CL - Colgate-Palmolive: A Better Year Ahead (Rating Upgrade)

2023-12-20 13:29:47 ET

Summary

- Colgate-Palmolive Company is in a very good position to improve its margins over the course of next year.

- Even though the market is already pricing in such an improvement, the right conditions are in place for the company to exceed expectations.

- From a dividend and free cash flow point of view, Colgate-Palmolive also looks attractive as we head into 2024.

Colgate-Palmolive Company (CL) delivered a total return of almost 41% over the past 5 years, which is equal to a 7% return on an annualized basis.

For a low beta stock, this is not a bad performance, but considering that CL has lagged behind the Consumer Staples Select Sector SPDR® Fund ETF (XLP) in recent years, it is reasonable to expect dissatisfaction among shareholders.

After being neutral on the stock for most of 2023, I can't help but notice that as the stock continues to be rangebound, business fundamentals are gradually improving.

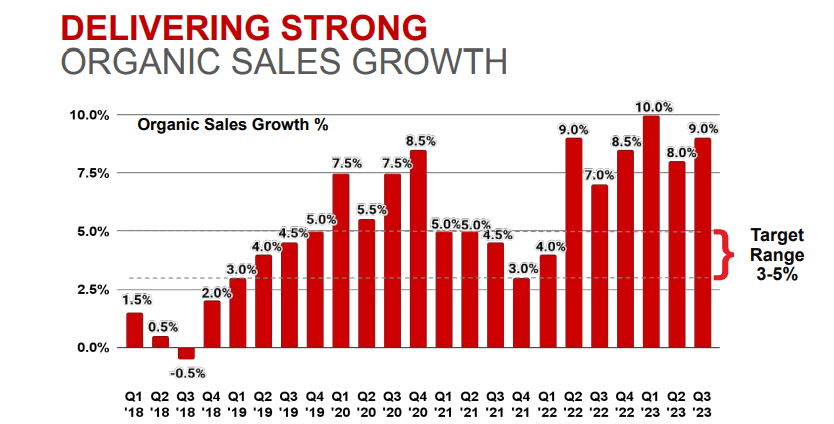

When I say that, I don't mean the company's top-line growth, which has been very high for a company the size of Colgate.

{kind=link}

Instead, what I focus on is Colgate's gross margin, which I recently called "the only game in town" . As impressive as double-digit quarterly revenue growth for Colgate might sound, it is largely a reflection of the company's pricing initiatives in response to the prices of raw materials.

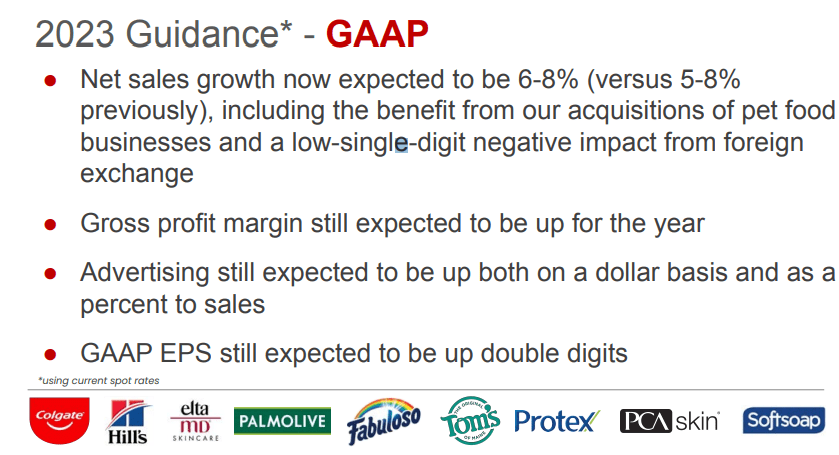

On a GAAP basis, top-line growth is expected to come within the range of 6% to 8% for the whole fiscal year, but this is likely to come down in 2024 as the impact of pricing fades away.

{kind=link}

The more important part of the guidance shown above is the line related to gross margin and its expected increase for the year. As one of the most important metrics for Colgate-Palmolive, I expect gross margin to improve in 2024 and with that to provide much-needed support for the share price.

Gross Margin Headed North

This summer, I went into all the detail on why gross margin is the key metric not only for Colgate-Palmolive, but for large consumer staple businesses more broadly.

Improving gross margin remains the only game in town for future shareholder returns.

Source: Seeking Alpha.

I called the gross margin for CL the "only game in town," and as it fell to one of its lowest levels since 2011, it was no surprise that the stock has been lagging behind other peers in the sector.

prepared by the author, using data from SEC Filings

As dramatic as the graph above might look, we should keep in mind that the scaling goes from 50% to 62%, which magnifies annual movements in gross margin. Moreover, in spite of the decline in recent years, Colgate-Palmolive remains one of the most profitable entities in the industry.

