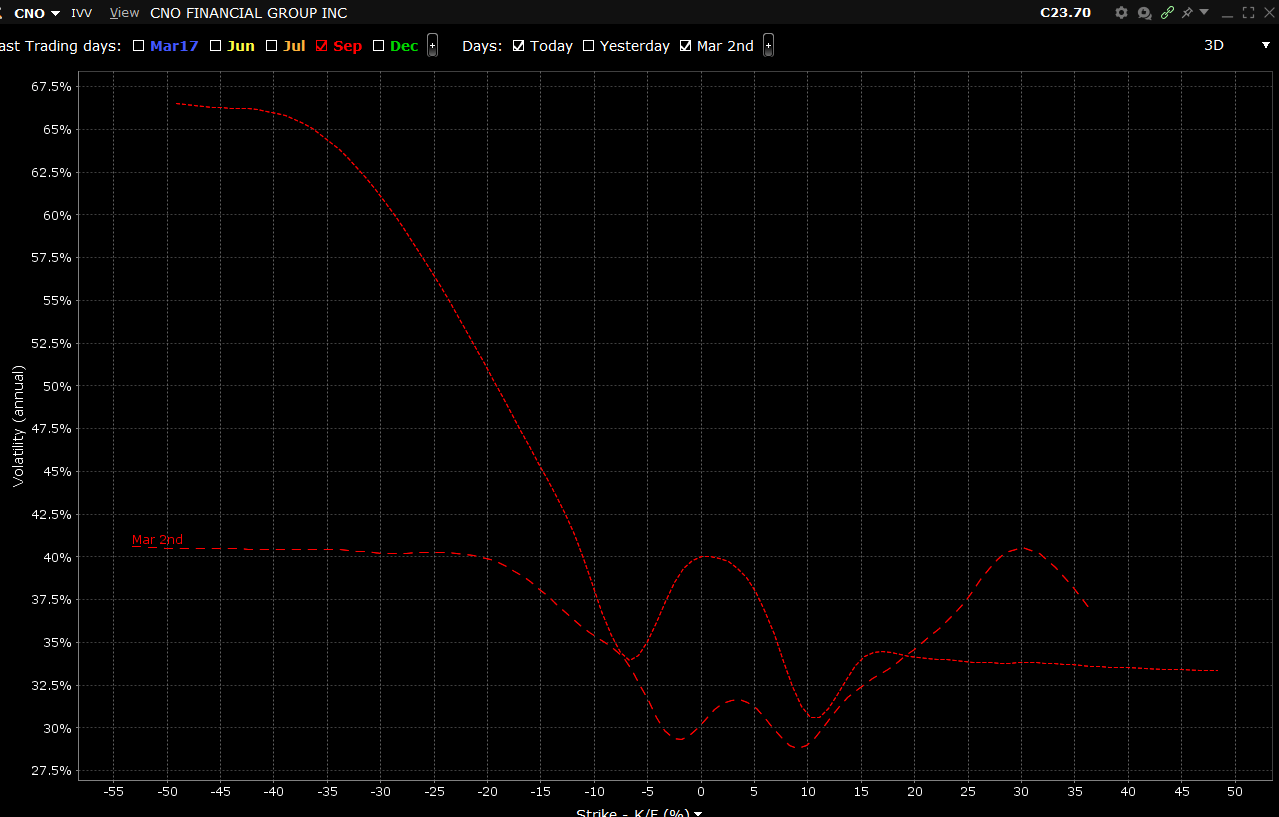

One more proof of the steady performance of CNO is the fact that the implied volatility of the common stock has been rather stable after the bank crisis in March 2023:

