COKE - COKE: Double-Digit Upside In 2023 Looking Forward.

2023-09-24 05:42:42 ET

Summary

- Coca-Cola Consolidated (COKE) is the largest bottler in the US with a 120-year history and a significant upside potential.

- The company has seen increases in net sales revenue, gross profit, and operational income despite a decline in case volume.

- COKE's strong brand strength, pricing power, and diverse product portfolio contribute to its solid fundamentals and profitability.

Dear readers/followers,

I've been writing on, investing in, and following Coca-Cola Consolidated ( COKE ) for all of 2023 and more at this point. This business is the largest bottler in the United States - a very good beginning when we look at a business such as this. The company has 120 years worth of history, and at a low valuation, it has a significant upside that's based on some of the more conservative beverage trends you could imagine.

With that, let's see what the current valuation dictates - because fundamentally speaking, not much has changed for this bottler.

It's still a fundamentally sound business.

Coca-Cola Consolidated - a lower upside than back in March of 2023

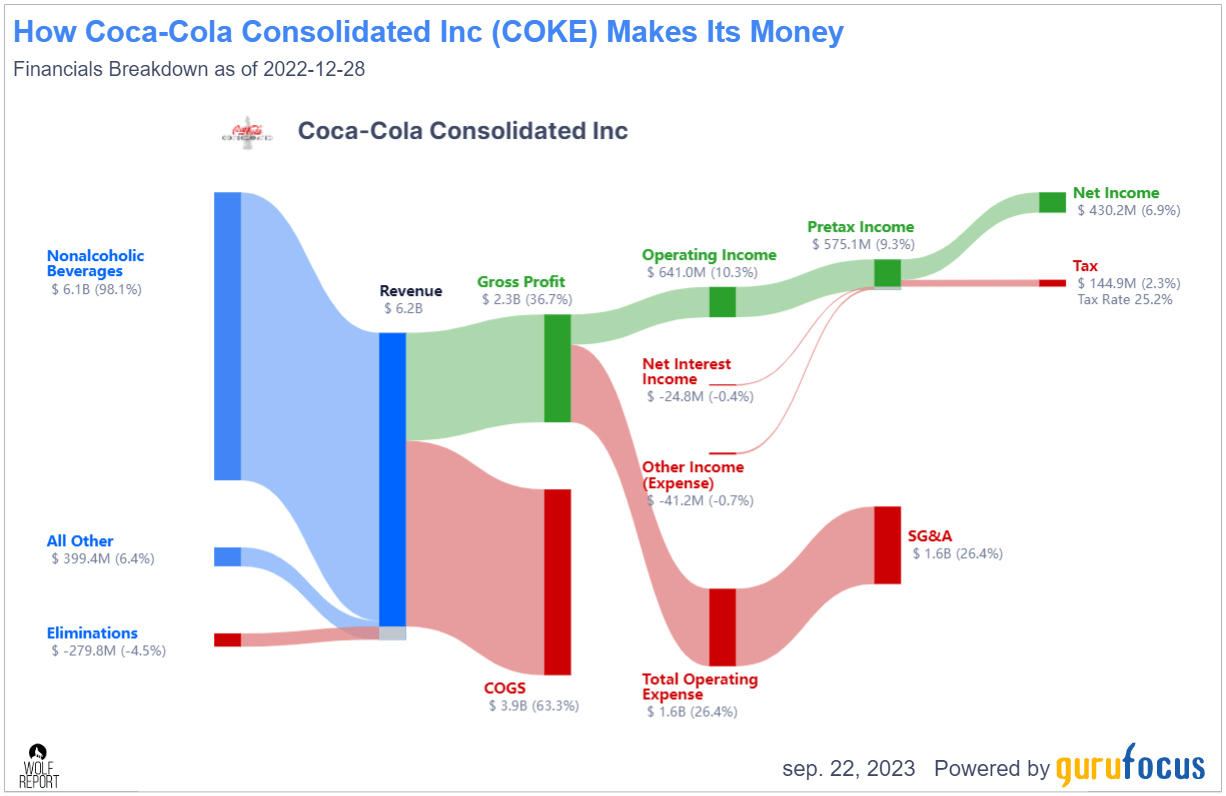

So, since my last article, we have 1H23/2Q23 results to consider. And those results, as we would say in German, they're "worth seeing". We're talking about a 9% increase in net sales revenue and an increase of 22% in gross profit on a YoY basis. This is nothing compared to operational income though, which is up 58%, with a margin improvement of 400 bps in 12 months' time.

How was this possible for the company? How did the company achieve what is a clear, record-level double-digit EBIT margin in the beverage industry, despite what is a standard physical case volume decline of 4% YoY with a decline in the sparkling category. (Source: 2Q23 COKE )

This increase in earnings came despite a significant, 9% increase in SG&A expenses - though declining as a percentage of overall net sales. These increases came from increases in labor costs, inflation, comp, benefits, one-off rewards for employees, and other factors - though the company is expecting this to decline overall going forward into the 3Q23/2H23 period. (Source: COKE IR/2Q23)

Well, much of the answer to the question of profit is relatively simple, as we've seen some of it before. Despite pension plan settlements and other one-off expenses, the company beat on an income basis simply because it increased the price of its product. This increased net sales, by itself, by around $185M - and this is only slightly offset by a decline in case volume during the sales period.

