SJM - Coffee Wars In Recession: Starbucks Vs. The J. M. Smucker

2023-06-06 02:08:52 ET

Summary

- Starbucks' non-franchise model may be limiting its value, but the company is hesitant to change due to potential harm to the brand.

- J.M. Smucker Company's Folgers coffee brand is a strong competitor and substitute, accounting for 31% of the company's sales and 43% of their profit.

- The potential recession and student loan repayments may impact consumer choices between Starbucks and more affordable coffee options like Folgers.

I always wanted to like Starbucks

Starbucks Corporation ( SBUX ) is a stock that I always wanted to like. The non-Franchise model which would seem to be such an obvious value unlocking was never pursued. Unlike McDonald's Corporation ( MCD ), this seems to be part of the reason the top line never dropped to the bottom in the same way. The argument that the Franchise model would be injurious to the Starbucks brand may be valid. So if they never want to go that route, do I want to be involved?

On the flip side of the coffee coin, we have The J. M. Smucker Company ( SJM ). The owner of the Folgers coffee brand, this product sits on the shelves of many an American household. Yes, this is just one part of the J. M. Smucker brand, but also one that accounts for 31% of the company's sales and 43% of its profit.

The narrative in the pipeline is there's a recession on the loose in the future. Youngsters will have to start repaying those student loans they forgot about. Will they be able to afford that triple macchiato soy double whipped latte? Or will they stock the shelves with Grandma and Grandpa's red can of yore? You know, the best part of waking up might be Folgers in your cup. At least until your student loans are paid off. Let's square these two coffee centric companies off.

The charts

Starbucks wins round one, the momentum wars. Regardless of what investors assume is coming down the pipe, Starbucks invariably has the more attractive market reputation and obvious coffee play.

Income versus revenue

While J. M. Smucker Company has been increasing revenue at a much lower clip, its net income has remained better intact from a standard deviation consideration. The greater thesis of this comparison is not to pit a little guy against a pure coffee play juggernaut, the point is to observe which direction the coffee market is going as belts tighten. Both are experiencing pinches in their profit margins due to inflation, however, once inflation subsides, a tough economic situation can remain.

