BTU - Coal Isn't Dead! I'm Bullish On Peabody Energy

2023-11-16 17:17:34 ET

Summary

- Peabody Energy is a coal company that can be used as a trading tool to track energy prices and geopolitical developments.

- Geopolitical developments and rising natural gas prices are favoring U.S. coal exports, potentially leading to increased demand for coal.

- Peabody's strong volumes and favorable outlook suggest potential for shareholder distributions and aggressive buybacks.

Introduction

It's time to talk about a company I've monitored for many years: Peabody Energy ( BTU ) , one of the largest coal companies in the world.

Essentially, there are two reasons why I cover coal stocks.

- Companies like BTU are terrific trading tools, as they track the price of coal and can be used as proxies for changing energy prices and geopolitical developments.

- When covering the big guys like BTU, we learn a lot about the industry, which tends to give us info that is usable well beyond the coal industry. Think of natural gas, renewables, and intel regarding the health of cyclical industries like steel production.

There's a third (minor) reason. I'm long Union Pacific ( UNP ), which ships coal for Peabody.

In this article, I'll explain why I believe that the risk/reward for Peabody is favorable. The stock is trading roughly 30% below its 2022 highs. It is down 12% year-to-date and unchanged since Russia set foot in Ukraine in early 2022.

Although economic risks remain very elevated, I believe there's good news on the horizon.

- Geopolitical developments favor U.S. coal exports.

- I'm bullish on natural gas. Rising prices give coal an edge as a cheap but dirty alternative.

- BTU is doing well. Its operations are running smoothly, volumes are strong, and its balance sheet is in great shape, paving the way for aggressive buybacks.

Before I go any further, I have to say that BTU is volatile - very volatile. As I already briefly mentioned, the main goal of this article is to discuss the coal market, not to push people into coal stocks.

As I almost exclusively cover dividends and similar long-term investments, BTU may not be right for you. Please be aware of that before you continue reading.

Coal Isn't Dead!

I'm not a big fan of coal. It's dirty, mining it is dangerous, and we have increasingly affordable alternatives like natural gas, nuclear energy, and related.

However, I do not support the "war" against coal for two reasons.

- Major economies have relied on coal production for centuries. Abruptly shifting away from coal has major societal implications. Think of Germany's Ruhrgebiet or the Appalachia region in the U.S.

- Coal is one of the cheapest forms of energy and one of the biggest sources of global energy (as seen in the chart below). While I agree with a gradual transition, a forced transition is expensive, very expensive, as we're currently finding out the hard way.

OurWorldInData

The other day, the Wall Street Journal wrote an article titled The Path To Green Energy Is Getting Messier .

According to the article, the energy transition, once hailed as a swift shift towards renewable sources is encountering challenges.

Offshore wind projects are being abandoned, renewable-energy company stocks are plummeting, and U.S. automakers are scaling back electric vehicle plans due to faltering demand.

Somewhat unexpected to many, the oil and gas industry is thriving with megadeals fueled by soaring profits.

Fossil fuel advocates argue that these resources will remain vital as carbon emissions are projected to reach record levels this year.

I agree with that.

On top of that, geopolitical developments continue to favor U.S. coal exports.

As reported by the U.S. Energy Information Administration, U.S. coal exports witnessed a notable increase of 5.7 million short tons (MMst) in the year following the implementation of EU sanctions on Russian coal in August 2022.

The surge was predominantly fueled by a 22% rise in U.S. coal exports to Europe, reaching 33.1 MMst between August 2022 and July 2023.

Energy Information Administration

In response to Russia's invasion of Ukraine in February 2022, the EU imposed sanctions on Russian coal in April 2022, with a grace period until August 2022 for pre-existing contracts.

Subsequently, a ban on European purchases of Russian coal led to a near cessation of imports, causing the United States, along with other coal-supplying nations, to fill the void.

Energy Information Administration

Especially if Europe gets a cold winter, I expect coal demand to accelerate.

Bear in mind that last winter was very mild, causing nations like the Netherlands to become net exporters of coal! The Netherlands does not produce coal. It sold inventories it didn't need anymore.

