LASR - Coherent: Discounted And Attractive Entry Point For The Medium To Long Term

2023-06-14 03:30:54 ET

Summary

- The acquisition of Coherent proved to impede the combined company’s resources considerably, due to the current macro conditions.

- The combined company of II-VI and Coherent now controls a durable and attractive portfolio within the industrial, communications, electronics and instrumentation markets.

- The company's silicon carbide platform is expected to be a major value driver, with electric vehicle and renewable energy markets driving adoption.

- Despite short-term challenges, Coherent's competitive advantages and strong intellectual property make it a promising long-term investment with potential for significant capital gains.

- We share an options strategy as well for risk-averse investors.

Editor's note: Seeking Alpha is proud to welcome Total Return Investing as a new contributor. It's easy to become a Seeking Alpha contributor and earn money for your best investment ideas. Active contributors also get free access to SA Premium. Click here to find out more »

Thesis

The current share price of Coherent Corp. ( COHR ) presents an attractive entry point for the medium to long term. Our analysis of the fundamentals and valuation shows that the stock is undervalued and leads us to take a bullish position. The most recent acquisition, combining the assets of Coherent and II-VI, created a heavy burden on the company, but we will examine how the acquisition will ultimately benefit investors long term. The company and the industry as a whole have been lagging behind the technology sector since the beginning of the year; we expect this to change as a result of mean-reversion. Coherent is a consolidator in an industry that is expected to grow significantly in the future. Coherent is positioning itself to become a prime beneficiary.