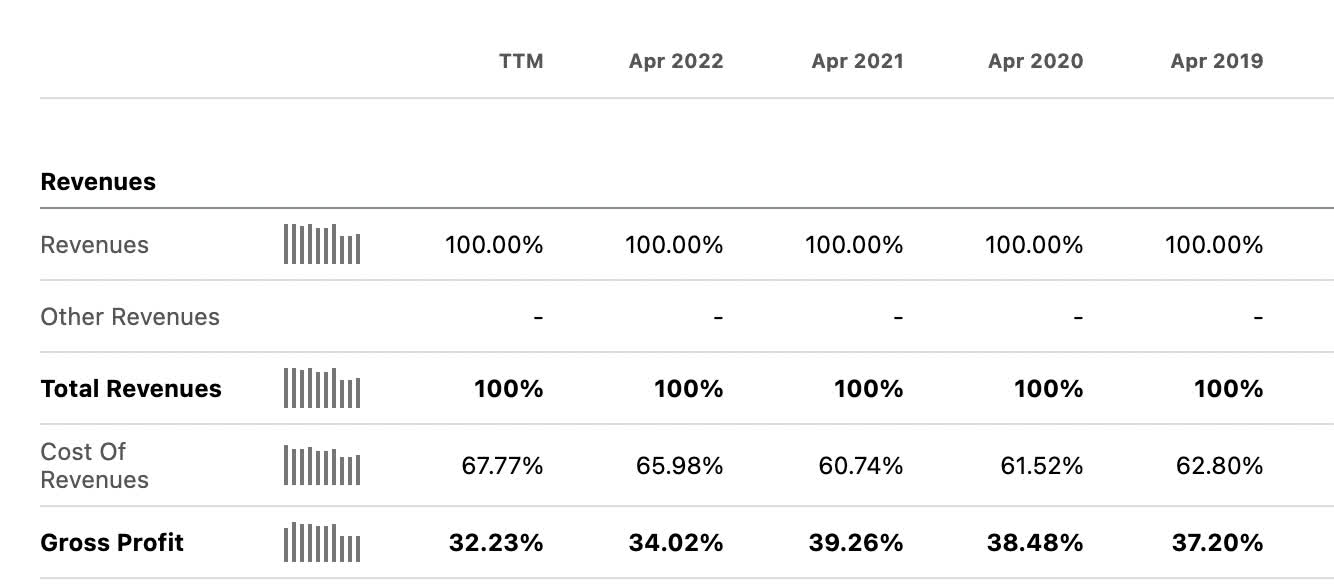

In light of prices of everyday consumer staples being more sticky than the underlying commodities themselves, let's see how the cost of goods sold situation is working out for both of them.

Starbucks:

{kind=link}

J. M. Smucker Co:

{kind=link}

As an observation of cost controls, we can see that J. M. Smucker Co. has a lower cost of goods sold and a higher gross profit margin. To be fair, J. M. Smucker is not 100% in coffee, so the commodities mix spread across the various businesses is quite different. However, I see this as a hedge against coffee consumption and prices period. Having the PB&J and dog food businesses that come along with J. M. Smucker is a hedge against coffee prices in general. J. M. Smucker sells Folgers and other coffee brands which are an inferior good and a direct substitute for Starbucks' products.

When inflation subsides, I expect J. M. Smucker's margins to grow while Starbucks may recede. The price of a can of Folgers is already palatable. The price of a Starbucks latte may need to come down to meet demand.

Business segments

From the Starbucks 10-K :

Starbucks is the premier roaster, marketer and retailer of specialty coffee in the world, operating in 83 markets. Formed in 1985, Starbucks Corporation’s common stock trades on the Nasdaq Global Select Market (“Nasdaq”) under the symbol “SBUX.” We purchase and roast high-quality coffees that we sell, along with handcrafted coffee, tea and other beverages and a variety of high-quality food items through company-operated stores. We also sell a variety of coffee and tea products and license our trademarks through other channels, such as licensed stores as well as grocery and foodservice through our Global Coffee Alliance with Nestlé S.A. (“Nestlé”). In addition to our flagship Starbucks Coffee brand, we sell goods and services under the following brands: Teavana , Seattle’s Best Coffee , Ethos , Starbucks Reserve and Princi .

From the J. M. Smucker Co. 10-K :

We have three reportable segments: U.S. Retail Pet Foods, U.S. Retail Coffee, and U.S. Retail Consumer Foods. The U.S. retail market segments in total comprised 87 percent of 2022 consolidated net sales and represent a major portion of our strategic focus – the sale of branded food and beverage products with leadership positions to consumers through retail outlets in North America. International and Away From Home represents sales outside of the U.S. retail market segments. For additional information on our reportable segments, see Note 4: Reportable Segments.

{kind=link}

Business growth

These are two companies that have two different growth trajectories. One is primarily customer-facing in Starbucks and the other is a grocery store consumer staple. As for Starbucks' growth expansion, China is the largest and most rapid segment of investment:

The International segment is a significant profit center driving our global returns, along with our North America segment. In particular, our China MBU contributes meaningfully to both consolidated and International net revenues and operating income. China is currently our fastest growing market, our second largest market overall and 100% company-owned. Due to the significance of our China market for our profit and growth, we are exposed to risks in China.

Let's put aside any political tensions in China for the moment. Are we all optimistic that the consumer demand for expensive coffee will persist in China? Student debt is not as big of an issue as it is here, but mortgage debt may be even worse. Chinese mortgages have to be paid back and can not be bankrupted. If you default, the bank not only takes your home but also gets a judgment against you for the difference between the sale value and the deficiency. Until that is paid, you can not buy a plane ticket or a train ticket. The results of default are Draconian.

Why I bring that up is that well-documented pay cuts are happening all over China at this very moment. The majority of young adult individuals in China have to purchase a home to be wed, this is a social norm and requirement of most parents. Therefore, the number of renters as a percentage is low in China when compared to the US. I believe the pay cuts combined with the capital retention to pay the mortgage will begin to hit many consumer discretionary products in China. Those without a mortgage in China, aged 50-80, are primarily tea drinkers from my experience and knowledge of the country. They buy local brands of amazing Chinese teas, not Starbucks tea bags.

