CL - Colgate-Palmolive: The Reasons We Are Becoming More Cautious

2023-06-05 16:31:31 ET

Summary

- Colgate-Palmolive's net margin has been gradually declining since 2020, but improving macroeconomic factors, including a weakening USD and falling energy prices, may lead to margin expansion in the coming quarters.

- The company's efficiency has been improving gradually since late 2020.

- According to our updated valuation model, including a higher required rate of return, the stock appears to be trading at a 15% premium compared to our highest fair value estimate.

- For these reasons, we now rate CL's stock as "hold".

Colgate-Palmolive Company ( CL ), together with its subsidiaries, manufactures and sells consumer products worldwide. The company operates through two segments, Oral, Personal and Home Care; and Pet Nutrition.

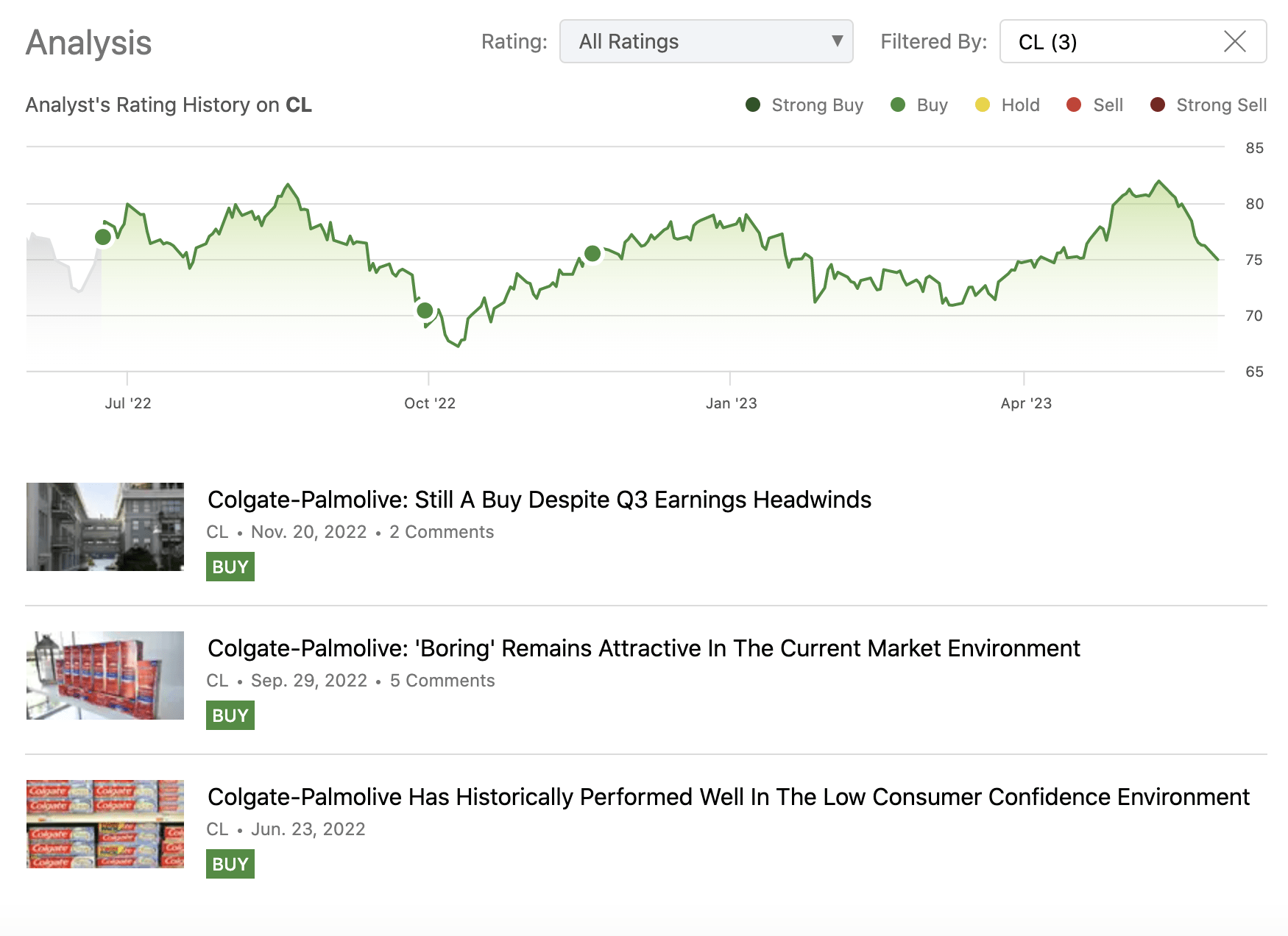

We have published three articles about the firm on Seeking Alpha in 2022, rating the company's stock as a "buy" each time.

{kind=link}

To recap, the primary reasons for our bullish view were:

- Colgate-Palmolive has a strong track record of outperforming the broader market during times of low consumer confidence.

- The firm's 58 years of consecutive dividend payments and 21 years of consecutive dividend growth make CL an attractive candidate for dividend investors.

- Expansion of the pet food business could fuel the firm's growth in the years to come.

- CL appeared to be trading close to its fair value, based on the Gordon Growth Model, however, it didn't capture the growth potential associated with the pet food business expansion.

As of today, these points still remain relevant and continue to make the business attractive, in our opinion.

