CL - Colgate-Palmolive: Positive Q1 But Operating Margin Remains Low

2023-04-30 05:16:54 ET

Summary

- Organic growth is driven by higher advertising spending but operating margin remains below historical average.

- Analysts' expectations were exceeded.

- Operating margin in Europe worsens due to high inflation, and in U.S. Fabuloso negatively affected home care sales.

Colgate-Palmolive's ( CL ) Q1 2023 surpassed analysts' expectations for both EPS and revenue.

- Actual EPS was $0.73 versus $0.70 expected.

- Actual revenues were $4.77 billion versus $4.57 expected.

Overall, the quarterly was good, but concerns still remain related to significantly lower margins than in the past.

Comment on Q1 2023

{kind=link}

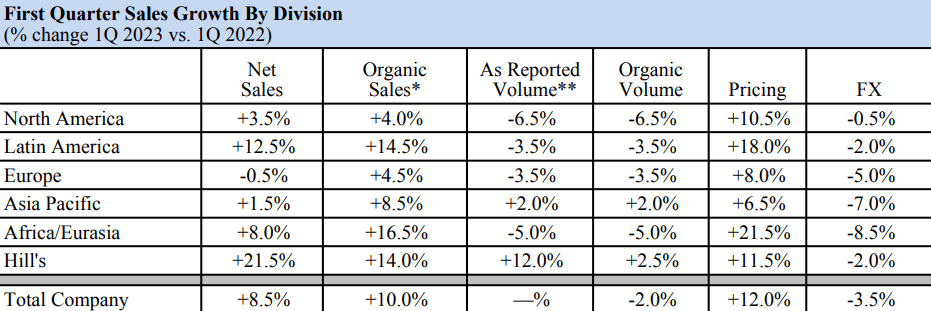

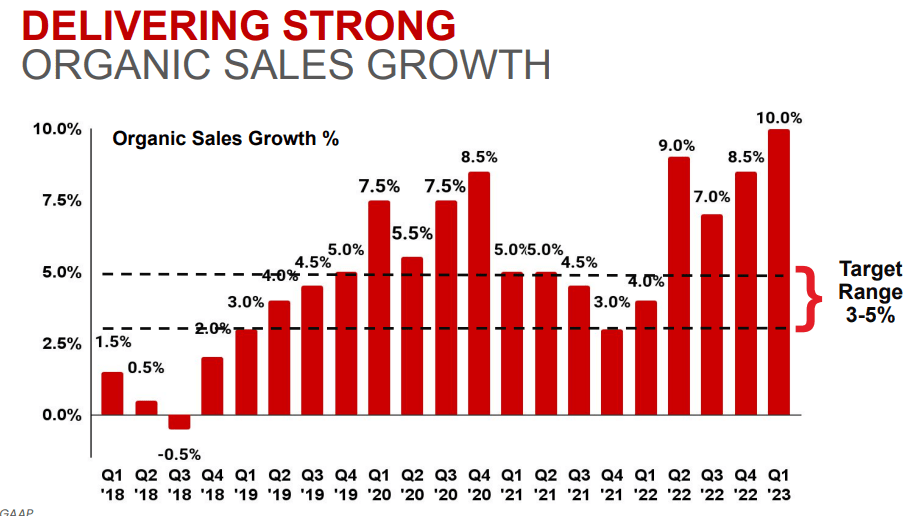

Compared to Q1 2022, both Net Sales and Organic Sales increased, respectively by 8.50% and 10%. However, as a result of the massive price increase, organic volume decreased in all divisions except Asia Pacific and Hill's. The overall result to date has been positive, but we need to assess consumer behavior over the long term after this price increase. The strong dollar continues to be a problem especially in the Europe, Asia Pacific, and Africa/Europe divisions.

