CL - Colgate-Palmolive: Own This Dividend King At The Right Price

2023-10-31 08:05:00 ET

Summary

- Colgate-Palmolive is a resilient dividend stock with a 60-year history of consecutive dividend growth.

- The company's strong brand recognition and global market share contribute to its consistent revenue growth.

- While the stock is currently overvalued, a pullback in price due to near-term headwinds could present a buying opportunity for investors.

Dividend stocks have taken a beating as of late, with some sectors having been hit more than others. As a value investor, I don't mind seeing lower prices on quality companies, as this just means that I can accumulate more shares with a higher starting yield.

Getting a solid starting yield is one of the most important steps to compounding wealth, and perhaps it's just as important as dividend growth down the line.

This brings me to Colgate-Palmolive (CL), which is a Dividend King that's raised its dividend consecutively over the past 60 years, a feat shared by just a handful of names. Unlike a number of other dividend stocks, CL has been rather resilient over the past 12 months, driven by a slight rally in price over the past 30 days. In this piece, I discuss CL, and its recent results, and make a recommendation, so let's get started!

{kind=link}

Why CL?

Colgate-Palmolive is a stock that I haven't covered before, perhaps because it strikes me as one of those 'set it and forget it' types of investments that investors can count on for income and growth during both good times and bad. That's because its namesake brands for toothpaste and dishwashing detergent carry significant market share and are essential products and recession-resistant in nature.

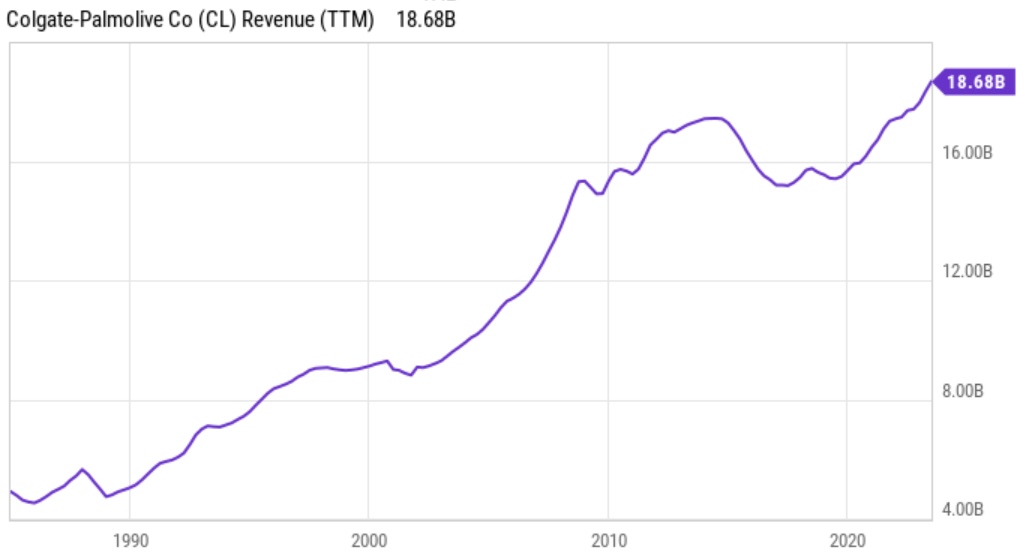

CL's products are available in 200+ countries and include additional Oral, Personal, Home Care, and Pet Nutrition products such as Tom's of Maine, Softsoap, Irish Spring, Ajax, and Fabuloso. These household staples have carried CL's revenue growth over the past 30+ years through multiple economic recessions and global events, as shown below.

{kind=link}

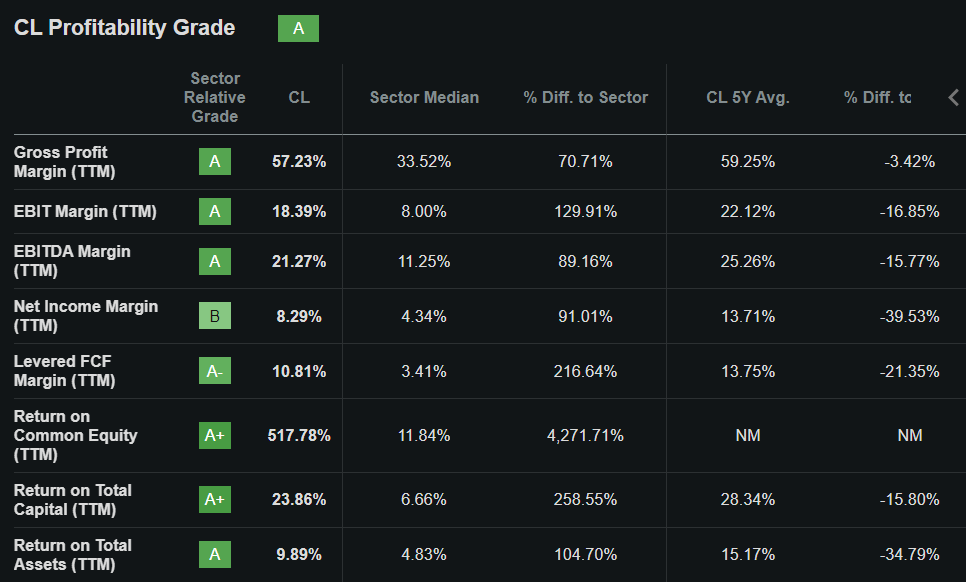

Brand recognition is especially important in the consumer products space, as household shoppers are more likely to entrust their families with recognizable brands with a long operating track record. Scale also matters as manufacturing efficiencies translate to barriers to entry and healthy margins. As shown below, CL scores an A grade for profitability, with sector-beating EBITDA and Net Income margins of 21% and 8%, respectively.

