CGNX - Cognex: Waiting For An Entry Point

2023-10-20 11:39:51 ET

Summary

- Cognex's stock has crumbled under the pressure of a high valuation and weak end-market demand.

- While demand is likely to remain soft in the near term, Cognex has a strong competitive position in a secular growth market.

- From a valuation perspective, Cognex is beginning to look attractive, but there is risk of further downside.

Cognex's ( CGNX ) stock has been in free fall over the past three months as the reality of a high valuation and weak end market demand has sunk in. For long-term investors, the stock price is already beginning to look attractive, but there may be little support in the near term. End market demand is likely to remain soft, particularly if economic conditions weaken, and deleveraging and salesforce expansion will weigh on Cognex's margins. Investors should not lose sight of the fact that Cognex still has a strong business in a secular growth industry, though.

Market

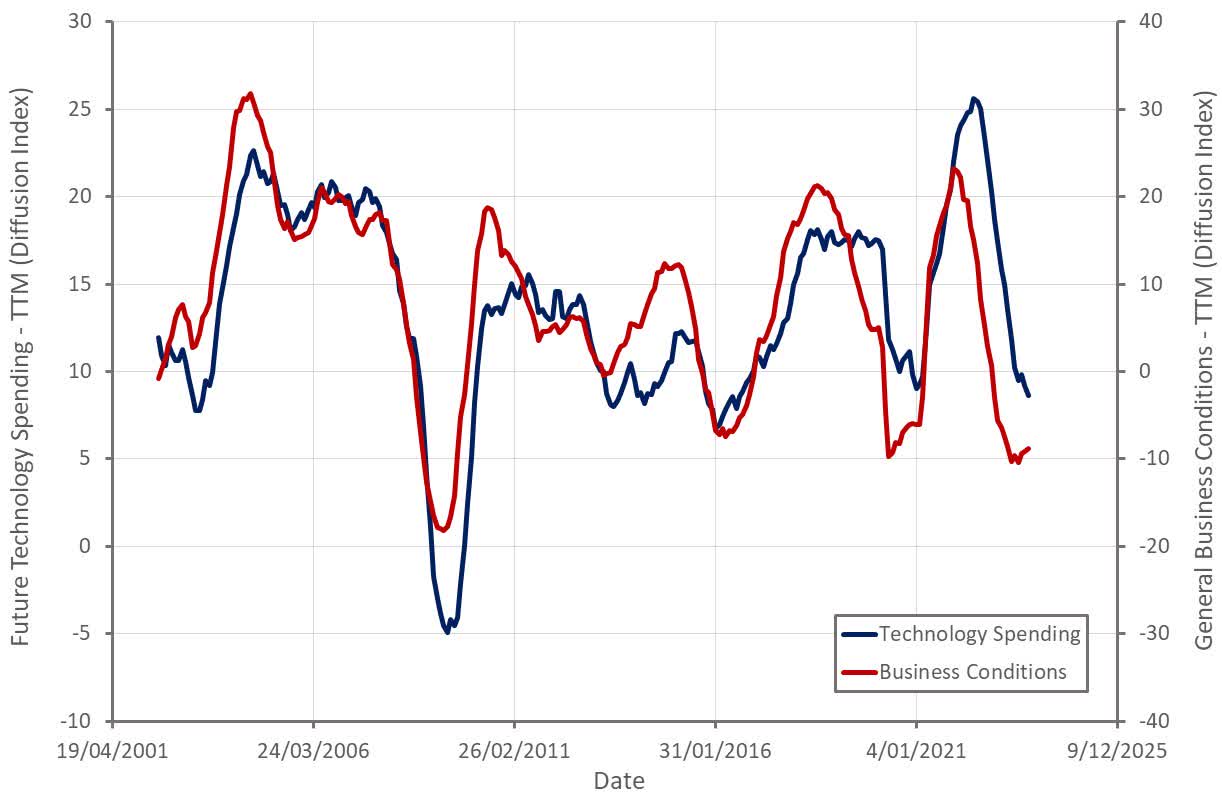

Cognex suggested on its second quarter earnings call that conditions weakened as the quarter progressed. This weakness is reflected in manufacturing survey data, which has been soft for the better part of a year now. Manufacturing activity in important markets for Cognex, like Germany and the US, is currently weak, and China’s reopening has failed to live up to the expectations of Cognex’s management team.