{kind=link}

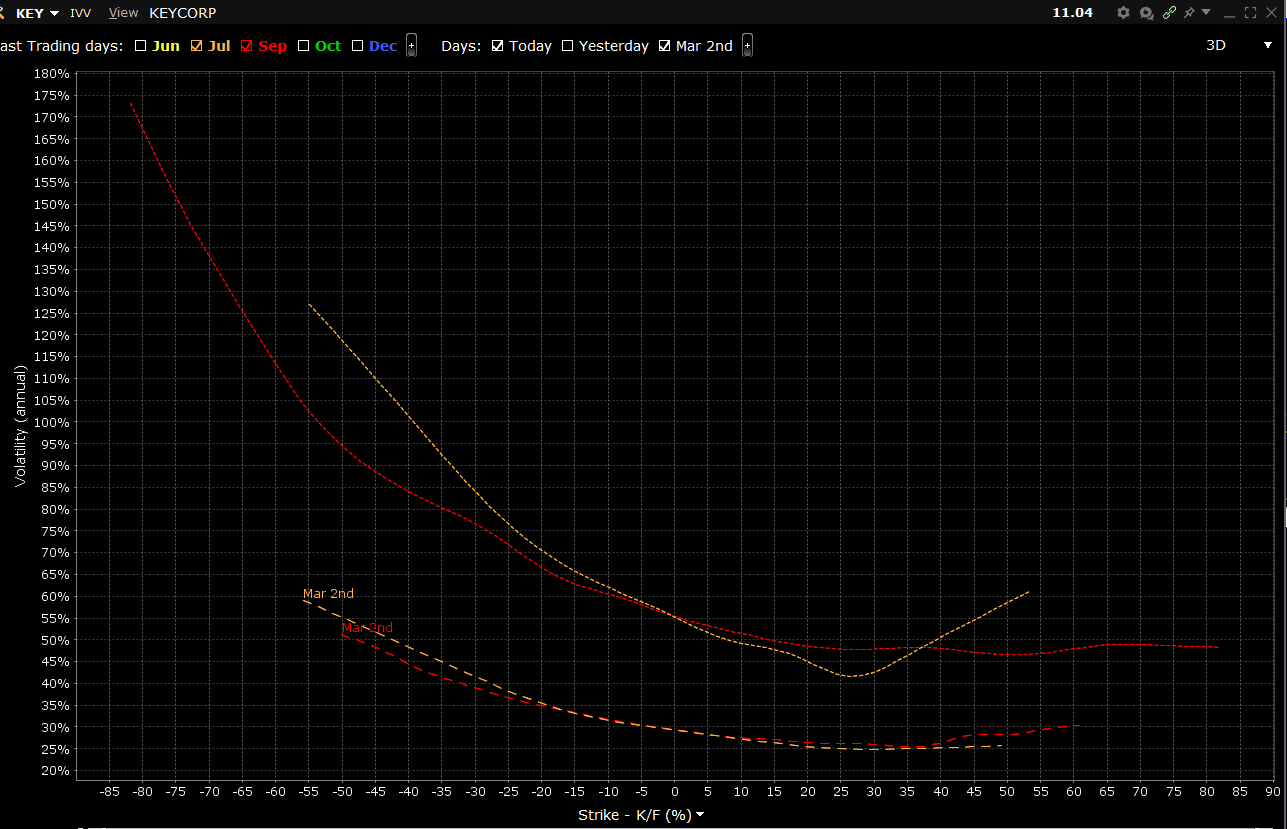

And for comparison purposes purely this is what the implied volatility of a troubled company looks like:

{kind=link}

Based on these considerations it seems that the market has not lost confidence in CNO Financial Group. Anything that signals some kind of serious trouble with the company should first be indicated in its common stock's performance, as it stays lowest in the capital structure.

