COHU - Cohu: Still Positive On The Recovery Despite Some Weakness Persisting

2023-12-03 22:20:36 ET

Summary

- Cohu's financials show a decline in revenue, but resilient recurring revenue and stable gross margins provide positive signs for potential recovery.

- Weakness in the automotive and industrial sectors continues to impact COHU's performance in the short term.

- Positive signs in the smartphone market and consistent gross margin stability suggest a potential turnaround in the cycle.

Summary

Readers may find my previous coverage via this link . My previous rating was a buy as I believed Cohu ( COHU ) would see an acceleration in growth over the next 2 years, similar to past cycles. I am reiterating my buy rating as I remain bullish about COHU's potential recovery by FY25. While Auto and Industrial weakness might persist for the next 2 or 3 quarters, there are certainly positive signs that suggest a turnaround in other verticals.

Financials/Valuation

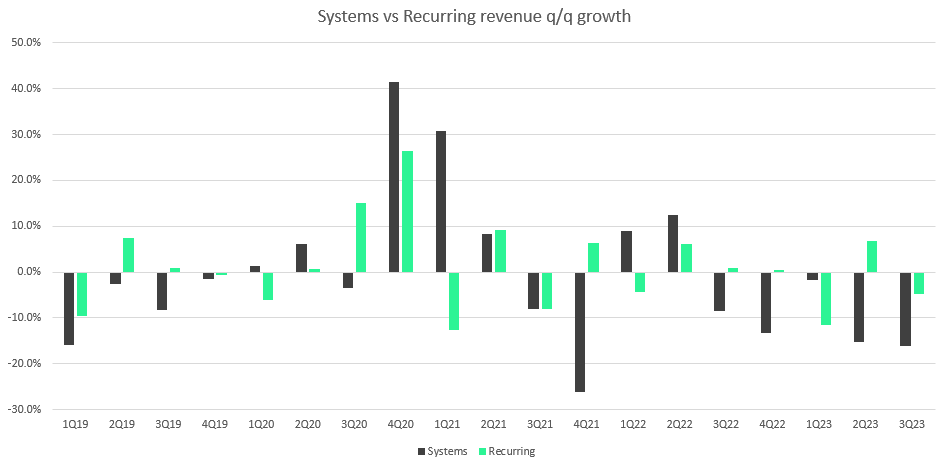

COHU 3Q23 revenue saw $150.8 million, split between Systems revenue of $73 million (down 15% sequentially and 39% annually) and Recurring revenue of $77 million (down 6% sequentially and 11% annually). COHU's strong recurring business and higher-than-expected margin on testers drove non-GAAP gross margin to 47.1%. Non-GAAP EPS came in at $0.35, beating estimates by 10%. While the 3Q23 results were right (tracking my previous FY23 estimates), I am not really happy with the guidance, which signals a potential delay in recovery. Management had anticipated a flat-to-up sequential 4Q23, but it seems like some of the expected demand didn't come through. From the call, we can also infer that more than two of COHU's auto customers delayed their orders until later in 2024.

At the same time, we see some of these customers starting to push out some of the deliveries and some of the orders into 2024 as, as I said in my prepared remarks, auto, and industrial came down, utilization came down about a point in the quarter and I wouldn't be surprised if that doesn't, you know decline, another point or a couple of points in the fourth quarter. Source: 3Q23 earnings

Based on author's own math

Previously, I expected the recovery over the next 2 years to mimic the COHU historical recovery (50% increase from the trough). Now that management is guiding for a 10% sequential decline in 4Q23, I am revising my optimism to a 40% increase (1.4x) by FY25. My assumption implies FY25 revenue of $889 million, down from the previous estimate of $950 million. I have also reduced my margin assumptions to reflect the slower revenue growth. However, I still expect margins to remain at levels above FY21 as COHU's gross margin profitability has improved significantly.

My valuation assumptions remain the same at 16x, as I expect the market to value COHU based on its path to recovery. While the current multiple is at 17.5x, I don't think that is sustainable, as based on history, COHU tends to trade down quickly when it reaches >17.5x.

Comments

Overall, I think my bullish view of the stock remains the same, but I have reset my expectations for the growth recovery timeline. While the guidance for 4Q was not great, there are several positives in the results. Firstly, COHU's recurring revenue was resilient in the quarter. In contrast to Systems revenue, which declined 15% sequentially and 39% annually, Recurring revenue only fell a modest 6% sequentially and 11% annually. Historically, Recurring revenue tends to have lower volatility in sequential growth. Now that Recurring revenue is 51% of total revenue (an all-time high since 2019), I believe this will help with stock valuation as growth becomes less volatile and more visible (recurring nature).

{kind=link}

Secondly, there are a number of positive signs that may suggest the smartphone market is about to trough, even though demand is still low. As an example, there was a 1% sequential increase in Mobility test cell utilisation, which could mean that smartphone component inventories have stabilised. Orders also rose sequentially in the mobility end-market. While one quarter of the data is not enough to establish a trend, it is a good start.

