RCI.B:CC - Cogeco Communications: An Undervalued Infrastructure Stock Offering A Growing Yield

2023-07-24 14:00:12 ET

Summary

- Cogeco Communications, a cable company operating in North America, seems a worthy income investment due to its stable business profile, growth prospects, and high starting dividend yield.

- Despite facing competition from fiber networks and fixed wireless internet services, Cogeco has maintained strong returns on capital and margins, and has increased its dividend for 17 consecutive years.

- The company is also exploring new business opportunities, including a mobile virtual network operator business in Canada and the acquisition of Canadian internet reseller Oxio, to offset the decline of legacy businesses.

Cogeco Communications ( CCA:CA ) is a cable company providing internet, phone and video services in North America. For an investor Cogeco is an infrastructure company with stable business profile, modest growth prospects and high starting dividend yield.

Cogeco's stock is one of the lowest valued stocks among its peers but has similar or higher returns on capital and better margins. Cogeco has increased its dividend rapidly for 17 years in a row. The dividend yield seems very attractive, and it's well covered by the earnings. I think the combination of business quality and growth prospects, discounted valuation and dividend profile, make Cogeco a worthy income investment.

Company overview

Cogeco Communications operates both in Canada and the U.S. The annual revenue of $2.9 billion is evenly derived from the two countries. The company serves 1.6 million residential and business customers. In the U.S. Cogeco operates in 13 states under a new Breezeline brand and in Canada the main brand is Cogeco. In 2022 the company had 4700 employees.

The ownership structure of Cogeco Communications is somewhat special. Cogeco Inc (CGO:CA) owns 35.3% of the equity but majority of the voting rights. Cogeco Inc. is controlled by the Audet family. Another large shareholder is Rogers, its Canadian rival, which owns a substantial amount of shares in both Cogeco companies.

The regional internet service markets have usually been a battle of 2-3 players. However, there's a significant risk of competition intensifying. Or at least that's what I think investors might be concerned about. Cable companies face competition from fiber networks, which is potentially a technically better solution. Another considerable threat is the fixed wireless internet services promoted heavily for example by T-Mobile ( TMUS ).

Short term these risks are likely overrated in my opinion, but fixed wireless could hurt the finances of cable companies. Competition, rising interest rates and fixed income investments becoming again an alternative to infrastructure stocks, have been some of the reasons for falling share prices among the companies offering broadband services.

Share price performance of Cogeco and its peers. (YCharts)