It put tremendous pressure on coal prices. The same goes for natural gas.

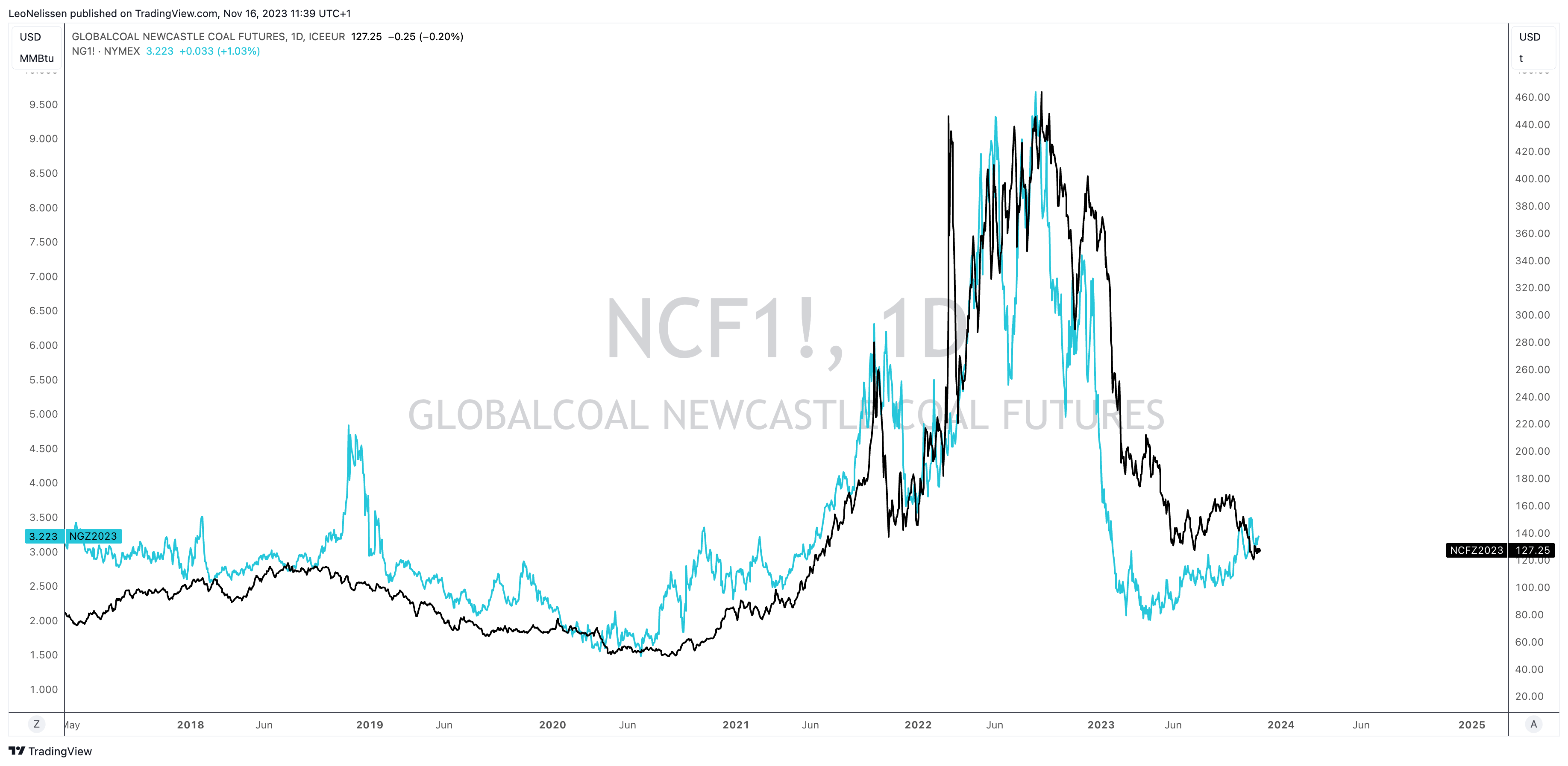

Now, it seems that natural gas prices have bottomed. After a massive decline, Henry Hub Natural Gas prices have been in an uptrend since April of this year (the blue line in the chart below). While major coal benchmarks like Newcastle Coal (black line) have continued to weaken, I expect to see bottoming coal prices in the months ahead.