{kind=link}

CL recently turned in fairly strong results amidst an uncertain macroeconomic backdrop due to higher interest rates. This is reflected by organic sales rising by 9% YoY, driven by growth in all 4 of CL's categories. CL has also demonstrated its pricing power in the face of inflation, with gross profit margin rising by 130 basis points over the prior year period to 58.5%. Importantly, growth has trickled down to the bottom line, with GAAP EPS growing by 16% YoY.

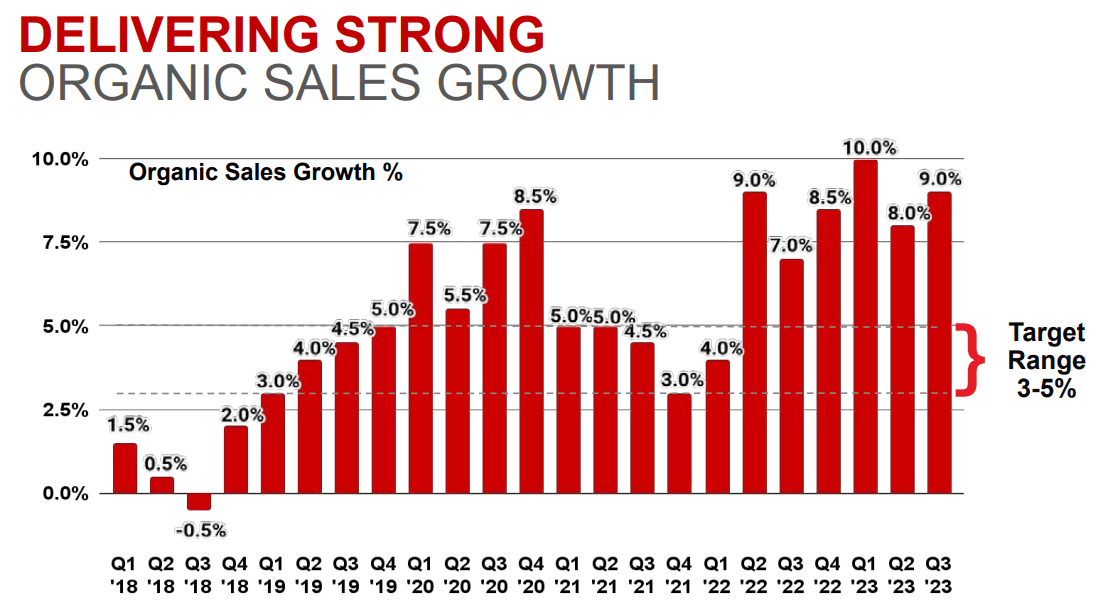

Notably, CL continues its global leadership position in its bread-and-butter oral care segment, with toothpaste and toothbrush holding a global market share of 41% and 31.5%, respectively. As shown below, CL's organic growth has been above its target range of 3-5% since Q2 of last year and has been above 3% every quarter since the start of 2019.

{kind=link}

CL's strong balance sheet comes in handy in this higher interest rate environment, as this reduces the likelihood that it will be materially impacted by debt refinancing. This is reflected by its A- credit rating by S&P, along with $1.2 billion in cash and short-term investments on the balance sheet, and a healthy net debt to EBITDA ratio of 1.8x, sitting well below the 3.0x level generally considered to be safe by rating agencies for standard C Corporations.

Given the durable and growing business fundamentals and the strong balance sheet, I see very little risk to the 2.6% dividend yield, which is well-protected by a 61% payout ratio and 60 years of consecutive growth, as mentioned earlier. What I would like to see, however, is for CL to "share the wealth" with shareholders, considering that its 5-year dividend CAGR is only 2.9%, despite strong underlying growth. For a consumer staples company with already built-out infrastructure, there is really little need to hoard cash unless CL is eyeing an acquisition.

Looking ahead, I do see risks on the horizon for CL, considering that management is guiding for 7-8% annual organic growth for the full year 2023, implying a deceleration in the fourth quarter. Moreover, recent economic reports this month indicate that the strength of U.S. consumer spending may be waning, considering that the average American consumer has been spending more than they are earning this year. As such, the whittling down of savings could lead to consumer downtrading towards store brands which could negatively impact CL's results next year.

With analysts expecting 7-9% annual EPS growth over the next two years, which I believe is on the optimistic side, CL stock appears to be pricey at $73.88 with a forward PE of 23.2. As such I don't believe is appealing for value investors at the current price. I would be more interested in the stock at a price of $63.60 or below, which translates to a forward P/E of 20.

This puts it on par with most consumer staples companies, which traditionally trade at an 18-20x P/E. I believe this is a more reasonable valuation for CL should it be able to sustain 7%+ annual EPS growth over the long run, which combined with the 2.6% dividend yield could translate to 9-10% annual total returns.

Investor Takeaway

Overall, CL is a moat-worthy consumer staples company that appears to be right on track with its strong brands and long-term growth strategy. It comes with a strong balance sheet to weather higher interest rates and has a well-protected, albeit slow-growing dividend. However, I believe the stock is overvalued at current levels with the positives more than fully baked into the current share price, and would wait for a pullback before considering an investment. As such I initiate a 'Hold' rating on the stock. Catalysts for a change in rating would be materially higher than expected underlying growth and/or more meaningful dividend growth.

For further details see:

Colgate-Palmolive: Own This Dividend King At The Right Price