Reshoring /near shoring/friend shoring of supply chains continues, particularly in consumer electronics and automotive, but challenges like labor and skill shortages are having an impact. This may also be negatively impacting Cognex's business relative to expectations.

{kind=link}

Figure 1: Manufacturing Survey Data (source: Created by author using data from The Federal Reserve)

Customers remain cautious in regard to CapEx, likely driven by macro uncertainty and higher interest rates. This has been particularly acute within the consumer electronics and semiconductor verticals, where Cognex has seen the steepest decline in demand. Cognex has suggested that it feels the impact of business cycles more rapidly than many of its industrial peers, given the short-cycle nature of its business.

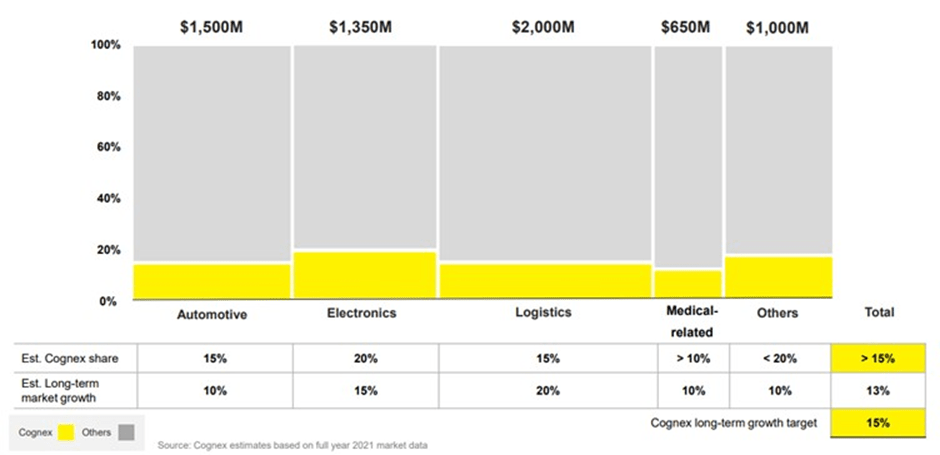

While Cognex is facing cyclical headwinds, machine vision remains a growth market due to the increasing capabilities of AI and greater automation of workflows. Cognex currently serves a 6.5 billion USD market , which is expected to grow at a double-digit annual pace going forward.

{kind=link}

Figure 2: Cognex's Market Size and Market Share (source: Cognex)

Automotive, electronics, logistics and life sciences are Cognex's most important end markets. Machine vision is used in most automotive manufacturing steps, and growth is expected from the increased use of electronics within vehicles. There is also a multi-year investment in EV manufacturing capacity underway, with Cognex standing to benefit in areas like battery production. Cognex remains bullish on the long-term prospects of its technology within EV battery manufacturing, but some projects have faced delays or are ramping more slowly than expected. EV battery growth is robust, but this has not been sufficient to offset the decline in traditional automotive applications. Cognex's EV business grew by over 30% YoY in the second quarter, but still only represents less than a quarter of automotive revenue. Cognex believes that many car companies are dealing with excess inventories and have little desire to invest in production at the moment.

Cognex’s business could also be impacted by the simultaneous strikes launched by the United Auto Workers union against General Motors, Ford and Stellantis in mid-September. While the strike has initially been fairly targeted, if the groups involved cannot come to an agreement, a larger strike may occur. In addition, a longer strike will have a more severe impact on the automotive supply chain.

Longer term, the strike could actually be a positive for technology suppliers like Cognex. If the cost of labor increases significantly, it should increase the demand for automation technology. A longer strike is also likely to boost the EV market, which should also be positive for Cognex in the long run.

Machine vision is also widely used in the manufacturing of consumer electronic devices. The adoption of AR/VR technology should be a tailwind, but growth is likely to be weaker than it has been in the past, as many markets are near saturation. The consumer electronics market is still recovering from a post-pandemic hangover, with the recent drop in demand for Cognex's products most severe within the consumer electronics and semiconductor verticals.

