COKE - Coca-Cola Consolidated: Still A Solid Performer With A Bright Future

2023-12-08 14:40:37 ET

Summary

- Coca-Cola Consolidated has shown solid performance in terms of sales and improvements in margins, leading to an updated price target and a buy rating.

- The company has seen impressive margin expansion and a strong balance sheet, resulting in a 52% increase in stock price since March.

- Despite potential risks such as declining margins and regulatory scrutiny, the company is well-positioned for future growth and is trading at a 24% discount to its fair value.

Investment Thesis

I wanted to take a look at Coca-Cola Consolidated ( COKE ) and give an updated view of my price target since I covered the company for the first time in March of this year. A couple of quarterly reports came out which showed solid performance in terms of sales and improvements in margins, which warranted an update on my previous valuation. The company's financials are still very solid, coupled with decent growth in sales and continuing margin improvement, I updated my price target to reflect these improvements while maintaining a buy rating.

What has happened since the last coverage

My first article on the company was published in March of this year, in which I argued the company's impressive margin expansion over time and solid balance sheet makes it a great contender for a long-term investment. Even with conservative estimates on margins and sales, the company was trading at a deep discount to its fair value. The company has appreciated around 52% since the article was published while the S&P500 is up around 15% in the same period. So, you would have done well if you had bought it then, and if you did, congratulations!

COKE performance since March ´23 (Seeking Alpha)

So, I wanted to go through the company's prospects and update my analysis as we got a lot more information on the company's performance since then.

Briefly on the latest results

I will be covering the last consolidated 3 quarters of the year, in which COKE has seen an outstanding improvement in margins all across the board, especially in the first and second quarters of the year where gross margins improved 380bps, and 410bps, respectively while in the latest quarter, the company saw a more modest improvement of around 50bps. Nevertheless, still an improvement. In the last 3 quarters so far, gross margins have improved by over 270bps, while operating margins improved by 300bps. Top line growth saw 12%, 9%, and 5.1% increases in Q1, Q2, and Q3, respectively, while volume sold decreased 3.1%, 4%, and 1.4% in the same periods.

When I was covering the company the first time, I was already impressed with how it managed to improve efficiency over time and to be honest I didn't expect this to continue as we enter further into 2023, where inflation was rampant and interest rates continue to be hiked. Surprisingly, the company managed to go above and beyond in the last 3 quarters, while many companies saw profitability slump due to softer demand for the products and services because of tougher economic conditions.

Comments on the Outlook

I am very surprised to see that the company managed to pass on a lot of the increases in cost to the consumer, without losing much demand. This can be seen from the figures above where revenues increased by much more than the company lost in bottling volume. This may suggest that even as companies like Coca-Cola ( KO ) and Pepsi ( PEP ), raised the average prices of their products by 11% and 14% in '22 , respectively, and continue to raise prices by another 10% in '23 (that's from KO), customers are not very price-sensitive and are still buying their favorite beverage whenever they want. This is a great business to be in.

As inflation moderates and comes down, costs will follow, but will companies decrease their product pricing too? That remains to be seen. Coca-Cola has stopped increasing its prices but didn’t mention anything about starting to lower them.

This may be an oversimplification of why the volume decreased so little while sales improved. Another reason could be that COKE is offering different-sized packaging to appeal to different types of people, to maintain affordability for price-sensitive customers, which seems to be a very valid reason as COO David Katz said in the most recent press release:

“Our strategy of offering consumers a variety of packages at affordable prices across our portfolio is helping differentiate us in the marketplace and drive solid volume performance, particularly with our Sparkling beverages.” So, this certainly helped soften the blow to the total volume decline.

I don’t think the company is going to reduce costs. I think the management will take that extra cash and put it towards marketing and advertising of the product, and further growth initiatives. Furthermore, I wouldn’t be against some sort of reward to shareholders, like the company has recently offered a special dividend of $16 a share . Although, I would rather have the management reinvest in the company, if it cannot find any other growth opportunities, then so be it.

Risks

Margins may come down if the company decides to cut prices. That is a risk, however, I don’t think I can see this happening any time soon. Margins may decline from other reasons other than lowering of prices, for example, if general demand for the product softens for some reason.

If costs continue to rise and the companies try to pass it on to the disgruntled consumer, expect margins to decline as people stop buying the product because the prices are too high, which is unlikely, but still a possibility.

