GIL:CC - Columbia Sportswear Company: A Decent Prospect At This Time

Summary

- Columbia Sportswear Company has had an interesting operating history, with revenue and profits rising nicely in most years.

- This year is slated to be somewhat weak for the business, but shares are still attractive from a cash flow perspective.

- Though not a strong prospect by any means, it does still warrant a favorable outlook at this time.

For many investors, the apparel, footwear, accessories, and other related markets are not viewed as particularly appealing. Often viewed as commoditized products that are subjected to severe competition and that can suffer from swings in consumer sentiment, the companies that operate in this space don't always perform well. At the same time, the players that do create a nice presence for themselves provide investors with an attractive opportunity for upside. One player that investors might want to consider is Columbia Sportswear Company ( COLM ). Over the years, the overall financial trajectory for the company has been positive. At present, shares are looking slightly pricey compared to similar firms. But when you consider the company's historical track record and how cheap shares are from a cash flow perspective, it's definitely worth some consideration. All things considered, I've decided to rate the business a soft ‘buy’, reflecting my belief that it will likely outperform the market for the foreseeable future.

Trying Columbia Sportswear on for size

According to the management team at Columbia Sportswear Company, the company operates as a global leader in designing, developing, marketing, and distributing outdoor, active, and everyday lifestyle apparel, footwear, accessories, and equipment products. Of course, more details are warranted. To truly understand the company, we should dig into the specific brands and products that it owns and offers. First and foremost, the company sells a variety of products under the Columbia brand name. This line consists of high-value outdoor apparel, footwear, accessories, and equipment products. Examples of specific offerings include, but are not limited to, shoes for all sorts of customers ranging from kids, to women, to men, and more. Under the activity category, the company sells products related to hunting, golf, camping, fishing, hiking, and more. Most of these include pants, shirts, vests, and other related products.

There are, of course, other leading brands that the company owns. One of the most significant is SOREL, which focuses on premium, durable, and design-driven footwear and accessories, largely centered around women but also catering to men and youth customers. The Mountain Hard Wear brand that the company acquired in 2003 focuses on premium apparel, accessories, and equipment for climbing enthusiasts. And the prAna brand focuses on sustainable clothing centered around activities like yoga, and the outdoors.

As I mentioned already, Columbia Sportswear Company is a global company. Having said that, its largest concentration is to the US market. That particular segment sells the firm's products to nearly 2,200 wholesale customers across the country and also direct-to-consumer through the company's own network. On the direct-to-consumer side, the company directly operates 142 different retail stores. During the company's 2021 fiscal year, this segment accounted for 65.9% of the firm's revenue and for 77% of its profits. Next in line, we have the LAAP segment, which focuses on customers in Japan, Korea, and China, as well as other related markets. As part of its operations, the company directly had 277 retail stores. It also maintained 29 concession stands and involved 69 franchise-based arrangements with third parties in the regions in which the segment operates. Last year, this segment accounted for 14.9% of revenue but for just 6% of profits.

The third segment to focus on is the EMEA (Europe, Middle East, and Africa) segment. In addition to focusing on wholesale customers across Europe, the Middle East, and Africa, the company also has 26 retail stores under its belt and it maintained 21 concession-based arrangements with third parties at the end of last year. 12.2% of the company's revenue and 9.4% of its profits came from this segment in 2021. And finally, we have the Canada segment. This one’s focus is fairly self-explanatory. In addition to focusing on wholesale customers, this segment also operates 10 retail stores throughout that nation. 7% of the company's revenue and 7.6% of its profits came from Canada last year.

