COHU - Cohu: Challenging First Half In 2023 - Likely Rebound In Second Half

Summary

- Cohu, Inc. revenue continues to drop even as the company heads into historically weaker quarters.

- Gross margin looks like it should be able to hold going forward.

- Cohu projects a slower first half in 2023, with a probable rebound in the second half.

- Its recurring revenue base should provide some support if Cohu stock corrects over the next couple of quarters.

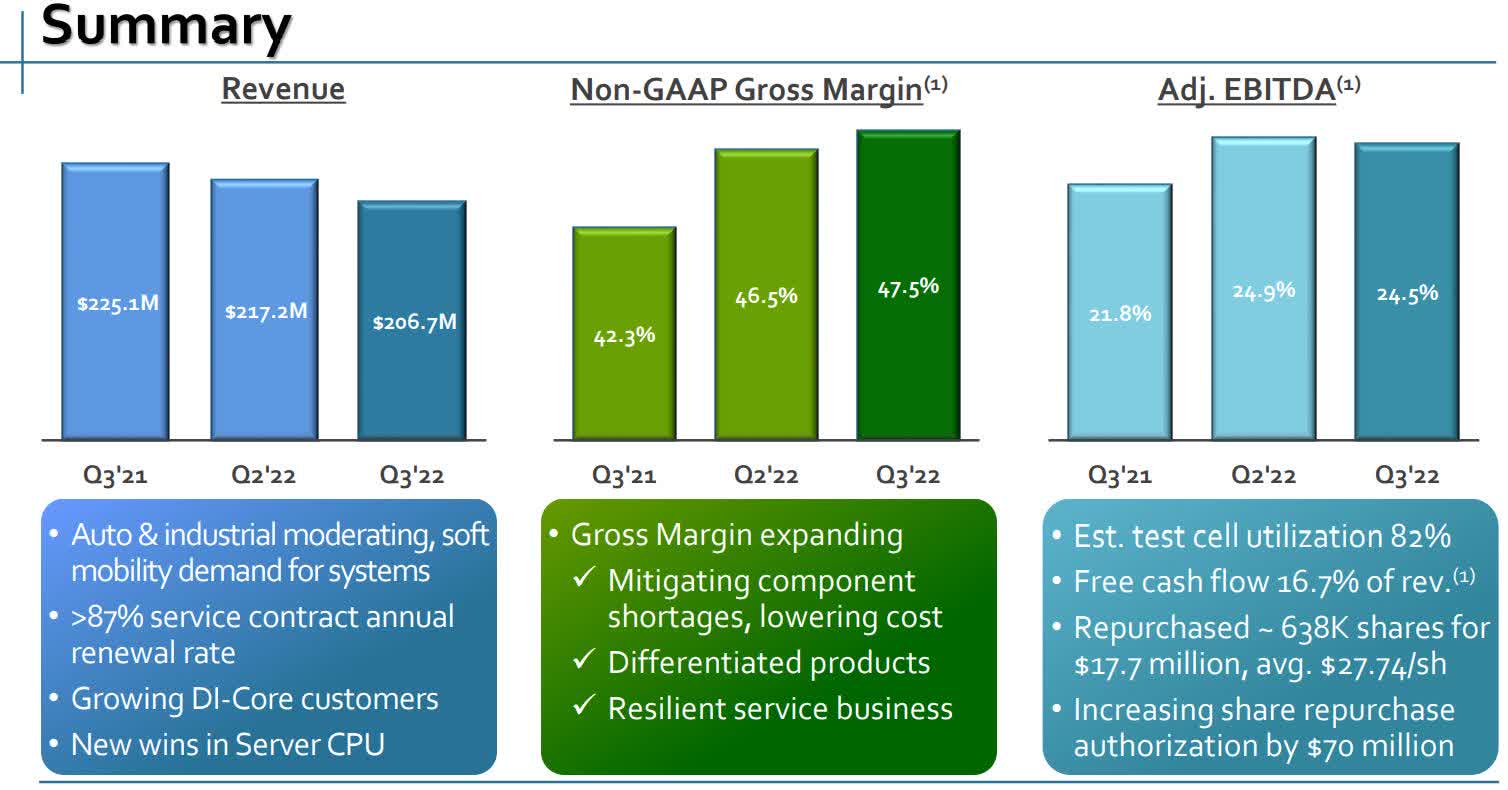

Cohu, Inc. ( COHU ) has had a period of steady revenue decline, falling from $225.1 million in the third quarter of 2021 to $206.7 million in the third quarter of 2022. It guided to drop to a range of $180 million to $198 million, and revenue's probably going to be lower in the first quarter of calendar 2023 because of it being an historically weaker quarter for the company.

