CL - Colgate-Palmolive: A Healthy 7% Return With A Safe Dividend For Investors In A Post-Pandemic World

2023-08-16 08:15:25 ET

Summary

- Colgate-Palmolive's ability to maintain or increase selling prices as needed is a testament to its strong brand and pricing power.

- Colgate-Palmolive has a strong global presence, with subsidiaries in numerous countries, indicating a diversified risk profile.

- Colgate-Palmolive has a robust dividend history, with a forward annual dividend yield of 2.53% and a payout ratio of 64.19%.

- Colgate-Palmolive’s current price allows for a 7% return based on a conservative discounted cash flow analysis.

Investment Thesis

I'm attracted to the Colgate-Palmolive Company (NYSE:CL) for the following reasons. First, the company's ability to adjust selling prices showcases its strong brand and competitive edge. Second, its global operations diversify risks and balance economic shifts. Third, a 2.5% forward annual dividend yield reflects a commitment to shareholders. Lastly, the current stock price of $76.90 seems to offer a safe 7% return.

Company Overview

Colgate-Palmolive, a household name synonymous with oral care products, is more than just a toothpaste company that we are all aware of. It is a global conglomerate with a diverse portfolio of products that extend beyond oral care to personal and home care, as well as pet nutrition. The company's commitment to sustainable growth, innovation, and its stable business model make it a compelling investment opportunity in the current market scenario.

Colgate-Palmolive's business strategy is tightly focused on two product segments: Oral, Personal and Home Care; and Pet Nutrition. These segments are not only resilient but also have strong growth potential. The company's strategy to grow these key product categories and increase its overall market share has been successful, as evidenced by its strong financial performance and market leadership in various product categories.

Leveraging Brand Strength for Pricing Power

Colgate-Palmolive's ability to maintain or increase selling prices, even in the face of inflationary pressures, is a testament to its strong brand and pricing power. In my opinion, this is a significant competitive advantage that not all companies possess, and it speaks to the strength and resilience of Colgate-Palmolive's business model.

When we consider the financial data. Despite the challenging economic environment, Colgate-Palmolive has demonstrated robust financial performance. The company's revenue for the last twelve months ((LTM)) stood at $18,338 million , reflecting a healthy growth rate of 8.4% year on year (YoY). This growth is partly attributable to the company's ability to pass on increased costs to consumers through higher selling prices without significantly impacting demand for its products. Moreover, the company's net margin remained relatively stable at 15.6% in FY 2022, compared to 16.2% in FY 2021 , indicating that it has been able to manage cost pressures effectively.

I also believe the quality of Colgate-Palmolive products also supports its pricing power. The company owns a portfolio of well-known and trusted brands, including Colgate, Palmolive, and Hill's, among others. These brands have a strong presence in households worldwide, and consumers are often willing to pay a premium for products they trust and value. This brand strength is a key factor that enables Colgate-Palmolive to increase prices without losing market share.

Furthermore, Colgate-Palmolive's extensive global distribution network is another factor that contributes to its pricing power. The company's products are available in over 200 countries and territories, providing it with a broad and diversified customer base. This global reach allows the company to balance out regional economic fluctuations and maintain stable pricing.

In addition, Colgate-Palmolive's continued investment in research and development (R&D) and marketing helps to reinforce its brand strength and pricing power. By continually innovating and improving its products, the company can justify price increases and I believe it will help to maintain or potentially improve customer loyalty. At the same time, effective marketing campaigns will continue to help enhance brand awareness and perception, further supporting the company's pricing strategy.

Harnessing Global Presence for Risk Diversification

Colgate-Palmolive's extensive global presence, with subsidiaries in numerous countries indicates a diversified risk profile. This international diversification not only provides the company with a broad and varied customer base but has historically helped to mitigate risks associated with economic fluctuations in any single market as seen during the global financial crisis of the late 2000s where the company continued to grow earnings per share ((EPS)) at a double digit rate unlike other S&P 500 companies.

In North America, the company's net sales for Oral, Personal and Home Care were $3,511 million in 2022 . For Pet Nutrition, the net sales in the U.S. were $2,432 million in the same year. This indicates a strong market presence in the U.S., which is one of the largest consumer markets globally. The company also has a strong market presence in large consumer markets in Europe, such as the United Kingdom, France and Italy in addition to other major emerging markets across Asia, Africa and South America such as India, Brazil and Kenya.

{kind=link}

This geographical diversification of revenue streams allows Colgate-Palmolive to mitigate risks associated with economic downturns or other adverse conditions in any single country or region. It also provides the company with the opportunity to benefit from growth in emerging markets. The IMF projects that emerging markets are expected to grow by 4.1% in 2024, as opposed to 1.4% growth for advanced economies. This is driven by factors such as a younger population, increasing urbanization, and rising middle-class consumption in these markets. By already being established in many of these emerging markets, I believe this positions Colgate-Palmolive perfectly to capitalize on this growth.

