COKE - Coca-Cola Consolidated Inc.: A Strong Buy For Long-Term Investors

2023-03-28 07:17:27 ET

Summary

- Strong financial results caught my interest as margin expansion was very impressive in my opinion.

- Coca-Cola Consolidated is very healthy on the books, with no apparent red flags.

- For the DCF valuation, I assume a slowdown in revenues and a contraction in margins in the first 2 years, followed by a slight recovery.

- Conservative estimates suggest the company is still undervalued and is a good contender for a long-term investment.

Investment Thesis

Solid FY2022 results, with improvement in margins, tell me that Coca-Cola Consolidated ( COKE ) could be a viable long-term hold. In this article, I will look at how the company has performed over the last few years, and how it may perform in the future via a DCF model, and will talk about the health of the company's balance sheet. I will argue that even if the company does not manage to improve net and operating margins over the decade, the company still is in a strong position to reward shareholders in the long run.

Coca-Cola Consolidated is the main distributor of Coca-Cola beverages in the US. The syrup is supplied by The Coca-Cola Company ( KO ). The company also bottles other non-alcoholic beverages including Fanta, Sprite, Dasani, and Powerade, and products licensed to the company like Dr Pepper ( KDP ), Monster Energy Products ( MNST ), and Dunkin' Donuts products.

FY2022 was not a bad year for the company. Revenues increased by over 11% y-o-y; net Income exploded by 126. Gross margins seem to have expanded 160bps, EBITDA % expanded 200bps and net margins doubled, going from 3.4% to 6.9%, an increase of 350bps. Not too shabby when many companies have seen contractions in margins during 2022, which was a very tough and volatile year for many.

In the last 10 years, the company did not see negative growth in revenues, even during the 2020 lockdowns. In 2019 and 2020, the company managed to grow revenues at 4% per year, suggesting that people have a hard time kicking these drinks. I believe the company is well positioned for the future, especially if we do see some sort of a downturn in the economy in the next 12-24 months and I would expect the company to still eke out some revenue growth for those years.