{kind=link}

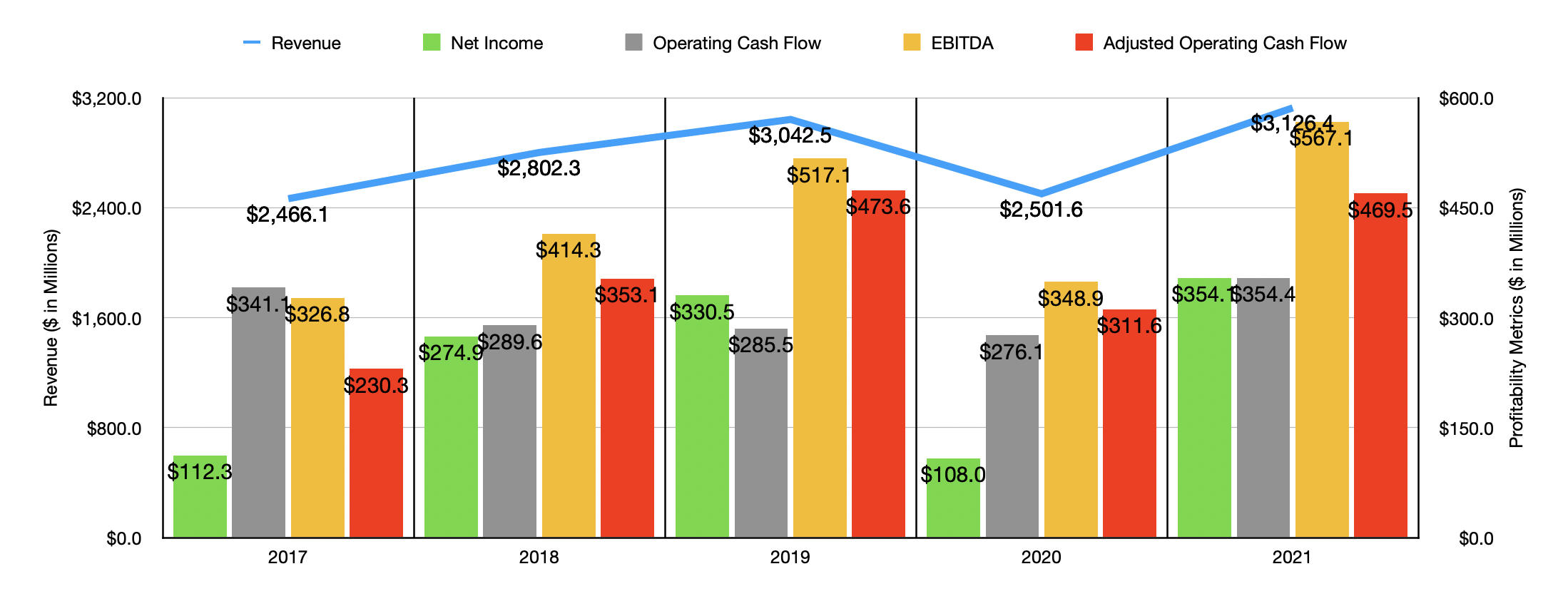

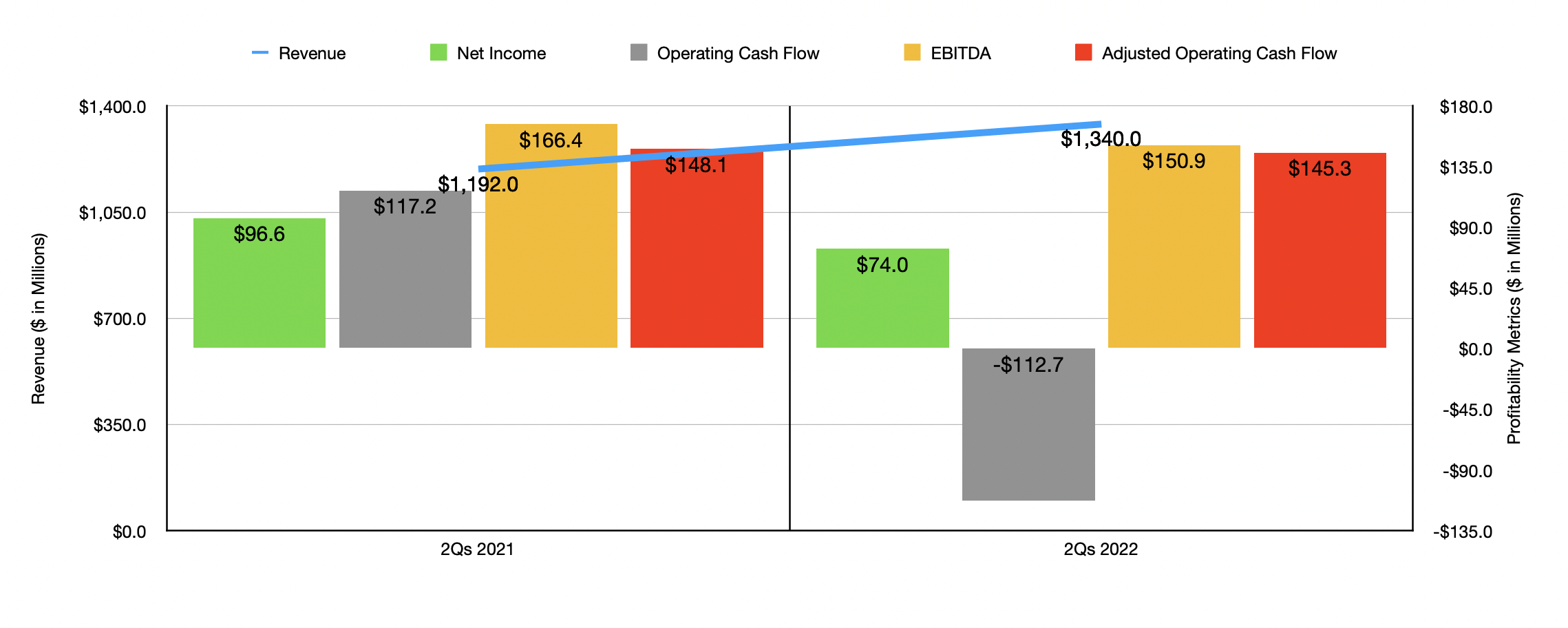

Over the past few years, the overall financial trajectory for Columbia Sportswear Company has been positive. Between 2017 and 2019, sales rose from $2.47 billion to $3.04 billion. Revenue declined to $2.50 billion in 2020 thanks to the COVID-19 pandemic. But then, in 2021, sales rebounded, hitting $3.13 billion. That growth has continued into the current fiscal year. In the first half of the 2022 fiscal year , sales came in strong at $1.34 billion. That represents an increase of 12.4% over the $1.19 billion generated the same time last year. By far, the greatest strength for the company involved the SOREL brand, with revenue rising by 33%. This was followed up by the much larger Columbia segment reporting an increase of 12%. There were multiple contributors to this year-over-year improvement. For instance, management attributed some of the sales increase to favorable late-season cold weather product sales in the first quarter. However, the company also said that its global direct-to-consumer e-commerce business fared quite well, growing by 10% year over year. Although this may not seem like all that much, it is worth noting that other retailers have seen their online sales decline as the economy opens up and people go back to visiting stores in person. So the continued growth there is encouraging.

On the bottom line, the picture has been remarkably similar. Between 2017 and 2019, net income rose consistently, climbing from $112.3 million to $330.5 million. In 2020, the company's profits dropped to $108 million before shooting up to $354.1 million last year. Unfortunately, not every profitability metric followed the same path. Operating cash flow, for instance, actually declined between 2017 and 2020, dropping year over year from $341.1 million down to $276.1 million. Though in 2021, it did rebound to $354.4 million. If we adjust for changes in working capital, however, it actually would have risen from 2017 to 2019. Then, after falling from $473.6 million in 2019 to $311.6 million in 2020, it then rebounded to $469.5 million last year. And finally, we have EBITDA. Its trajectory looked remarkably similar to what we can see by looking at net income. After dropping in 2020, it ultimately hit an all-time high of $567.1 million last year.

