CL - Colgate-Palmolive: Dividend King With Limited Growth

2023-09-27 12:03:33 ET

Summary

- Colgate-Palmolive's dividend has been increased for 60 consecutive years.

- The company is well-positioned to mitigate inflationary pressures through price adjustments, volume optimization, and improved operational efficiency.

- Colgate-Palmolive's sideways price movement for the last decade makes it hard to recommend.

Thesis

When most people hear of Colgate, they typically first think of toothpaste since that is what the brand is most known for. Toothpaste aside, CL has seen some excellent growth in Latin America and I believe the current momentum of organic sales growth puts CL is an interesting position. The Colgate-Palmolive Company ( CL ) is in a strong position for increased revenue growth driven by strategic initiatives including price hikes, results-driven marketing, and products that continue to sell no matter what the economy is doing. Colgate's solid performance as a divided growth stock also reinforces why it's a great company to consider adding to your portfolio if you are looking for some reliable dividend income.

I want to really like Colgate but the lack of price growth over the last decade really makes this a tough stock to recommend if you are an investor that values total return. Colgate has managed to increase their dividend payouts for 60 consecutive year which makes them a dividend king. Despite this, the low starting yield of 2.6% and lack of price growth means you are likely to underperform the market.

Portfolio - South America Momentum

Colgate's Investor Presentation

{kind=link}

With a wealth of products in CL's portfolio, there's no wonder they manage to continue growing through recessions and through a period of high inflation resulting in less consumer spend. Colgate is primarily known for a portfolio that centers around everyday usage products. This extensive range of offerings span throughout various price tiers within many of the product categories. This is great because it means that customers of all income levels are spending money on CL's products. To maintain the competitive edge, CL places a strong emphasis on supporting their pricing strategies through continuous innovation and effective advertising campaigns.

Through these efforts, the data has shown us that CL has effectively grown the quickest in the South American pool of consumers. In my opinion, the main contributing factor to the growth is because CL has a large enough portfolio of products that they can offer affordable and modern products that match all income levels. Now, I love collecting dividend payments from companies that create, produce, or distribute products that personally use. However, I am not quite convinced that CL fits my needs right now. With very underwhelming price movement over the last decade, I feel that cash can be better allocated right now.

{kind=link}

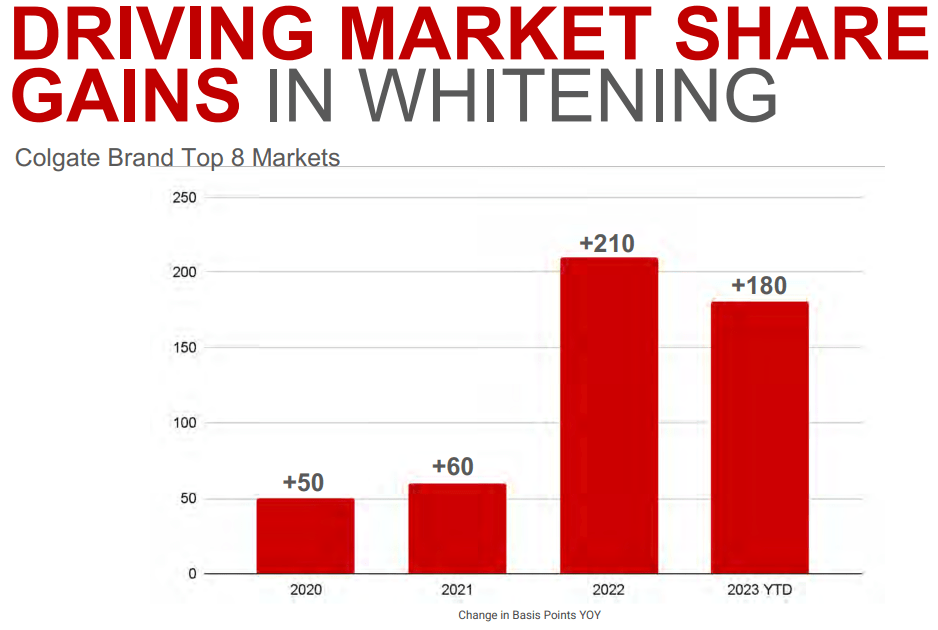

CL's oral care product line has seen tremendous sales growth and market share growth. The teeth whitening brands have seen a 180 basis point change year over year. Alongside the whitening strip market, CL has an already established toothpaste brand that currently captures about 41% of the total toothpaste market share worldwide. One of their fastest growing brands that has contributed to the Latin America growth is a sensitivity toothpaste brand by the name of Elmex. Elmex is the fastest growing brand in drugstores in Brazil.