Pricing power is on full display here, and the brand strength for things like COKE is of course significant here.

Remember, what COKE does isn't just Coke itself. Yes, many of the company products that it bottles and sells, indeed has the contract to sell across several geographies in the US, are Coca-Cola ( KO )-based, such as well-known Coke brands, Fanta, Sprite, Pibb, Minute Maid, Mello, Fresca, and Barqs. But the company also works other parts of the segments, selling licensed products from other companies such as Dr Pepper (Diet and non-diet), Sundrop, Dunkin Donuts products, NOS, Reign Products, Full Throttle, and worth considering, COKE is a bottler for Monster Energy ( MNST ). (Source: 2Q23 COKE)

COKE selling is typically associated with exclusive bottling and distribution rights. This is the case with KO products, and it's why a bottler/distributor like COKE is such a powerful business. Because of what COKE can do for one soda brand, it can obviously plug-and-play/offer turnkey solutions for other brands as well.

And COKE has so many advantages to speak of.

Margins? Take a look at the current business model specifics.

{kind=link}

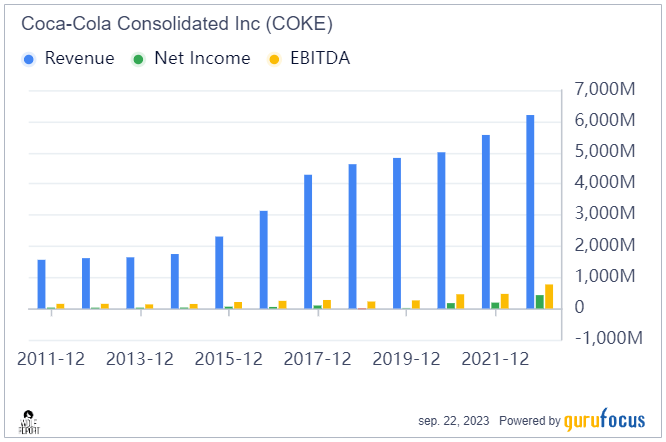

The company remains an above-average beverage player - and those are the 2022 results. The 2023 results so far, as you can see above in the 2Q23 detailing, are even better. We're also taking near-class leading RoE, ROIC and RoA margins, each between 12-48% and qualitative, historical profitability. This company has the sort of "stairstep" model that I look for in terms of net income and revenues.

{kind=link}

In fact, even if KO for some reason lost some of its brand dominance, I remain convinced that COKE could plug its capacity into other brands where needed. And there is no sign that I can see that KO brands are losing significant portions of their market dominance in any one market.

So fundamentals remain rock-solid, and in fact, improving. The recent few quarters have proven beyond a doubt that the company and the associated brands have the strength to move forward in confidence in terms of pricing power here.

The one disadvantage remains the company's absolute lack of a dividend. It's a snail's pace, and it's not going up anytime soon again. Because of that, investing in COKE requires the realization that you're not going to become rich by way of dividend payouts. Rather, your returns are decidedly oriented towards the capital side of things.

COKE is a margin leader and a return leader, or close to it, amongst most KPI's in the beverage industry. Its return on equity, which is considered a measure of a corporation's profitability and how efficient it is in generating profits, shows us a position in the 98th percentile in beverages. This is close to a class leader, and for the notoriously difficult beverage industry, this is something to really home in on.

There's also no shift in fundamental ratings. COKE is BBB+ rated, and I don't see any potential headwinds that have the power to derail this company on a fundamental level. This is the lowest-yielding company I invest in , barring the few investments I have that do not pay a dividend at all. This should show you that I have no problems investing in lower-yield stock, provided I can get on board with the thesis for returns for the company. (Source: 2Q23 COKE)

Since my last article, we've seen some softness from COKE, declining below the $700/share level again. To me, this seems mostly like macro noise, not something specific as to the risk of the business.

Both an advantage and a bit of a risk, which I also touched upon in my first article on the company, is the company shareholder structure. Over 40% of the company is actually held by insiders. Usually, this is a positive, but in this case, it also means that management has very little incentive to, for instance, bump the dividend. That's not the end of the story either. While over 40% is held by insiders, a full 71% of voting power is held through your typical voting-heavy B-class shares, which isn't unusual, but always something to look closer at here.

I like motivated ownership. But in this case, I actually consider the ownership concentration to remain one of the major risks to the business , and what's preventing the dividend from rising here?

Still, valuation shows a compelling continuing thesis, and that's what I'm going to look at and present to you here.