Financials

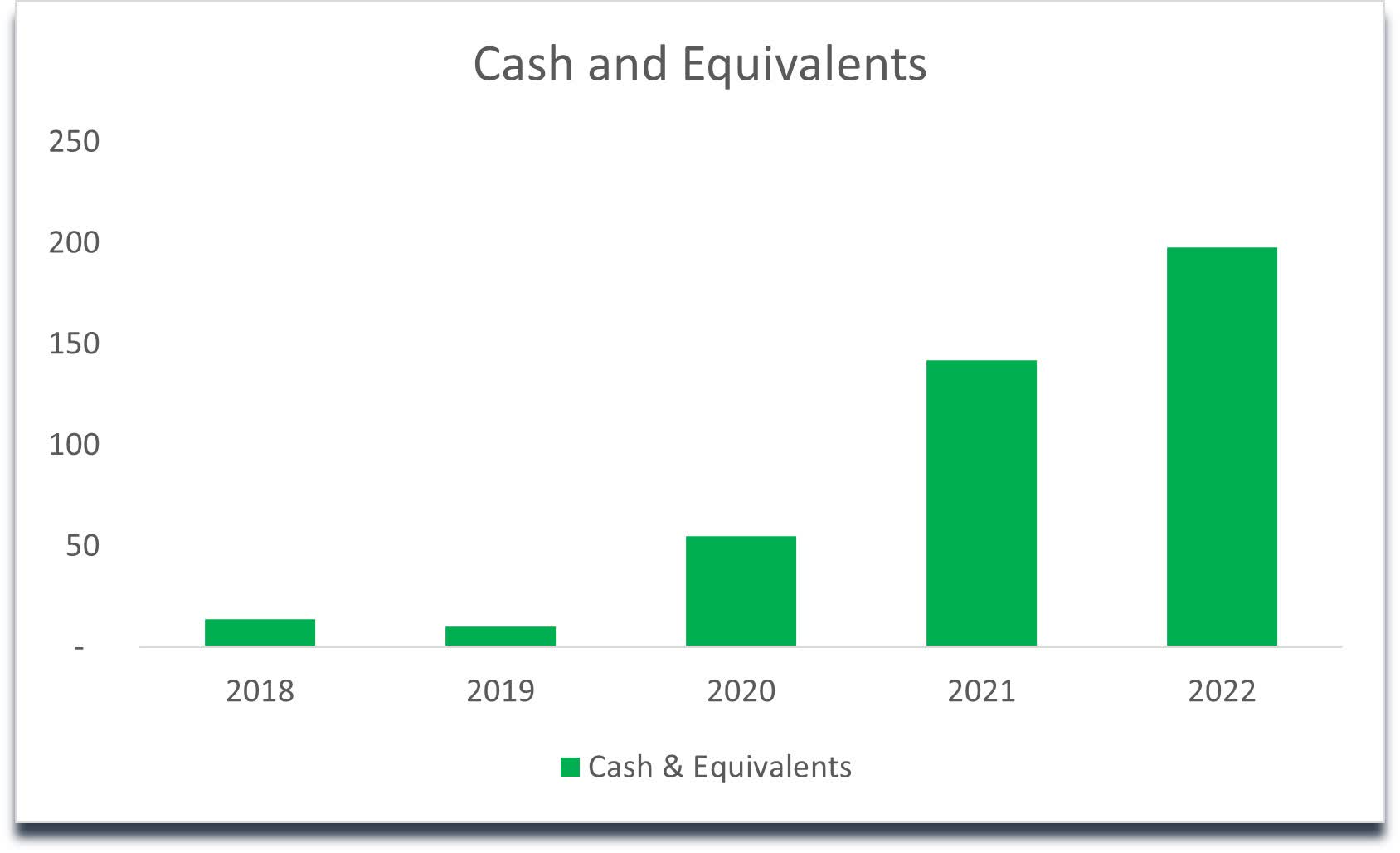

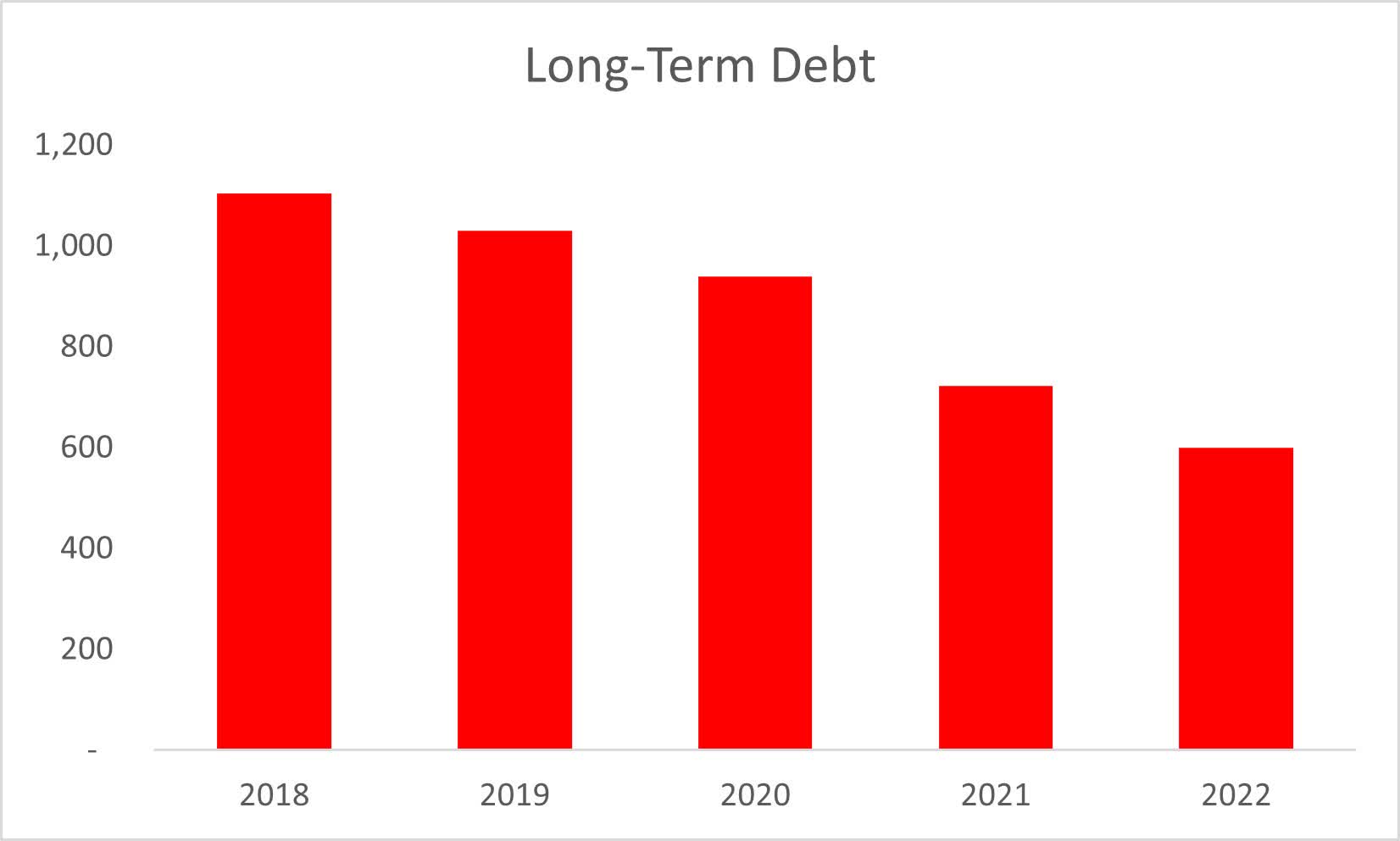

The company has been growing its cash position quite well over the last 5 years. It is still not enough to cover the outstanding debt, however, the debt position has been coming down nicely too and I don't see this to be an issue in the long run. The Debt/Asset ratio is well below the warning levels, sitting at 0.16. The interest coverage ratio has been quite bad in 2018 but it has increased quite dramatically since and now it is sitting at 25.64. With the continuation of debt reduction in the future, the company will become unleveraged and very liquid. This will help the company reward its shareholders in the long run in terms of stock price appreciation, maybe even stable dividend increases as the company finally increased dividends by 100% and start repurchasing shares.