What's of concern isn't the typically slower fourth and first quarters of the calendar year, but the fact the company has guided for a weak first half of calendar 2023, which suggests the second quarter is going to be weaker than usual.

While gross margin has been holding up fairly well, if revenue drops further in the second quarter of 2023, it should result in lower gross margin and downward pressure on earnings.

Since Cohu, Inc. believes most of its supply chain issues should be resolved by the end of the first half of calendar 2023, it could point to a rebound in the second half.

In this article, we'll look at some of the numbers from Cohu, Inc.'s last earnings report and why the share price could come under pressure in the first half, and how it could be a tough year if it doesn't get the rebound it's looking for in the second half.

{kind=link}

Recent numbers

Revenue in the third quarter of 2022 was $206.7 million, down about $19 million from the third quarter of 2021. Revenue in the first nine months of 2022 was $621.7 million, down approximately $65 million from the $695 million in revenue generated in the first nine months of 2021.

As mentioned above, Cohu, Inc. revenue in the fourth quarter of 2022 is projected by the company to be in a range of $180 million to $198 million. With the first quarter also being historically weaker, those numbers aren't likely to improve.

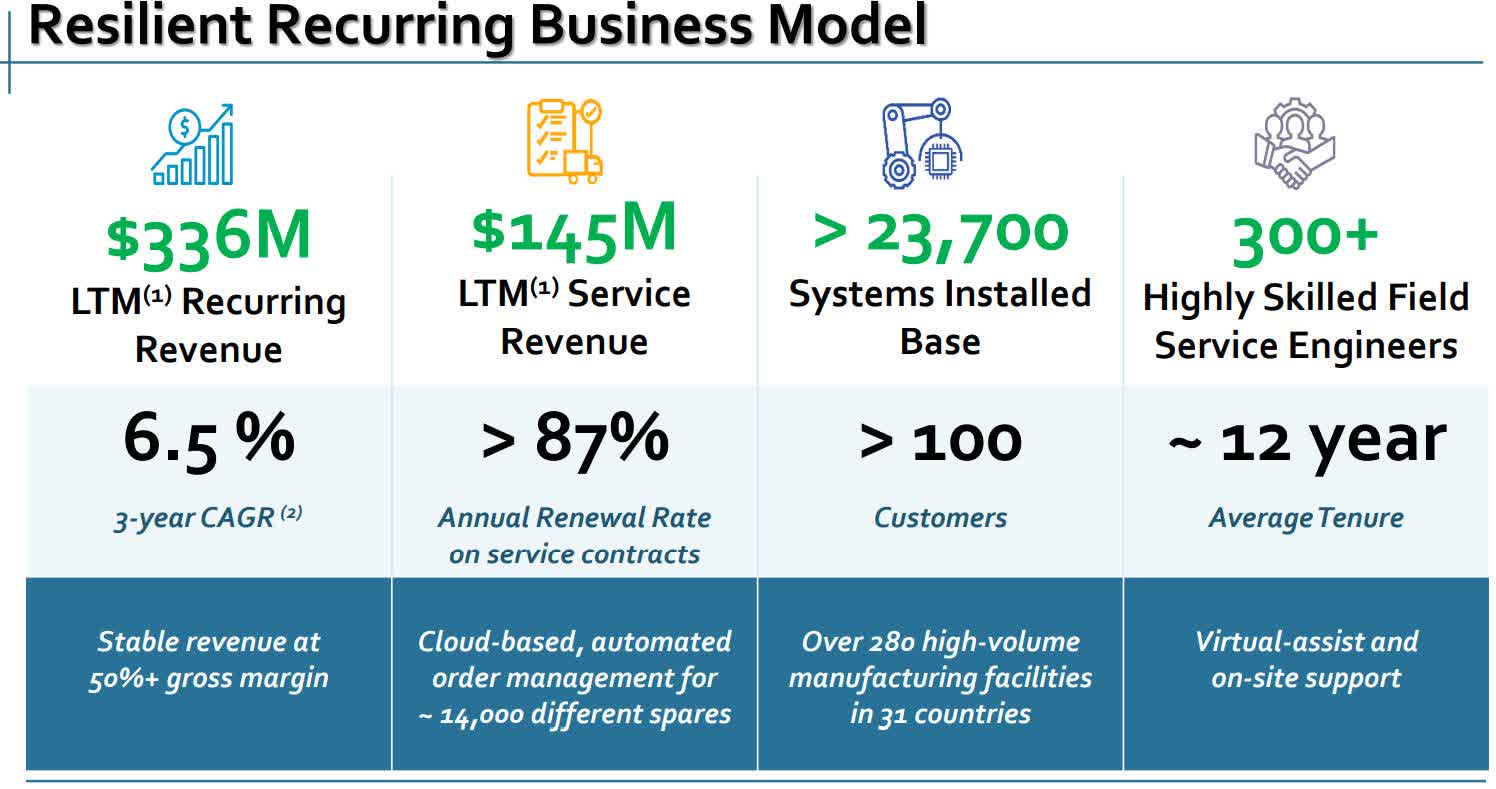

Over the last four quarters, recurring revenue was $336 million or 41 percent of sales. Most of recurring revenue comes from "test contactors and device application kits that are mainly IC design-driven." The catalyst is primarily from the introduction of new semiconductor products from its customer base.

Based upon the probability of lower revenue in the first half of 2023, recurring revenue should help support the floor of the share price if it takes a hit, which I think is how it's going to play out over the next couple of quarters.

{kind=link}

Gross margin in the reporting period was 47.5 percent, up 5.2 percent year-over-year. Based upon lower sales volume and mix, the company expects gross margin in the fourth quarter of 2022 to be at approximately 47 percent.

Adjusted EBITDA in the third quarter of 2022 was 24.5 percent, compared to adjusted EBITDA of 21.8 percent in the third quarter of 2021. Adjusted EBITDA in the fourth quarter of 2022 is expected to come in at about 21 percent.

Net income in the third quarter of 2022 was $25 million, or $0.51 per diluted share. Net income in the first nine months of 2022 was $75.2 million or $1.53 per diluted share, compared to net income of $146.4 million or $3.04 per diluted share in the first nine months of 2022.

Cash and cash equivalents at the end of the third quarter of 2022 was $232.4 million, compared to cash and cash equivalents of $290.2 million at the end of calendar 2021. It had long-term debt of $73 million at the end of the reporting period, down over $30 million from the end of calendar 2021.

A look at gross margin

I think gross margin is probably going to contract some based upon expected lower revenue in the first half of 2023, but the company has taken some steps to keep it at attractive levels.