Beverages are constantly under the scrutiny of regulators. The most recent one I can think of is the whole aspartame debacle as a potential carcinogen. This hasn't changed anything regarding Coke's recipe, however, future incidents of other ingredients may cause concern and a dramatic shift will have to be made if the company continues to be successful. From these issues, there may come lawsuits that may damage the company's reputation.

Valuation

So, a lot has changed since March of this year, in terms of macroeconomic climate. The 10-year treasury yield stood at around 3.5% back at the end of March compared to 4.13%, and the difference was even worse just a couple of weeks ago when the yield was close to 5%. With all this new information, I had to update my valuation analysis accordingly.

The company managed to grow at a whopping 16% CAGR over the last decade. Nevertheless, I will approach the analysis with a conservative mindset for that extra margin of safety. Below are my updated assumptions for the base, conservative, and optimistic cases, and their respective CAGRs.

{kind=link}

For margins and EPS, I decided to use the same conservative approach and have margins stable over the next decade. I went with very slight improvements to reflect the better position the company is in, in the last 9 months of the year. I'm sure the company will be able to improve further, but also, I would like to stay less optimistic about that, to have a larger margin of safety in the end. Below are those assumptions.

{kind=link}

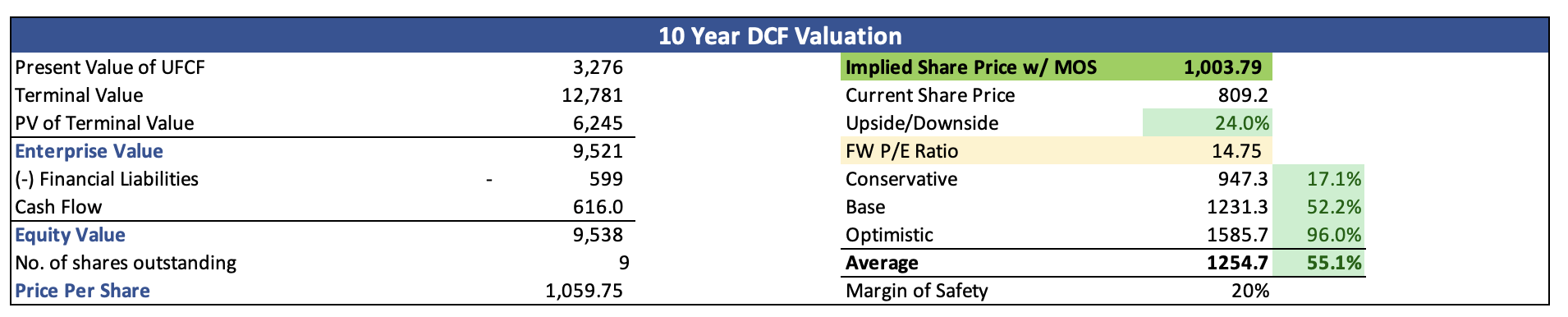

Furthermore, for my DCF analysis, I went with the company's WACC of 7.42% as my discount rate and 2.5% as my terminal growth rate. On top of these estimates, I decided to add a little extra margin of safety of 20%, just to be on the safe side. With that said, COKE's intrinsic value is $1003 a share, implying that the company is trading at a 24% discount to its fair value.

{kind=link}

Closing Comments

The outstanding improvements in margins and reasonable top-line growth made me reassess my price target. 9 months ago, I didn't have as much information as I do now, and that is a long time without revisiting the company. I believe that COKE still has a long way to go before it is considered overvalued. Therefore, I maintained my buy rating on the company and updated my PT to around $1,000 a share.

The margins may come down sometime in the future if it decides to lower prices once again, but I don’t see this as very likely. The customer is not very price-sensitive, however, there is still a limit to how far the customer can be pushed, so it is a good thing that many beverage companies have stopped the price hikes.

I believe the company is in a great position to perform well going forward, and the share price will continue to go up accordingly.

The price may be a little too expensive for the individual investor, but if you can afford it, I don’t think you'll regret holding it over the next few years. Who knows, maybe at some point the company will announce a stock split, but I wouldn't hold my breath since the company hasn't done one since 1984 according to Seeking Alpha.

For further details see:

Coca-Cola Consolidated: Still A Solid Performer With A Bright Future