{kind=link}

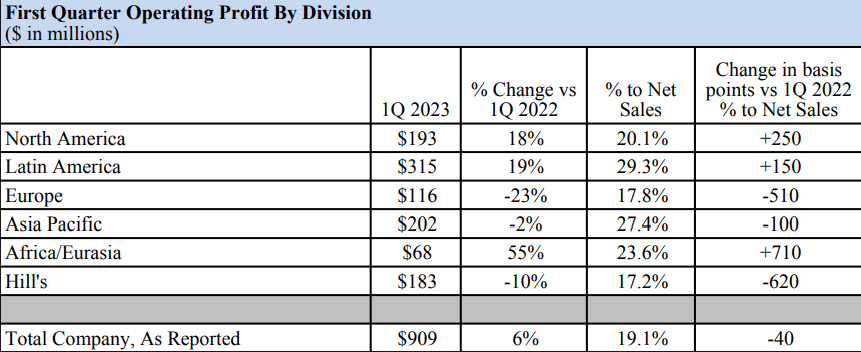

Having ascertained organic sales growth, we now need to understand how profitable individual divisions have been.

{kind=link}

Overall, Q1 2023 recorded operating income of $909 million, 6% higher than Q1 2022. In all divisions, pricing managed to limit cost increases due to higher raw material prices, packaging, and advertising investments. Without this component, Colgate's margins would have been significantly worse. There are, however, aspects to consider about individual divisions, as results diverged widely.

Organic growth in oral care and personal care in North America was partially offset by declining organic sales in home care. The reason is attributed to problems with Fabuloso . From December 14, 2022 to January 23, 2023, about 5 million bottles were produced in which less preservative was added than usual, and this was enough for the company to state that these bottles could be potentially harmful to those with already weak immune systems. Fortunately, about 3.9 million bottles were never sold, but the image damage to the brand and the lost revenue of millions of bottles remain.

Europe is an important market for Colgate-Palmolive and it performed rather disappointingly. Not only was operating income down 23% from Q1 2022, but operating margin deteriorated by 510 basis points. An interesting question was asked about this by Mark Astrachan during the conference call and Noel Wallace's ((CEO)) response was as follows:

Europe, a little bit driven, obviously, by the foreign exchange environment to a certain extent and obviously, more increased inflation in Europe than we've seen in other markets around the world, particularly around the high gas prices and the fall-off effects of higher gas prices, and some of the raw materials that we purchased into our European plants. So overall, there's been a little bit more pressure there.

In short, according to the CEO, the reasons for the drop in operating margin are the usual ones and should be temporary. No mention is made of any increase in competitive pressure in the industry, which I personally would not rule out entirely.

Still on the subject of operating expenses, it is worth clarifying the company's position on advertising expenses, as they are currently above the standard levels to which the company has accustomed us. They accounted for 12% of net revenues this quarter, up 14% from Q1 2022.

While advertising spending is helpful in supporting organic revenue growth, it can weigh too heavily on the operating margin, which is far from past levels. During the conference call, many analysts asked questions about this but management did not seem concerned. In fact, in the FY2023 guidance, advertising is still expected to grow both in terms of dollars and as a percentage of sales.

We've got strong innovation in emerging markets and you've seen the level of advertising that we're putting back into the business. That gives us, again, confidence that we're able to sustain that advertising as we move into the back half of the year, and we intend to continue to do everything we can to increase that advertising support in the back half, particularly in emerging markets in order to: one, support the innovation we have; second, drive the pricing into the market and continue to accelerate volume growth in the category.

So, for the time being, the company is focusing heavily on growing its products in emerging markets, and in fact the best results this quarter were achieved in Latin America and especially Africa/Eurasia. At the moment, management is satisfied with the results obtained and will keep advertising expenses high so that it can support increased pricing. In my opinion, this situation will persist until the inflation problems disappear and the company can raise prices less aggressively.

Finally, let's take a look at debt-related expenses. Colgate-Palmolive has now a total debt of $8.90 billion, quite high considering that 2022 net income was only $1.59 billion. In Q1 2023 interest expenses were $54 million, double the $27 million in Q1 2022. In any case, this does not seem to worry the CFO as he stated that the cost of debt will have a modest impact on the year.

Final considerations

Overall, it was not a bad quarterly, however, the operating margin remains low compared to the past due to the countless problems in the current macroeconomic environment. High advertising spending at the moment seems necessary to support revenue growth.