At the same time, we have highlighted the near-term headwinds, which have been associated with the challenging macroeconomic environment. These included rising inflation, elevated energy price, unfavorable FX environment, and the geopolitical tensions around the globe.

In today's article, we will be focusing on the firm's profitability and efficiency and assess how these measures compare with those of CL's peers/competitors and how they may develop further in the quarters to come, based on the changing macroeconomic environment. We will also reassess the firm's valuation in order to understand, whether our previously established "buy" rating is still intact.

To begin, we will first discuss one of the most common profitability measures, the net profit margin. Later we will use the asset turnover ratio to elaborate on the efficiency of the firm. We will finish our writing with the valuation section.

Net profit margin

The net profit margin is calculated as the ratio between net income and revenue. The following chart depicts CL's net profit margin over the past five years.

In general, we prefer firms that have stable or expanding net profit margins. This is, however, not the case for CL. The company's margin has been gradually declining starting from the second half of 2021.

This development, while not favorable, is not surprising. The challenging macroeconomic environment has been putting downward pressure on the margins of most businesses.

Cost of goods sold has been rapidly increasing along with SG&A expenses. While the firm has managed to increase its revenue, this increase has not been able to completely offset the cost increases, resulting in a margin contraction. At this point, one may also ask the question, why was the firm not able to pass on all the cost increases to its customers? Despite selling largely non-discretionary products, the demand for these items may be somewhat elastic in times of low consumer confidence.