International Monetary Fund

Moreover, the company's ability to adapt its product offerings to cater to local tastes and preferences in different countries is an underrated aspect which further strengthens its global position. This adaptability, combined with the company's strong brand recognition and extensive distribution network, contributes to its robust financial performance on a global scale.

A Dividend Aristocrat with a Safe Balance Sheet

Colgate-Palmolive is one of the most remarkable dividend paying companies I have come across. The company has paid uninterrupted dividends since 1895, demonstrating over a century of commitment to its shareholders. What I think is even more impressive, is that Colgate-Palmolive has increased its dividend payments for the past 60 consecutive years.

Despite the impressive history, I wanted to check to make sure the dividend Colgate-Palmolive pay is sustainable, so I have assessed the safety of the by examining its payout ratio, which is the proportion of earnings paid out as dividends. The business produced net income for the last twelve months ((LTM)) as of Q2 2023 of $1.598 billion . Since Colgate-Palmolive's payout ratio is 64.19%, this indicates that it returned over half of its earnings to shareholders, while still retaining a significant portion for reinvestment.

A review of the company's balance sheet further underscores the safety of its dividend. The company's cash and cash equivalents have increased from $775 million at the end of 2022 to $867 million as of Q1 2023 . This increase in cash reserves provides the company with additional financial flexibility and further supports its ability to meet its short-term obligations, including dividend payments. The company's long-term debt stands at $7,699 million and as of Q1 2023, Colgate-Palmolive's current ratio is 1.1, indicating that it has enough assets to cover its short-term liabilities.

Financials

As I mentioned, Colgate-Palmolive has a reasonably solid balance sheet with an impressive dividend history. The rest of the company's financials, like the CL's dividend have also been solid over the past five 5 years. Its revenue has shown steady growth, increasing from $15,544 million in 2018 to $18,676 million in the last twelve months ((LTM)) . The earnings per share ((EPS)) has been a bit more volatile, with the current EPS being $1.80, down from the high of $3.14 in 2020.

DJTF INVESTMENTS

The stability of CL's business model is well reflected in its Free Cash Flow ((FCF)), with LTM FCF being $2.356 million, which is roughly in line with the FCF from 2018 of $2.620 million, which is a testament to the company's ability to generate FCF despite the challenging economic conditions we have experienced over the last few years. The robust nature of Colgate-Palmolive's FCF during difficult economic environments give me confidence the company will continue to generate an impressive amount of FCF into the future.

DJTF INVESTMENTS

Regarding the short term of Colgate-Palmolive, particularly their upcoming quarterly earnings results, I anticipate the company will continue to improve on the 3 priorities which they outlined for the year, being increasing sales growth, increasing brand investment and improving earnings. I expect that this will be reflected in improving margins, increased revenue and accelerating EPS growth. Given that the most recent earnings release was promising in my opinion and management felt confident in improving their outlook for 2023, I fully expect the company to deliver on their 2023 outlook. I will be particularly eager to see management deliver on their Non-GAAP EPS outlook of $3.00 to $3.15 per share given that this saw significant declines resulting from inflation.

Valuation

As of August 2023, Colgate-Palmolive stock has underperformed the S&P 500 having declined 2.8% year to date compared to the 17.0% returned by the S&P 500, suggesting that CL stock may be undervalued compared to the rest of the market due to recent price action.

When considering valuation, I always consider what we are paying for the business (the market capitalization) versus what we are getting (the underlying business fundamentals and future earnings). I believe a reliable way of measuring what you get versus what you pay is by conducting a discounted cash flow analysis of the business as seen below.