The US student debt issue domestically will hit Starbucks come September by my estimation. This is when the Federal Student loans that have been in deferment from the Covid era will kick back into gear.

The Fiscal Responsibility Act of 2023, also known as the debt ceiling deal, requires the U.S. Department of Education to restart student loan repayment on federal student loans in September 2023. Yes, repayment is really going to restart in September. For real. Seriously! You can count on it happening. No kidding!

The hunt for a good, cheap solution to the morning coffee fix will ensue.

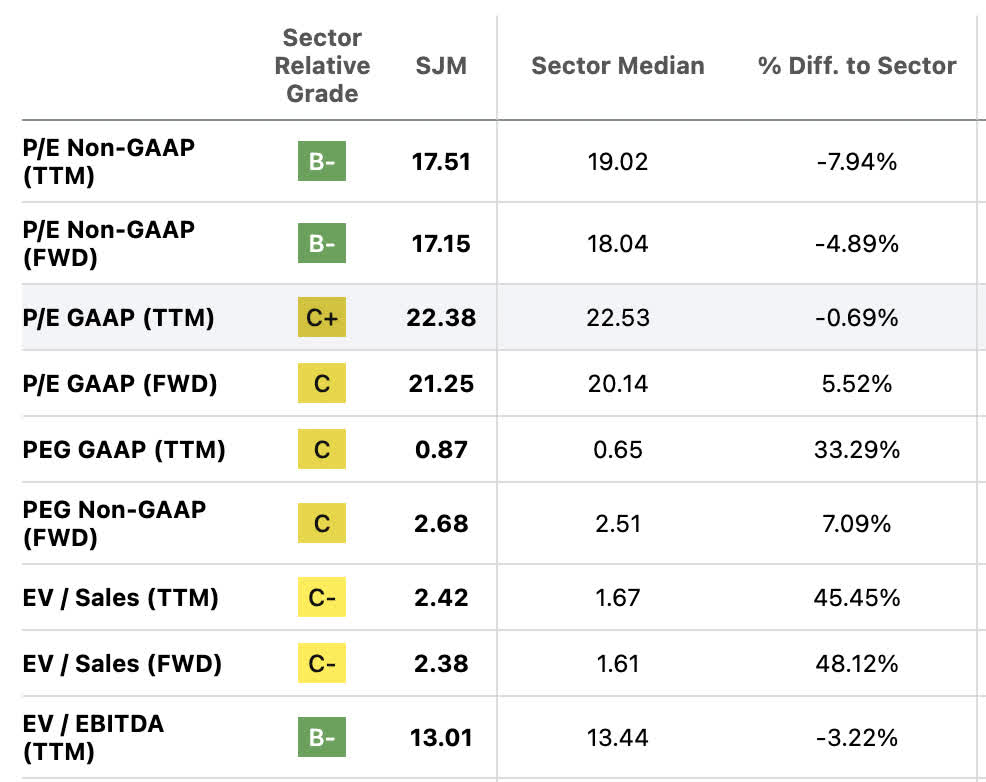

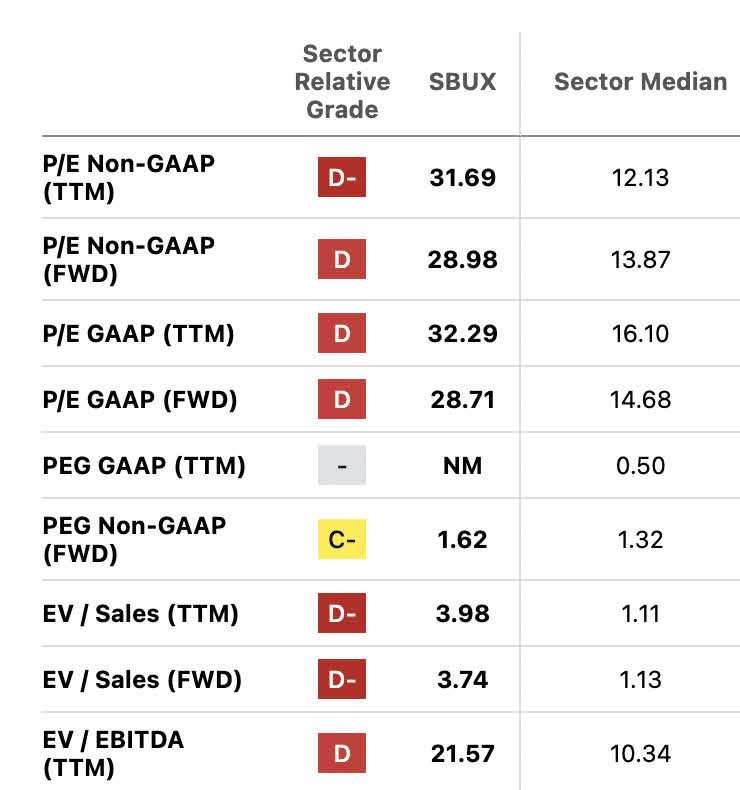

Valuation models

Neither are exhibiting big trailing income growth or cheap asset valuations, lets take a look at the overall ratios:

J. M. Smucker Co.

{kind=link}

Starbucks

{kind=link}

Starbucks looks to be the more expensive valuation with better forward-looking GAAP Peg. Neither is cheap based on assets. I'll take a look at the stabilized owner earnings models for both and draw up a GAAP PEG value for Starbucks based on next year's earnings growth assumptions since they seem to have an advantage there in analysts' eyes.

Owner earnings Starbucks:

- TTM's Net income of $3.554 Billion

- Plus Depreciation and Amortization of $1.461 Billion

- Minus $1.971 Billion CAPEX

- Equals owner earnings of $3.044 Billion

- Discounted at a 10-year treasury rate of 3.69% = $82.493 Billion fair market cap.

