RRC - CNX Resources: Third Quarter Results Weak But Firm Enjoys Financial Strength

2023-10-31 10:45:12 ET

Summary

- CNX Resources Corporation reported disappointing Q3 2023 earnings, missing analyst expectations for both revenues and net income.

- The decline in revenues was largely attributed to lower natural gas prices compared to the same quarter last year.

- Despite the challenging results, the company remains optimistic about long-term fundamentals and expects improved free cash flow in the future.

- The company has been focused on improving its balance sheet, which is nice as it has no near-term debt maturities.

- The valuation could be questionable compared to some of its peers, but it is not too bad overall.

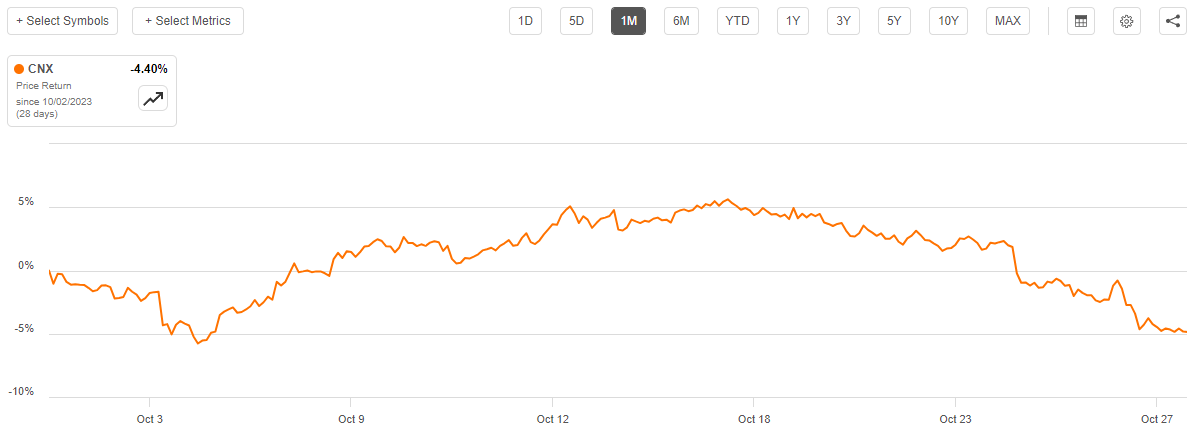

On Wednesday, October 25, 2023, Appalachian natural gas producer CNX Resources Corporation ( CNX ) announced its third quarter 2023 earnings results. At first glance, these results were rather disappointing, as the company missed the expectations of its analysts in terms of both top-line revenues and bottom-line net income. For its part, the market was not particularly understanding and it drove the company's stock price down on the day of the results announcement. This represents the continuation of a rather disappointing month for the company:

{kind=link}

This is roughly in line with the performance that we have seen from many other energy companies, however. Over the same period, the iShares U.S. Energy ETF ( IYE ) is down 4.36%, so CNX Resources' stock is not completely out of line with the rest of the sector.

A closer look at the company's results reveals that the overall performance was generally disappointing. This was not altogether unexpected though considering the price action of the commodities markets over the past year, and it seems likely that many of the company's peers will also post disappointing results when they announce their own results over the upcoming weeks. The long-term fundamentals continue to remain intact, though, and holders of the company should probably continue to do so. It could be a little while for the story to play out though so patience is a virtue here.

Earnings Results Analysis

As long-time readers are no doubt well aware, it is my usual practice to share the highlights from a company's earnings report before delving into an analysis of its results. This is because these highlights provide a background for the remainder of the article as well as serve as a framework for the resultant analysis. Therefore, here are the highlights from CNX Resources' third-quarter 2023 earnings results:

- CNX Resources received total revenues of $302.5 million during the third quarter of 2023. This represents a 74.33% decline over the $1.1786 billion that the company brought in during the prior year quarter.

- The company reported an operating income of $50.3 million during the reporting period. That compares quite favorably to the $207.3 million operating loss that the company suffered during the year-ago quarter.

- CNX Resources produced an average of 1.5590 billion cubic feet of natural gas equivalent per day during the most recent period. That represents a 2.01% decrease over the 1.5909 billion cubic feet of natural gas equivalent that the company produced per day on average during the equivalent quarter of last year.

- The company reported a negative levered free cash flow of $26.9 million during the current period. That compares quite favorably to the negative $53.2 million levered free cash flow that the company had in the corresponding quarter of last year.

