COLM - Columbia Sportswear: Shaky Q1 Results And Short-Term Headwinds

2023-05-23 13:30:24 ET

Summary

- The footwear segment is off to a slow start to the year due to near-term concerns for U.S. consumers.

- International expansion is going well but the key will be maintaining U.S. share as these markets grow.

- Digital growth has not panned out as hoped with margins contracting in Q1.

- The factors above lead me to a hold rating for COLM.

Introduction

Columbia Sportswear ( COLM ) is down ~13% YTD as the business started the year off slowly. Revenue has grown at a CAGR of 7% for the past 5 years while EPS has grown at 27% over the same time period. Management's current focus is to return value to shareholders by growing key segments of the business while also paying a dividend and buying back shares consistently. My valuation model calculates a fair value of $78.27.

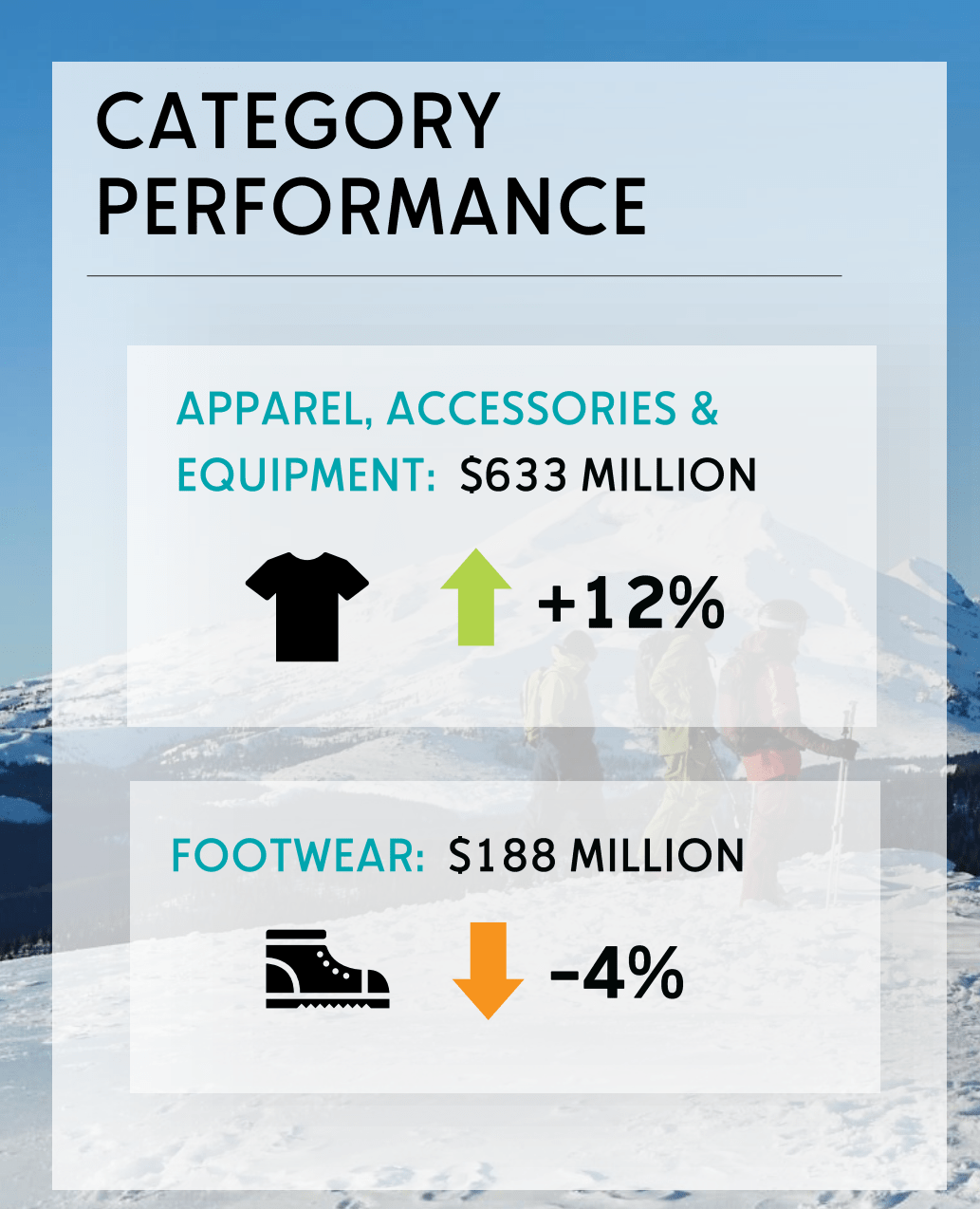

Footwear Business Starts 2023 Off Slow

One of Columbia's key drivers of growth moving forward will be their ability to successfully introduce new products. Currently, they are focusing on growing their footwear brands. Based on the most recent quarterly report , footwear sales are off to a slow start in 2023. The footwear category achieved sales of $188 million, which