PANL - Coffee Holding: Reverse Merger Partner Delta Finally Provides Some Eagerly-Awaited Financial Information

2023-04-18 06:05:21 ET

Summary

- Reverse merger partner Delta Corp ("Delta") finally provides some eagerly-awaited financial information but numbers appear to be hand-picked and lack important details.

- Delta has also filed a confidential draft registration statement on form F-4 with the SEC.

- Delta's implied equity value of $625 million continues to look wildly exaggerated, particularly when compared to closest U.S. exchange-listed peer Pangaea Logistics Solutions.

- Even at the current share price, early investors in Delta might actually be happy sellers upon closing of the transaction.

- Given the ongoing issues surrunding the proposed reverse merger transaction, I would advise investors to avoid Coffee Holding's common shares or even consider selling existing position.

Note: I have covered Coffee Holding ( JVA ) previously, so investors should view this as an update to my earlier articles on the company.

Six months ago, Coffee Holding, a small company specializing in the highly competitive coffee roasting, packaging and distribution business surprised market participants by announcing a reverse merger transaction with Delta Corp Holdings Limited ("Delta") which brands itself a "fully-integrated one-stop logistics provider":

{kind=link}

Company Presentation

On Monday, Coffee Holding provided additional information regarding the proposed business combination in an investor presentation .