- CNX Resources reported a net income of $21.4 million during the third quarter of 2023. This compares very favorably to the $427.1 million net loss that the company reported during the third quarter of 2022.

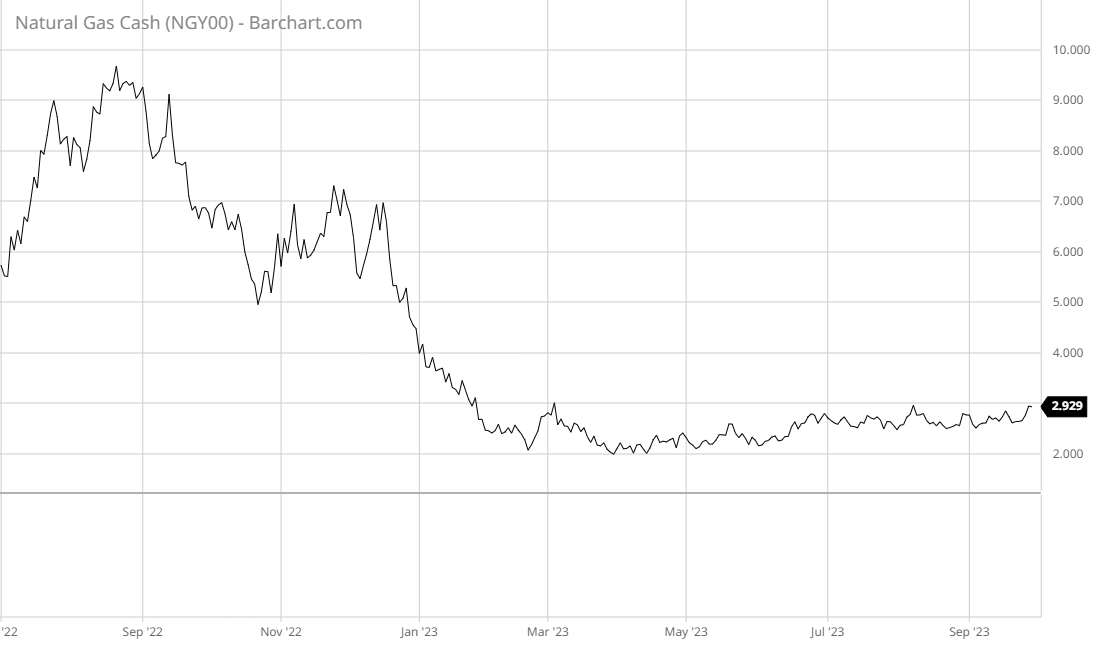

It seems essentially certain that the first thing that anyone reviewing these results will notice is that the company's revenues declined substantially compared to the third quarter of 2022. As might be expected, the biggest reason for this is that natural gas prices were much lower during the most recent quarter than they were a year ago. We can see that quite clearly here:

{kind=link}

As I have discussed previously, the United States has been oversupplied with natural gas for quite a while. This was caused by two factors:

- The winter of 2022 was much warmer than normal;

- The Freeport LNG plant was out during the second half of 2022, which removed a significant source of demand from the market.

Natural gas prices tend to be much more local than crude oil due to the difficulty of transporting it internationally. Thus, these two factors reduced demand sufficiently to cause natural gas prices to decline. The Freeport LNG plant is now back online and natural gas producers have reduced their production somewhat, but thus far it has not been sufficient to tighten the supply-demand balance for natural gas in the United States. The National Oceanic and Atmospheric Administration predicts that this coming winter will also be warmer than normal so we cannot expect demand to rise significantly from Americans trying to heat their houses. Thus, natural gas prices may remain range-bound at levels below 2022 averages for a while longer.

It should be immediately obvious why lower natural gas prices would have an adverse impact on CNX Resources' results. After all, the company is an Appalachian shale producer that produces mostly natural gas. The company's guidance projects that only about 7% of its production will be liquids, so that means that 93% of its total production is expected by its own management to be natural gas. Thus, natural gas prices in the market largely dictate the amount of money that the company receives for each unit of product that it sells. The fact that natural gas prices were lower during the most recent quarter than they were during the equivalent quarter of last year means that the company would bring in less revenue, all else being equal. As a general rule, lower revenue means that every other measure of financial performance will come in weaker because the company has less money available to cover its fixed expenses and make its way down to profits or cash flow.

