CL - Colgate-Palmolive: Mixed Outlook

2023-04-25 14:10:00 ET

Summary

- Revenue should benefit from increasing production capacity for Hill’s Pet Nutrition business, but the product recall of Fabuloso Multi-Purpose Cleaners is expected to negatively impact Q1 results.

- Margins should benefit from price increases but inflationary headwinds are still there.

- Valuation is a slight premium to 5-year average.

Investment Thesis

Colgate-Palmolive Company ( CL ) is set to report its Q1 earnings on Friday, April 28. I previously gave the stock a neutral rating in December and its stock price has stayed around similar levels. Looking forward, the company’s revenue and margin growth prospects are mixed. In Q1, the company’s volume is expected to be negatively impacted by the recall of Fabuloso Multi-Purpose Cleaners while improving capacity for Hill’s pet products should help. On the margin front inflation should still hurt but the company is taking pricing action to offset its impact. The stock is trading at a slight premium to its historical valuation and given a mixed outlook, I have a neutral rating on the stock.

Revenue Outlook

During the pandemic, Colgate's sales benefited from increased demand for oral and personal care products as people prioritized their overall hygiene. In addition, the Hills Pet Nutrition business also experienced healthy demand due to increased pet adoption around the globe. The sales growth continued in the following years. However, FX headwinds, supply chain disruptions, and an economic slowdown in Europe and China due to the ongoing energy crisis and COVID-19 lockdown respectively, partially offset the demand for CL’s product categories.

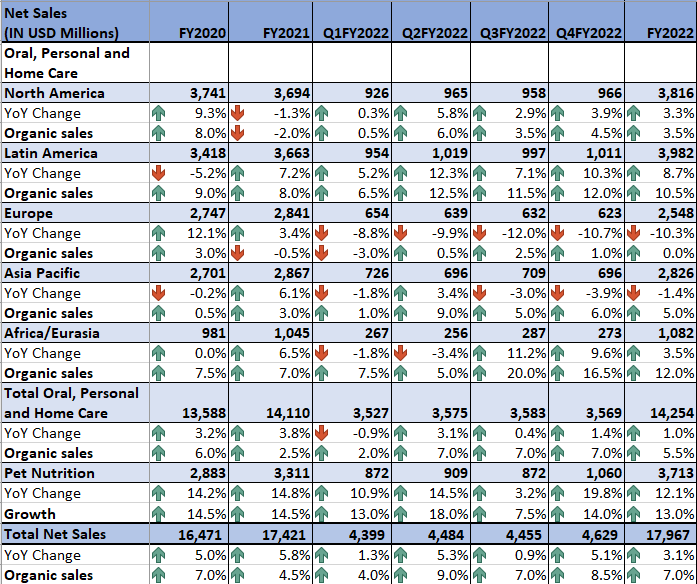

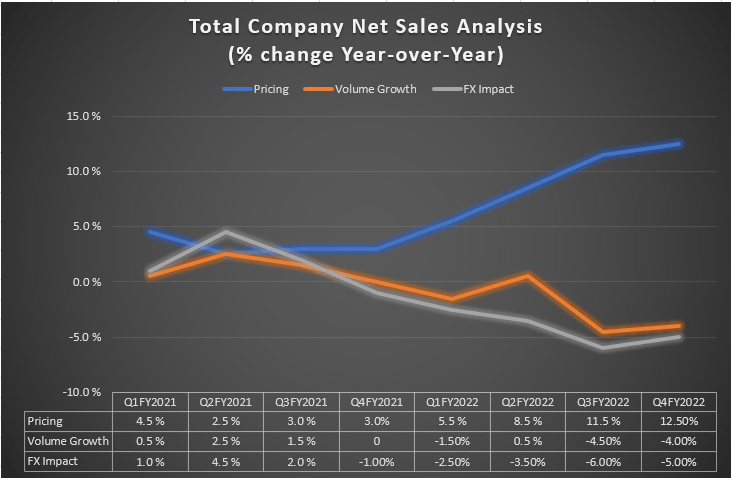

In the fourth quarter of 2022, while these headwinds continued, CL’s net sales benefited from price increases, new innovations, and healthy demand for Oral care products and Hill’s Pet Nutrition business. This resulted in net sales growth of 5% Y/Y to $4.6 bn, reflecting a 1.5% benefit from the Red Collar Pet Food business acquisition and a negative 5% FX headwind. On a constant currency organic basis, net sales increased 8.5% Y/Y, reflecting 12.5% benefits from pricing and a 4% volume decline.