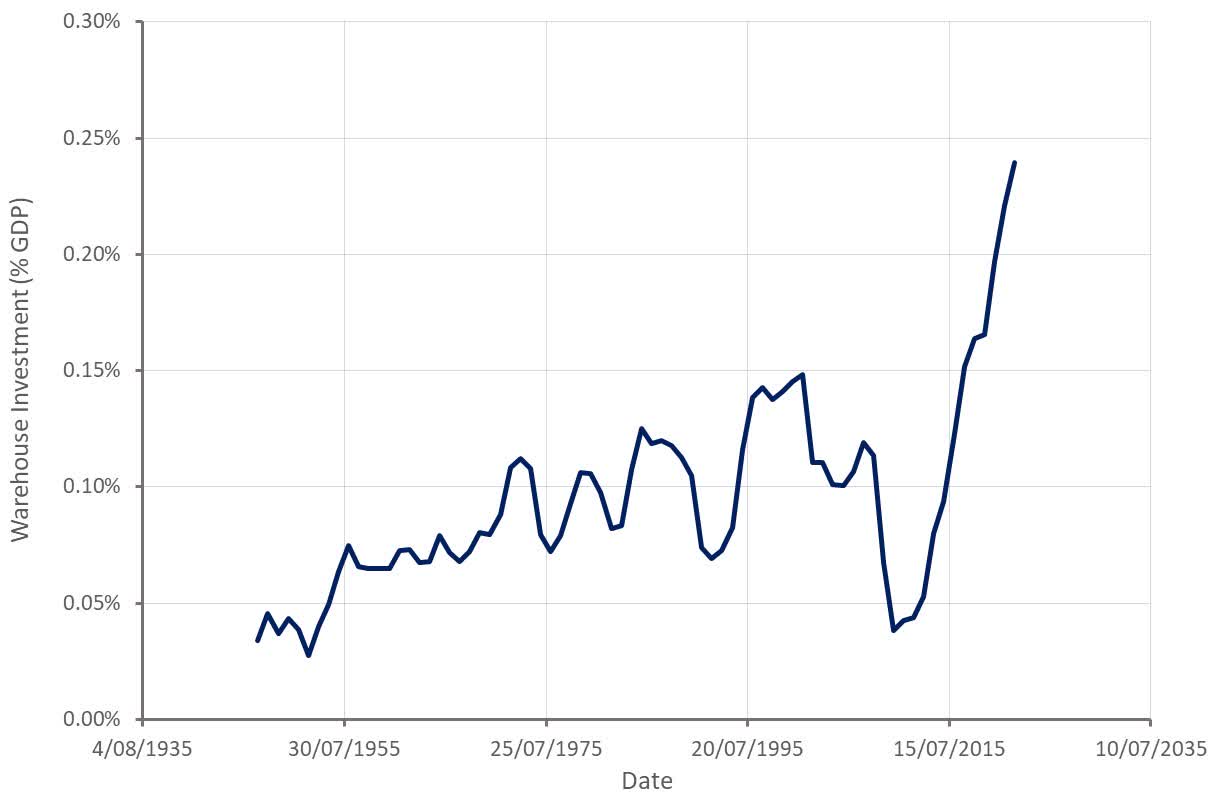

Logistics is Cognex’s largest and fastest growing market. Despite this, adoption of machine vision in logistics is still relatively low. The past 12–18 months has been difficult due to a supply chain bullwhip effect negatively impacting logistics markets and the market still digesting large infrastructure investments made over the past few years. Revenue from large ecommerce customers remains depressed, but has been fairly stable over the past four quarters. The rest of Cognex’s logistics business is outperforming the ecommerce segment.

{kind=link}

Figure 3: Private Warehouse Investment in the US (source: Created by author using data from The Federal Reserve)

Life sciences is a highly regulated, non-cyclical market with long product life cycles. Cognex’s technology is specified in over 100 machines, and this is reportedly a high growth market for Cognex.

Outside of these main segments, revenue has generally been lower YoY, with the exception of consumer products and food and beverage.