Naturally, all else is rarely equal with upstream independent exploration and production companies like CNX Resources. As we can clearly see in the highlights, the company's production came in a bit lower than in the prior-year quarter.

| Q3 2023 |

| Q3 2022 |

| Shale Sales Volumes (bcf) |

| 121.1 |

| 125.1 |

| CBM Sales Volumes (bcf) |

| 10.2 |

| 10.7 |

| Other Sales Volumes (bcf) |

| 0 |

| 0.2 |

| NGL Sales Volumes (bcfe) |

| 11.9 |

| 10.2 |

| Oil and Condensate Sales Volumes (bcfe) |

| 0.2 |

| 0.2 |

| Total (bcfe) |

| 143.4 |

| 146.4 |

As we can see, the company's natural gas production was down year-over-year, although liquids production was up slightly. This exerted a negative impact on the company's revenues and by extension profit and cash flow. The reason for this should be fairly obvious. After all, if the company has lower production then it has fewer goods with which it can convert into revenue.

Thus, we have a situation in which the company's product pricing was lower and its sales volumes were down. It is only natural that the company's revenues would come in much worse than we saw in the prior-year quarter.

With that said, eagle-eyed readers will likely note that CNX Resources' profits actually came in a bit stronger than they did in the prior-year quarter. This is despite the fact that revenue was significantly lower year-over-year. The biggest reason for this is that CNX Resources suffered a substantial loss on commodity derivative instruments during the third quarter of last year. The company's income statement from last year shows a $1.062353 billion loss on commodity-linked derivatives. That was sufficient to offset the impact of the much stronger revenues and drag down all of the company's financial figures. There is no such loss in the most recent quarter (in fact, the third-quarter 2023 income statement shows a $47.833 million gain on the same derivative instruments).

This is, unfortunately, something that we just have to deal with when it comes to this company. As I pointed out in a previous article on CNX Resources, the company uses commodity-linked derivatives as a method of managing its overall exposure to commodity prices. This has the effect of stabilizing its cash flow over the long term, but it does mean that sometimes there will be a significant gain or loss during a given quarter if natural gas prices move very rapidly. This is the biggest reason why the company's reported earnings from this quarter came in better than its reported earnings from last quarter despite the steep decline in revenues.

During the company's third quarter earnings conference call , Nick Deiuliis, CNX Resources' President and CEO, made a pretty big deal out of the company's free cash flow generation during the quarter. He stated:

The third quarter represented the 15th consecutive quarter of free cash flow generation. Utilizing this free cash flow, we continued to repurchase shares, and cumulatively, since the inception of the buyback program in 2020, we have retired approximately 31% of our outstanding shares. We believe that our share repurchase program provides an opportunity to create incredible value for our long-term, like-minded shareholders, who will benefit as their per share value continues to grow meaningfully over the coming years.