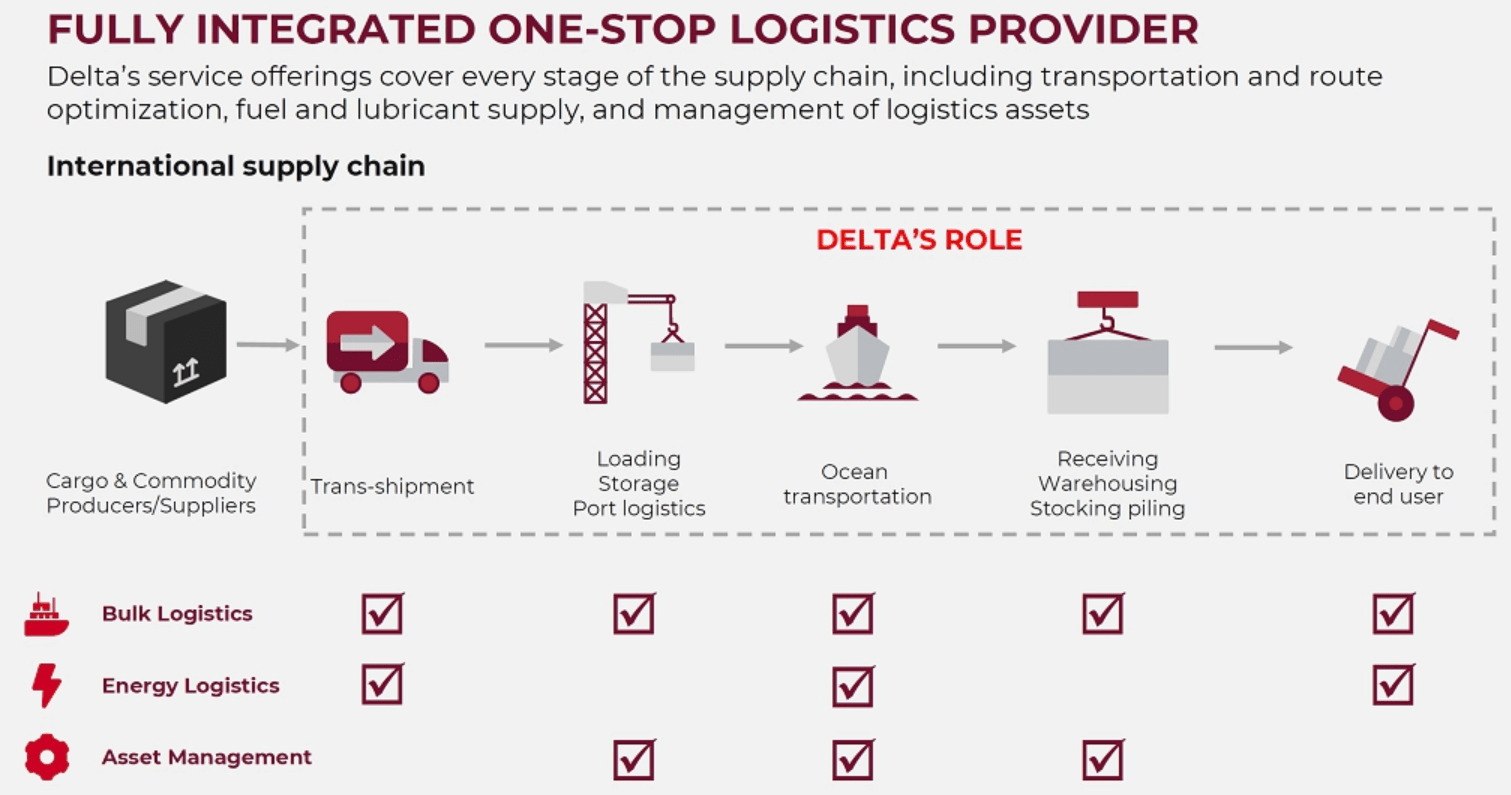

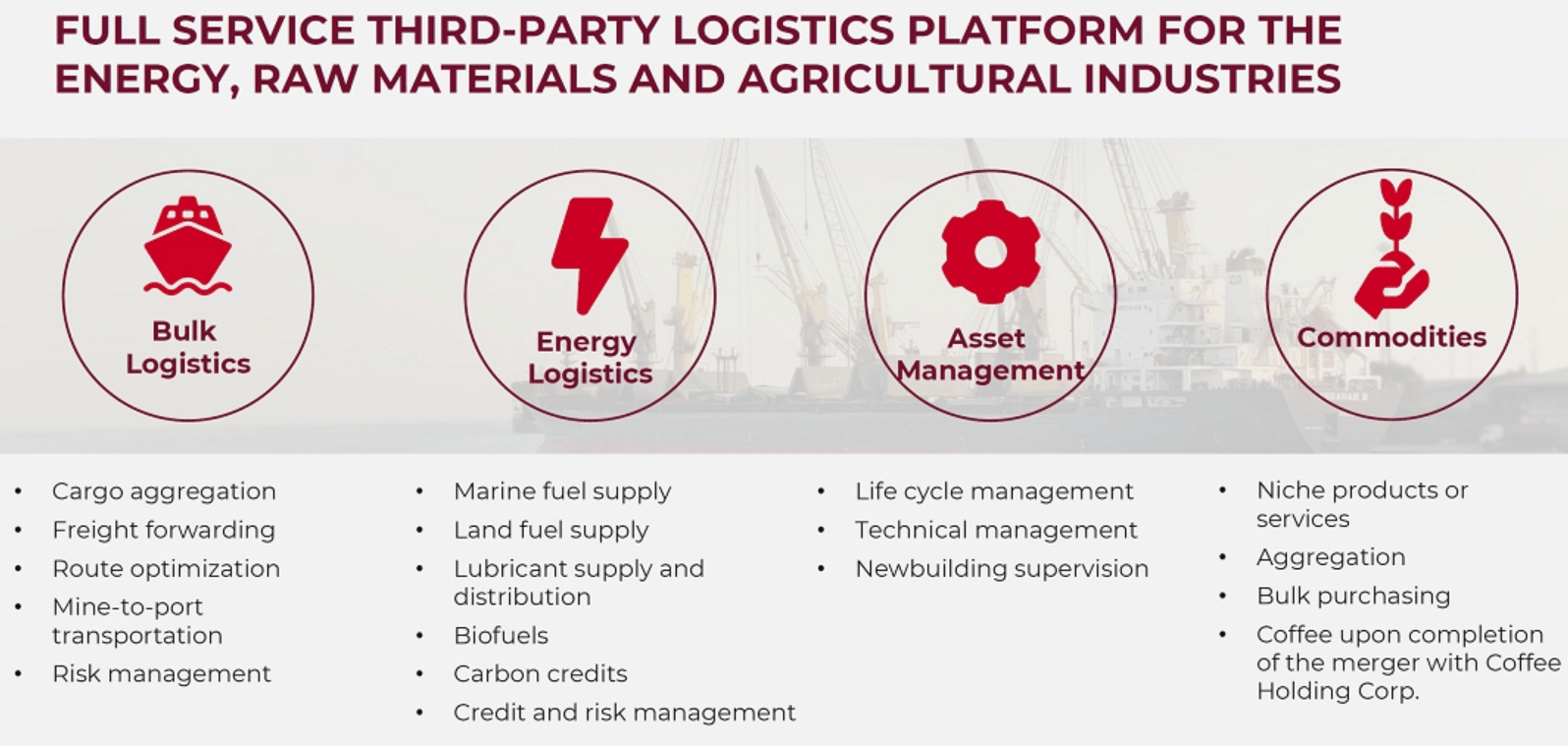

Delta operates in four main segments, Bulk Logistics, Energy Logistics, Asset Management and Commodities with the vast majority of revenues apparently generated by the company's bulk shipping and energy logistics operations.

{kind=link}

Company Presentation

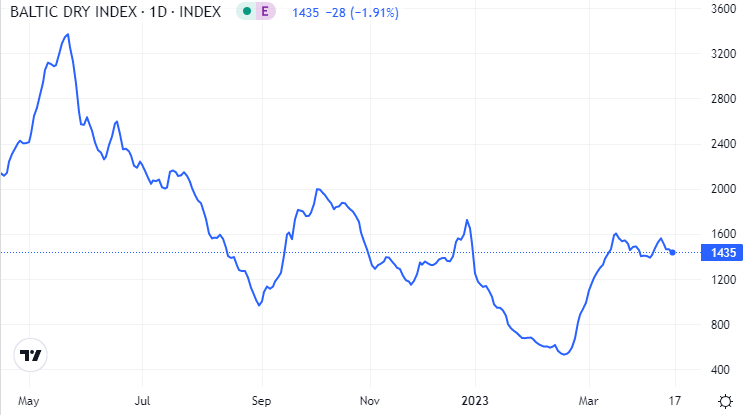

Unfortunately, the financial information provided in the presentation is solely based on Delta's FY2021 and H1/2022 results and conveniently does not include the second half of last year which saw a dramatic decline in dry bulk charter rates:

{kind=link}

TradingEconomics.com

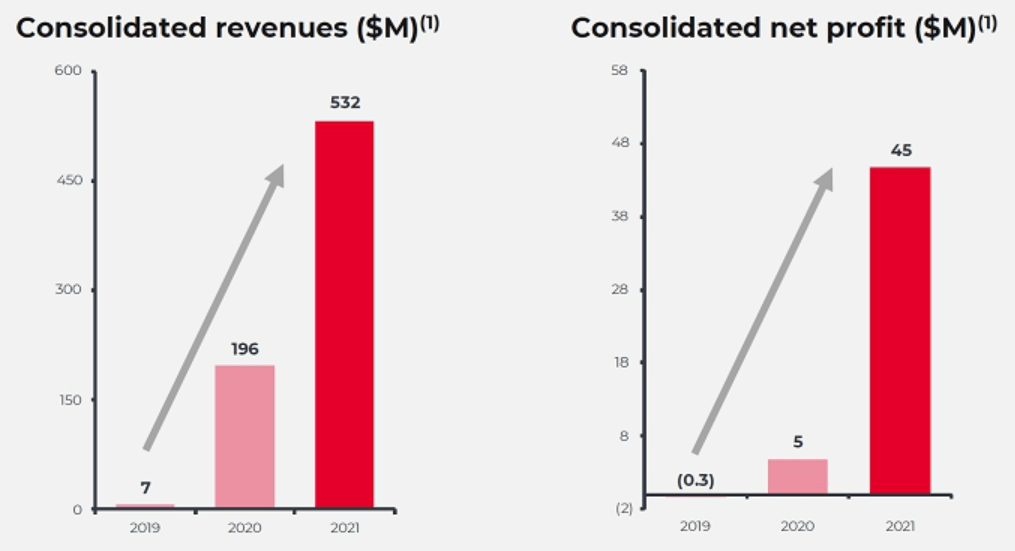

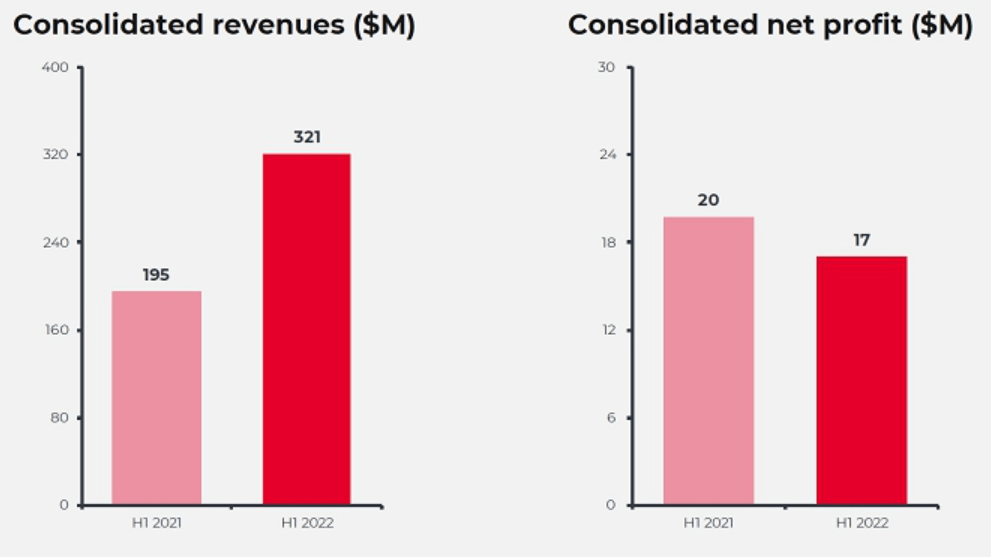

In 2021, results benefited from the strongest dry bulk charter market environment in more than a decade with revenues soaring by 170% year-over-year and net profit increasing ninefold to $45 million.

{kind=link}

Company Presentation

In the first half of 2022, dry bulk charter rates were still decent thus resulting in a 65% year-over-year revenue increase but compared with the second half of 2021, revenues were actually down somewhat.

{kind=link}

Company Presentation

In addition, increased costs of goods sold resulted in reported gross margin being cut in half from 2021 levels:

Company Presentation

Given the weak dry bulk charter market in the second half of last year, it is fair to assume Delta's H2/2022 results having been nowhere near the company's first half performance and likely a far cry from 2021 levels.

Investors should note that the company already knows about its H2/2022 performance but decided to exclude this information from Monday's presentation. In addition, no cash flow statements have been provided.