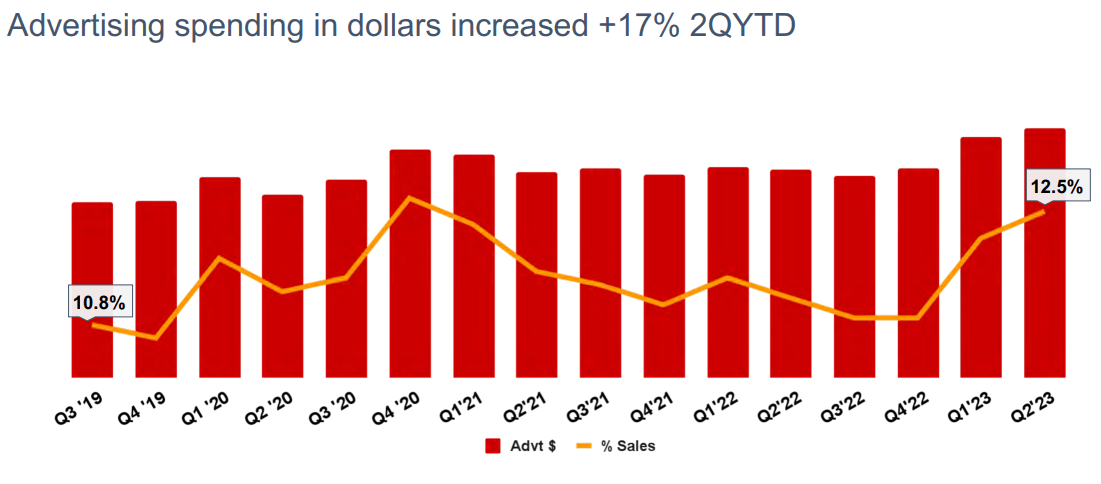

Another reinforcement to show CL's growth in Latin America is their impressive growth to having the #1 selling electric toothbrush handle in Mexico after only 1 year. I believe this a direct result of their increased investment into advertising their products globally. Advertising spend increased 17% through Q2. Ultimately though, the wealth of competition in this space leaves me skeptical of how well CL can do over time.

{kind=link}

Revenue Growth and Outlook

{kind=link}

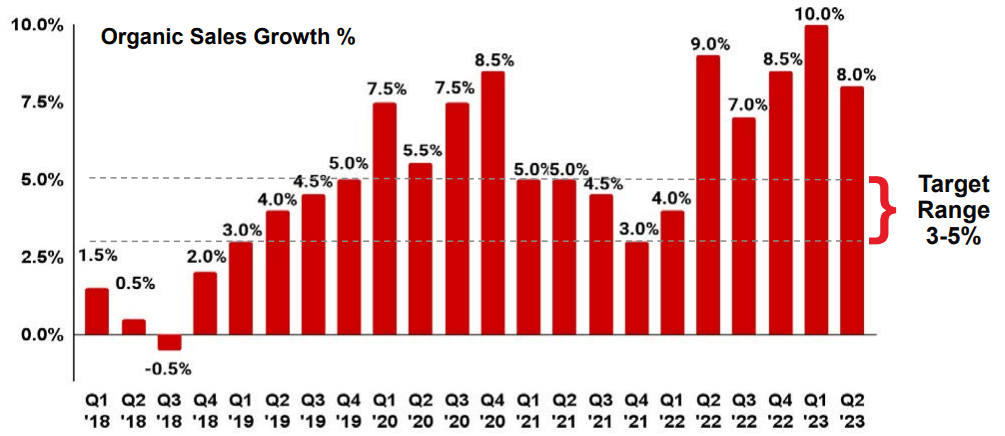

CL has comfortably reached their target organic sales growth range consistently over the last handful of years. With a targeted growth range between 3% - 5%, we can see that CL has surpassed this target amount quite frequently. In their most recent earnings report, the company benefitted from increased sales attributed to heightened advertising expenditures and price hikes.

Their sales growth outlook has been really solid in Latin America. As of Q2, CL managed to grow by a massive 16% in organic sales growth. This is a great improvement of the 6.5% sales growth from the prior year during the same period.

{kind=link}

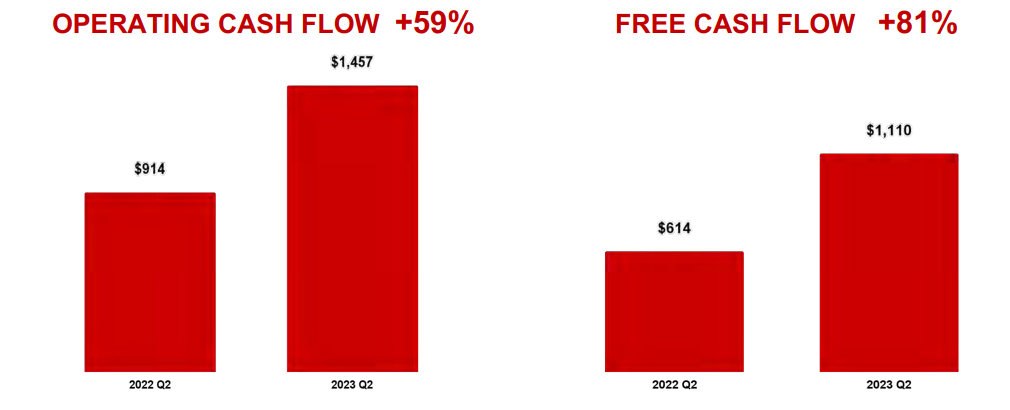

Colgate's global pricing has increased 11% as of Q2. I estimate that we will see a lower growth of pricing in the upcoming quarters as inflation cools. AS a result of these price increases, we can see that CL achieved a 59% year over year in operating cash flow. We can also see that CL has achieved an 81% increased free cash flow over the prior year.