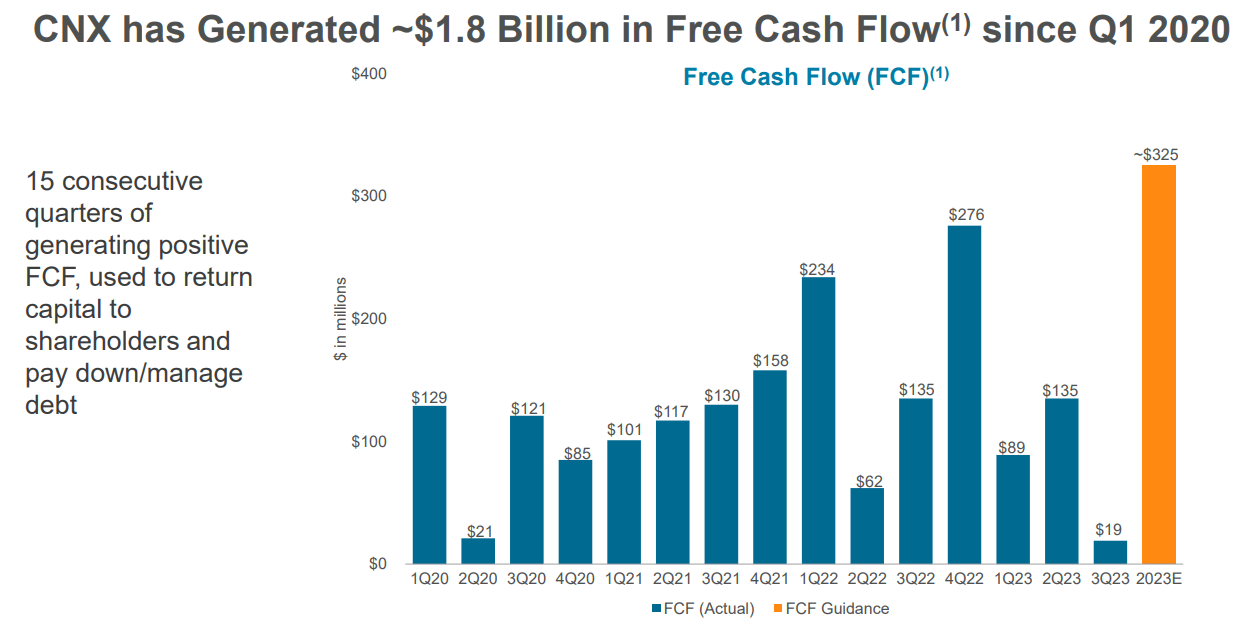

The company goes on to state that it had a free cash flow of $19 million in the third quarter, which is far lower than it had in any quarter since the start of 2020:

{kind=link}

This is in direct contrast to the negative leveraged free cash flow of $26.9 million that is presented in the highlights. The biggest reason for this discrepancy is that CNX Resources is using a non-standard definition of free cash flow. The usual definition of free cash flow is operating cash flow minus capital expenditures. Levered free cash flow subtracts the company's mandatory interest payments on its debt as well. However, CNX Resources is actually adding in its proceeds from asset sales and excludes debt payments completely. The company received $19.1 million from the sale of assets in the third quarter, which explains the discrepancy.

Normally, we will not want to include asset sales in free cash flow because it is a non-standard transaction. Free cash flow is a metric that is intended to tell us how much money a company generates from its ordinary operations after it pays all of its bills and makes all capital expenditures. CNX Resources' cash flow statement consistently shows asset sales in every quarter going back at least until the start of 2021. Thus, it appears that selling its assets is a regular part of business for this company, which may explain why it considers the proceeds of these sales to be part of its free cash flow.

Management stated in the conference call that it expects this quarter to be the worst for its free cash flow. Alan Shepard, CNX Resources' chief financial officer stated:

Looking ahead, we expect this quarter to mark the trough of our free cash flow generation, as the confluence of lower capital, higher expected gas pricing and growth in our New Tech cash flows, solidifies our confidence in achieving robust free cash flow generation in the quarters ahead.

There may be some reasons to believe that this scenario will play out. As I have discussed in numerous articles that went out to Energy Profits in Dividends subscribers (such as this one ) the global and domestic demand for natural gas is expected to surge over the coming years. This should pressure the price of natural gas upward as it causes the supply glut to ease. After all, it seems unlikely that producers of the compound will boost their production much until prices increase on a sustainable basis.

Financial Considerations

As I explained in various previous articles:

It is always important that we analyze the way in which a company is financing its operations before making an investment in it. This is because debt is a riskier way to finance a company than equity because debt must be repaid at maturity. This is usually accomplished by issuing new debt and using the proceeds to repay the existing debt. That can cause a company's interest expenses to increase following the rollover in certain market conditions.

As of the time of writing, interest rates are at the highest levels that we have seen since 2001 so it seems certain that any debt rollover will cause a company's interest expenses to increase. Indeed, a number of highly indebted companies throughout the economy have either started to grapple with this or will have to deal with this problem by 2025.

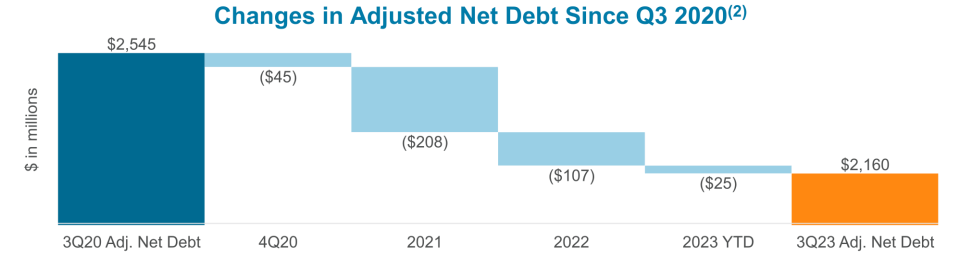

Fortunately, CNX Resources has been fairly proactive about addressing its debt and strengthening its balance sheet . As of September 30, 2023, CNX Resources has an adjusted net debt of $2.160 billion. This represents a fairly dramatic decrease from the $2.545 billion that it had exactly three years ago:

{kind=link}

Basically, what the company has been doing is that it has been using some of the cash that it was able to generate during the high energy price environment over the full-year 2021 and 2022 periods to pay down its debt. This is something that many energy companies have been doing over the period since the market taught them all a very harsh lesson about depending on it for capital during the pandemic and the following year. This is a much better situation than we see in the utility sector, which has seen some companies actually increase their net debt despite the very high interest rates.