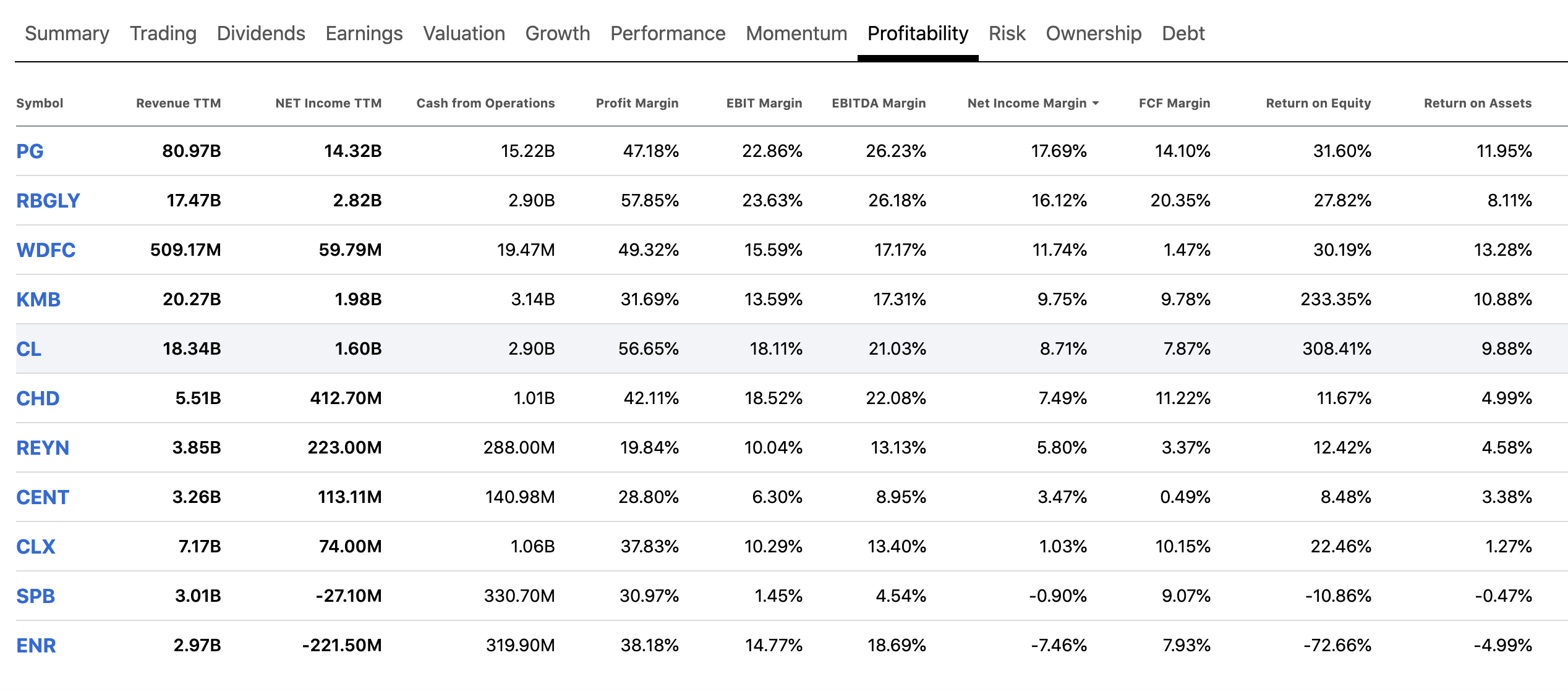

Despite the significant decline in the net profit margin, CL's profitability measures still rank high among those of other players in the household products industry.

The following table shows that CL's gross profit margin, EBIT- and EBITDA margins as well as the net profit margin remain relatively attractive.

Profitability comparison (Seeking Alpha)

{kind=link}

Further, at this point, it is also important to look forward and not backwards. Some of the macroeconomic factors that have been negatively impacting the financial results of the firm have substantially improved over the past quarters. We would like to highlight two of these here:

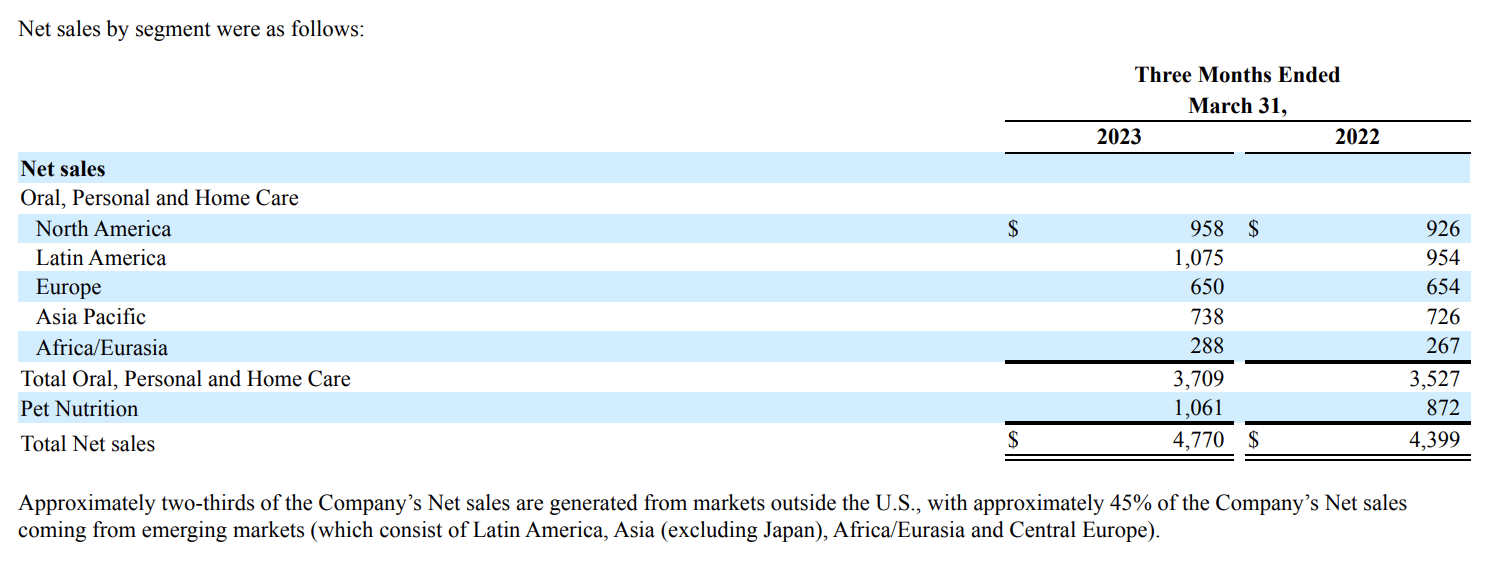

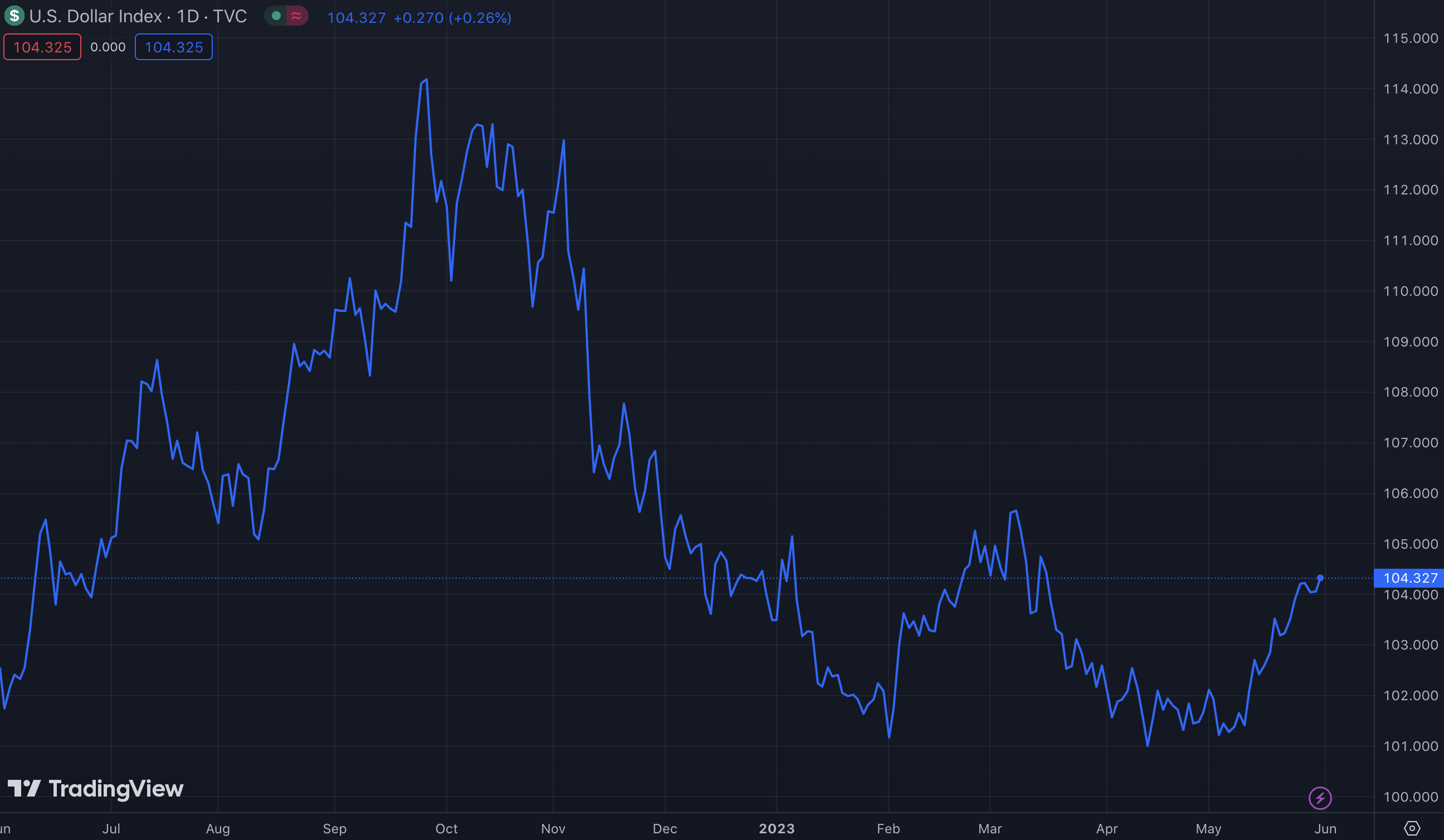

1) Weakening USD.

A substantial portion of CL's revenue is being generated outside of the United States. Therefore, the strong USD relative to other currencies has been negatively impacting the financial figures in the past year.

Net sales by segment (CL 10-Q) Dollar index (TradingView.com)

{kind=link}

{kind=link}

Since its peak in Q3 2022, however, the dollar has meaningfully weakened. We believe that this development can potentially have a positive impact on CL's financial results in the coming quarters.

2) Falling energy prices.

Second, energy prices have also fallen substantially. Both crude oil and natural gas have peaked in 2022 and have kept declining since then.

Lower energy prices are likely to have a positive influence on the expenses and therefore may lead to an expanding net profit margin in the quarters to come.

Last, but not least, we need to highlight that CL has performed well in Q1, beating both EPS and revenue estimates. The management also sounds quite optimistic about 2023, as they have set expectations for net sales growth in the 3% to 6% range and a gross margin expansion .

Asset turnover

Asset turnover is calculated as the ratio between sales and total assets. This ratio is a measure of efficiency and essentially shows, how effective a firm is in generating profits, using its assets.

In general, we also prefer firms that have stable or improving efficiency.

During late 2019 and early 2022 CL's asset turnover has declined significantly. Since the second half of 2020, however, the trend has changed and the efficiency has started to increase.

It's important to mention here that the decline in 2019 and 2020 has not been due to declining sales (sales have been actually increasing gradually over the past five years), but because of a material jump in the total assets, driven by one of CL's largest acquisition to date, the acquisition of Laboratories Filorga.

One more important item to mention is the growth of accounts receivable in relation to the growth of revenue. Sometimes companies manipulate their sales figures by starting to sell more on credit or by changing their revenue recognition practices, just to inflate their revenue figures. This can be normally detected, if accounts receivable increase at a much faster pace than revenue. This, however, is not the case for CL, which is a good sign.

All in all, despite the asset turnover still being below pre-pandemic levels, it has been improving in the past quarters. We believe that the demand for CL's products is likely to remain strong, even if a recession occurs in the near future.

For these reasons, we like CL from an efficiency point of view.

Review of valuation

In our previous article, we have elaborated extensively on the valuation of CL using the Gordon Growth Model. Today we will review whether our input assumptions are valid, and if not, how to change them and what fair value these changes would yield.

1) Perpetual growth rate.

We believe that our previously established range for the perpetual growth rate between 2.5% to 4.5% is still valid, as this range is still in line with the firm's historic averages. So no changes in this assumption.

2) Required rate of return.