A Vibrant History

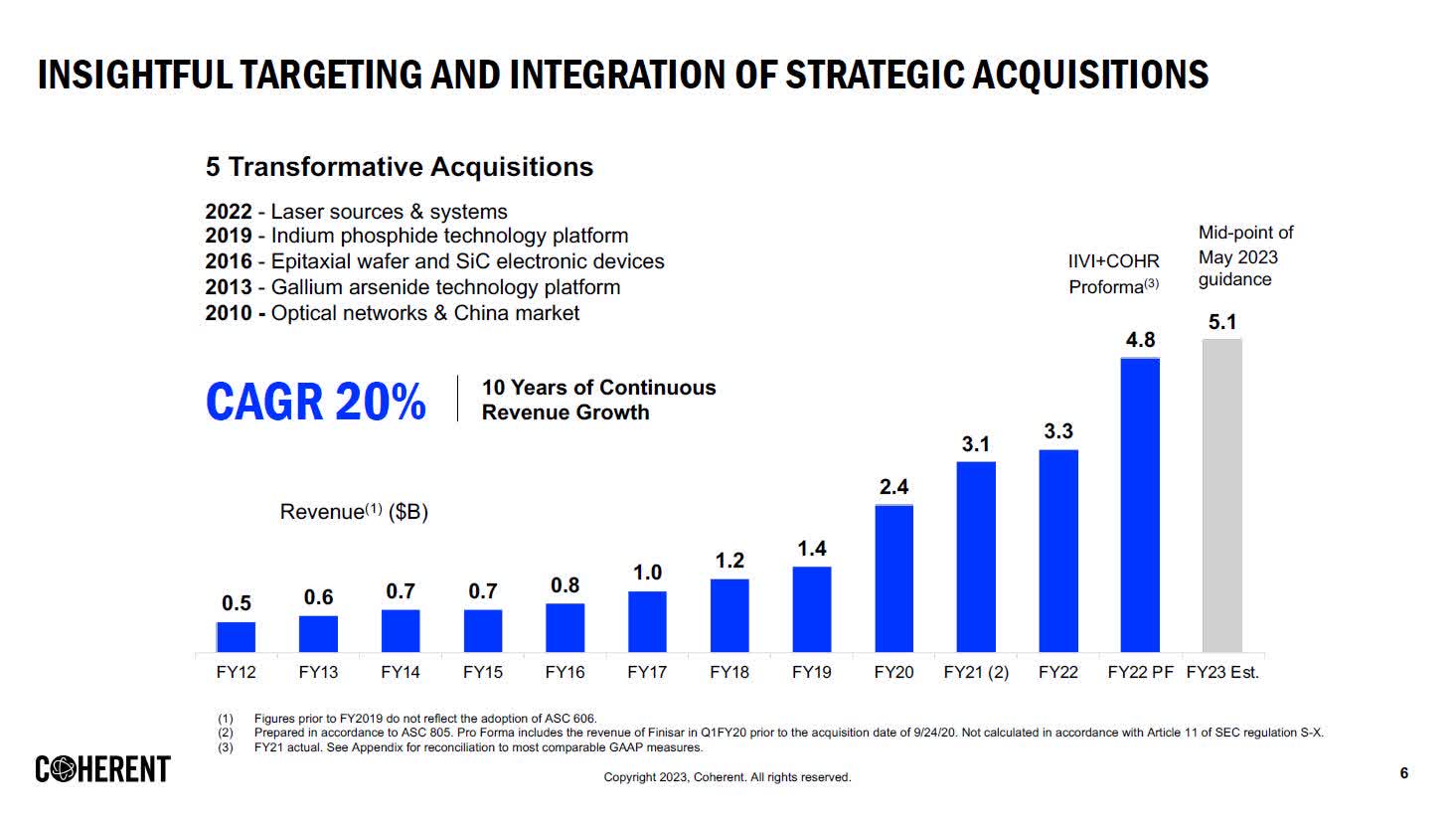

Coherent, as the company is now named, has had a vibrant past. Founded as II-VI in 1971 to manufacture high-quality materials and optics for industrial lasers, the name was a reference to the groups II and VI in the periodic table. II-VI then held its IPO in 1987 and during the '90s, it began to grow and diversify its portfolio organically, and also to a strong degree, by acquiring technologies from other companies.

Before the Coherent acquisition, in 2019, the company acquired Finisar for its indium phosphide technology platform, in a deal valued at ~ $3.2 billion. Most recently, the Coherent acquisition, completed just under a year ago, on the 1st July 2022 in a deal valued at ~ $7 billion at the time, was arguably its most significant and risk prone acquisition yet. The acquisition stemmed from a bidding war , involving competitors MKS Instruments, Inc. ( MKSI ) and Lumentum Holdings Inc. (LITE). Initially, Lumentum started the bidding war by offering to pay ~$5.7 billion for Coherent. The price that II-VI ultimately paid was a ~23% markup to the initial offer. The market treated the deal with a heavy dose of skepticism, and rightly so, as this was suddenly a heavy premium to pay, on top of having to pay a termination fee of over $200 million to Lumentum. Around the time the deal was announced, II-VI was trading near its all-time high. From that point on, although the underlying business performance was relatively strong, the share price began to erode as inflation in the US began to surge and the market began to price in the cost of the newly issued debt to fund the acquisition, and its impact on earnings. It was unfortunate timing, to say the least.

Through a combination of macro headwinds that the company faces, in addition to persisting industry headwinds , the company's share price has remained depressed, while the technology sector as a whole has seen a strong rally since the beginning of the year. We see both issues as being somewhat resolved in the short term. Starting from late 2024 and going into 2025, we anticipate a strong rebound for the industry, with analysts expecting 58.4% non-GAAP earnings growth in FY2025. We also see the macro headwinds which are currently causing the company to carry a significant burden from the elevated debt, on top of softening demand, to also ease around this time frame. We also expect that the company continues to execute on improving operating efficiencies through synergies created by the acquisition, as they have managed to do in the past. Coherent has a strong track record of executing well on acquisitions, as seen by the excellent revenue growth performance of the last 10 years, all while increasing their EBITDA margin over the years; so far they have always come out on top.