The OTC traded debt

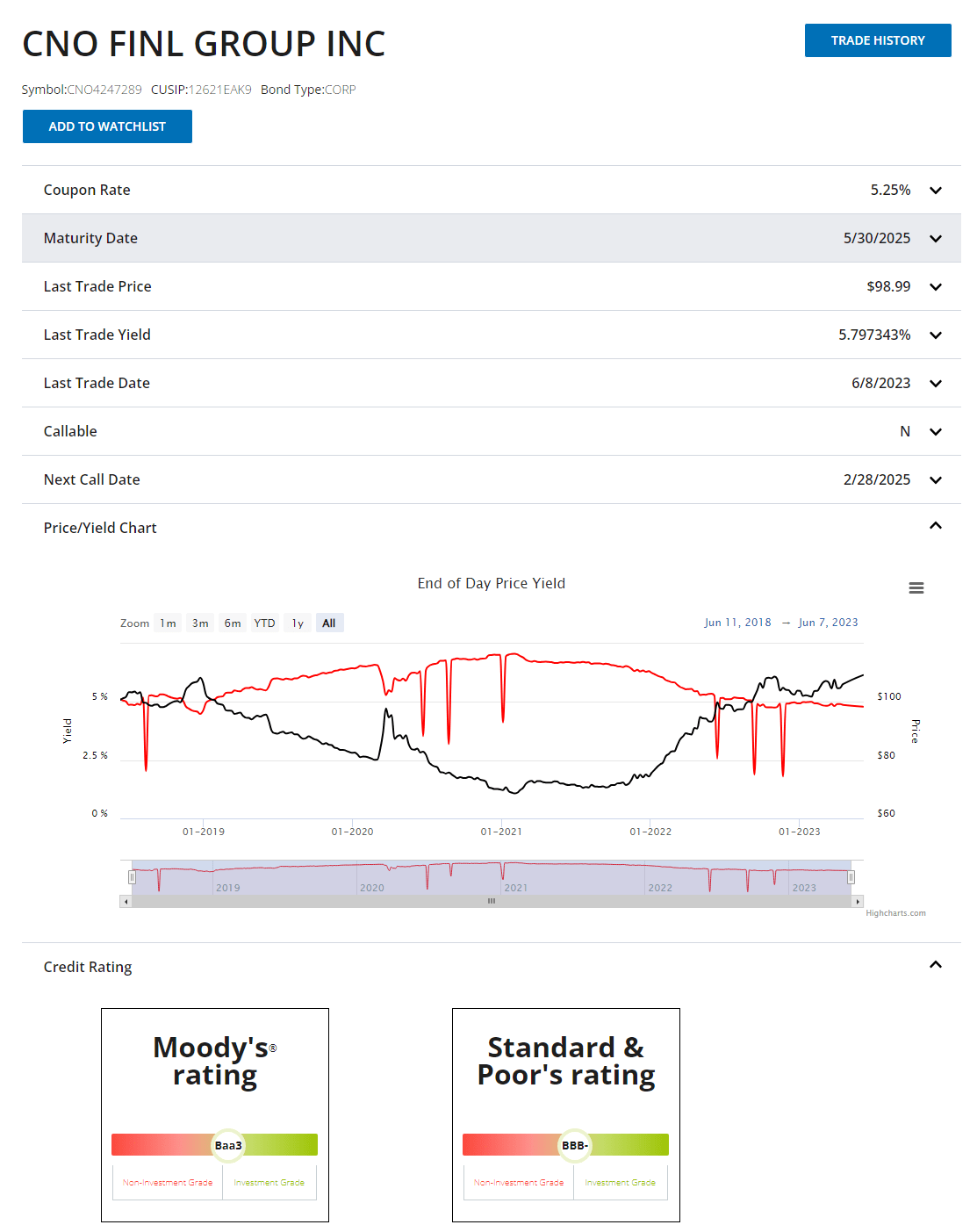

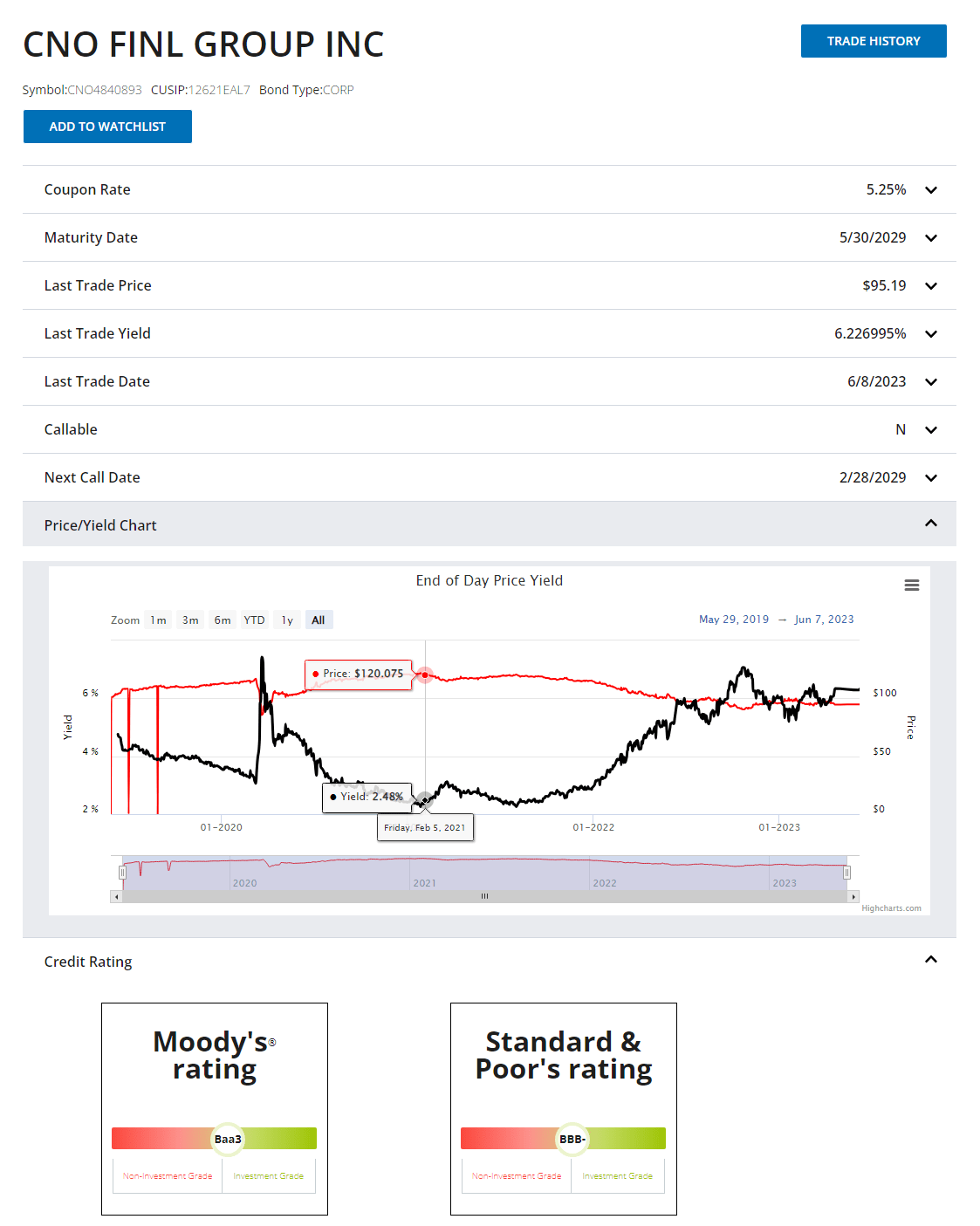

CNO Financial Group Inc. has two 5.25% fixed-rate OTC-traded bonds with CUSIPs, respectively 12621EAK9 and 12621EAL7 that are higher in the capital structure of the company compared to CNO-A.

{kind=link}

These are regular bonds and do not trade on the exchange but on the bond market where they can be found by their CUSIP numbers. Anyone who wants to invest in such kind of securities should work with a broker that allows trading them. We are going to use these two bond issues as a basis to evaluate the debt of CNO Financial Group. Below are given the main details about each issue.

{kind=link}

{kind=link}

Both OTC bonds are issued as senior unsecured debts of CNO and are rated Baa3 by Moody's and BBB- by S&P. They stand higher in the capital structure of the company compared to CNO-A which is a subordinated debenture and their credit rating is accordingly one notch higher. At the moment of writing this article, the bonds are trading with 5.8% YTM for 12621EAK9 and 6.2% YTM for 12621EAL7 respectively.

Debt issues comparison

When we are evaluating given fixed-income security's yield we compare it to its benchmark bond yield at IPO and in the moment and look for deviations in the credit spread. In this particular case, the bond we are examining has brothers issued by the same company and this fact makes our analysis even sounder, as we have additional information to step on. Using the OTC bond's credit spread as a basis can help us place CNO-A not only relating to the benchmark but also to the credit structure of the issuing company.

{kind=link}