{kind=link}

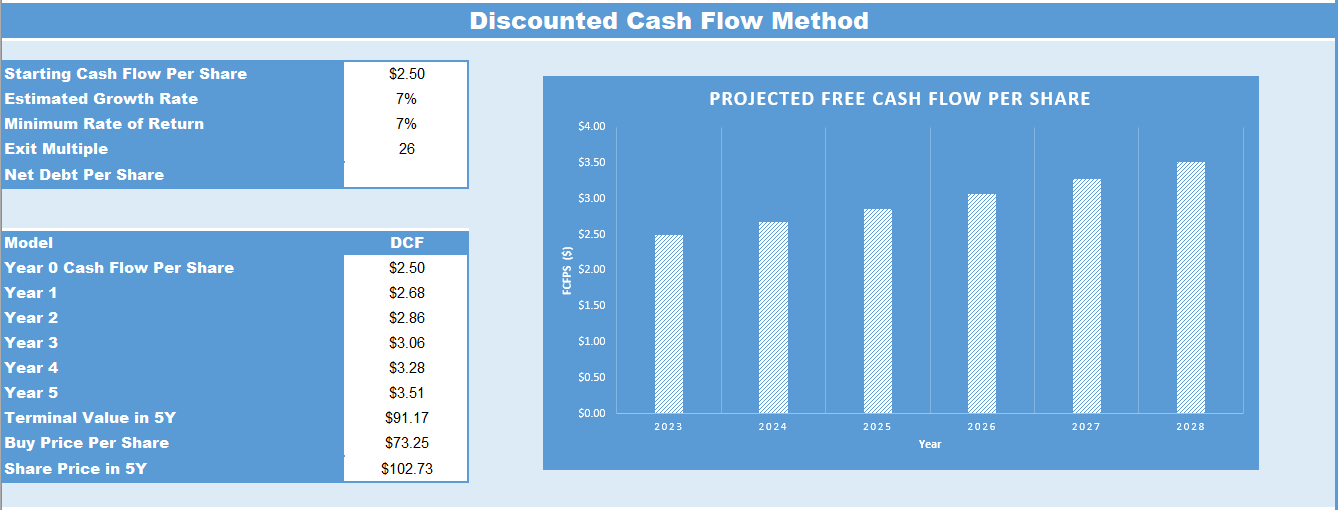

First, I looked at the company's historical growth rates. I analyzed the company's free cash flow over the past several years to understand the trend and the rate at which it has been growing. This gave me a sense of how the company has been performing and what kind of growth it has been able to achieve in the past. I also factored in analyst estimates growth rate of 7.0% per annum for the next five years.

I am aware that both historical growth rates and analyst estimates have their limitations and generally use them as an upper limit when determining the growth rate to apply.

I also wanted to ensure that I was using a reasonable starting point for the company's free cash flow when doing my DCF. I decided to take a different approach than I typically do for DCF models by normalizing free cash flow ((FCF)) to a number which better reflects typical cash flow of the past ten years.

Instead of using the FCF from FY2022, I chose to use a normalized free cash flow per share of $2.50 per share. By using a normalized figure, I aimed to smooth out one-time events that have affected the company's free cash flow in FY2022 such as the merger and restructuring charges and asset write downs.

In my view, using this normalized free cash flow per share of $2.50 provides a more accurate and conservative starting point for projecting the company's future cash flows. It's more in line with the company's historical performance and, I believe, provides a more realistic basis for estimating the company's intrinsic value.

After conducting my discounted cash flow ((DCF)) analysis on Colgate-Palmolive, I arrived at a buy price of $73.25 per share. Based on the 7% growth rate and the 7% discount rate applied to this valuation, this would imply a share price of $102.73 per share in 5 years. The current share price is $76.90, therefore investors can expect to achieve an annual compounded growth rate of 7% based on this DCF analysis given the company's projected cash flows and long-term stability and resilience.