{kind=link}

The Company's Present And Future Opportunity

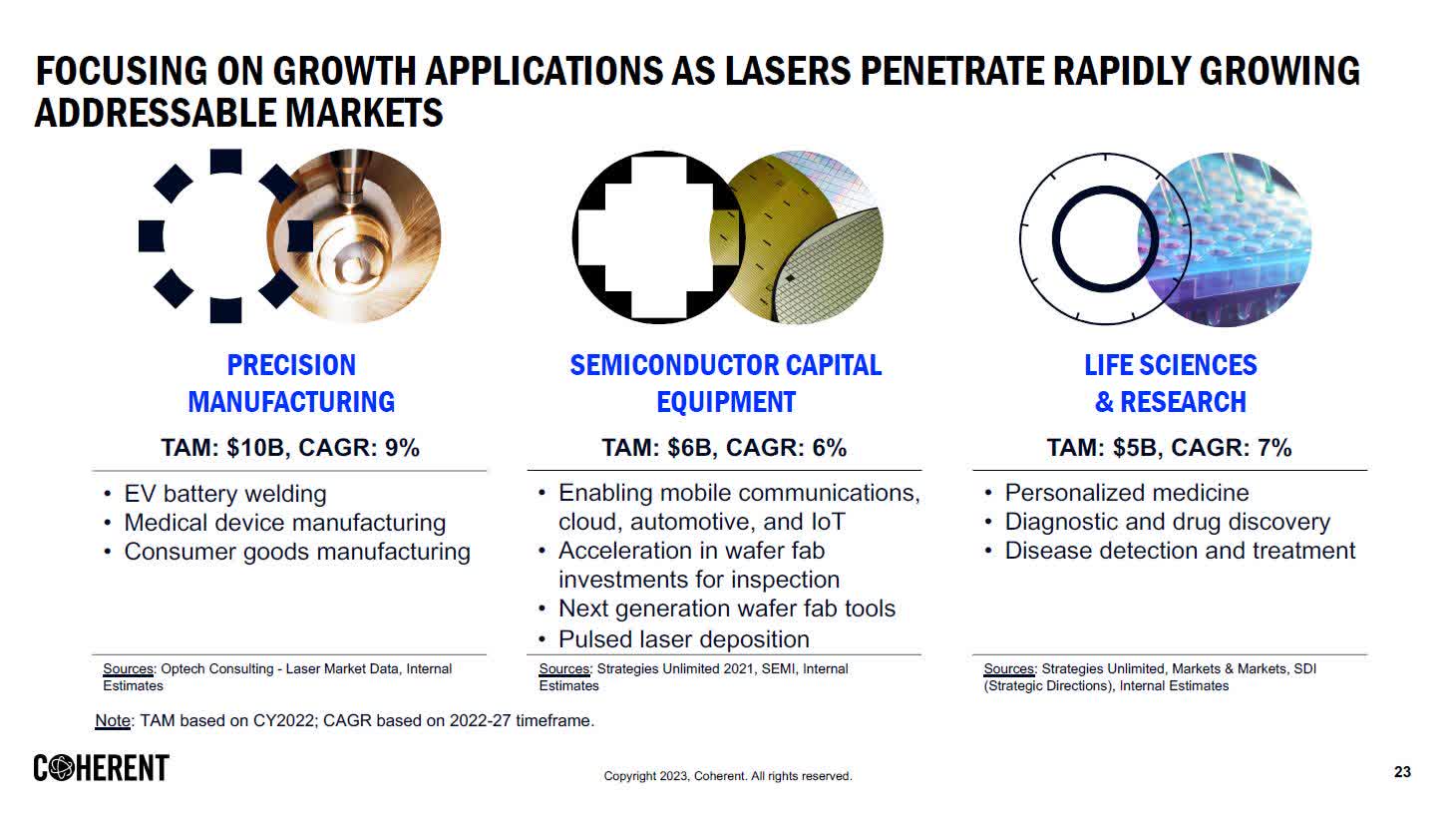

As shown in the previous section, Coherent is no doubt within the ranks of a group of companies known to be serial acquirers. We consider Broadcom (AVGO) to arguably be the gold standard of this subset of companies. Successful serial acquirers can over the years become a dominant force within their respective industry, if they have a strong track record of prudent acquisitions and a successful execution of integration; there is certainly a lot of value to be created. While Coherent has a lot to prove with its latest acquisition, we believe the building blocks for continued success have been laid. A strong portfolio of laser products was added. In particular, Coherent pioneered the development of Excimer Laser Annealing for producing Low Temperature Polysilicon TFTs, enabling the production of OLED and upcoming microLED displays. The full portfolio of products now spans across the materials, lasers and networking segments, giving the company additional diversification and protection against cyclicality in any one segment.