{kind=link}

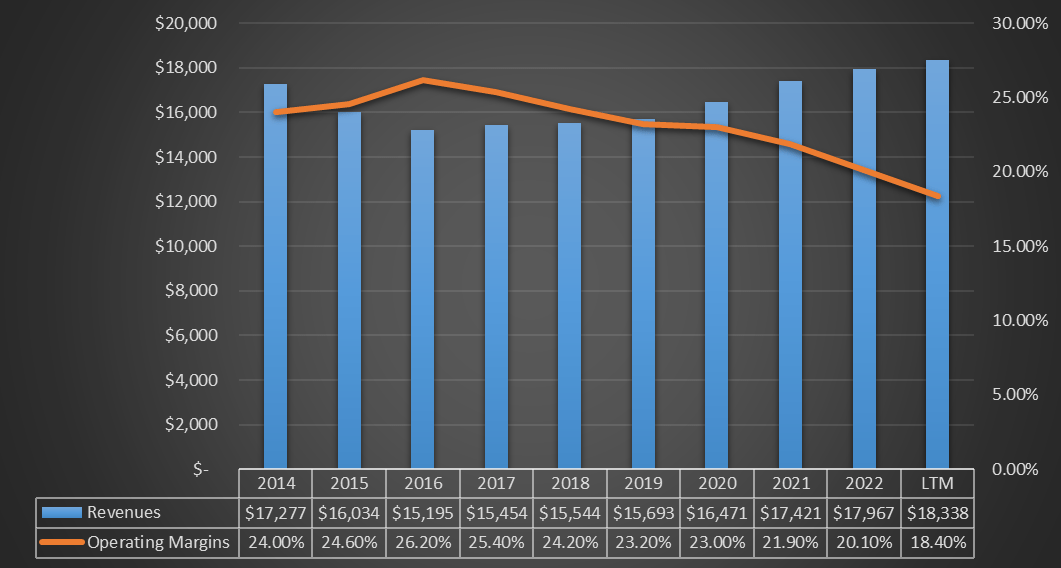

The reason there is so much pressure on margins is because the company's revenues struggle to grow over the long term, so with a decreasing operating margin it all gets complicated. This is certainly not an ideal situation for a company that has been issuing a growing dividend for 59 years. At this rate, the long-term sustainability of the dividend is at risk.

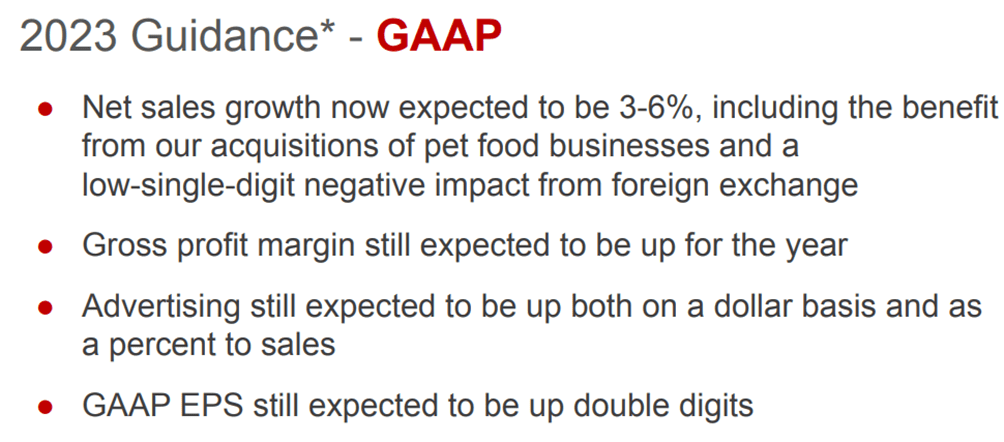

Finally, I conclude this quarterly analysis with the company's guidance on the full FY2023.

{kind=link}

For further details see:

Colgate-Palmolive: Positive Q1 But Operating Margin Remains Low