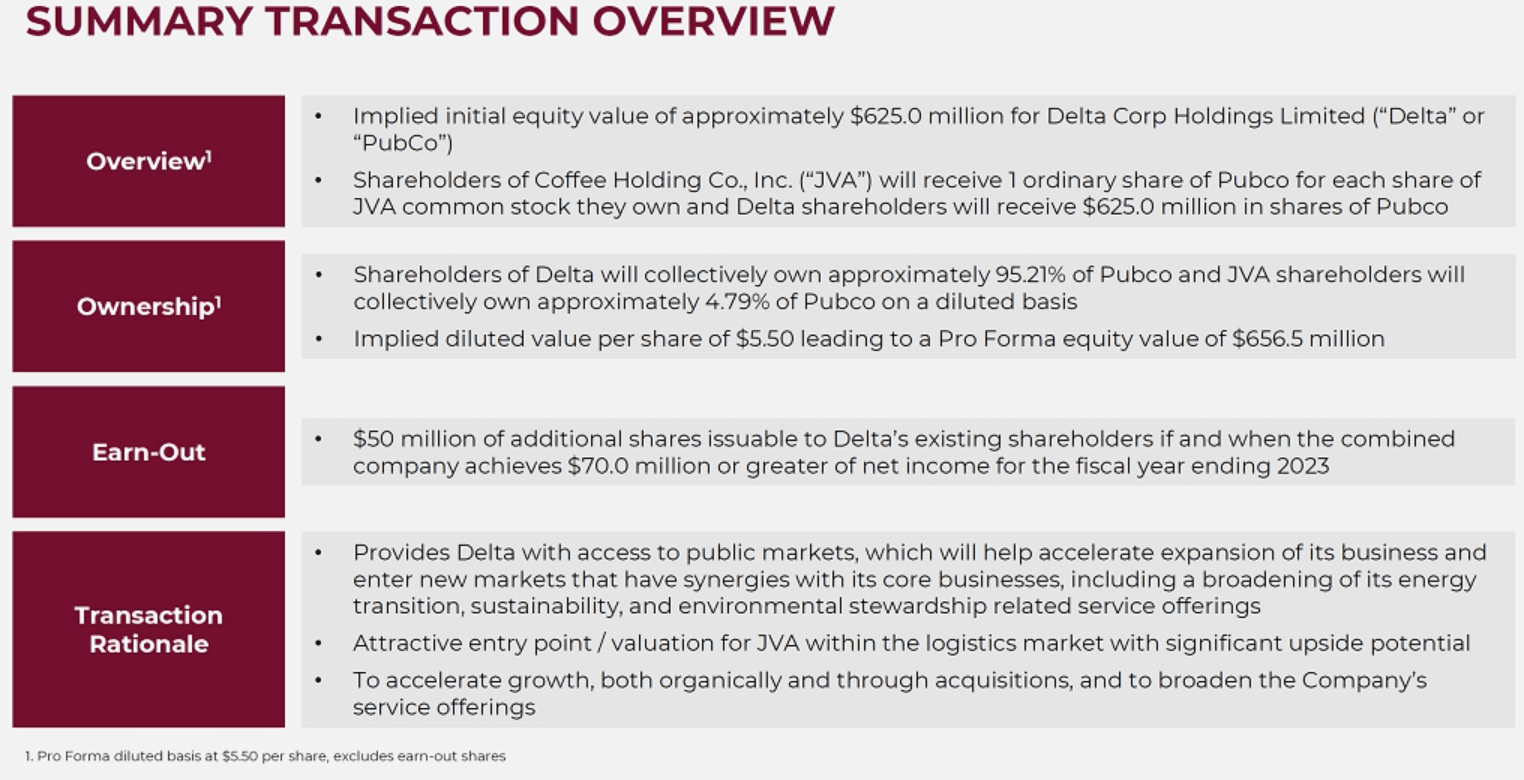

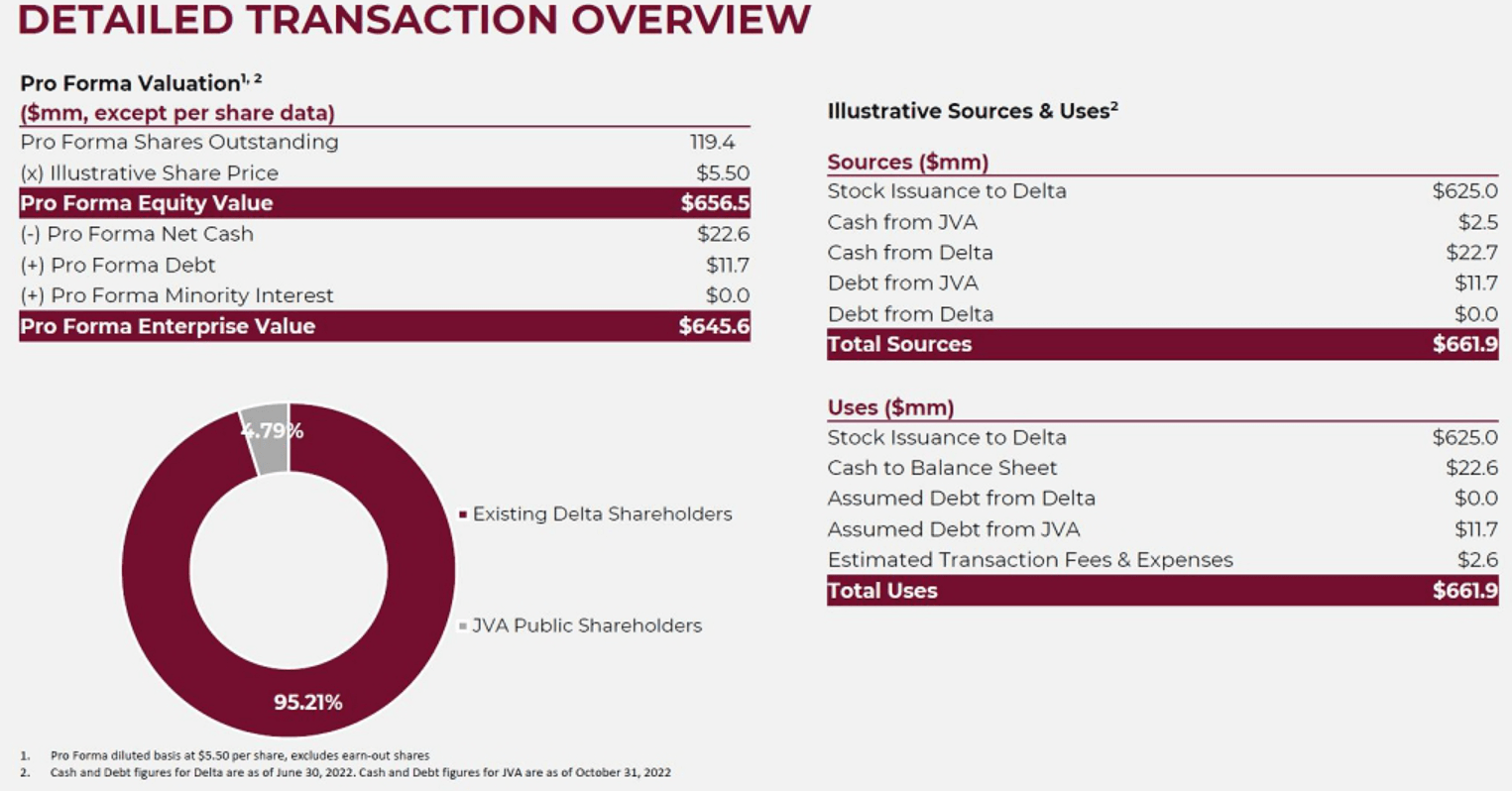

The presentation also included a comprehensive transaction overview with current Coffee Holding equity holders expected to own below 5% of the combined company:

{kind=link}

Company Presentation

Following the close of the transaction, 119.4 million shares are expected to be outstanding. Please note that legacy Delta shareholders will be entitled to $50 million of additional shares in case the combined company achieves net income of at least $70 million this year which based on current dry bulk charter and forward freight agreement ("FFA") rates appears unlikely at this point.