{kind=link}

While the existing and newly added product lines, stemming from decades of deep domain knowledge in the industry, are all beneficiaries of a fast growing market in the long term, we recognize the silicon carbide platform to be the biggest value driver going forward. In our view, the biggest opportunity cost of the latest acquisition is not being able to allocate more resources to invest even more into the silicon carbide (SiC) platform.

{kind=link}

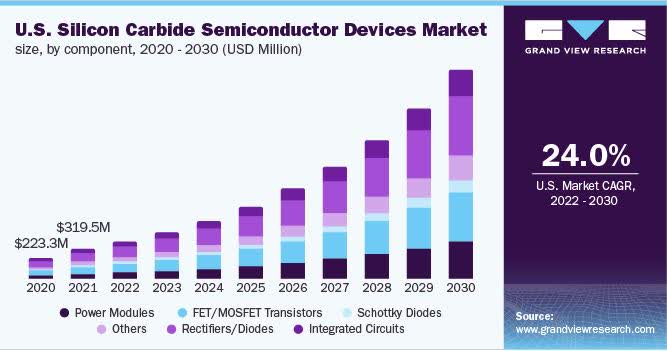

The electric vehicle and renewable energy markets will continue to be major drivers enabling SiC adoption. Coherent engineers and manufactures the wafers, namely 100 mm and 150 mm wafers, with 200 mm wafers starting manufacturing in 2024. Coherent has a history of pioneering here too, with demonstrating the world's first 200 mm SiC wafer in 2015. As the production costs for clients becomes considerably cheaper with the introduction of 200 mm wafers, demand for Coherent's SiC wafers will substantially increase. Wolfspeed, Inc. ( WOLF ) is a major competitor with a 53% market share, while Coherent's share stands at 19%. Recently, very notable partnerships with Infineon Technologies AG ( IFNNY ) and Mitsubishi Electric Corporation ( MIELY ) were inked out, bolstering its stance in the market. The most recent partnership with Mitsubishi Electric will see Coherent developing a supply of 200 mm SiC wafers to a future manufacturing plant of Mitsubishi Electric. This illustrates how customers are eager to lock in supply deals in an increasingly supply constrained market for SiC wafers.

The CEO, Dr. Vincent D. "Chuck" Mattera, stated on the Q3 2023 earnings call :

Even with the $1 billion investment over 10 years that we announced in August of 2021, the gap between projected supply and demand is accelerating, and so we now believe that the market leader who emerges will be the incumbent who is able to timely close the gap and serve the market needs.

With respect to our silicon carbide business, it grew more than 40% year-over-year. This business continues to be one of our top priorities. Therefore, our equipment investments in the silicon carbide platform expansion were again about half of our total capital investment. The market is showing signs of a prolonged period of severe capacity constraints forming.

{kind=link}

The Investment Opportunity

No matter the magnitude of potential a company may be presented with, we believe investors should always take a holistic view, and not be blindsided by hype or emotions. As such, we believe the valuation of a company is just as important as the underlying business fundamentals. When finding an investment opportunity that ideally leans as far as possible towards excellent fundamentals combined with excellent valuation, alpha can be generated. Of course, in the market, there is no free lunch and the chances of finding that perfect opportunity is rare, as risks are always involved, that the market identifies and prices in. We believe the market can, however, be rather short-sighted on occasion and also over-blow risks. To that end, based on a variety of conditions, investments can simply just be temporarily out of favor. We observe Coherent, and the industry as a whole, to currently be out of favor. We also rate the fundamentals and the valuation of Coherent to be better than the industry average right now. This is even when accounting for the current interest expense, as competitors, especially MKS Instruments, are also in somewhat the same situation.

{kind=link}

Unfortunately, the investment case here relies entirely on the investor profiting from capital gains, with very little assistance from management rewarding shareholders with stock repurchases. In fact, stock-based compensation has been larger than stock repurchases over the last number of years, therefore being dilutive by nature. Over the past 5 years, Coherent generated a healthy ~ $2.053 billion in operating cash flow with ~ $1.196 billion being spent on capex, leaving ~ $857 million in free cash flow over that span. The free cash flow has historically mainly gone to paying for acquisitions, and until the debt burden becomes significantly less, we expect free cash flow to mainly repay debt going forward.