{kind=link}

TradingView (HH Natural Gas, Newcastle Coal)

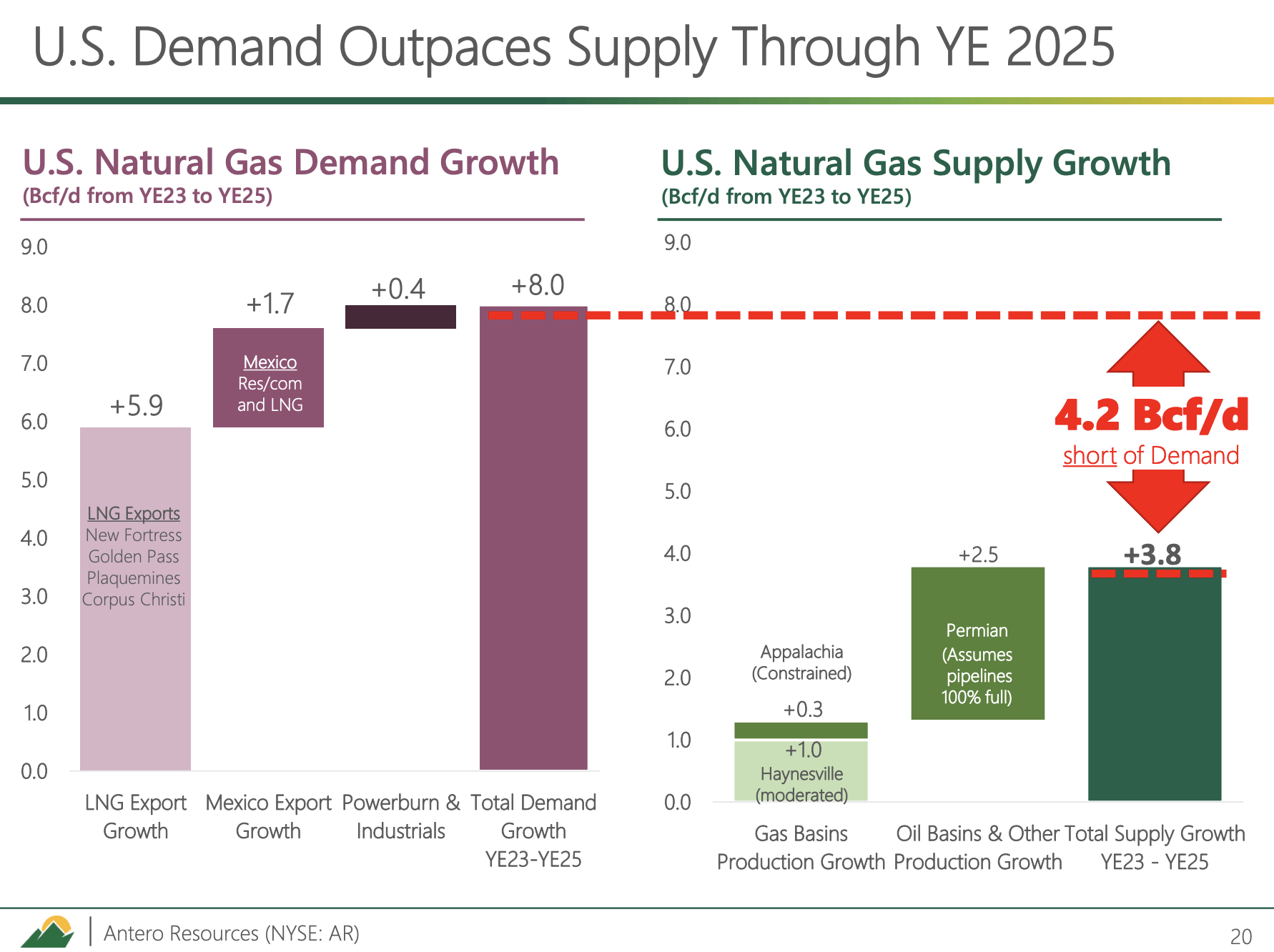

Meanwhile, natural gas benefits from an increasing supply gap. Antero Resources ( AR ), one of America's largest natural gas producers, estimates a 4.2 billion cubic feet per day supply gap through 2025, fueled by massive LNG exports.

{kind=link}

Antero Resources

This means the main reason why natural gas prices were low before the pandemic is gone. That's bullish for coal as well.

If I'm right, we could see both volume and pricing tailwinds for Peabody.