{kind=link}

{kind=link}

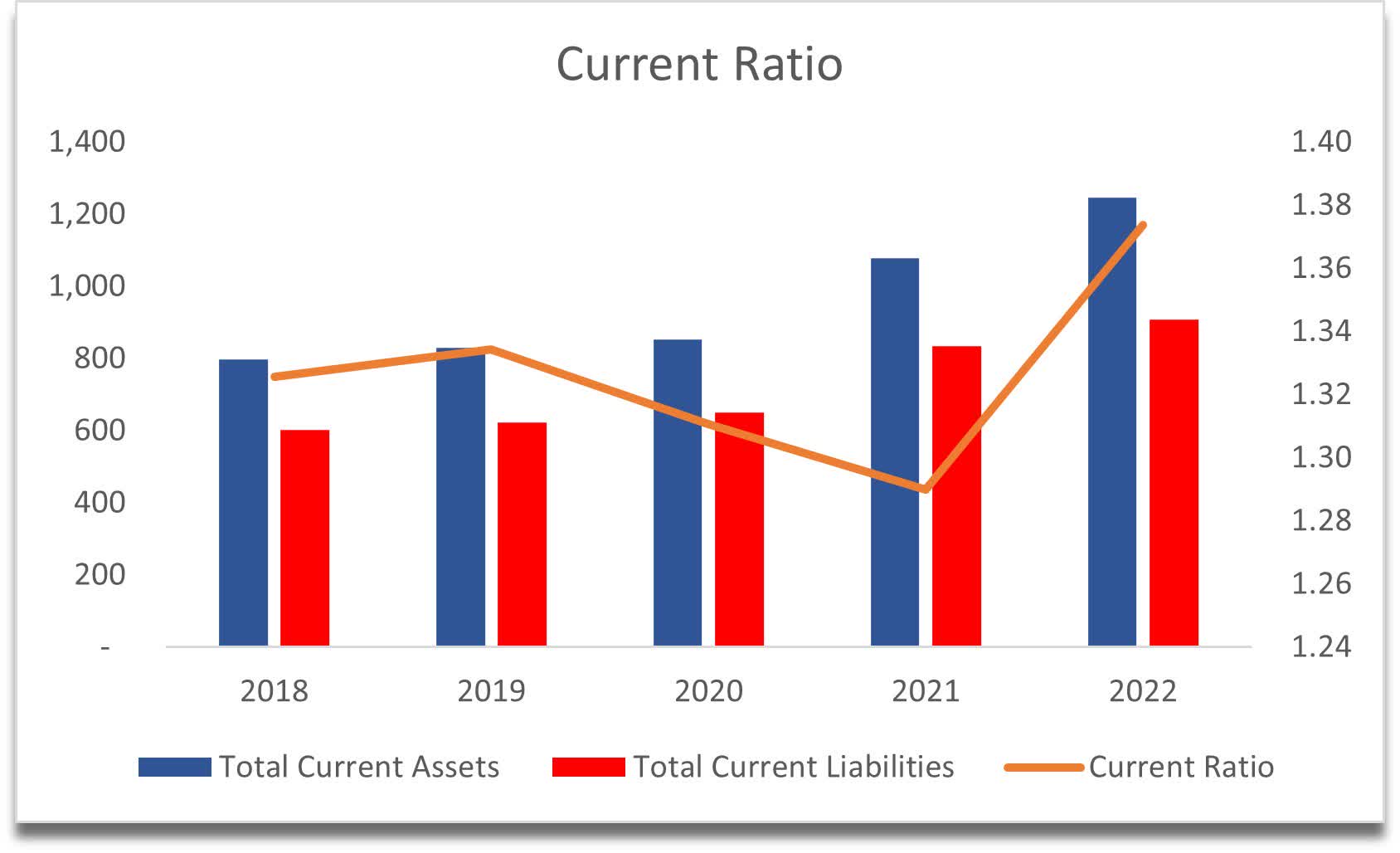

Speaking of liquidity, the current ratio of the company is acceptable. The company can cover its short-term obligations with ease and seems to be financially healthy and stable as the ratio hasn't changed much in at least 5 years. It looks like it had a slight improvement in '22. Hopefully, that trend continues or at least stabilizes at this level.