Valuation

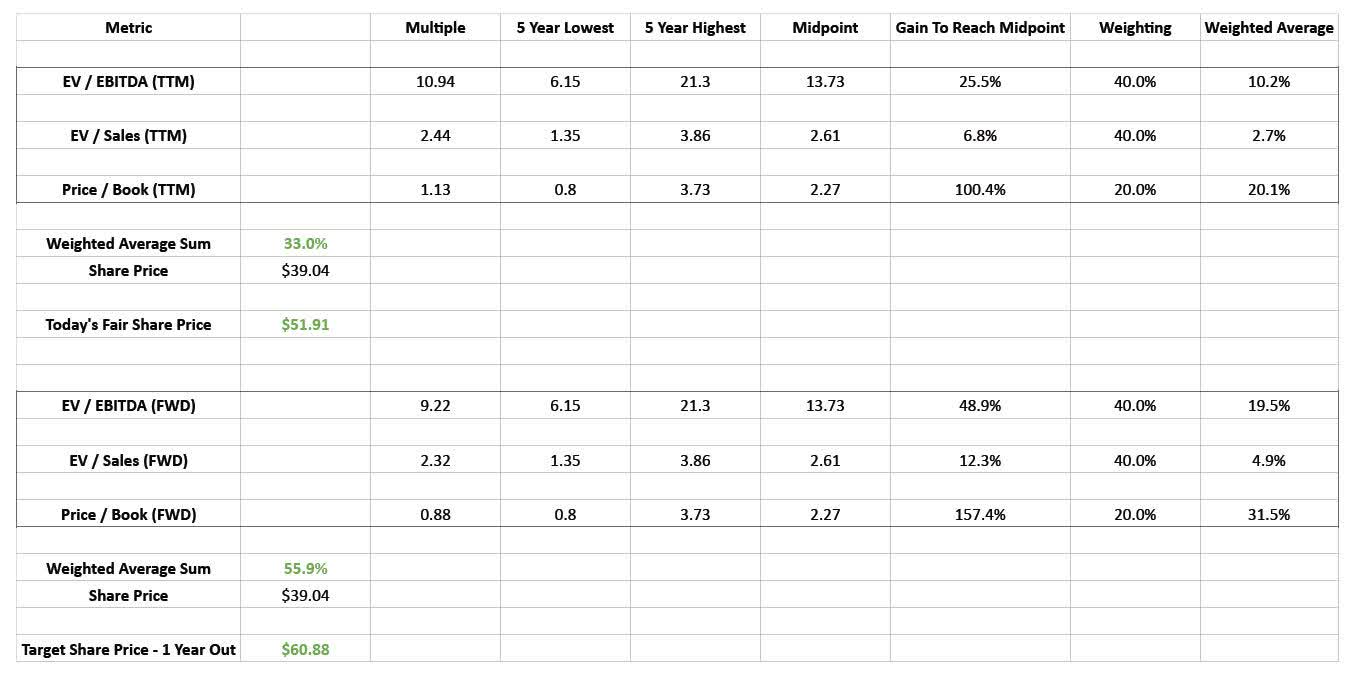

At the time of writing, the share price is $39.04 with an enterprise value of $11.7 billion. The TTM free cash flow is just ~ $129 million, currently leaving us with a whopping EV / FCF multiple of 91. This multiple increased drastically over the years as capex increased substantially. However, a large portion of the capex spend is going towards growth capex, which should reward shareholders in the future.

Due to the wild change of GAAP earnings (due to costs associated with the acquisition) and free cash flow, we will use the trailing twelve month EV / EBITDA, EV / Sales and Price / Book metrics as valuation metrics to compare the current valuation to historical levels.

The aim is to find the lowest and highest multiple the stock has traded at in the past 5 years. We are using data from the past 5 years, as that covers a diverse range of market conditions including the low interest rate period leading up to the COVID crash, the COVID rally and now the high interest rate, high inflation conditions we currently find ourselves in. From the lowest and highest multiple points of each of the three metrics, we will calculate the midpoint. We can now see the share price gain that would take place if the midpoint of each metric was to be reached again, in other words, if the valuation was to revert to the historical mean.