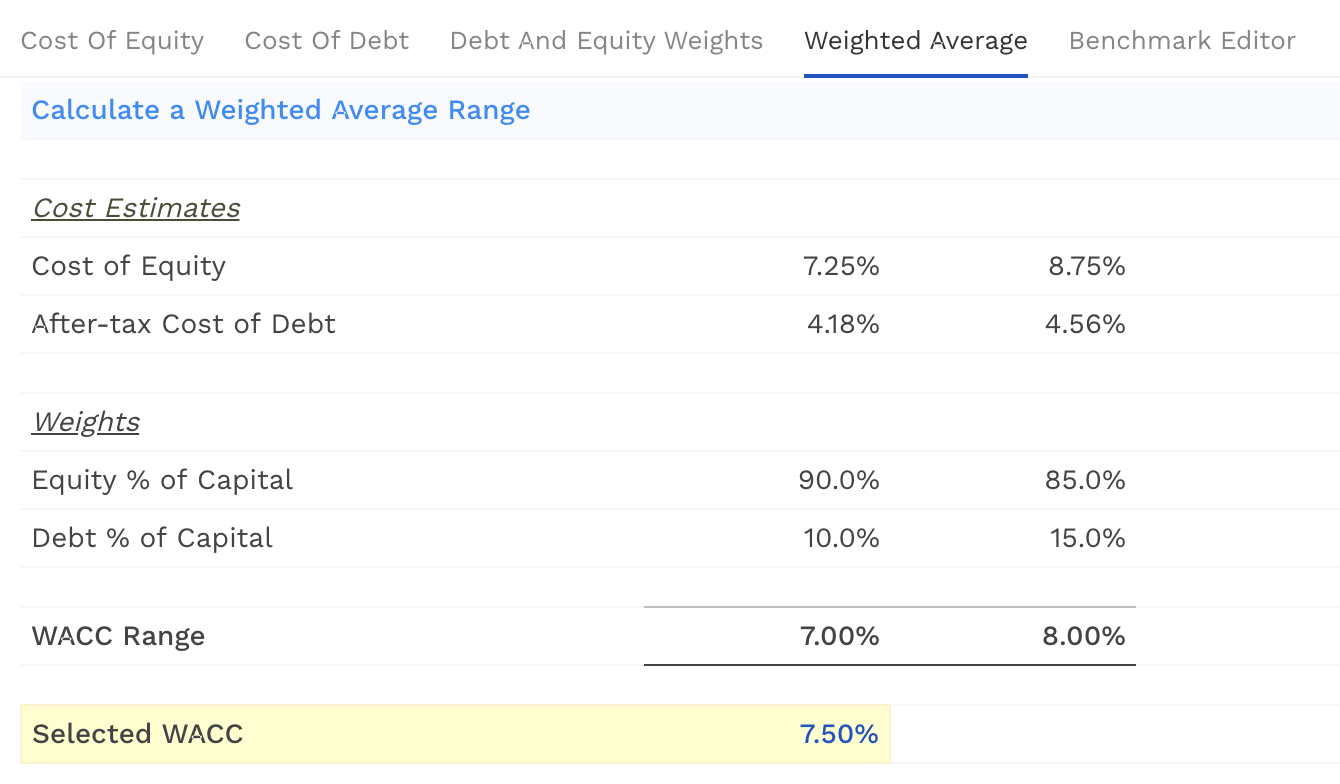

Previously, we have used a required rate of return of 6.5%, which was the firm's estimated weighted average cost of capital at the time of writing (November 2022). Using the weighted average cost of capital is still justified, however, due to the changing macroeconomic environment, including the rising interest rates, the WACC has changed.

According to the most recent estimates from finbox.com, the WACC is thought to be about 7.5%.

WACC (finbox.com) Fair value range (Author)

{kind=link}

{kind=link}

Because of the higher discount rate, the estimated fair value range has decreased substantially compared to our previous estimates. As CL's stock is currently trading around $76 per share, it is more than 10% above our highest estimate. For this reason, we believe that CL may not be currently trading at an attractive price level to justify maintaining our previous "buy" rating.

To wrap up

CL is still trading at a price level which is about in the middle of our previously estimated fair value range of $48 - $98, but is more than 10% above our newly established fair value range of $39 - $67, which better reflects the most recent changes in the macroeconomic environment.

While the net profit margin has been gradually shrinking since 2020, we believe that the improving macroeconomic environment may lead to a margin expansion in the coming quarters. The Q1 results and management's expectations about 2023 also look promising.

The firm's efficiency has also been gradually improving since late 2020.

For these reasons, we downgrade CL's stock to "hold".

For further details see:

Colgate-Palmolive: The Reasons We Are Becoming More Cautious