Peabody Is Where It's At

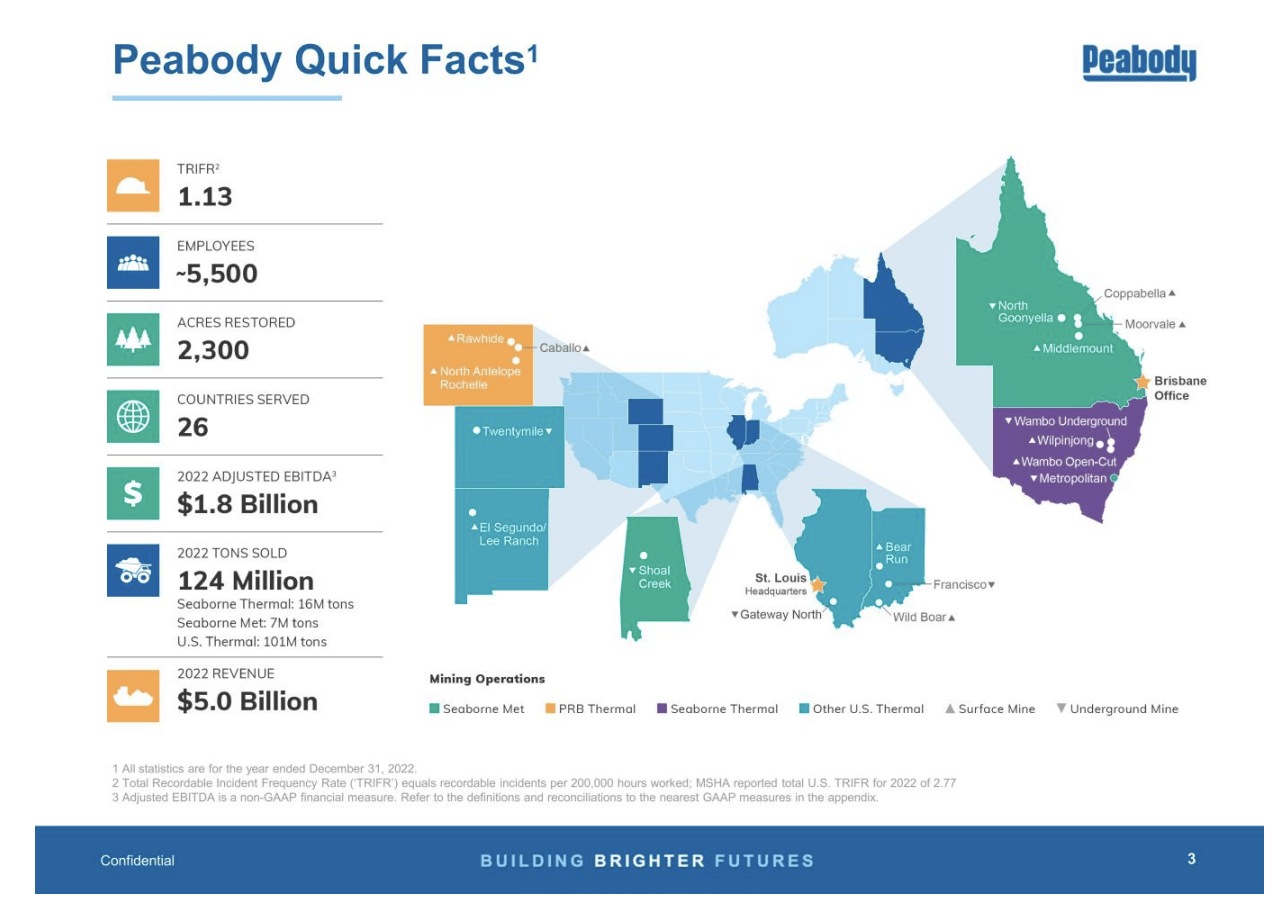

Peabody is the owner of the North Antelope Rochelle Mine, the world's largest coal mine in the world. It also owns other mines, including assets in Australia.

Last year, it sold more than 120 million tons of coal. Most of its production is thermal coal, often used by utilities.

{kind=link}

Peabody Energy

Although its largest markets are the U.S. and Japan, two nations that are moving away from coal, it does benefit from global pricing benefits and higher export demand.

In its third-quarter earnings call, the company noted that seaborne thermal coal markets experienced volatility, with modest pricing improvements.

Factors such as coal and natural gas inventories in the Northern Hemisphere, weather conditions in Australia, and increased coal imports by China and India were discussed :

Seaborne thermal coal markets remained volatile during the quarter with modest pricing improvements. Robust, but moderating coal and natural gas inventories in the Northern Hemisphere have continued to weigh on demand for high-energy thermal coal, coupled with better supply prospects due to drier weather on Australia's East Coast, resulting in Newcastle coal trading within a range of $130 to $160 a ton. China's year-to-date imports of lower-grade thermal coals continue to significantly surpass the prior year, with an increase in the annual thermal coal input run rate of approximately 93% over 2022 levels. India has also increased seaborne market participation, as our power demand continues to grow.

At the end of October, the International Energy Agency reported a 6% YoY growth in overall seaborne coal trade.

In the United States, electricity generation from thermal coal declined YoY due to low gas prices and growing renewable generation.

However, near-term demand for U.S. thermal coal is anticipated to be supported by higher gas prices. The third quarter saw improvements in coal burn compared to the previous quarter.

So far, the company seems to see the same developments that I'm monitoring and relies on the same bull case.

It also benefits from strong volumes.