Gross margin has been improving on a continuous basis as a result of the company moving its contactor manufacturing to the Philippines, lower costs associated with an improving supply chain situation, and the differentiated products it offers in test and inspection of advanced semiconductors.

This is partially offset by cost increases for IC components which had an impact on gross margin of around 130 basis points in the third quarter. The expects this headwind to continue on into mid-2023, albeit at a reduced level based upon assumptions the supply chain continues to improve. In the fourth quarter, the company believes IC costs and lower sales volume and mix will have an impact of approximately 50 basis points on gross margin, and probably for the first two quarters of 2023 as well.

Depending on revenue performance in the first and second calendar quarters of 2023, Cohu, Inc. will probably have further contraction of gross margin, but I don't see the bottom falling out because of improvements in its contactor and handler businesses.

Full-year gross margin for 2022 is expected to come in at about 46.5 percent. With operating expenditures being at close to $52.5 million in the third quarter - slightly higher than the usual $50 million during softer performances, the company will reduce spending if the situation warrants it. If not, the combination of lower revenue, IC, and slightly higher spend could push gross margin down a little more than the market is looking for in the first half of 2023.

{kind=link}

The company has generated compound annual growth rate of 6.5 percent in recurring revenue, accounting for approximately 42 percent of revenue in the third quarter. If it continues to grow at this pace and increases recurring revenue as a higher percentage of total revenue, all things being equal, it should boost gross margin because of the 54 percent gross margin it produces.

Conclusion

There are a number of moving parts to Cohu, Inc. that position it for growth over the long term, but in this article, I wanted to primarily focus on the expected softening market through the first half of 2023. This should result in lower revenue in the first two quarters of the year and the probable contraction of gross margin during that time, although not to the degree it has an extraordinary impact on the performance of the company.

That said, it's possible the economy ends up being worse than expected in 2023, and under that scenario, Cohu, Inc. stock would get punished more than I think it will in the first half of 2023.

My conclusion is Cohu, Inc. is going to lose some of its momentum in the first half of 2023, and if the economy and supply chain continue to improve, it'll start to rebound in the second half.

With that in mind, the share price of Cohu, Inc. is likely to take a hit in the first quarter or two of 2023 before reversing direction. If my thesis is correct, probably the best way to play Cohu, Inc. is to wait for the correction to get an attractive entry point.

For further details see:

Cohu: Challenging First Half In 2023 - Likely Rebound In Second Half