{kind=link}

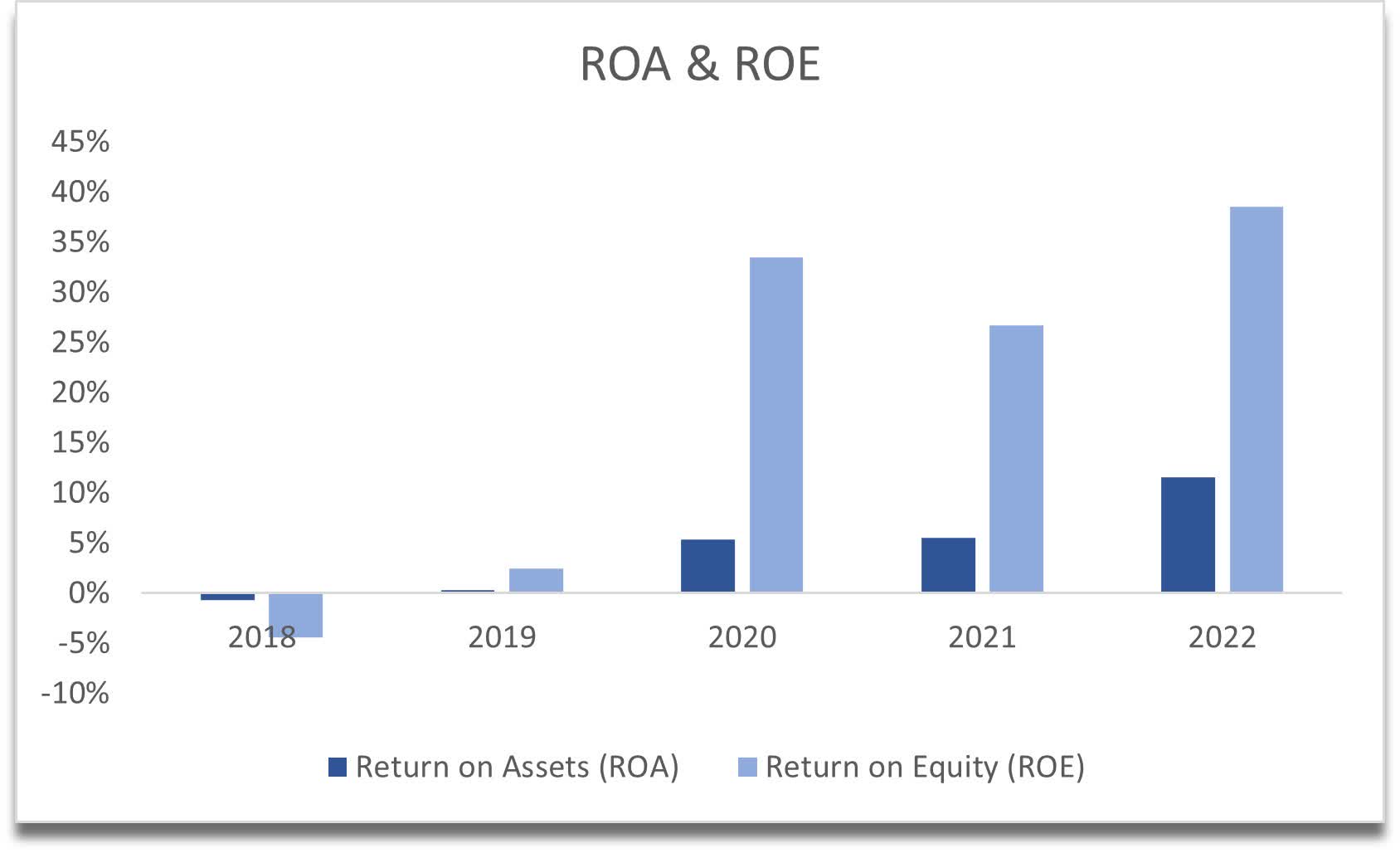

The next metrics show how much the company has improved over the last couple of years in terms of profitability and efficiency. The management has been able to invest capital into positive NPV projects since at least 2018 and the uptrend is clear. ROA and ROE metrics were negative in 2018 and since then exploded to the upside, especially during the lockdowns in 2020, where I imagine the management had to cut costs and other measures to improve profitability and efficiency. Let's hope that the company found a more efficient way of operating and that these elevated metrics are the new norm.