- Divided by 1.147 Billion shares outstanding = $71.92 a share

FWD PEG Starbucks:

{kind=link}

With forward EPS estimated at $4.1 a share and full 2023 estimated at $3.43, that would give us a yoy earnings growth rate of 19.53%, some very nice estimated growth. Using 19.53 as the multiplier and $4.1 as the multiplicand would lead us to a fair value based on FWD PEG of $80 where the PEG ratio would equal 1.

J. M. Smucker :

Owner earnings:

- TTM's net income is USD 711 million

- Plus Depreciation and Amortization of USD 452 million

- Minus CAPEX of USD 505 million

- Equals owner earnings of USD 658 million

- Discounted at a 10-year treasury rate of 3.69% = $17.831 Billion fair market cap.

- Divided by 106 million shares outstanding= $168 a share.

Balance sheet trends

Shares outstanding have remained rather flat for J. M. Smucker while Starbucks had bought back 20% of shares since 2016, or 3.8% per year on average. Certainly advantage Starbucks here. If they bought back another 3.8% next year that should put us at 1.103 Billion shares outstanding, improving the fair value per share to $74.78 based on discounted owner earnings.

Current assets vs LT debt

Both companies have similar LT debt to current asset trends. Starbucks' current assets are equivalent to 46% of LT debt and J. M. Smucker is equivalent to 44% on the same token. This seems to be an industry norm for companies involved in similar commodities.