In their most recent earnings call , we get further reinforcement of the increased push on advertising and strong sales:

On the margin line, clearly, very pleased with the progress that we're making both at the gross profit level and the operating margin level. And I remind everyone that our gross profit does not include logistics and cost of goods. So if you take logistics, obviously, we had a very strong quarter relative to gross profit acceleration. And our SG&A was down despite the fact that we implemented a 20% increase in advertising. - Noel Wallace - Chairman & CEO

Even with all of these great metrics, the price growth of CL has been underwhelming. A targeted growth range between 3% - 5% has not been enough to get the stock price to grow. CL has severely underperformed the S&P ( SPY ) for decades. I also worry that even if sales continue to hit the targeted range growth, is this growth enough to get any sizeable dividend raises? It would be really disheartening if we continue to get dividend raises of 3% and below, and it would further reinforce why I believe money can be better suited elsewhere as a dividend growth investor.

Consistent Dividends But Poor Returns

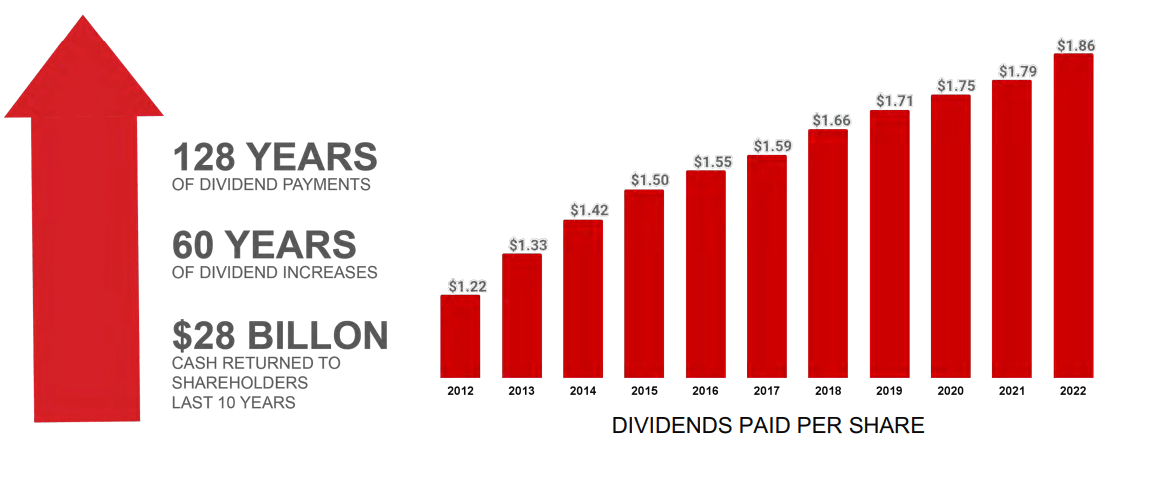

CL has consecutively increased their dividend payouts for 60 ears. This makes CL a part of the very slim dividend king club. Dividend kings are companies that have increased their dividends for at least 50 years and above. There are currently only 48 other dividend kings in existence.

{kind=link}

Colgate's starting yield sits at an average 2.7%. As of their latest announcement, they declared to pay out $1.92 per share in dividends. This results in a modest payout ratio of 62%. In addition, the 5-year average dividend growth rate has been on the slow end at an average 3% growth per year. If you are trying to build a dividend snowball, tiny raises of 3% and below are not going to help you gain much momentum. We like to see raises at a minimum of 5% for stocks that have low upfront yields under 2%.

I will admit that price growth over the last decade has been very underwhelming for CL. Comparing Colgate against the S&P 500 ((SPY)), we can see severe underperformance. A 50% return over a 10-year period is pretty lackluster, especially when you consider that most of the return comes from the dividend payments and less than half of that growth is from price appreciation. Getting most of your return from dividend payments is totally fine if that is your goal. However, if you are looking to stay on par with the indexes or obtain the highest total return possible, the CL is probably not the best choice.

Even comparing Colgate amongst their peer group, we can see that CL drastically underperforms the leaders of the sector. Colgate gets absolutely smoked by every single major competitor in the sector.

Conclusion

Colgate-Palmolive ((CL)) presents a complex investment proposition. While the company has demonstrated impressive growth, particularly in Latin America, driven by strategic initiatives like price increases and effective marketing, there are certain factors that raise concerns.

Despite being a dividend king with a consistent record of dividend increases over 60 years, the low starting yield of 2.7% and slow dividend growth of around 3% per year may not align with the objectives of dividend growth investors seeking more substantial income growth.

Furthermore, Colgate's stock performance has been lackluster over the past decade, significantly underperforming both the S&P 500 and industry peers. While the company's robust product portfolio and market share in oral care are commendable, the stagnant stock price growth raises doubts about its ability to provide strong total returns.

For further details see:

Colgate-Palmolive: Dividend King With Limited Growth