{kind=link}

CL’s Historical Revenue (Company Data, GS Analytics Research)

{kind=link}

CL’s Historical Net Sales Analysis (Company Data, GS Analytics Research)

Looking forward, the company’s near-term outlook is mixed. The company has been facing some issues from capacity constraints at Hill’s Pet Nutrition business in recent quarters, but the situation is expected to improve in Q1 2023 and beyond. The company intends to use some of the excess capacity at the recently acquired Red Collar pet food business for the production of Hill’s Pet Nutrition products. The company is also launching its new Pet Food facility in Tonganoxie, Kansas, which is expected to be operational in the second half of 2023. Management is planning to increase its advertising spending to take advantage of these additional capacities. This should support sales growth in 2023.

However, the company faces a headwind from the product recall of Fabuloso Multi-Purpose Cleaners (~5 mn units) which should negatively impact volumes. Colgate’s volumes are already under pressure as the company is raising prices and the economy is slowing. This product recall may make Q1 volumes look worse. The company also faces difficult comps for organic sales from Q2 onwards as in FY22, the company’s organic sales were up high single digits from the second quarter to the fourth quarter. The current sell-side consensus is expecting ~ 4.14% Y/Y sales growth for Q1 2023, which is a modest slowdown compared to ~5.1% Y/Y growth in Q4 2022. I am slightly less optimistic and see a potential for the topline to miss the consensus estimates when the company reports its Q1 2023 earnings due to the impact of the product recall as well as continued pricing increases in this inflationary environment.

Margin Outlook

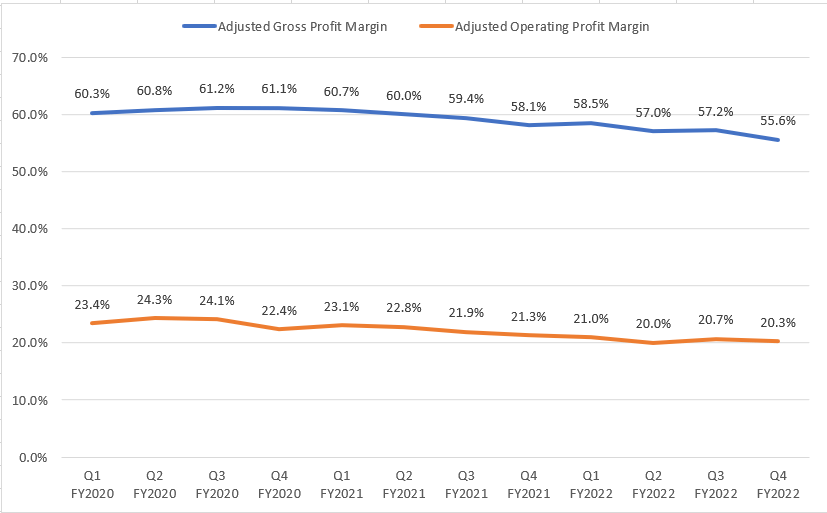

CL’s gross and adjusted operating margins are under pressure from higher inflationary costs from rising raw material and packaging costs. In the fourth quarter of 2022, in addition to higher raw material costs, a negative mix from lower sales in the skin health business and start-up costs associated with Hill’s additional capacity also impacted margins. These headwinds were partially offset by price realizations and CL’s productivity initiatives including cost savings in SG&A and overheads. As a result, the gross margin declined 250 bps Y/Y to 55.6%, while the adjusted operating margin declined 100bps to 20.3%.

{kind=link}

CL’s Historical Gross Profit and Adjusted Operating Profit Margin (Company Data, GS Analytics Research)

Looking forward, I believe, that the near-term headwinds from inflationary costs are still there. Management has hinted at $300-$400 million of raw material inflation in 2023, during the earnings call for Q4 2022. Moreover, the company expects further start-up costs (including hiring and training new staff) associated with the new food facility in Kansas to impact margins in the current year. However, the price increases in the first half of FY23 should offset some of its impact. Further, as we move towards the back half of this year, inflation is expected to moderate. So, while I am not too optimistic about Q1, margins should slowly improve as the year progresses. Gross margin comparisons are also easing in the back half of this year, especially Q4, which should also help.

Valuation and Conclusion

Colgate is currently trading at a 25.05x 2023 consensus EPS estimate of $3.11 which is below its 5-year historic average P/E of 24.25x . The company has a good dividend yield of 2.47% . The company’s near-term outlook is mixed with Q1 results expected to be impacted by the product recall. Though margin should benefit from price increases, inflationary headwinds are still expected to negatively impact this year’s results. I expect conditions to improve in the back half of this year. But till then I prefer to remain on the sidelines and continue to have a neutral rating on the stock.

For further details see:

Colgate-Palmolive: Mixed Outlook