{kind=link}

Although revenue has risen this year, profitability has been a bit weak. Net income in the first half of the year totaled just $74 million. That's down from the $96.6 million reported one year earlier. Substantially all of this pain came from an increase in the company's cost of sales relative to revenue. Gross profit, as a result, declined from 51.5% of sales to 49.5%. Much of this, in turn, was driven by higher inbound freight costs, some of which was offset by foreign currency translation, favorable channel net sales shifts, and increased channel profitability due to the net effect of higher direct-to-consumer margins and lower wholesale margins. Other profitability metrics followed suit so far this year. Operating cash flow went from $117.2 million to negative $112.7 million. Though if we adjust for changes in working capital, the picture would have been much better, with the metric inching down from $148.1 million to $145.3 million. We also saw a decline in EBITDA, with the metric dropping from $166.4 million to $150.9 million. Interestingly, these pains did not stop the company from buying back a significant amount of stock. In the first quarter of the year, management bought back $217.3 million worth of shares, while in the second quarter they repurchased $69.6 million worth. With only $99 million left under its share reauthorization plan, the company decided to increase the plan by a further $500 million in the second quarter.

When it comes to the 2022 fiscal year as a whole, management does expect revenue to come in a bit weaker than anticipated. Previously, they forecasted revenue of between $3.63 billion and $3.69 billion. That range has now been decreased to between $3.44 billion and $3.50 billion. Although this is disappointing, it does still represent a 10% to 12% increase compared with the company generated last year. Earnings per share, meanwhile, should come in at between $5 and $5.40. At the midpoint, this would imply net income of $215.5 million. If we analyze financial results for the other profitability metrics, then we should anticipate adjusted operating cash flow of $460.6 million and EBITDA of $514.3 million.