Balancing between growth and debt

Decent growth prospects

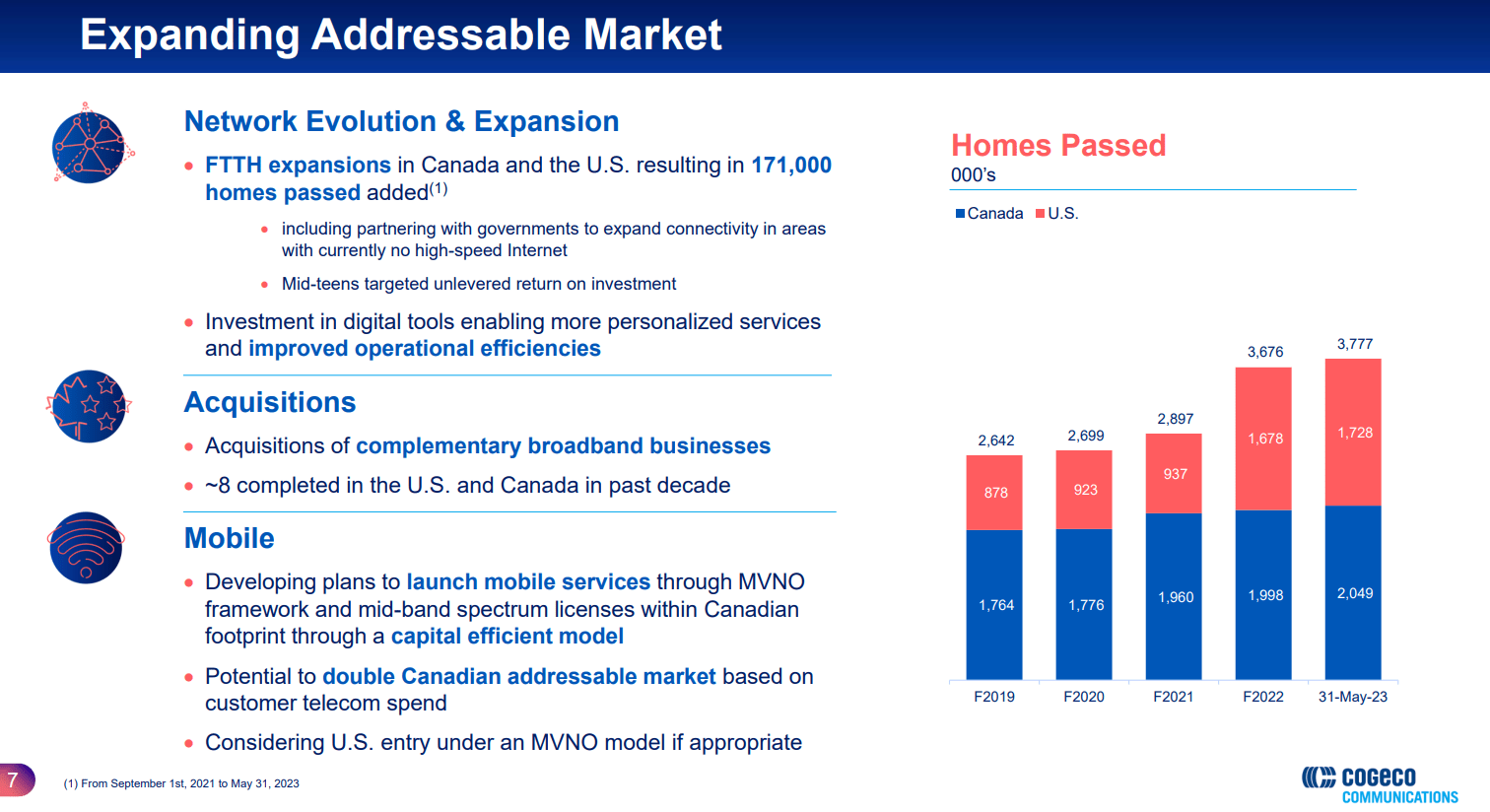

In addition to the internet, Cogeco provides phone and video services. Customers are increasingly subscribing only to internet services, which puts the other two services into a structural decline. This is presumably an important reason why Cogeco is continuously expanding its network to new homes and seeks new business opportunities. The downside of the expansion is reduced free cash flow, which is required to overcome the decline of the legacy businesses.

Cogeco is investing to grow number of homes passed. (Company presentation)

{kind=link}

Cogeco is in the midst of negotiations to commence a mobile virtual network operator (MVNO) business in Canada. This means that Cogeco would be offering cellular plans to its customers, but rely on someone else's infrastructure to deliver the service. The MVNO operations could potentially commence by the end of 2023. Presumably, Cogeco aims to increase its ARPU and wants to remain relevant to its customers who increasingly cancel their landline phone services. MVNO operations could support Cogeco to maintain its excellent historical growth rates.

Historical growth rates of Cogeco. (Seeking Alpha)

In February 2023 Cogeco acquired a Canadian internet reseller Oxio, which aims to renew the way how internet services are sold and provided. For Cogeco, Oxio will be the second brand under which it provides broadband services. At the time of acquisition Oxio served 48 000 customers. Oxio is in a growth phase and the management doesn't expect it to contribute to the company's earnings in the near future.

Cogeco is not just an acquirer. It's also a potential acquisition target itself. However, in the current market and interest environment, this scenario seems unlikely to unfold. According to Tikr, Rogers Communications owns 37% of the Cogeco Communication shares. In 2020 Rogers attempted to acquire Cogeco for $150 per share. Currently, Rogers' net debt to EBITDA stands at a whopping 5.7x, so the company intends to pay down the debt, but not sell its assets.

Debt position is increasing but manageable

Infrastructure stocks could be poor investments in the times of high inflation and interest rates. High inflation makes new investments more costly and weakens returns on capital if the pricing won't grow in line with the costs. As it is also the case with Cogeco, infrastructure companies are typically levered. For the trailing 12 months the interest expenses are over $100 million higher than they were in 2021.

Cogeco's debt position grew sharply due to the acquisition of WideOpenWest's broadband assets in Ohio in 2021. Cogeco paid a rather high multiple for the assets in my opinion, approximately 11x on enterprise value to adjusted EBITDA basis. Currently, Cogeco is trading at a multiple of 5.7x. To finance the acquisition the company took on $900 million of debt. Unfortunately the American business has faced some headwinds due to competition and rebranding of the U.S. operations from Atlantic Broadband to Breezeline. The headwinds and the high multiple paid on the acquisition, could be a drag on Cogeco's share.

Cogeco's long term debt and debt to equity ratio. (YCharts)

At the end of the fiscal 2022 the net debt to adjusted EBITDA ratio stood at 3.2x compared to 2.5x the year before. The adjusted EBITDA covered financial expenses 7.4 times. 72% of the debt is fixed-rate. Cogeco's debt position is much more modest than many of its peers, whose debt ratios are often twice as high.