Cognex

Cognex's future growth should be supported by the rollout of new products and recent efforts to address the long tail of the market. A record thirteen new products were launched in the first half of 2023, with a focus on offering machine learning at the edge.

Edge learning makes Cognex's solutions more powerful and makes the technology easier to deploy. Products can be trained on relatively few samples without requiring much programming, meaning they can be utilized by customers who don't have large engineering teams.

Cognex believes that this could help expand its customer base from 30,000 today to hundreds of thousands in the future. Cognex is scaling its salesforce to address these new customers, which is a drag on margins at the moment. The bulk of hiring for this initiative has now been completed and training is reportedly progressing well.

Cognex's attempt to broaden its customer base is somewhat risky, as it will require a different sales motion. There is also the question of whether easier to use technology lowers the barriers to entry in the industry.

Moritex Acquisition

Cognex has a strong balance sheet and relatively large cash balance, which positions the company to take advantage of a favorable environment for M&A. In October 2023 Cognex completed the acquisition of Moritex , a Japanese manufacturer of optical components for machine vision systems.

Cognex believes that the inclusion of optical components in its product portfolio will enable a more comprehensive offering . Cognex has long sold Moritex optics components as a part of its solutions but believes integrating the two technologies will streamline its solution and enable more advanced offerings. Moritex could also help Cognex to penetrate the machine vision market in Japan.

This was an all-cash transaction, worth approximately 275 million USD . Moritex is expected to contribute 6-8% of Cognex’s revenue going forward, meaning Cognex paid a multiple something like 5x sales.