As can be seen in the table above the credit spreads at IPO are somewhat expected - the two OTC traded bonds are issued at approximately 3% above 10-year treasuries, while CNO-A is issued at 3.5% above its benchmark - the 30-year treasuries. This is a normal IPO practice in which the lower standing in the capital structure bond receives a higher credit spread. The other thing that should be noted is that in spite of the four years difference in the IPOs of the two OTC products they receive almost the same credit spread by the underwriters. That fact is indicative of the stable performance of the company throughout the years.

The calculations for the credit spread at the moment give us a rather straightforward result - the OTC traded bonds of CNO Financial Group have narrowed the credit spreads to their corresponding benchmarks now (2-year treasuries for 12621EAK9 and 7-year treasuries for 12621EAL7) while CNO-A has widened its. These valuations of different bonds issued by the same company are rather strange to us. If the market deems the OTC bonds of CNO safer than at the time of their IPOs, then there is no logical explanation for the exchange-traded debt to trade at a higher risk premium than it did at its IPO.

Summary

Based on price action from the last couple of years, the P/E ratio and implied volatility of the common stock as well as the credit spread narrowing of the OTC traded debt of CNO Financial Group, we can conclude that at the moment the market does not indicate any particular credit danger for the company. This leads us to believe that the 9.1% YTM of CNO-A at the moment is a clear market mistake that the investors can profit from. According to our understanding, when both the higher and the lower standing in the capital structure of the company products indicate that at the moment there is no increase in the credit risk, there is no reason for the middle tier to widen its credit spread.

If the market decides to love CNO-A as much as its OTC brothers, it should trade around 20$ at 6.5% YTM. This gives the investors an over 30% capital appreciation potential for CNO-A from its current price.

For further details see:

CNO-A Is Deeply Undervalued To The OTC Debt Of CNO Financial Group