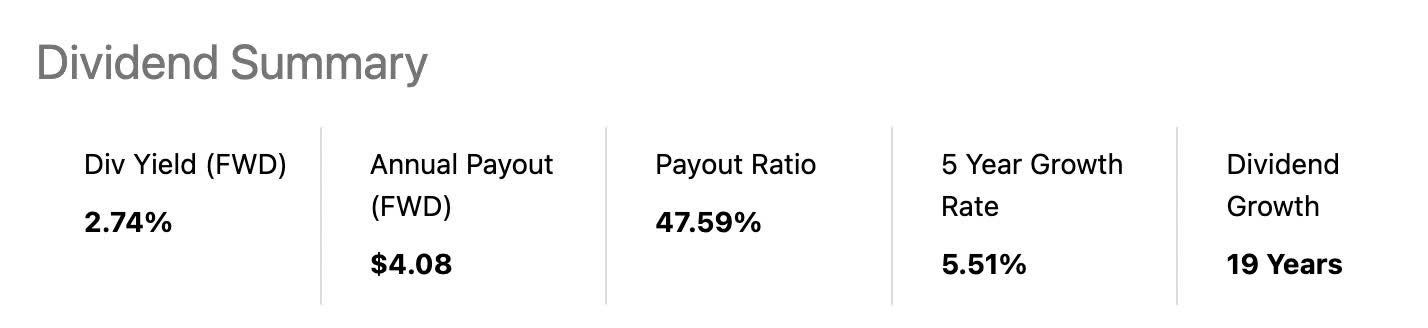

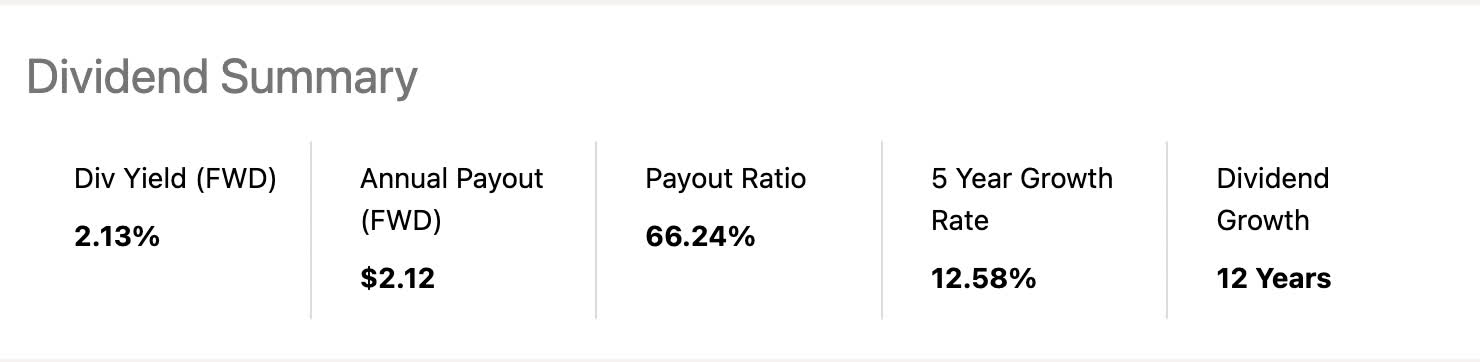

The dividend and free cash flow

Both of these pay dividends, let's take a look at the trends and payout ratios:

J. M. Smucker Co.:

{kind=link}

Starbucks:

{kind=link}

Analysis

Both pay nice 2+% dividends with growth for over a decade. Coverage on earnings appears better for J. M. Smucker. Let's take a coverage versus free cash flow:

- Starbucks FCF/share $2.4

- FWD Dividend $2.12

- Ratio 88.3%

- J. M. Smucker Co. FCF/share $6.00

- FWD Dividend $4.08

- Payout Ratio 68%

As we can see, based on the current free cash flow per share, J. M. Smucker has a higher margin of safety on the dividend as well with a lower payout ratio of free cash flow. Longer growth and less exposure to China are positives for me.

Catalysts

Starbucks would be in a more advantageous position than J. M. Smucker Co. should we see a lack of a recession and lowering interest rates worldwide which could take pressure off consumer debt of all categories. I don't see that happening.

J. M. Smucker Co. should see better numbers and margins with a worsening consumer situation which forces consumers into lower priced substitutes such as Folgers coffee versus Starbucks. My positive catalyst arrow is pointing toward J. M. Smucker's direction.

Conclusion

I'm taking a position in J. M. Smucker Co. The dividend coverage is there with a nice payout. With about a third of the business in cheaper coffee substitutes, they should absorb some of Starbucks' business should the consumer situation worse amongst the younger demographics. Not only that, but Folgers has a market with more older consumers than the likes of Starbucks.

My growth thesis on J. M. Smucker Co. is centered squarely around the coffee business growing. It is also cheaper on a discounter owner earnings model. Starbucks is about 33% overvalued if I blend the PEG and owner earnings model to get to a pt of $77. I'm buying J. M. Smucker over Starbucks as the winner of my coffee battle.

For further details see:

Coffee Wars In Recession: Starbucks Vs. The J. M. Smucker