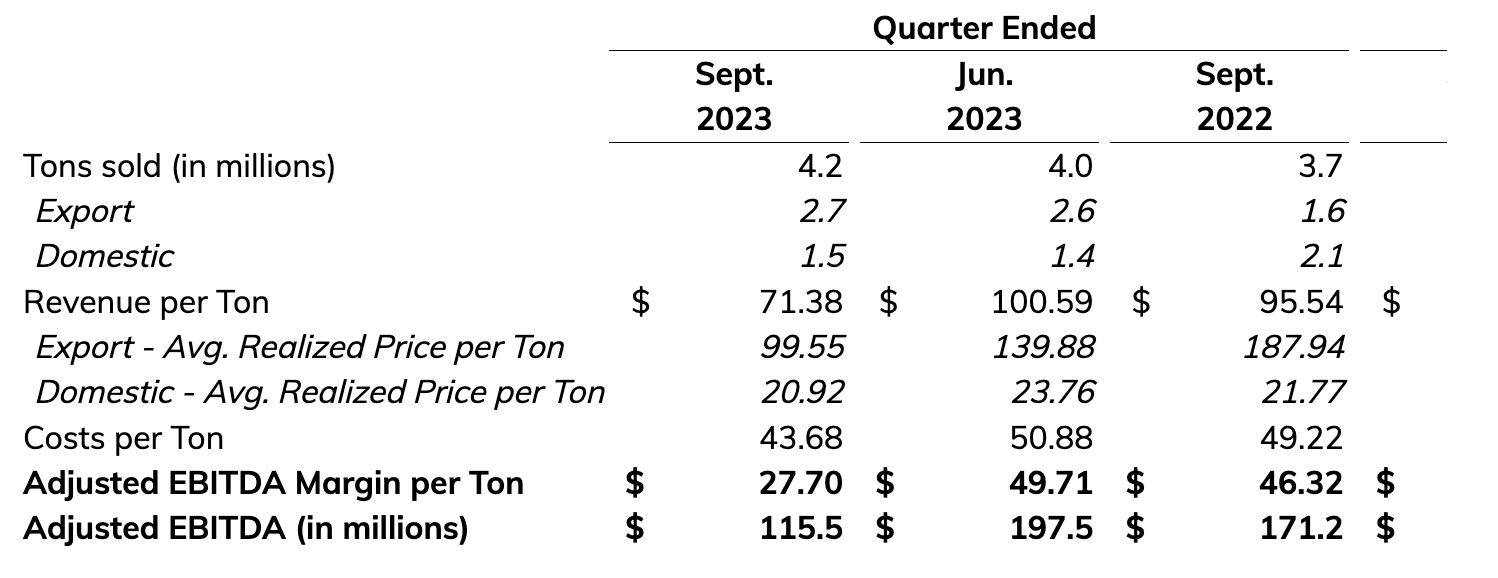

In the third quarter, seaborne thermal coal exports reached 2.7 million tons, with segment costs per ton lower than in the second quarter.

{kind=link}

Peabody Energy

- Seaborne metallurgical segment shipments were 1.5 million tons, with total segment costs per ton 20% lower than the second quarter.

- Shoal Creek showed progress towards resuming longwall production, potentially ahead of schedule.

- PRB (Powder River Basin) shipments of 22.7 million tons exceeded expectations, with cost reductions and margin expansion.

{kind=link}

Peabody Energy

- Active operations in other U.S. thermal segments saw an increase in shipments to 4.2 million tons, driven by customer demand.

The company's outlook was also strong.

- The seaborne thermal cost guidance was lowered to $45 to $50 per ton.

- Fourth-quarter seaborne thermal export volumes are expected to increase, with costs projected at $45 to $50 per ton.

- Seaborne metallurgical volumes are projected to be 45% higher in the fourth quarter, with costs expected to be $110 to $120 per ton.

- In the PRB, shipments of 21 million tons are anticipated, and other U.S. thermal shipments are expected to be 4.1 million tons in the fourth quarter.

When adding the tailwinds of pricing and volumes, we get fertile ground for shareholder distributions.

Through October 20, the company returned $307 million to shareholders, reducing the share count by 9.3%.

There is $713 million remaining under the share repurchase program.

The commitment to return at least 65% of annual available free cash flow to shareholders remains steadfast.

The reason BTU is able to buy back stock is because of its healthy balance sheet. The company is net cash positive, meaning it has more cash than gross debt.

This is great, as it paves the way for aggressive buybacks.

Next year, the company is expected to generate $530 million in free cash flow. 65% (buyback target) of that is $345 million. This translates to 11% of its $3 billion market cap.

While free cash flow expectations are subject to significant changes, it shows how strong the company's buyback potential is.

If I'm right and coal prices rebound, free cash flow will be much higher in the years ahead.

Valuation

This is the tricky part.

After all, BTU is highly tied to coal prices.

Also, analysts believe coal prices are in a long-term decline.