Now we just have to assign a weighting to each metric and calculate the weighted average of each metric. We will attribute a weighting of 40% to both EV / EBITDA and EV / Sales as these metrics focus on the underlying business profitability and growth in relation to valuation, which is what we primarily want to focus on. We are attributing a 20% weighting to the Price / Book metric as it showcases the value of the underlying shareholder equity and should provide a share price floor going into the future, as it has done historically. We don't see the business trading below book value for a prolonged period of time.

With the current share price of $39.04 and a weighted average sum of 33%, we calculated today's fair share price to be $51.91 ($39.04*1.33).

Now that we have our basis of comparison, we will seek to take the forward multiple estimates of each of the three metrics and compare that to the historical valuation trading range. The forward multiples in conjunction with the historical valuation range of the business can give us a good indication of what the fair value of the share price will be in a year's time, based on our model of mean-reversion. This will take into account analyst expectations of the industry moving forward, macro conditions moving forward, the performance of the business itself on top of the valuation range the market has historically given the business.

With the current share price of $39.04 and a weighted average sum of 55.9%, we calculated our target share price at the end of FY2024 to be $60.88 ($39.04*1.559).

Author's representation based on data from Seeking Alpha

{kind=link}

Our model shows in combination with strong underlying business fundamentals as outlined previously and a significantly undervalued business based on future valuation, there is a strong case to be made for generating a high total return going forward. According to interest rate traders , the Fed target rate reaching 350-375 bps on 18 December 2024 is the highest probability of outcomes. That's a 150 bps drop from the current target rate. This also ties into our thesis of the market rewarding highly indebted companies going forward.

With a current share price of $39.04, risk averse investors can profit from the high IV by writing the 19th January 2024 $50 strike covered calls for a current mid price of $3.10. This strike price is just below the modeled fair value price of today, but with the generated premium, the maximum profit of $53.10 is still above the modeled fair value price of today. This strategy would provide a ~7.9% downside protection. In addition, the annualized return of just the option premium would be 12.9%. If the share price increases above $50 and the shares are called away, the annualized return would still be 45.5%. Combined, the total annualized return would be 58.4% in that scenario.

Risks

There are execution risks. The company must execute exceedingly well on driving synergies between the combined assets, continue paying down debt to improve its balance sheet and lower the interest expense burden. Macro conditions could worsen or continue to be strong headwinds for longer than anticipated. The company is spread rather thin right now and due to its poor balance sheet; it is challenging to allocate further resources, if necessary, to stave off competitors. Industry competitors include Lumentum Holdings Inc, MKS Instruments Inc, Wolfspeed Inc, IPG Photonics Corporation (IPGP), Trumpf, and nLIGHT, Inc. (LASR).

Geopolitical risks are present as the company has a large manufacturing base in the Asia-Pacific region with approximately 18,600 employees located in the region, almost 80% of the global workforce. Export restrictions to China could have a slight impact on the company, with 11% of Q3 FY23 revenue coming from China.

The market could continue to value Coherent significantly below the medium-term mean for an unknown period of time. Valuation dislocation can be present for much longer than anticipated. The market might permanently provide Coherent with a lower than historical valuation. We see this risk as being very minimal however.

The biggest threat to the bullish thesis would emerge if Coherent is unable to maintain a technological leadership due to the debt burden, a major geopolitical event in the Asia-Pacific region occurring, or management missteps in resource allocation and vision. Over the following quarters, strong scrutiny on the execution of synergies of the combined company is required.

Conclusion

The competitive advantages of having strong intellectual property, a diverse product portfolio, technological leadership and deep domain knowledge will fortify the company in this challenging phase of its existence. We find the current share price to be an attractive entry point for investors looking to wait out the short-term noise and position themselves for large sector tailwinds in the medium to long-term. Our mean-reversion model shows strong performance to be made when the market re-values the company. Taking into consideration both the large potential, but also the above average risk, we are assigning a buy rating to the stock.

For further details see:

Coherent: Discounted And Attractive Entry Point For The Medium To Long Term