{kind=link}

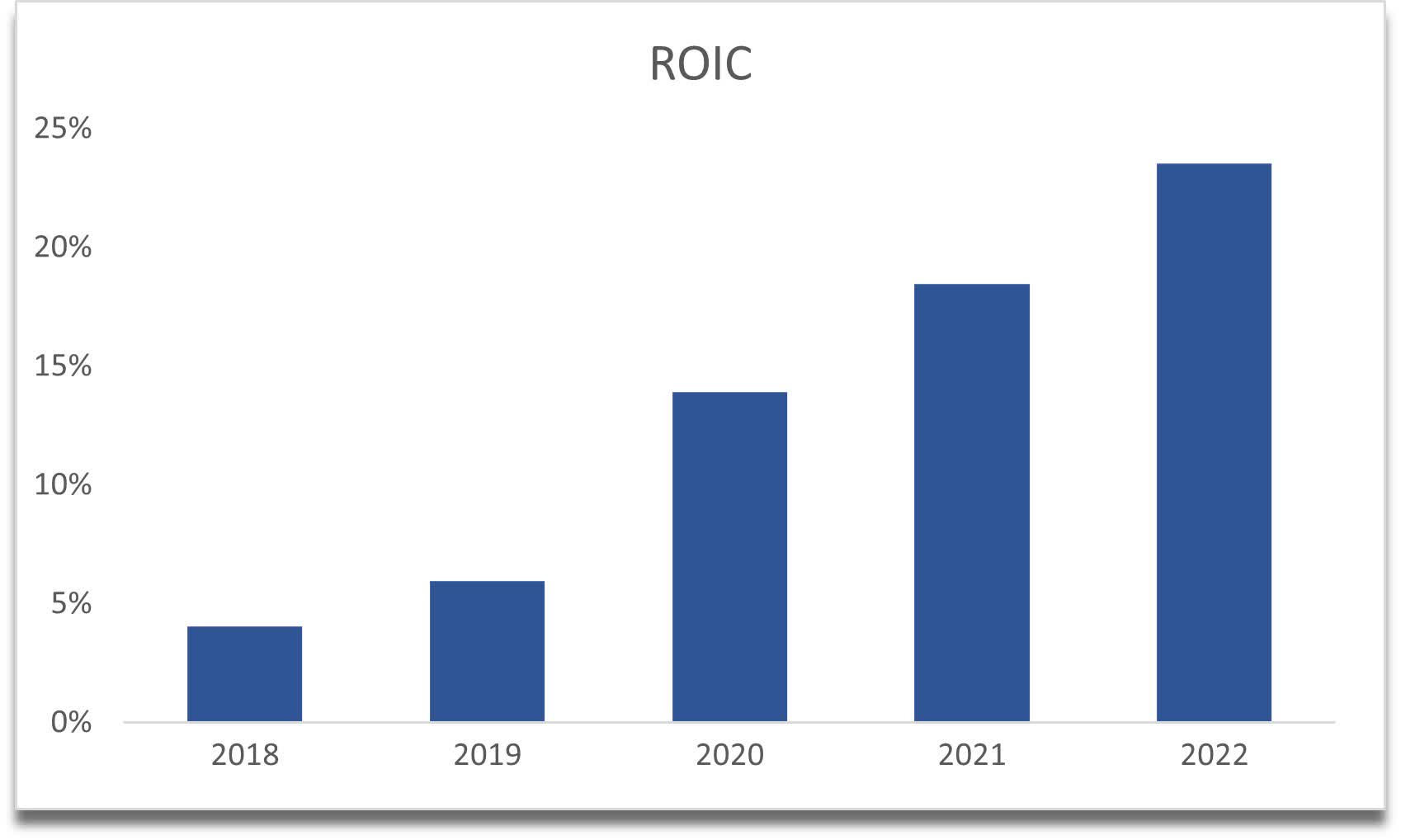

ROIC has been in an even better, more pronounced uptrend in the last 5 years. If the company manages to stay at these levels going forward, the company will reward its shareholders in the long run without a doubt.

{kind=link}

Overall, I don't see any potential red flags in how the company is being managed. We can see that the management has done a really good job of running the company since the pandemic hit and seems to have stayed at these new levels for the last two years. I just hope that this is the new norm and that we will not see profitability and efficiency come down. It is possible since we may see a recession in the next 12-24 months. That will be a good test for the management to prove to everyone that they are capable of running a business and I am looking forward to seeing what happens.

Valuation

Looking at the previous years, the company as I mentioned, has not seen negative revenue growth in the last decade. Even if we go back to 2006 through 2010, the company saw -a 1.4% decrease in revenues in 2009 during the financial crisis. For my DCF model, I took into consideration the looming uncertainties in the next couple of years, which I believe will not be as bad as '08 so I modeled the company is still going to eke out revenue growth. I will have three scenarios: a base case, a conservative case, and an optimistic case.

For the base case, I assumed the company will grow at 4% in '23 and will linearly grow down to 3% by '32. These estimates assume a slowdown in the economy keeping quite conservative throughout the model for an extra margin of safety. The company will see a growth of around 4% a year throughout the model. For the conservative case, I simply took away 2% from the base case and added 2% to the base case for the optimistic case.

The company has very tight margins, so it was interesting to see that they managed to improve on these margins quite a bit as I mentioned above. Changes in margins will play the biggest role in the company's valuation and not revenue growth.

For the base case, I speculate that the company will lose some gross margin due to the upcoming recession. The gross margins, I assume, will contract by around 100bps in '23 which will persist into '24 as well, however over time, I speculate that the company manages to become more efficient again, and by '32, gross margins improve by 200bps over time. The company saw over 300bps improvement in the last 5 years, so I think 200bps over a decade is conservative. Operating margins have improved quite a bit over the last 5 years also, however, I'd like to be more conservative and show no improvement in the operating margin with a slight decrease in efficiency of around 100bps for the next decade. Improvements in gross margins will primarily drive the other margins.

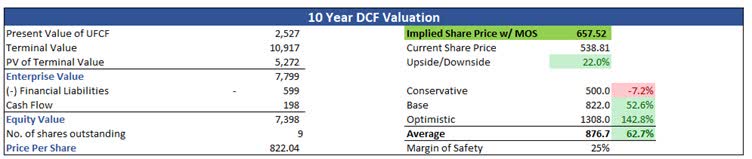

To be even more conservative I will add a 25% margin of safety on the intrinsic value calculation, and with that said, the implied intrinsic value of the company is $657.52 a share, showing around 20% upside from current valuations.

{kind=link}

Conclusion

I believe the company is a strong contender for a long-term investment. The estimates above suggest the company is undervalued even with what I believe are quite conservative assumptions. What worries me currently is the economic environment that we are in right now. In the short run, companies will get hammered once again if we see a slowdown in the economy. The share price will come down, no doubt about it. The question is, is the potential investor willing to start a small position now and weather the volatility, and average down if the stock price does come down, or is the investor not in a hurry and can wait a couple of months to see how it all plays out? I am not opposed to opening a small position as I believe, in the long run, there is a lot of upside for the company. The demand for the beverages is not going to go away anytime soon and with sugar-free alternatives taking over the world, the company is well-positioned to serve the healthy consumer.

With the mentioned dividend increase recently, the company is starting to reward dividend seekers, although the yield is nothing to write home about currently, the increase may signal the company is going to start to take dividends more seriously in the future.

Please take this analysis of the company as your first step of many to determine whether you want to own this company in your portfolio. Due diligence is key.

For further details see:

Coca-Cola Consolidated Inc.: A Strong Buy For Long-Term Investors