Performing well against the peers

Measured by return on assets, Cogeco performs well compared to its peers. The differences are small, but the purpose of the comparison is to showcase that the reason behind the lower valuation of Cogeco can't be an inferior business. BCE ( BCE ) which is more of a wireless operator comes closest to Cogeco. The difference to other broadband operators is more substantial.

ROA of Cogeco and peers. (YCharts)

Furthermore, measured by ROCE, Cogeco performs in line with its peers. Its ROCE comes very close to Charter Communications ( CHTR ) and the rest are performing worse than Cogeco.

ROCE of Cogeco and its peers. (YCharts)

When looking at EBIT and EBITDA margins Cogeco performs the best among the same peer group. Excluding the period around 2017, the margins have been steady and increasing which reflects the nature of the business.

Margins of Cogeco and peers. (YCharts)

The stock appears undervalued

Like the shares of other cable companies, Cogeco shares have fallen deep since hitting its all-time high of $122 two years ago. The increasing debt has resulted in the enterprise value holding its level compared to the market capitalization.

Market cap and enterprise value development. (YCharts)

Nonetheless, Cogeco shares seem valued at a substantial discount to its historical averages. Forward-looking EV/EBITDA stands currently at 5.7x against a 5-year average of 6.6x and EV/EBIT is 10.7x against 12.1x. Last 12 months EV/S stands at 2.7x compared to an average of 3.3x. The discount to historical averages could be justified by the increased required rate of returns, but points out that the shares are not richly valued against the past.

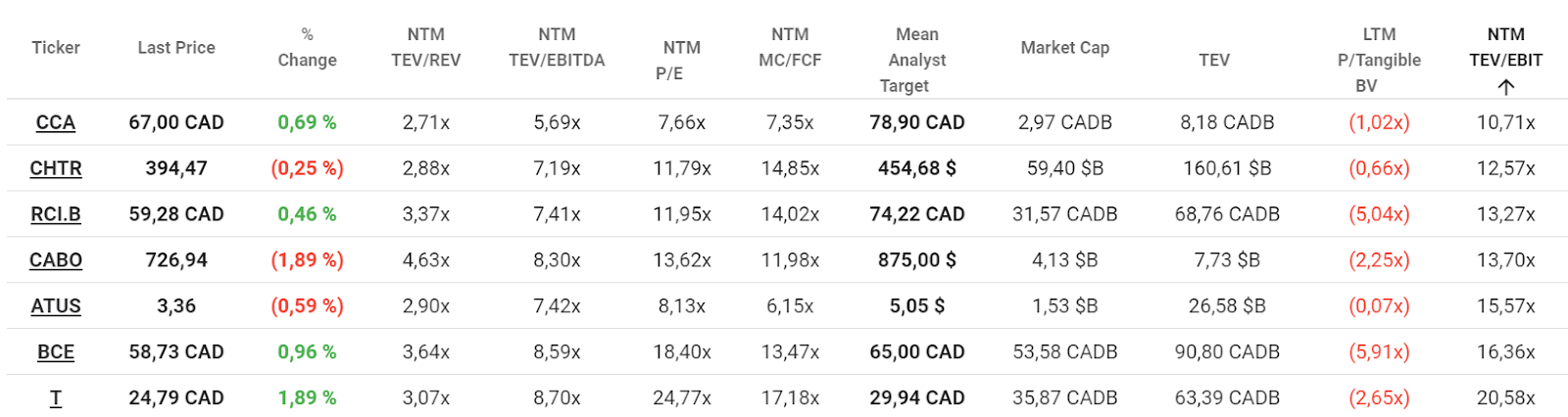

Compared to a group of peers, Cogeco's shares are the cheapest by nearly every measure. Only Altice is cheaper on a P/FCF basis, but it carries a lot more debt and doesn't pay a dividend. The average multiples of the peer group are significantly above Cogeco's multiples.

The average forward looking P/E is 13.8x, P/FCF 12.1x and EV/EBITDA 7.6x. As we saw in the section above, Cogeco performs well in terms of returns on capital and margins against its peers, which doesn't seem to justify the discount.

Valuation of Cogeco and its peers. (Tikr)

{kind=link}

Based on earnings Cogeco appears undervalued. If we take the estimated EPS of $8.9 for 2023, apply 5% growth rate for the first five years and 3% for the following years and expect the dividend to grow along with the earnings, the fair value would be $74.4. The calculation assumes the P/E-multiple to reverse closer to its 5-year mean of 12.3x. If the multiple would remain around 8x, the fair value would be approximately $64.