Financial Analysis

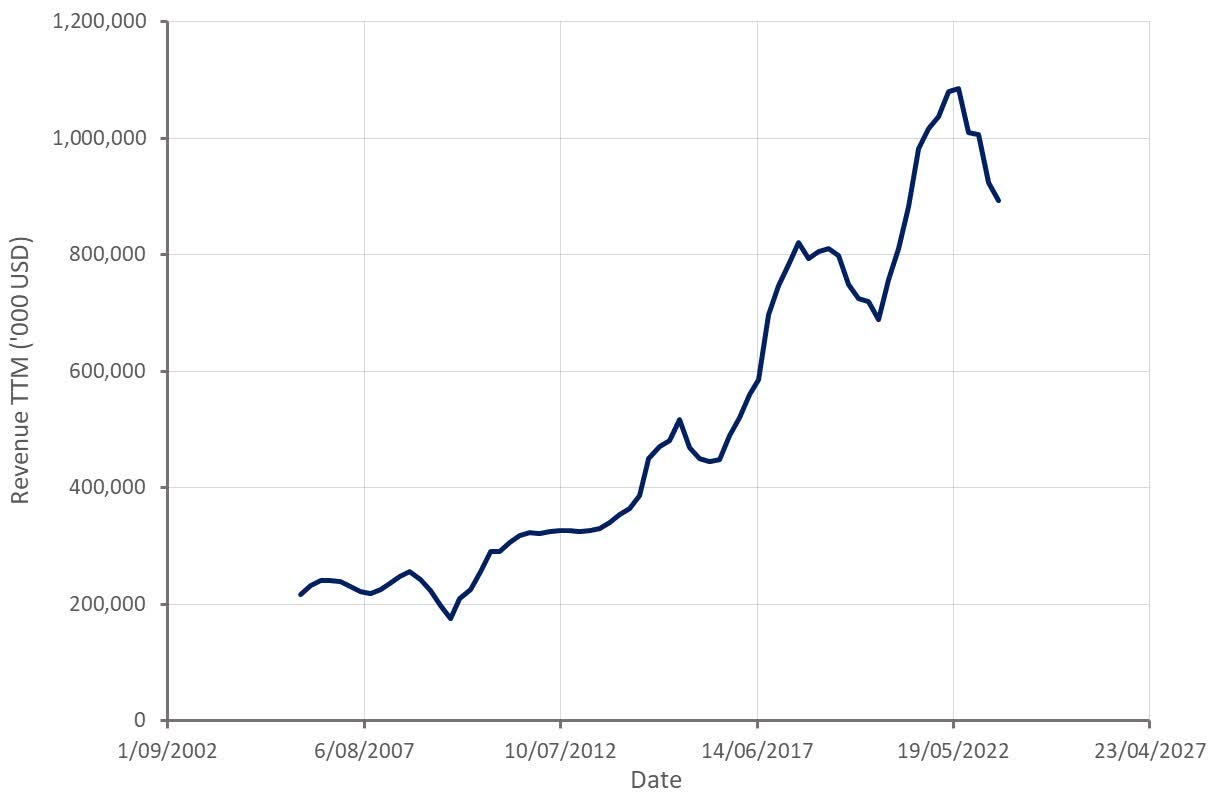

Cognex’s second quarter revenue was 243 million USD, a 12% YoY decline. Second quarter revenue was aided by the recognition of approximately 15 million USD of consumer electronics revenue that was not expected until the third quarter. Excluding this impact, revenue would have been down roughly 17% YoY. Revenue in the Americas was down 10% YoY and 8% YoY in Europe. Excluding the 15 million USD consumer electronics tailwind, revenue in China and other Asian markets were both down by close to 30% YoY.

Revenue in the third quarter is expected to be 180-200 million USD, which would represent a 9% decline YoY at the midpoint.

{kind=link}

Figure 4: Cognex Revenue (source: Created by author using data from Cognex)

Cognex’s gross profit margin in the second quarter was 74%, in line with guidance and the company’s long-term target. Margins have benefited from high-cost inventory moving off the balance sheet, although this has been partially offset by foreign exchange headwinds and lower revenue.

Cognex is also facing margin headwinds from a shift in revenue mix. Usage of software in Cognex's consumer electronics products is relatively high, creating high gross profit margins for this segment. The rapid decline in consumer electronics revenue has therefore been a margin headwind.

{kind=link}

Figure 5: Cognex Gross Profit Margins (source: Created by author using data from Cognex)