Estimated test cell utilization remained flat quarter-over-quarter at 73% with automotive in industrial down 1 point sequentially, utilization in the consumer segment was 2 points up and mobility increased by 1 point

In fact, mobility, was the only segment across the board that in absolute dollar terms, we saw an increase in orders on the third quarter. Source: 3Q23 earnings

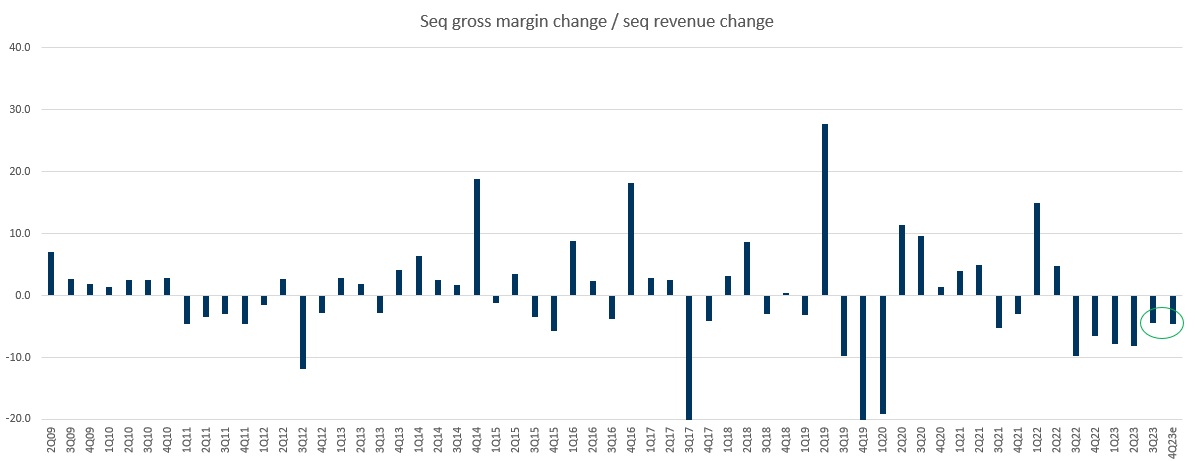

Finally, another positive sign that suggests a trough is near is that COHU's gross margin remains stable. If it were still on a downcycle, I would've expected the gross margin to further erode. In 3Q23, COHU delivered a non-GAAP gross margin of 47.1%, 110bps above management's guidance and also representing the 7th consecutive guidance beat. Looking ahead into 4Q23, while the guide was for gross margin to fall by 110 bps, note that this is against a 10% sequential decline in revenue. The magnitude of the decline is the same when compared to 3Q23, suggesting no major deterioration. Importantly, the magnitude of the decline has improved compared to last year, indicating that the cycle might be turning. Another interesting thing to note is that management 4Q23 guidance effectively implied that COHU's gross margin profit structure has improved significantly. Management's 4Q23 revenue guide at the midpoint is $136 million, and the last time COHU generated this amount of revenue was in 1Q20 ($138 million). Back then, COHU had a non-GAAP gross margin of 42.3%, but 4Q23 is expected to see a 46% gross margin. This tells me that in the next upcycle, profit margins should heavily exceed the past cycle.

{kind=link}

Now for the weakness in the quarter that led me to revise my assumptions. Weaknesses in the Automotive and Industrial sectors continue to persist. The Automotive and Industrial end-markets saw a significant drop in revenue for COHU in 3Q23, falling 38% and 43% qoq, respectively. Additionally, according to management, test cell utilisation is 73%, which is unchanged from the previous quarter. Comparing utilisation rates by segment, we can see that industrial and auto were down 1% sequentially, consumer was up 2%, mobility was up 1%, and compute was down 2% sequentially. System sales are believed to be driven by customers purchasing tools for capacity expansion when the utilisation rate exceeds 80%. On the other hand, when the utilisation rate drops below 80%, management believes that technology upgrades will be the only thing driving the process. Another way to think of this is that there is no "new demand"; upcoming demand will be from the existing base, which means lower growth potential. While I am encouraged by early signs of a potential recovery in Mobility and Consumer, given that, I think the right assumption to make here is that the weakness will persist for the near term (likely through the next 2 or 3 quarters).

Conclusion

While COHU faces ongoing weaknesses in the Automotive and Industrial sectors impacting its short-term performance, my optimism in the company's long-term recovery remains undeterred. Despite the less-than-ideal 3Q23 results and guidance for 4Q23 indicating a potential delay in rebound, there are several positives in the quarter. Notably, COHU's resilient recurring revenue is currently at an all-time high of 51%. Positive signs within the smartphone market hint at a potential trough, evidenced by stabilized inventories and rising orders. Moreover, COHU's consistent gross margin stability, beating estimates for seven consecutive quarters, suggests a potential turnaround in the cycle. However, acknowledging the persisting weakness in key sectors, I've adjusted growth expectations.

For further details see:

Cohu: Still Positive On The Recovery Despite Some Weakness Persisting