CGNT - Cognyte Software: An Attractive Investment Idea And A Potential Acquisition Play Too

2023-08-12 00:05:46 ET

Summary

- Cognyte is a global leader in security intelligence and investigative analytics, which serves hundreds of customers, primarily in the government sector, in over 100 countries.

- In 2022, Cognyte's stock value plummeted by 80% due to disappointing results caused by challenges in converting backlog to revenues, reduced customer funding, and global supply chain disruptions.

- During this year, Cognyte has observed a macro environment improvement, which indicates a positive turning point and generates optimism that profitability is within sight.

- Considering the increasing demand for AI-powered solutions and the ongoing improvement of fundamentals, I view the current price as an attractive buying opportunity.

- Cognyte is seen as a potential acquisition target for companies such as Palantir or L3Harris, offering opportunities for synergies and driving accelerated growth and value creation for the buyer.

Editor's note: Seeking Alpha is proud to welcome Black Tiger Research as a new contributor. It's easy to become a Seeking Alpha contributor and earn money for your best investment ideas. Active contributors also get free access to SA Premium. Click here to find out more »

Thesis

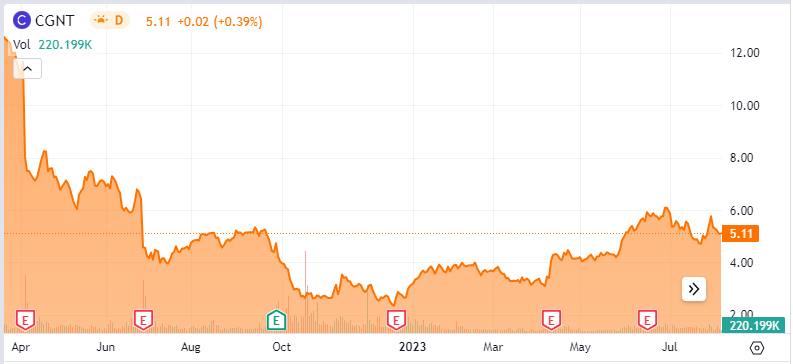

Cognyte ( CGNT ) exhibited significant volatility over the last 18 months. During 2021, CGNT traded at its highest level of $33.3 and then plummeted to its lowest level of $2.3 by December 2022. CGNT is currently trading at an attractive sales multiple of 1X. The recent developments in AI provide new opportunities for driving long-term growth. The company has been able to keep costs down in Q1, leading to a narrowing of losses. If this trend continues, it should be able to return a profit in Q4 and its multiple will likely rerate to reflect its improved fundamentals .

I believe that the current price level is seen as an attractive buying opportunity under the following vectors, the first is ongoing fundamental improvement and the company's willingness to return to the same levels of profitability as in fiscal 2022, and the second is an attractive potential acquisition target by a large player, such as Palantir ( PLTR ) or L3Harris ( LHX ).

Business Overview

Cognyte is a global leader in security intelligence and investigative analytics. The security intelligence industry is driven by the increasing need of organizations to protect their assets, people, and information in the face of growing security threats, including cybercrime, terrorism, fraud, and other malicious activities. Cognyte specializes in investigative analytics and develops software solutions that gather, analyze, and derive actionable insights by AI capabilities, from vast amounts of data to address security threats and risks mainly in the realm of communication. The company serves a wide range of industries with various clients, including governments, law enforcement agencies, financial services, and more.

Advanced analytics and AI-powered solutions have become critical and Cognyte's solutions empower organizations with insights that help connect the dots and accelerate time-critical investigations more effectively . Cognyte has been using AI for years and has identified the potential for expanding these capabilities to derive greater value, considering the increasing demand for AI-powered solutions.

Cognyte employs ~1,650 FTEs worldwide and serves hundreds of customers, primarily in the government sector, in over 100 countries. While it is very active in EMEA region, where it generates 83% of its revenues, only a small fraction of its revenue is generated in the US.

