MNST - Coca-Cola Europacific Partners: Beverage Winner With Consistent Cash Flows

2023-07-08 06:49:28 ET

Summary

- Coca-Cola Europacific Partners is expected to continue its growth trajectory due to strong performance in key brands and has scope for margin improvements.

- CCEP has successfully navigated health and sustainability trends by reducing sugar content and focusing on environmental responsibilities.

- The company is currently trading at a fair valuation, with potential for further M&A and diversification beyond Coca-Cola, making it an attractive investment opportunity.

Investment thesis

Our current investment thesis is:

- Growth is strong and where possible, has been supplemented with M&A. As long as brands such as Coca-Cola and Monster remain strong, which we suspect, CCEP will continue on its current growth trajectory.

- Margins are sticky but we see scope for some improvement as inflationary pressures ease and synergy benefits are realized.

- Commercial development continues to be strong, as CCEP reduces sugar in its products and focuses on the sustainability of its production process.

Company description

Coca-Cola Europacific Partners PLC (CCEP) is engaged in the production, distribution, and sale of a wide range of non-alcoholic ready-to-drink beverages. Their product portfolio includes flavors, mixers, energy drinks, soft drinks, waters, isotonic drinks, ready-to-drink tea and coffee, juices, and other beverages.

The company offers various popular brands such as Coca-Cola, Diet Coke, Coca-Cola Zero Sugar, Fanta, Sprite, and Monster Energy, among many others.

Share price

CCEP's share price has had a mild decade but when considered alongside dividends, returns have been strong. The company has provided investors with consistently strong cash returns, generating over 200%.

This is a reflection of the resilience of the brands the company bottles, the primary of is Coca-Cola. Continued growth and strength in the brand have supported its European performance.

Financial analysis

{kind=link}

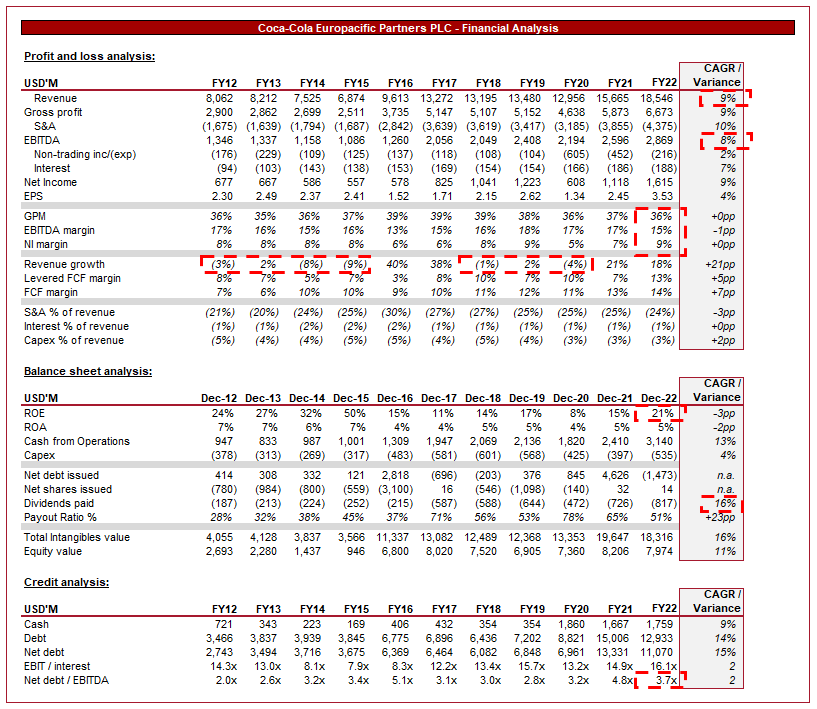

Presented above is CCEP's financial performance for the last decade.

Revenue

Revenue has grown at an impressive 9% rate annually, reflecting continued strong growth in CCEP's key brands. This does somewhat mask a period of soft growth between FY12-FY15, and FY18-FY20. The large uptick in FY16 and FY20 is due to the acquisition of smaller Coca-Cola bottlers across Europe and the Asia Pacific , contributing to CCEP becoming one of the largest Coca-Cola bottlers.

Despite the name, Coca-Cola only represents 58.5% of the company's 2022 volume. With a diversified range of beverages across the subcategories. This gives the company the benefit of diversification and reduced reliance on any single brand.

Volume (CCEP)

Volume growth remains strong across brands, with FME and Hydration performing particularly well. This is driven by the strong performance of Monster Energy ( MNST ) in recent years, as well as changes in consumer behaviors (explored later).

Vol growth (CCEP)

Further, the company is highly diversified by region, partially due to the acquisitions in recent years. No single region represents more than 18% of revenue, with the UK business remaining the largest segment. This allows CCEP to maximize its benefit from European growth in its brands, which for the most part are global. Also, the scope for margin improvement through synergistic benefits from production facilities is high.