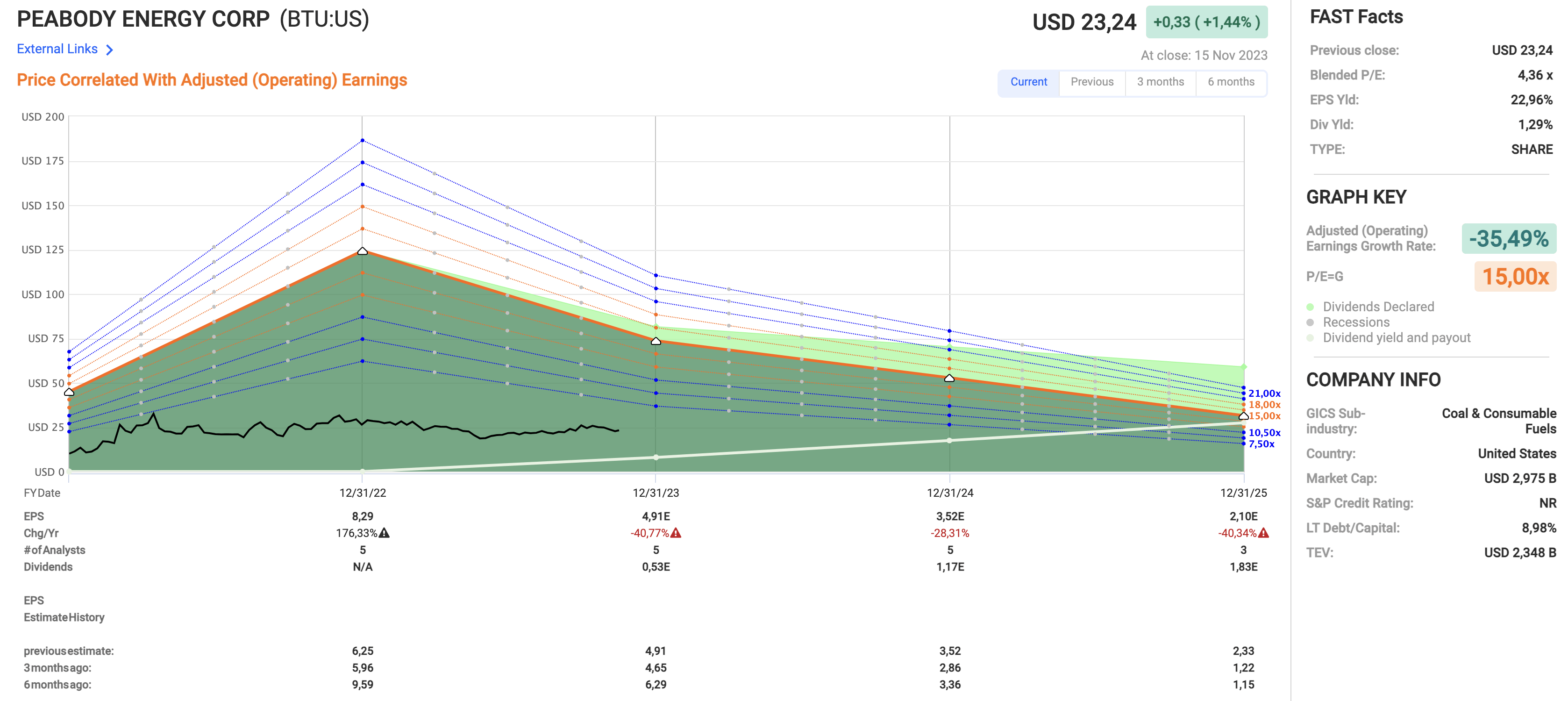

Using the numbers in the chart below:

- EPS is expected to decline by 41% this year.

- EPS is expected to decline by 28% in 2024.

- EPS is expected to decline by another 40% in 2025.

- In other words, $8.29 in 2022 EPS is expected to fall to $2.10 in 2025 EPS.

- Compared to six months ago, 2023 expectations have come down significantly.

- 2024 and 2025 expectations have been raised in the past six months.

{kind=link}

FAST Graphs

I believe that the company's 2024 and 2025 actual results will be higher than expected. While we'll likely see results below 2022 levels due to that year being very unusual, I expect that BTU benefits from slowly bottoming coal prices with more upside if rising natural gas prices give coal a bigger boost.

If my thesis is correct, I would expect BTU to break its 2022 highs in 2024, followed by an uptrend to $40.

However, that requires:

- Further rising natural gas prices (I think we could see $4.50 to $5.00 Henry Hun).

- Rebounding economic growth.

While we could see some short-term stock price downside, I like the mid-term risk/reward for 2024.

For further details see:

Coal Isn't Dead! I'm Bullish On Peabody Energy