{kind=link}

Company Presentation

Quite frankly, even after taking a closer look at the provided financials, I have no idea how Delta managed to negotiate a transaction based on an implied equity value of $625 million for its operations.

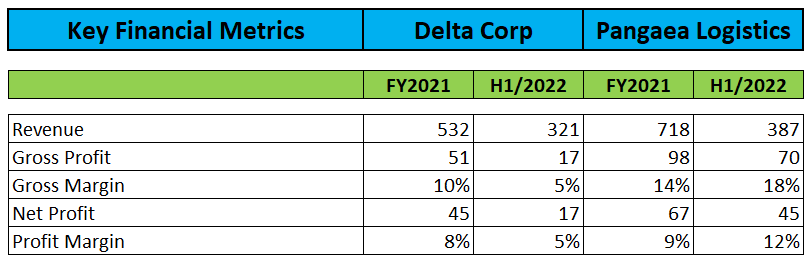

With the company lacking hard assets and considering the volatility of the shipping markets, Delta's valuation looks mind-boggling, particularly with closest U.S. exchange-traded peer Pangaea Logistics Solutions ( PANL ) or "Pangaea" trading at a large discount despite also owning 24 dry bulk carriers. After deducting related debt, these vessels represent a net asset value of more than $100 million. In addition, Pangaea carries almost $130 million in cash on its balance sheet and pays a quarterly dividend of $0.10 per share.

Nevertheless, Pangaea's enterprise value remains well below $500 million, a sizeable discount to Delta's valuation despite Pangea apparently being the superior choice from basically all aspects of the business:

{kind=link}

Delta Corp Presentation / Pangaea Logistics Press Releases

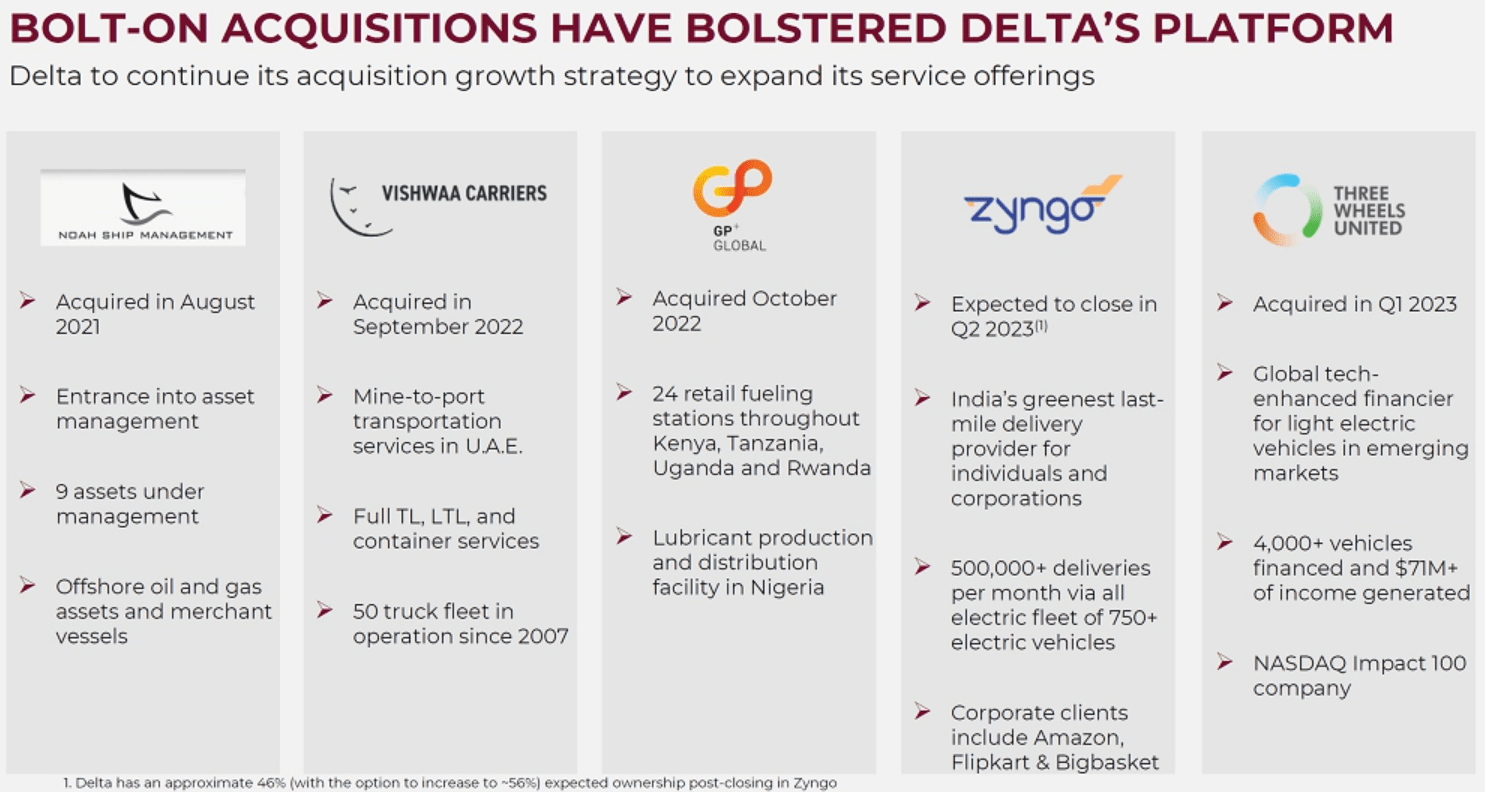

Delta also highlighted its recent acquisition spree including two venture capital-style investments in India's last mile delivery industry:

{kind=link}

Company Presentation

While investments in delivery platform Zyngo and related Fintech Three Wheels United appear to have been limited so far, these start-ups will likely require further capital injections to deliver on their growth ambitions. Please note also the misleading claim of " 71M+ of income generated " in the slide above related to Three Wheels United as this number does not refer to the company but rather to its customers:

ETAuto.com

Bottom Line

Finally, Coffee Holding's reverse merger partner provided some eagerly-awaited insights into its business but numbers appear to have been hand-picked and do not provide a complete picture. On Monday, Delta also filed a confidential draft registration statement on form F-4 with the SEC.

While I have no doubt about Delta being a perfectly legal and viable entity, the valuation assigned to the business in the proposed reverse merger transaction doesn't make any sense to me, particularly when looking at closest U.S. exchange-listed competitor Pangaea Logistics Solutions which appears to be a vastly superior investment based on a comparison of key financial metrics.

As evidenced by the trading price of Coffee Holding's common shares, market participants remain skeptical, too but even at the currently implied market capitalization of $235 million, early investors in Delta might actually be happy sellers once the transaction has closed.

In any way, Delta's desire to become a publicly-traded entity doesn't bode well for existing Coffee Holding shareholders as the combined company is either looking to raise capital or provide early investors the possibility to exit their holdings or even both.

Lastly, I wouldn't be surprised to see senior officers Andrew and David Gordon buying back the operations of Coffee Holding from Delta in the not-too-distant future thus increasing their stake in the company founded by their father and grandfather to 100% while getting rid of the expenses and disclosure requirements associated with a publicly-listed company.

After all, Delta is mainly interested in Coffee Holding's Nasdaq listing.

Given the issues discussed above, investors should continue to avoid Coffee Holding's common shares or even consider selling existing positions.

For further details see:

Coffee Holding: Reverse Merger Partner Delta Finally Provides Some Eagerly-Awaited Financial Information