{kind=link}

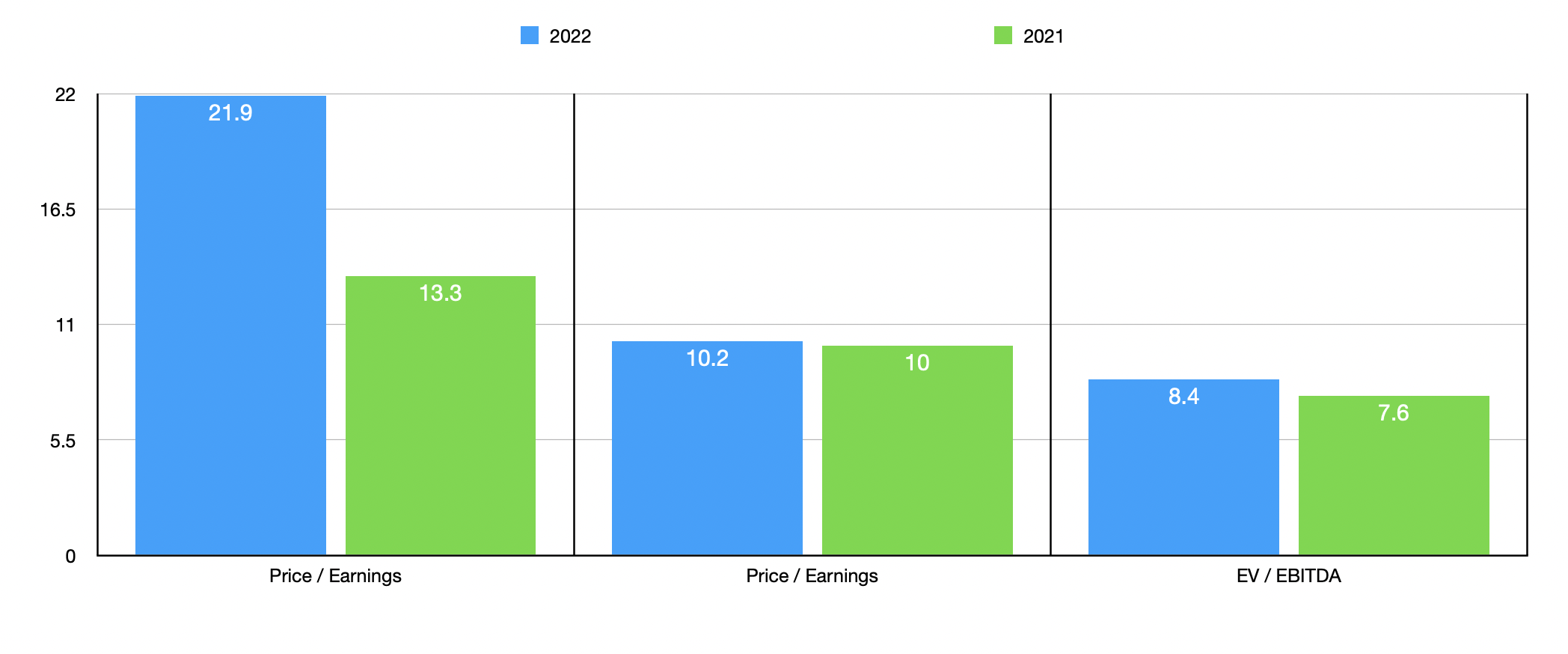

Using these figures, it becomes fairly simple to value the business. On a price-to-earnings basis, the company does look considerably more expensive than it did using last year's results. The multiples, shown above, rose from 13.3 to 21.9. Even so, the increases for the other profitability metrics are much smaller, as can be seen in the aforementioned chart. As part of my analysis, I also compared the company to five similar firms. Using our forward figures, we can see these businesses ranging from a low of 7.7 to a high of 16.5 when it comes to the price-to-earnings approach. In this case, Columbia Sportswear Company was the most expensive of the group. When it comes to the price to operating cash flow approach, the range is between 6.1 and 13.8. In this scenario, four of the five companies are cheaper than our prospect. And for the EV to EBITDA approach, the range is between 6.4 and 10, with two of the five businesses cheaper than our target.

| Company |

| Price / Earnings |

| Price / Operating Cash Flow |

| EV / EBITDA |

| Columbia Sportswear Company |

| 21.9 |

| 10.2 |

| 8.4 |

| PVH Corp. ( PVH ) |

| 7.7 |

| 6.1 |

| 6.4 |

| Under Armour ( UAA ) |

| 16.5 |

| 13.8 |

| 9.6 |

| Hanesbrands ( HBI ) |

| 9.5 |

| 8.0 |

| 10.0 |

| Gildan Activewear ( GIL ) |

| 10.4 |

| 9.2 |

| 8.5 |

| Carter's ( CRI ) |

| 11.1 |

| 8.3 |

| 7.0 |

Takeaway

Based on the data provided, it seems to me as though Columbia Sportswear Company is doing fairly well considering the current economic situation it is being forced to contend with. Although the company is pricey relative to some of its peers, shares don't look unreasonably priced from a cash flow perspective. This low pricing, combined with the company's historical track record, is enough for me to be slightly bullish on the firm, ultimately rating it a soft ‘buy’ as a result.

For further details see:

Columbia Sportswear Company: A Decent Prospect At This Time