Seeking Alpha

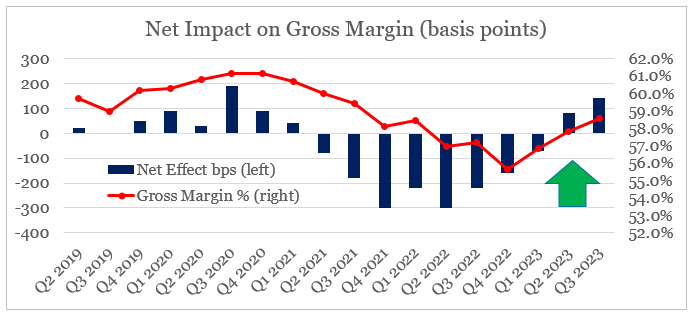

As we can see from the graph below, margin headwinds for Colgate have been dissipating in recent quarters, and with that gross margin has increased from 55.6% in the last quarter of 2023 to 58.6% during the last reported one.

{kind=link}

By breaking down the three key drivers of gross profitability, we could see that it was the rising costs of raw materials in 2022 that caused the large drop. The negative impact from rising input costs, however, is already fading, and we are slowly returning to more normal levels.

prepared by the author, using data from Earnings Releases

At the same time, pricing and productivity improvements are falling at a slower pace, which creates the positive dynamic for gross margin that we saw on the previous graph.

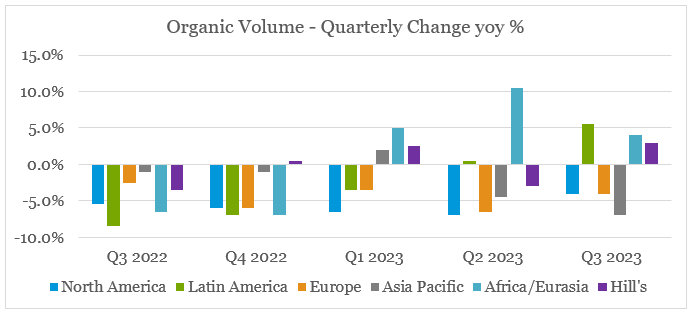

Volumes, on the other hand, have suffered following the price increases in 2022, but they are also slowly returning to normal with Latin America, Africa/Eurasia, and Pet Food segments already in positive territory.

{kind=link}

All that creates the necessary conditions for Colgate-Palmolive's gross margin to return to its high in the coming year. The bad news is that the market is already expecting that, and that is why CL's sales multiple stands at elevated levels, which implies an annual gross margin within the range of 58% to 59%.

prepared by the author, using data from SEC Filings and Seeking Alpha

Given the fact that volumes are slowly normalizing, however, I expect positive pricing and productivity impacts on gross margin to be sustained in the near term, which could lead to gross margin improvements exceeding current expectations. Coupled with the elevated top-line growth, this could have a double whammy effect on the share price, with an upward multiple repricing and higher absolute value of sales on profits in 2024.

Possible Dividend Increases

At first glance, CL appears very unattractive as a dividend stock. To begin with, the current forward yield of 2.46% is quite low when considering the current yield on long-dated Treasuries. It also sits below the industry median, which is already quite low to begin with.

Seeking Alpha

In terms of dividend safety , things are not looking good either, and with a payout ratio of nearly 100%, it appears that future dividend increases are wishful thinking.

Seeking Alpha

The company, however, recorded a very large impairment charge in the last quarter of 2022 related to the recent large acquisition of Filorga.

During the fourth quarter of 2022, we recorded a non-cash charge of $721 pretax ($620 after tax) to adjust the carrying values of goodwill and intangible assets related to the Filorga skin health business . The impairment was due primarily to the continued impact of the COVID-19 pandemic on the Filorga business, particularly in China, as a result of government restrictions and reduced consumer mobility, which negatively impacted consumption in the duty-free, travel retail and pharmacy channels, and the impact of significantly higher interest rates.

Source: Colgate-Palmolive 10-K SEC Filing (emphasis added).

The good news here is that by simply lapping the fourth quarter of 2022, the GAAP payout ratio would improve considerably, and I see a dividend increase next year as a highly likely scenario. The bad news, of course, is that apparently Colgate-Palmolive did overpay for its large acquisition of Filorga.

I am not surprised by this development, and I was expecting problems with the large acquisition of Filorga all the way back in 2020.

Smaller size acquisitions are usually a much better choice to enter the category as integration is usually smoother and the acquirer is not overpaying for an already well-established business.

Source: Seeking Alpha .

On a free cash flow yield basis, Colgate is now approaching more attractive levels prior to 2021. The current yield of 4% might not look attractive at first, but we should also consider the potential for free cash flow improvements next year, on the back of the high expected sales growth and the potential for margin improvement.

prepared by the author, using data from SEC Filings

Furthermore, CL's capital expenditures are currently at multi-year highs relative to the company's sales as capacity expansion and restructuring in pet food continues.

prepared by the author, using data from SEC Filings

Over the coming years, this should also normalize, which would create yet another tailwind for free cash flow.

Conclusion

After a disappointing 2-year period, Colgate-Palmolive Company is now in a good position to outperform its peers in 2024. The strong brand portfolio and Emerging Markets exposure allow for sustained price increases as raw material costs are returning to normal. This should have a positive impact on margins over the next year, while not sacrificing volume growth. On a free cash flow basis, things are also looking good, and I see a dividend increase to be in the cards for 2024 as well.

For further details see:

Colgate-Palmolive: A Better Year Ahead (Rating Upgrade)