Revenue Challenges in FY23

In 2022, Cognyte stock experienced a significant 80% decline. The company encountered a series of difficulties, reported bad financial results, and had difficulty providing a forecast for the entire year. The reasons for this were the challenges of converting backlog to revenues, due to customers’ reduced funding and shifting spending priorities along with global supply chain disruptions. Additionally, overall negative sentiment towards companies that were unprofitable. The company which generated $89M of Adj. EBITDA in the fiscal year 2022 (Cognyte's annual fiscal year ends in January) has moved to a sequential decline in revenue and significant losses throughout fiscal 2023 .

the macro environment negatively affected customers and led to government budgets being reallocated for military needs due to the Russia-Ukraine war, along with global supply chain disruptions that occurred after COVID-19. These challenging macro developments were reflected in the company's share price, which plummeted to its lowest level in 2022.

Better Visibility

Cognyte has an impressive backlog of $583M (RPO), which has been steadily growing as per its latest annual report (As you can see below). Cognyte has sharpened its focus on backlog conversion and has taken proactive steps to address the issues hindering the process. The management hired a CRO (Chief Revenue Officer) to better understand the slow conversion challenges and to enhance internal performance .

Throughout the current year, Cognyte has observed a notable improvement in the macro environment compared to the challenges faced in 2022 . CGNT continues to win deals from a variety of customers, indicating a positive shift in market conditions. In the last conference call , the company's management described that the current macro environment conditions are better, with more visibility. Many customers have returned to their regular behaviors, expressing confidence and stability in their budgets and plans.

These positive factors strengthened the company's ability to convert its significant backlog into revenue, resulting beat expectations, with sales reaching $73M while the expectation was $68M for Q1 of fiscal 2024 .

The management provided revenue guidance of $303M for the entire year, which represents solid 7% growth from the previous year’s SIS Adjusted non-GAAP revenue. I think that the combination of a significant backlog and an improving macro environment presents huge potential for achieving significant revenue growth.

*The annual fiscal year ends in January (Cognyte’s IR Presentation)

CGNT Shows Improvement in Results

Source: Cognyte’s IR Presentation (“SIS” refers to situational intelligence solutions business, which was part of the 'Threat Intelligence Analytics' offering’ and divested on December 1, 2022.)

{kind=link}

Cognyte has a good margin profile which should generate earnings in the short and long term. CGNT has demonstrated a strong ability for profitability by reaching an Adj. EBITDA of $89M with a margin of 19% in the fiscal year 2022. In FY 2023, the gross margin was 61.6% (not SIS Adjusted), which saw an improvement to 68.4% during the first quarter of FY 2024 as attributed to increased software revenue. Impressively, the management has provided a gross margin guidance of 66.5% for the entire year, indicating a 8% enhancement compared to FY 2023. Looking ahead, I anticipate the company reaching a long-term gross margin of over 70%. This growth will be driven by the continuous expansion of revenue from software operations. In addition, the management also provided an outlook of positive cash flow from operations for the full year.

For the fiscal year 2023, $140M was invested in R&D, which constituted 45% of the revenues, and another $155M was invested in S&M and G&A, which constituted 50% of the revenues - which is 95% of total revenue. Q1 of FY 24 displayed an impressive improvement in the operating expenses ratio as a result of implementing an efficiency plan . The company significantly cut operating expenses and the OPEX margin constituted 77% of total revenues .

These indicators point towards a positive turning point, leading to optimism that profitability is within sight for Cognyte, thus have contributing to the upward trajectory of the stock price since the beginning of the year.

CGNT is trading at a market cap of $352M and has a cash balance of $73M, which means its forward EV / Sales multiple is 1. Cognyte's large security competitors include, among others, Palantir, L3Harris, Thales and Datawalk. I think that Palantir and Datawalk ( DATP ) are more similar to Cognyte, compared to L3Harris and Thales, which have a broader range of operations across various fields. When examining direct competitors in the industry, it can be seen they are commanding double-digit sales multiples. Palantir, with an annual revenue forecast of $2.2B for the entire year, holds a significantly higher forward EV / Sales multiple of 15. Datawalk also has a higher sales multiple of 10. In March 2022, Google announced that it would acquire Mandiant for $5.4 billion. Mandiant, another competitor, which spun off from FireEye, provides solutions for security and threat intelligence. Google's acquisition of Mandiant marked a sales multiple of 10 based on the FY 2021 results.