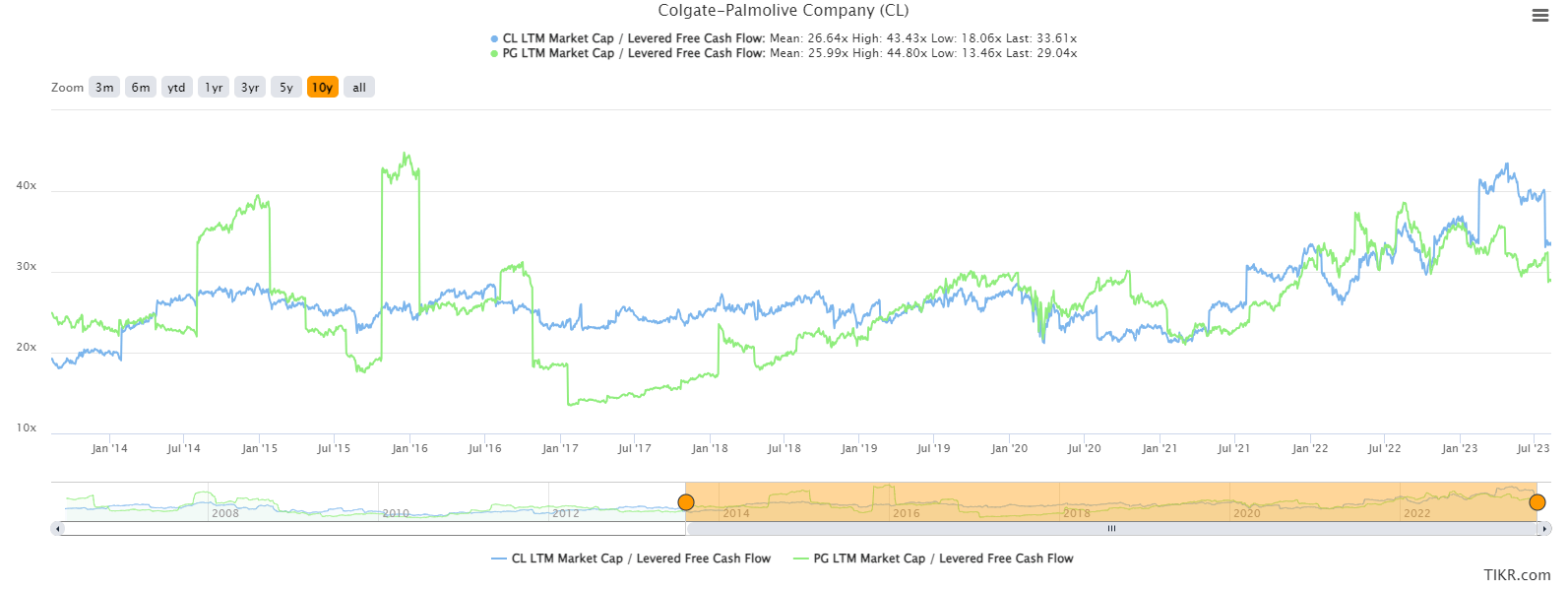

As seen below, when conducting a peer comparison of Price/Free Cash Flow ratio trends between Colgate-Palmolive and Procter & Gamble of which each are competitors in the consumer staples industry, it is clear that both businesses have historically traded at similar valuations. Currently, Colgate- Palmolive is trading at a slightly higher multiple, however this is likely due to one-time events that have affected the company's free cash flow in FY2022 such as the Merger and Restructuring Charges and Asset Write Downs. Once these one-time expenses have been accounted for, both businesses trade at very similar valuations and offer a comparable risk/reward profile.

{kind=link}

Risks

Large multinational competitors such as Johnson & Johnson, Unilever and Oral-B (much like Colgate-Palmolive) have extensive financial resources, broad product portfolios, and established distribution networks. As a result, I believe there to be a risk of them leveraging their scale and operational efficiencies to potentially undercut Colgate-Palmolive on price, invest heavily in marketing and product development, or negotiate favorable terms with suppliers and retailers.

On the other hand, the rise of digital marketing and e-commerce has lowered the barriers to entry allowing smaller players to reach consumers more directly and cost-effectively. These smaller scale companies often have a deeper understanding of local consumers, enabling them to tailor their products more effectively. They also tend to be more agile and innovative, therefore enabling them to quickly adapt to changing market trends and consumer behaviors.

This competitive landscape could exert pressure on Colgate-Palmolive's market share. If competitors are able to offer similar products at lower prices, or if they are more successful in innovating and meeting consumer needs, Colgate-Palmolive could lose market share.

Colgate-Palmolive, like many companies in the consumer goods industry, relies heavily on a variety of raw materials such as calcium carbonate, fluoride, plastic, and cardboard to manufacture its products. We have seen in the past, the prices of these materials fluctuate due to factors, including changes in supply and demand, geopolitical events, natural disasters, or shifts in global trade policies.

When commodity prices rise, it increases the cost of goods sold for Colgate-Palmolive. If the company is unable to pass these increased costs onto consumers in the form of higher prices, it could result in a squeeze on the company's gross margins. This could subsequently impact the company's profitability and its ability to invest in other areas of the business such as research and development, marketing, or capital expenditures. Even if the company is able to pass on some or all of the increased costs to consumers, it may still face a lag between the time the costs are incurred and when the price increases take effect. This could temporarily impact the company's margins and cash flows.

Another risk is currency exchange rate risk. The company generates approximately 74% of its revenues outside of North America . Therefore, if the U.S. dollar strengthens against these foreign currencies, the value of these revenues and profits in U.S. dollar terms would decrease, potentially impacting the company's reported financial performance. Conversely, a weakening U.S. dollar could inflate the U.S. dollar value of foreign revenues and profits. While the company may use financial instruments to hedge against some of this risk, it cannot eliminate it entirely.

Conclusion

I'm drawn to Colgate-Palmolive for several compelling reasons. Firstly, I'm impressed by the company's ability to maintain or increase selling prices as needed, a clear testament to its strong brand and pricing power. This ability is a significant competitive advantage that speaks volumes about the robustness of Colgate-Palmolive's business model. Secondly, I appreciate the company's extensive global presence. With operations in numerous countries, Colgate-Palmolive has a diversified risk profile that allows it to balance regional economic fluctuations. Thirdly, I value the company's robust dividend history. With a forward annual dividend yield of 2.53% and a payout ratio of 64.19%, it's clear that Colgate-Palmolive is committed to returning capital to its shareholders. Lastly, based on my conservative discounted cash flow analysis, I believe that the current stock price of Colgate-Palmolive offers a 7% annual return over the next five years.

For further details see:

Colgate-Palmolive: A Healthy 7% Return With A Safe Dividend For Investors In A Post-Pandemic World