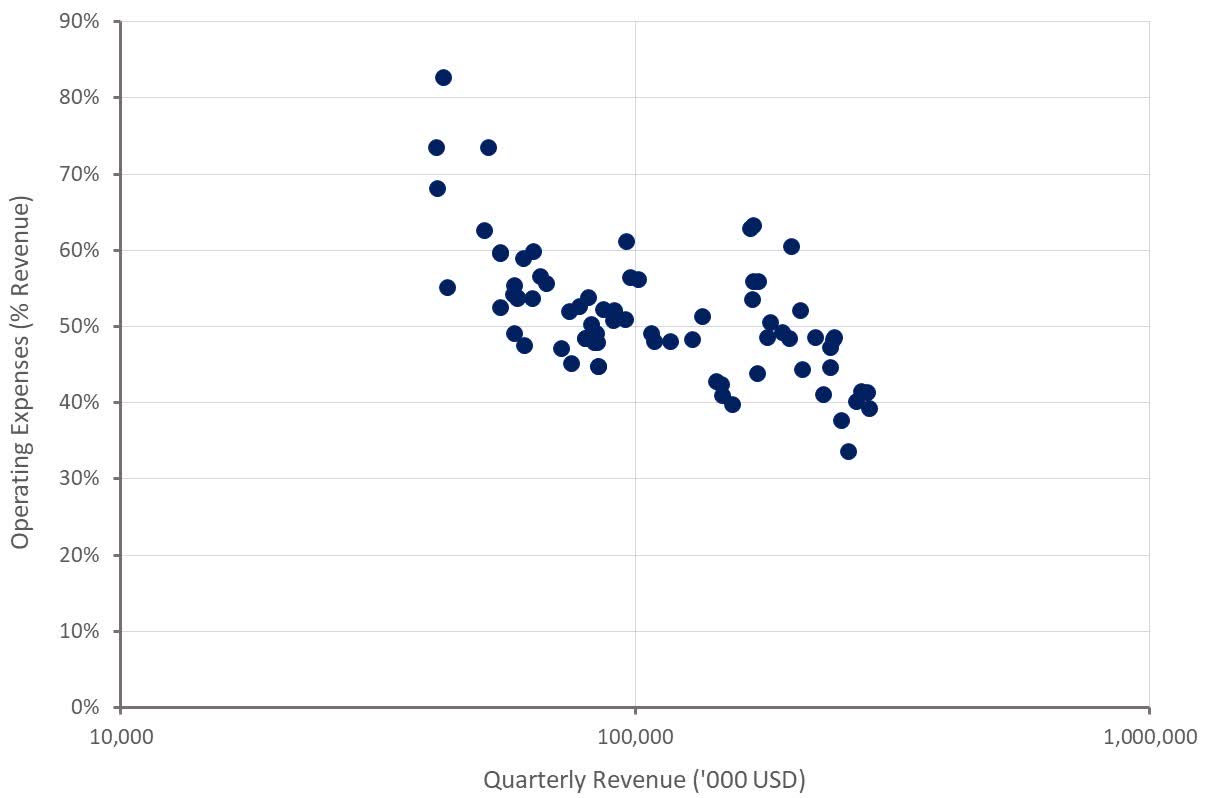

Despite a significant decline in revenue, Cognex’s operating profit margins have held up reasonably well, as the company has carefully managed costs (headcount, compensation, discretionary spend).

OpEx declined by 13% YoY, including a 20 million USD expense in Q2 2022 related to a fire at Cognex’s primary contract manufacturer. Excluding this impact, operating expenses increased 3% YoY due to investments in an emerging customer initiative.

{kind=link}

Figure 6: Cognex Operating Profit Margins (source: Created by author using data from Cognex)

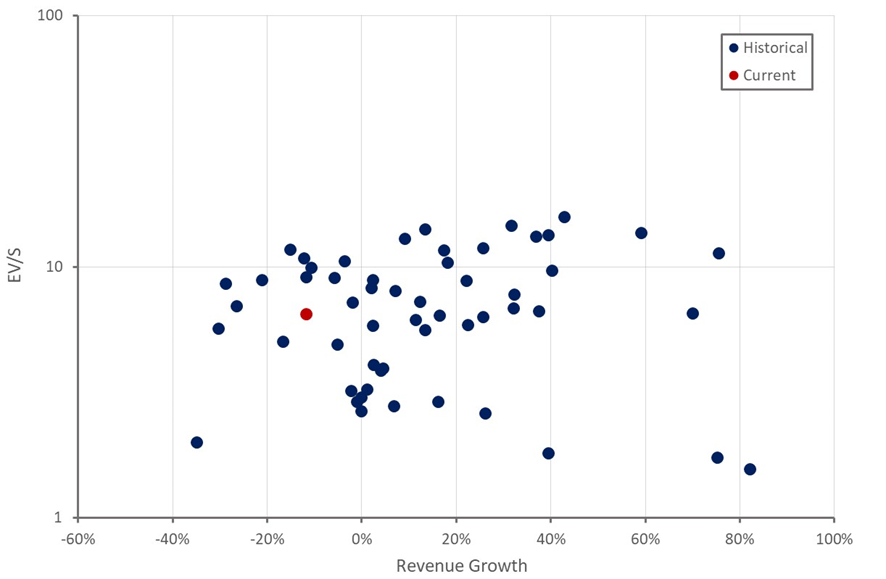

Valuation

Cognex's stock is now down approximately 60% from its peak in early 2021, and its revenue multiple is near the lower end of its normal range, excluding recessionary periods.

For investors willing to look through near term weakness, there is a potential opportunity, though. In a healthier demand environment, Cognex is likely to sustain double-digit growth over the long run. Operating leverage should also help operating profit margins to increase towards 35-40%. A combination of solid growth, margin expansion and multiple expansion could see the stock offer something like 15-20% annual returns over the next 5-10 years.

Revenue will probably continue to decline in the near-term, though, and further multiple compression seems likely. Cognex has long been an investor favorite, but confidence in the business appears to have been broken. From a technical perspective, there also may not be much support for the stock until 25 USD per share.

{kind=link}

Figure 7: Cognex Relative Valuation (source: Created by author using data from Seeking Alpha)

For further details see:

Cognex: Waiting For An Entry Point