was a decrease of 4% compared to Q1 of last year. The decrease was largely due to a decrease in U.S. sales of about $15 million. LAAP was flat YoY, EMEA increased~16%, and Canada increased~27%. The positive interpretation of these results would be that the U.S. consumer is facing short-term headwinds currently causing a temporary drop in sales while international growth remains strong. Overall, I believe that more information is needed before a conclusion is reached on whether the slowdown in U.S. sales is temporary or not.

{kind=link}

International Expansion

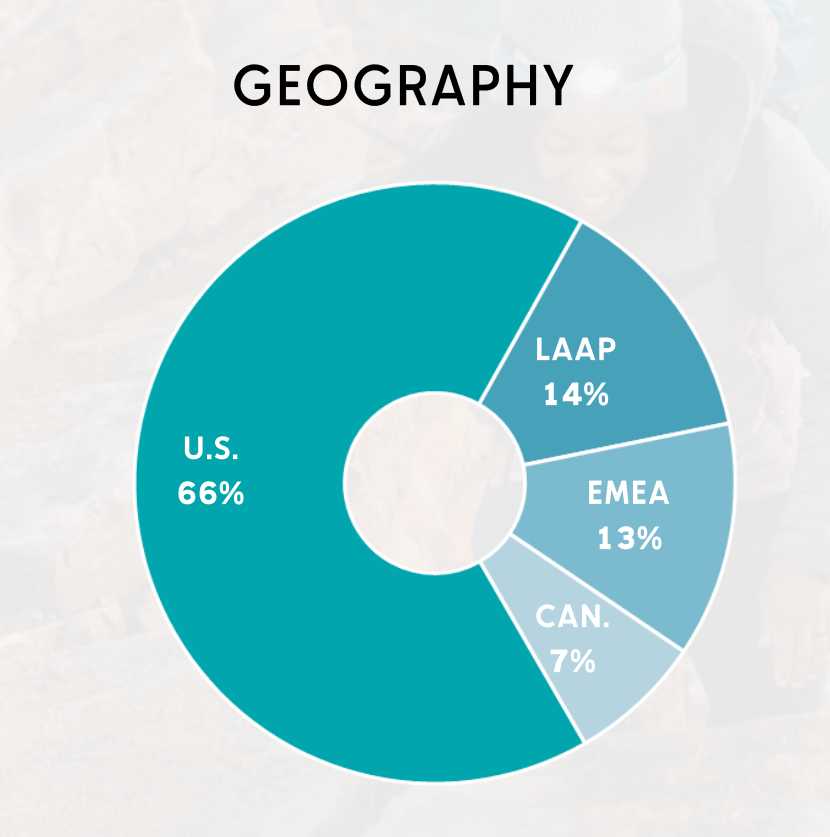

COLM's focus on international expansion seems to be working out well so far. Canada led the way in Q1 with a 35% increase in net sales. EMEA posted a 14% increase and LAAP followed with an additional 12%. The U.S. was able to generate a small gain of 3% for the quarter. Although international growth is positive, these sales still represent a small portion of total net sales. The U.S. remains the majority contributor to revenue at 66%. In order for COLM to continue to grow, they will need to replicate their business model internationally while maintaining their sales volume in the U.S. This will prove to be challenging as we see short-term headwinds for the U.S. consumer.