Regions (CCEP)

Competitive Landscape

CCEP has developed its competitive position through the acquisition of its competitors. This is the only possible way in such an industry as each country has a monopoly supplier. For this reason, the scope for development is through expansion into new regions. CCEP's competition is thus other large bottlers, with the nearest geographical one being Coca-Cola HBC AG, which serves Eastern Europe. CCHBC is listed in the UK and represents a potential acquisition target.

Key trends

Health and Wellness

We have seen growing consumer demand for healthier beverage options, including low-sugar, natural, and functional beverages. This is driven by a greater understanding of diets and a healthy lifestyle, as well as social signaling. This has forced Coca-Cola ( KO ), and others, to develop healthier options, as well as acquire brands in this segment.

We have seen a clear reduction in average sugar per liter toward current targets, with volume growth remaining strong. This reflects consumer happiness with the product despite this, reducing any concerns around flavor.

Sugar (CCEP)

Sustainability and Environmental Responsibility

In recent years, we have seen an increased focus on sustainability and environmental responsibility across the beverage industry. This is part of the wider target of nations to reduce their environmental impact by reducing Co2 emissions.

CCEP is committed to sustainable packaging, water stewardship, and carbon emissions reduction, achieving impressive progress toward key targets. This is part of the wider Coca-Cola requirements. Impressively, this has come without a material cost to margins.

Sustainability (CCEP)

Margin

CCEP's margins are strong, with an EBITDA-M of 15% and a NIM of 9%.

Margins have been relatively sticky across the historical period, reflecting the strong value proposition from the brands it bottles, allowing the business to maintain its target margins. Further, its monopolistic position in key geographies supports this.

The company has faced some inflationary pressure due to the increased cost of glass bottles, partially offsetting recent development.

We see scope for improvement in the coming years, as the recent acquisition yields further synergy gains and inflationary pressures subside. The company has peaked at an EBITDA-M of 18%, which looks achievable. This could translate to a double-digit NIM.

Balance Sheet

CCEP operates with a large amount of debt, primarily due to leases for production locations (Change in accounting standards to bring leases on balance sheet). With a strong interest coverage, we are not concerned from a solvency perspective.

CCEP generates a substantial amount of cash. It had a $3.1m CFO in FY22. Its Capex commitments are a c.30% of this, leaving a large amount of cash available for distributions.

In recent years this has been accumulated, which could be used for future transactions or to enhance distributions in the coming years following a period of deleveraging.

Outlook

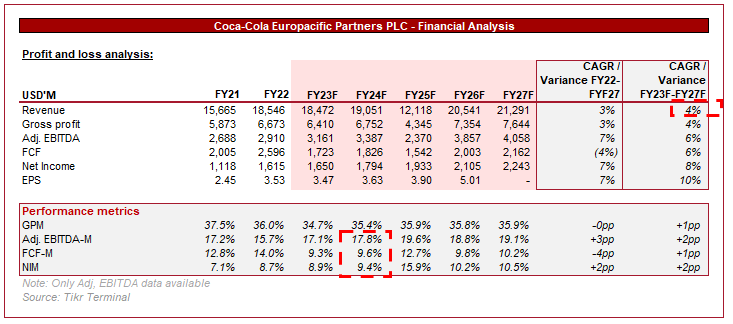

{kind=link}

Presented above is Wall Street's consensus view on the coming 5 years.

Analysts are forecasting a growth rate of 4% in the coming 5 years, representing a healthy level in our view. Given the maturing of the industry, a good organic rate would be 3-5%.

Further, margin improvement is forecast, with gains in the coming years representing improved efficiency and reduced inflationary pressures.

Valuation

CCEP valuation (Capital IQ)

CCEP is currently trading at 11.8x NTM EBITDA and 16.4x NTM earnings.

This valuation is in line with its 10-year historical average, implying the company has not materially developed during the period. This is a harsh assessment in our view, as we see the following as value drivers above and beyond the last 10-year average:

- Acquisition of the Pacific business representing another region to grow.

- Margin improvement at a larger scale.

- Continued strong demand for current brands, as well as newer brands (such as Monster) outperforming.

- Sustainability and healthy consumption developments have not negatively impacted the business, reflecting the navigation of a potential headwind.

Final thoughts

CCEP is a highly attractive business. The company operates a monopolist position in Western Europe, allowing it to benefit from the growth of global brands while maintaining sticky margins.

We expect growth to continue in the coming years and believe margin improvement is also possible. It is possible that further M&A is possible, as well as diversification beyond Coca-Cola.

With a defensible yield that could increase, as well as the factors stated above, we initiate at a buy.

For further details see:

Coca-Cola Europacific Partners: Beverage Winner With Consistent Cash Flows