Considering the nature of the business, historical growth rates, indebtedness, margins, and returns on capital, I think a P/E-multiple of 10x is rather conservative.

Fair value calculation based on earnings. (Author)

There are ten analysts following the company with an average target price of $79, but ranging from the lowest of $60 to the highest of $105.

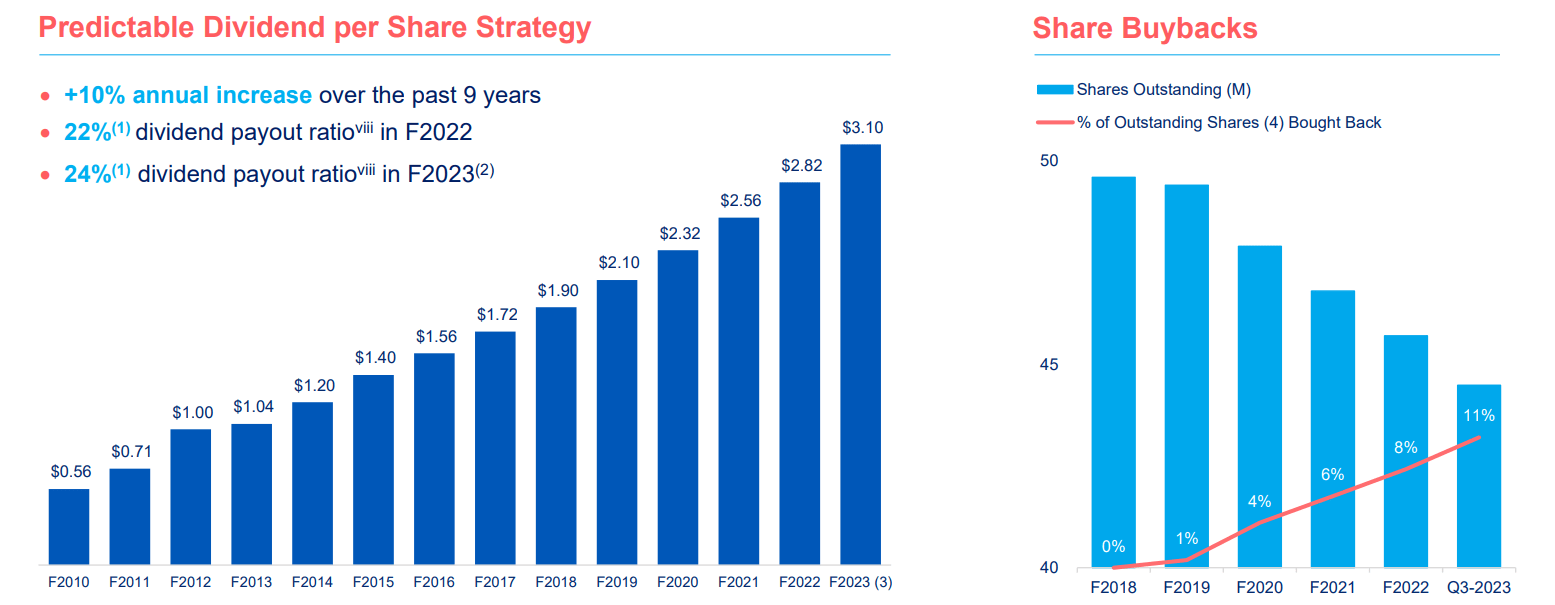

A high, safe, and growing dividend

According to Seeking Alpha, Cogeco has increased its dividend for 17 years in a row. The forward annual payout stands at $3.1 translating to a dividend yield of 4.6% and a payout ratio of 31%. The five-year dividend growth rate sits at 10.3%.

Dividend history and buybacks. (Company presentation)

{kind=link}

As mentioned above, the large shareholder, Rogers, could be in need for cash in order to reduce its indebtedness. Potentially, Cogeco could also buy all or some of its own shares from Rogers and reduce the share count substantially. Before that could happen, Cogeco probably would need to get its own indebtedness to a slightly lower level first. Such an event could be a boost for shareholder yield, which together with dividends and buybacks has historically reached an excellent level.

Conclusion

Fears of increasing competition, high capital expenditures consuming the cash flows and increasing interest expenses are some of the reasons that have driven the cable equities down. Cogeco is clearly one of the best companies in the group of broadband companies, and it's trading at an attractive valuation. Together with an excellent, safe, and growing dividend, Cogeco appears an attractive income investment with upside potential.

For further details see:

Cogeco Communications: An Undervalued Infrastructure Stock Offering A Growing Yield