COKE - The Upside remains at least in the double digits

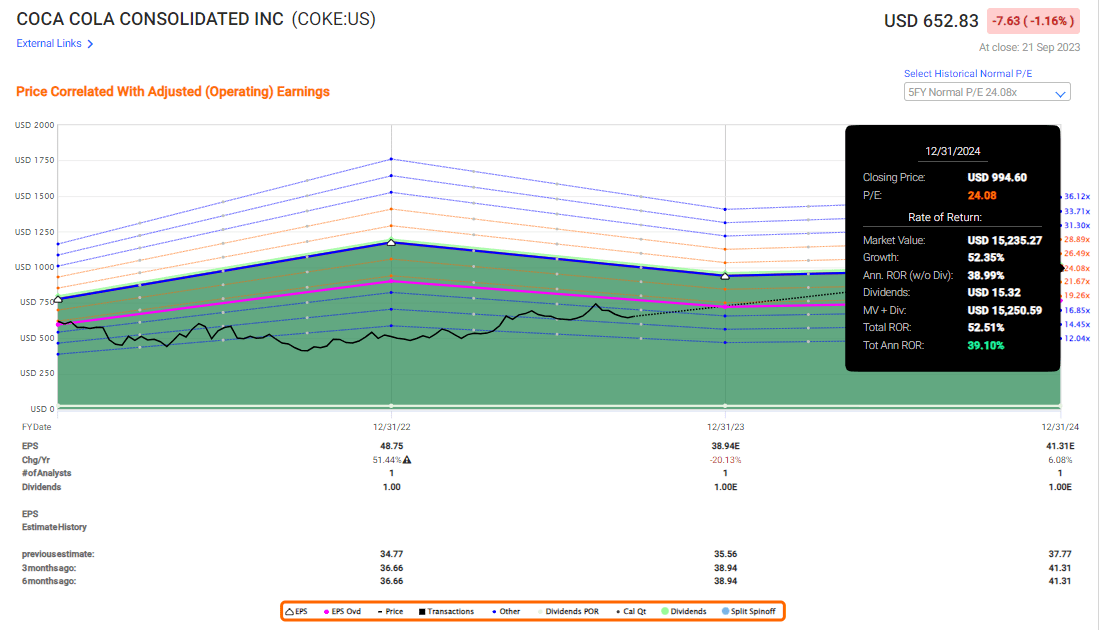

So, in my last article, I made it clear to you that my PT for COKE is at $690/share. If you kept an eye on the share price, you would notice that there was a certain time in the last 3 months when the company would have been considered a "HOLD" for me. I did not update at the time, but there was indeed that time when the company was best considered a "HOLD".

Now it's back down below $690/share, and that means that the upside looks as follows.

Because we're now expecting an EPS decline roughly to the tune of -0.65% per year, that means our 15x P/E forward estimate is no longer at a positive annualized RoR. We require the maintaining of a 20-24x P/E premium to see a market-beating upside for this company here. If you accept the market premium on a 5-year basis, then this is what you could expect from COKE from here on out.

{kind=link}

But this is nearly a $1,000 PT for this to materialize in a realistic way - so it might not happen as expected. A more conservative future estimate, as I usually tend to do, would put this company at more of a 25% annualized upside to a 20x P/E on a forward basis - and this is something I still consider realistic here.

This isn't the biggest, nor the most yielding company. We're still only at a yield of 0.3%. But with a company beating estimates almost half the time with a 10% margin of error on a 1-year basis (Source: FactSet), we're in a strong position to see continued upside for the company here.

A 19-20x P/E rating comes to around $800/share with these new targets. While I won't be bumping my PT to $800/share to reflect this new 20x P/E reality, I have already bumped it to around $690/share, which implies at least 17-18x P/E. At 17-18x, the upside is still over 15%, and that's where my minimum requirement for investing in a business lies.

I remind you that COKE has already delivered what I spoke about in some of my initial articles. At that point, I forecasted the company to rise above $650/share. I do believe it has the potential to go higher, but some of the upside you may read about in my earlier articles, well that upside is something we've already seen at this point.

So the future isn't as bombastic for COKE as the recent 8 months have been - but there's still upside to be had in this conservative beverage company.

As always, I focus on investing in quality and safety. COKE certainly qualifies as quality and safety, and for that reason, I neither shift my target nor shift my stance - at least not yet.

Here is my current thesis.

Thesis

- COKE is an advantageous soft drink/beverage investment with bottling and manufacturing capacity across 5 attractive US regions. This makes the company a "guaranteed cash cow", "with exposures to things like input inflation, CapEx, and risks associated with companies like this - including customer concentration.

- However, the company has a superb track record of delivering value to its shareholders, almost quadrupling KO 20-year returns, and is well managed, even if its dividend leaves something to be desired.

- After outperforming in 2022 and a 40% ROR since my last article, I am now bumping my price target on this attractive bottler.

- At a premium, I still view COKE as a worthy "Buy" with a 17X P/E long-term target, indicating a PT of $690/share. I refuse to shift my PT down here - I view the trends as longer-term noise.

- Because of that, I'm going with a "Buy" here as of September of 2023.

Remember, I'm all about:

1. Buying undervalued - even if that undervaluation is slight and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

2. If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

3. If the company doesn't go into overvaluation but hovers within a fair value or goes back down to undervaluation, I buy more as time allows.

4. I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them (italicized).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside based on earnings growth or multiple expansion/reversion.

COKE fulfills every single one of my investment criteria except that I can no longer in good conscience call it cheap.

For further details see:

COKE: Double-Digit Upside In 2023, Looking Forward.