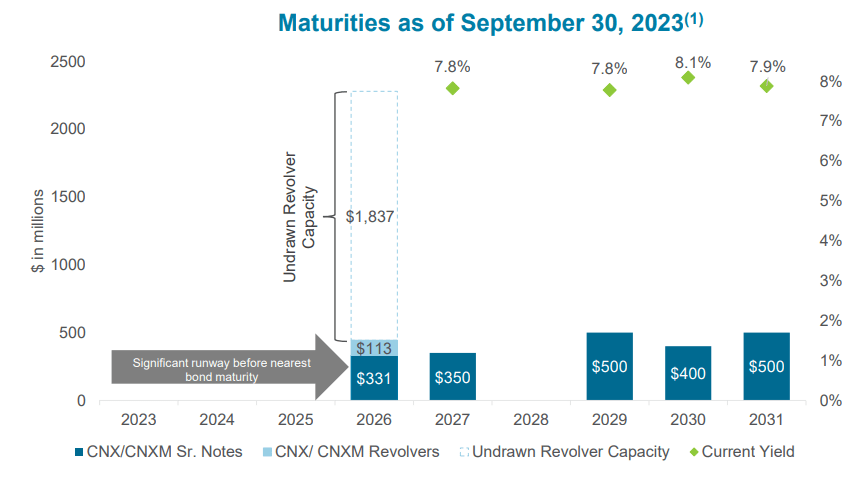

Investors should also be able to take some comfort in the fact that CNX Resources does not have any debt maturities until 2026:

{kind=link}

This gives the company some advantages right now as it does not need to roll over debt in the near future. It has some options as to how it wishes to deal with the debt. For example, if natural gas prices stage an improvement by 2026 then it could very easily pay down some of this debt with its cash flow and reduce the amount that it needs to roll over. Alternatively, the market expects that interest rates will be lower by 2026. I personally do not believe that this will be the case, as I explained in a recent article . Nonetheless, it is possible that rates could drop if the United States enters a severe recession. In short, though, the company has options here that it would not have if it were not proactive about managing its debt and improving its balance sheet as the opportunity presented itself.

Valuation

According to Zacks Investment Research , CNX Resources will grow its earnings per share at a 5.56% rate over the next three to five years. This gives the company a price-to-earnings growth ratio of 2.45 at the current price, which suggests that the stock may be overvalued relative to its forward earnings growth. This would be a departure from the general trend across the energy sector over the past two years. As I have pointed out in the past, most fossil fuel producers have traded at a discount to their forward earnings growth.

Here is how CNX Resources' valuation compares to its peers:

| Company |

| PEG Ratio |

| CNX Resources |

| 2.45 |

| Range Resources ( RRC ) |

| 0.58 |

| Antero Resources ( AR ) |

| N/A |

| Comstock Resources ( CRK ) |

| N/A |

| EQT Corporation ( EQT ) |

| 0.97 |

Zacks is projecting that Antero Resources and Comstock Resources will both see their earnings come in below 2022 levels for the near term. That is certainly a reasonable expectation, especially if the coming winter is warmer than normal. However, both Range Resources and EQT Corporation look much cheaper than CNX Resources right now based on their earnings per share growth.

At the same time, CNX Resources trades with a forward price-to-earnings ratio of 13.62 at the current price. That is quite a bit cheaper than the S&P 500 Index ( SP500 ), so the stock does not appear to be an especially terrible deal right now.

Conclusion

In conclusion, CNX Resources' third quarter 2023 results certainly showed the impact that low natural gas prices had on the company. These low prices exerted a significant adverse impact on its revenues, although it still managed to maintain a certain degree of financial strength. The long-term story remains strong here, as natural gas demand is expected to grow over the coming years. It could be a multi-year thesis, though, as there could be some reasons to believe that the United States will be oversupplied with natural gas for a little while.

For further details see:

CNX Resources: Third Quarter Results Weak, But Firm Enjoys Financial Strength