P/S Ratio Comparing

The main concern may lie in the execution aspect of the business, although management has promised to pay close attention to this issue. I believe that in the near future , the results should be satisfactory, as the company expected to deliver solid upcoming quarters, in order to solidify the assessment that Cognyte is genuinely on track for a positive turning point with better visibility on the horizon. At the current price level, I see no significant additional risks since the crisis faced by the company was an exogenous event that impacted numerous companies. Moreover, CGNT benefits from a steadfast customer base, and long-standing relationships that have spanned decades.

As mentioned above, apart from being an attractive investment at 1X sales multiple, Cognyte holds significant potential for value creation, making it an attractive target in the event of a strategic buyout or merger situation.

Could Cognyte be an attractive acquisition target?

Palantir and L3Harris are two prominent players in the industry, which could potentially unlock significant synergies and further drive growth by acquiring Cognyte. Both companies have significant expertise in data analytics and security intelligence, making them ideal candidates to acquire Cognyte. Such an acquisition will surely lead to an expansion of a wider range of solutions, and further enabling a seamless integration of data, analysis, and threat detection.

Cognyte has a stable and strong customer base outside of the US, with most of its revenue coming from the EMEA region. This geographic exposure could be very complimentary for Palantir or L3Harris, as they are very active in the US, with 61% and 90% of revenues, respectively. The acquisition of Cognyte will open new market opportunities outside the US, thus increasing the chance to leverage each other’s geographic footprint.

Source: Cognyte & Palantir Annual Reports

Think about it...

Cost Synergies : The acquisition of Cognyte would enable Palantir or L3Harris to pool their R&D resources, allowing the merged entity to accelerate innovation and foster the development of next-generation security analytics tools. Such shared expertise and collaboration would accelerate the creation of cutting-edge solutions and to maximize the opportunities in the space. Furthermore, as mentioned above, Cognyte has massive operating expenses that constitute a high percentage of the company's revenues, which can be significantly reduced by this type of acquisition leading to significant cost savings.

Source: Cognyte’s Reports

Think how much this savings is worth…

I evaluate that the merged entity will be able to save at least $100M, as it is a strategic buyer that can offer many synergies and operates in the same industry.

Market growth and revenue potential : The security intelligence market is experiencing significant growth, driven by increased security threats and the need for advanced data-driven solutions. By acquiring Cognyte either Palantir or L3Harris, will be able to open new revenue streams and expand their customer base. Alongside leveraging their existing customer networks, established relationships, and market presence to cross-sell additional security intelligence solutions to their extensive customer base, thereby driving accelerated revenue growth.

Market Dominance : The merged entity would possess a formidable market presence. The increased market dominance would enable either company to set industry standards, shape market trends, stay ahead of competitors, and drive sustainable growth and profitability.

Conclusion

While the price of CGNT has been volatile, I believe the current price level presents an attractive buying opportunity. Throughout the current year, Cognyte has observed a notable improvement in macro environment conditions which positively contributed to their business . CGNT continues to win deals, and customers expressed confidence in their budgets and plans. The improvements seen in the first-quarter results, along with the encouraging outlook for the entire year, indicate a positive turning point for the company, which supports the upward trend of the share price since the beginning of the year. Cognyte is focused on returning to profitability levels that it had in the past and possesses a significant potential that may surpass expectations and command a higher premium.

Cognyte's blend of technological expertise and a cheap sales multiple, positions the company as an attractive acquisition target for larger companies that are aiming to strengthen their business. Prominent industry players, such as Palantir and L3Harris, have an opportunity to expand their offerings through the potential acquisition of Cognyte. Such an acquisition would create significant value to both companies, by extending their reach into additional territories outside the US, due to Cognyte's broad customer base outside the US, and potentially expand their product offerings. The potential for cost savings is very significant as well, as an efficient merger will surely reduce a significant portion of Cognyte’s operating cost base . Lastly, the significant spread between the buyer’s and seller’s multiple means an immediate value creation to the buyer at the date of acquisition .

Accelerated growth + wider margins + attractive multiple = significant value creation

{kind=link}

For further details see:

Cognyte Software: An Attractive Investment Idea And A Potential Acquisition Play Too