{kind=link}

Digital Growth

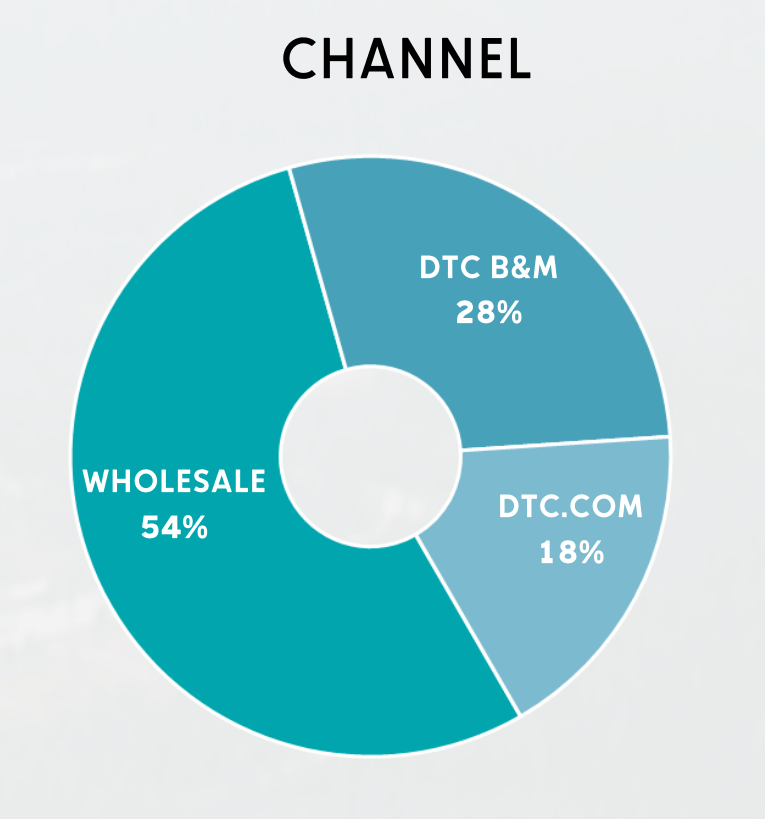

COLM's final lever to drive growth in their business is their digital sales channel. DTC is expected to generate higher gross margins than wholesale due to retail prices being higher. However, there are extra expenses that come along with DTC sales, such as marketing and shipping. This was evident in Q1 as DTC margins contracted due to higher promotional spend as well as freight costs. DTC sales for the quarter increased by 4% while wholesale reported an 11% increase. My conclusion from these results is that DTC will not be as strong a lever to drive growth as the international and the footwear business. Overall, COLM's best option is to continue to focus on growing the first two channels and returning cash to shareholders through dividends and buybacks.

{kind=link}

Valuation & Scenario Analysis

{kind=link}

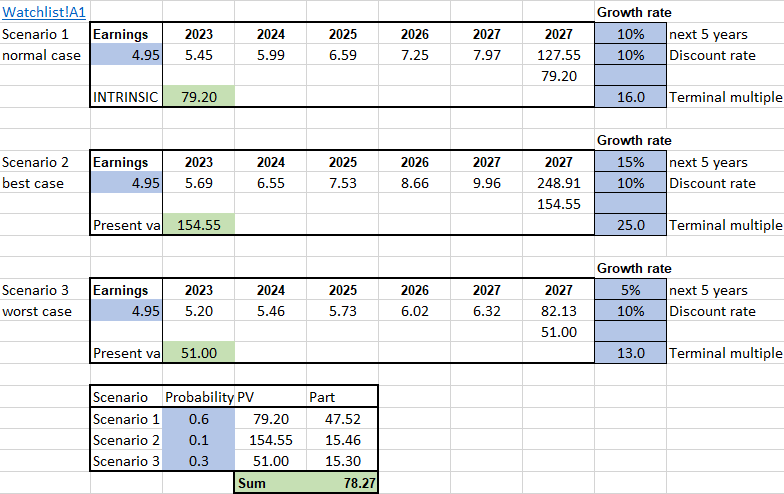

For all my calculations of value, I will be using a discount rate of 10%. 10% is my minimum required return because this has historically been the return you can expect if you decide to just put your money in an index fund that tracks the S&P 500. Lastly, keeping the discount rate the same allows for comparability between different investments.

Also, I assign a weight of 0.6 to my base case, 0.1 to the best case, and 0.3 to my worst-case scenario. With that out of the way, I will move to the individual scenarios.

Scenario 1 is my base case, which assumes 10% growth for the next 5 years with a terminal multiple of 16x. Discounting the 2027 sales price back to present value yields a fair value of $79.20 for an investor with a target return of 10%.

Scenario 2 is my best case, which assumes 15% growth for the next 5 years with a terminal multiple of 25x. Discounting the 2027 sales price back to present value yields a fair value of $154.55 for an investor with a target return of 10%.

Scenario 3 is my worst case, which assumes 5% growth for the next 5 years with a terminal multiple of 13x. Discounting the 2027 sales price back to present value yields a fair value of $51 for an investor with a target return of 10%.

The sum of the weighted PVs is $78.27, implying that the stock is currently fairly valued.

Risks

Potential weakening U.S. consumer

COLM is a consumer discretionary stock which means that it is sensitive to changes in U.S. consumer spending. If we have a recession or experience extended inflation, COLM sales could see a decline.

Loss of brand relevance

Although the Columbia brand is still very much intact, a material slowdown in sales could provide an opportunity for a new competitor to arise and take market share from COLM.

Conclusion

COLM is a solid company with good management. I do have concerns about their elevated inventory and ability to grow their secondary brands.

As a result, I rate COLM a hold.

For further details see:

Columbia Sportswear: Shaky Q1 Results And Short-Term Headwinds