CMCO - Columbus McKinnon: Significant Tailwinds And Undervalued Stock

2023-07-27 23:55:48 ET

Summary

- Columbus McKinnon offers smart mobility products and expects to benefit from global megatrends like automation and digitalization.

- CMCO has impressive financial expectations for the year 2027 and is launching new solutions like Intelli-Connect.

- With a solid balance sheet and expertise in M&A, inorganic growth could lead to significant net sales growth for Columbus.

Columbus McKinnon (CMCO) offers smart mobility products, which are expected to benefit from a significant number of global megatrends including automation and digitalization as well as modernization of infrastructure. The company also offered impressive expectations for the year 2027, and expects successful commercialization of new solutions like Intelli-Connect. Besides, with a solid balance sheet and proven expertise in the M&A markets, I think that inorganic growth could bring significant net sales growth. Even taking into account risks from competitive market, cyclical conditions, or failed M&A, I think that Columbus could trade at a higher price mark.

Columbus McKinnon: Beneficial Market Position, Net Sales Growth, And EBITDA Margin Growth Expected

Columbus McKinnon focuses on design, manufacture, and sale of smart mobility products. Among them are cranes, components for cranes, instruments for high-precision conveyors, light rails, and digital control and drive systems.

{kind=link}

The company focuses its operations on solutions for customers in industrial and commercial areas, achieving a high customer retention rate due to the high quality of services, mainly in the areas of manufacturing, transportation, energy, industrial automation, construction, infrastructure, and different stages of electronic commerce, such as storage and distribution among others.

Columbus appears to be well positioned in different markets. Thanks to the positioning with other products at the local level, a very good portfolio in Europe, and acquisitions in recent years, it has managed to establish active distribution channels and sales. Currently, the company seeks to convert its historical business model as a provider of industrial services to a digitalization service for mobility solutions through the Columbus McKinnon Business System program.

I believe that investors would appreciate having a look at the estimated market share reported and the total addressable market in the lifting, conveyance, automation, and linear motion product categories. I believe that management already has a good position in these markets, but it may be able to acquire other peers without worrying about antitrust issues.

The activities are reported in a single segment of operations, which are, in turn, divided according to the continent in question. In this sense, the company's presence is greater in the United States and Germany, and its operations extend to the rest of Europe, Canada, Oceania, and Latin America to a lesser extent.

With that about the products and international exposure, it is worth noting that the company is expecting to experience significant business growth thanks to several megatrends. Automation and digitalization, e-commerce, and modernization of infrastructure trends are expected to significantly enhance the growth in several markets in which Columbus sells.

I made my own assumptions and forecasts for Columbus, however readers may have a look at the expectations of other analysts. In this case, market analysts expect net sales growth, EBITDA increases, FCF growth, and net margin increase.

More precisely, investors are expecting 2025 net sales of close to $1.047 billion, 2025 EBITDA of $178 million, 2025 EBIT of $128 million, 2025 net income of $69.3 million, and free cash flow close to $98.8 million.

Source: Marketscreener.com

Balance Sheet

In the last balance sheet reported in 2023, Columbus saw an increase in the total amount of assets driven by increases in cash, accounts receivables, inventories, and prepaid expenses. The increase is not significant, however most investors would most likely appreciate the tendencies seen in the financial statements. At the same time, the decrease in total liabilities is quite appealing. Further increases in the asset/liability ratio or lower debt would most likely accelerate the demand for the stock.

In the annual report, the company included cash and cash equivalents worth $81 million, trade accounts receivable worth $146 million, and inventories of about $200 million. Also, with prepaid expenses of about $34 million, property, plant, and equipment stood at $94 million, and goodwill was equal to $642 million. Finally, total assets were equal to $1.649 million, and the asset/liability ratio stood at close to 2x.

Source: 10-Q

The list of total liabilities does not really look worrying. Columbus reported trade accounts payable of about $70 million, accrued liabilities close to $104 million, current portion of long term debt and finance lease obligations worth $40 million, and total liabilities of $838 million.

Source: 10-Q

Financial Model

Columbus is currently applying its secular growth strategy in order to increase the offer of digital services, and is changing the historical core of the company's business. This strategy is based on strengthening the core through the development of new product lines or technological innovation in existing ones, with a focus on digital tools that serve the experience of its consumers. Under my financial model, I assumed that further implementation of digital tools will accelerate net sales growth and net income margin. The following figures are part of my DCF model. I believe that both sales growth and net income growth appear conservative.

{kind=link}

I also assumed further successful increase in the position in certain markets through organic growth and future acquisitions. Considering the successful operations in certain territories, I believe that gaining access to new sales channels and customers and achieving global expansion will most likely be possible. The company disclosed a list of initiatives in a recent presentation, but I would highlight that management intends to find new channel partners and offer next generation platforms and product developments with regards to automation, monitoring, and diagnostics.

Among the specific strategic intents discussed, Intelli-Connect appears quite promising. The solution offered includes easy programming, remote access capabilities, and real time actionable information. The solution is expected to improve end user's safety, productivity, and uptime. Successful commercial implementation and marketing of these solutions would most likely lead to net sales growth.

Source: Presentation to Investors

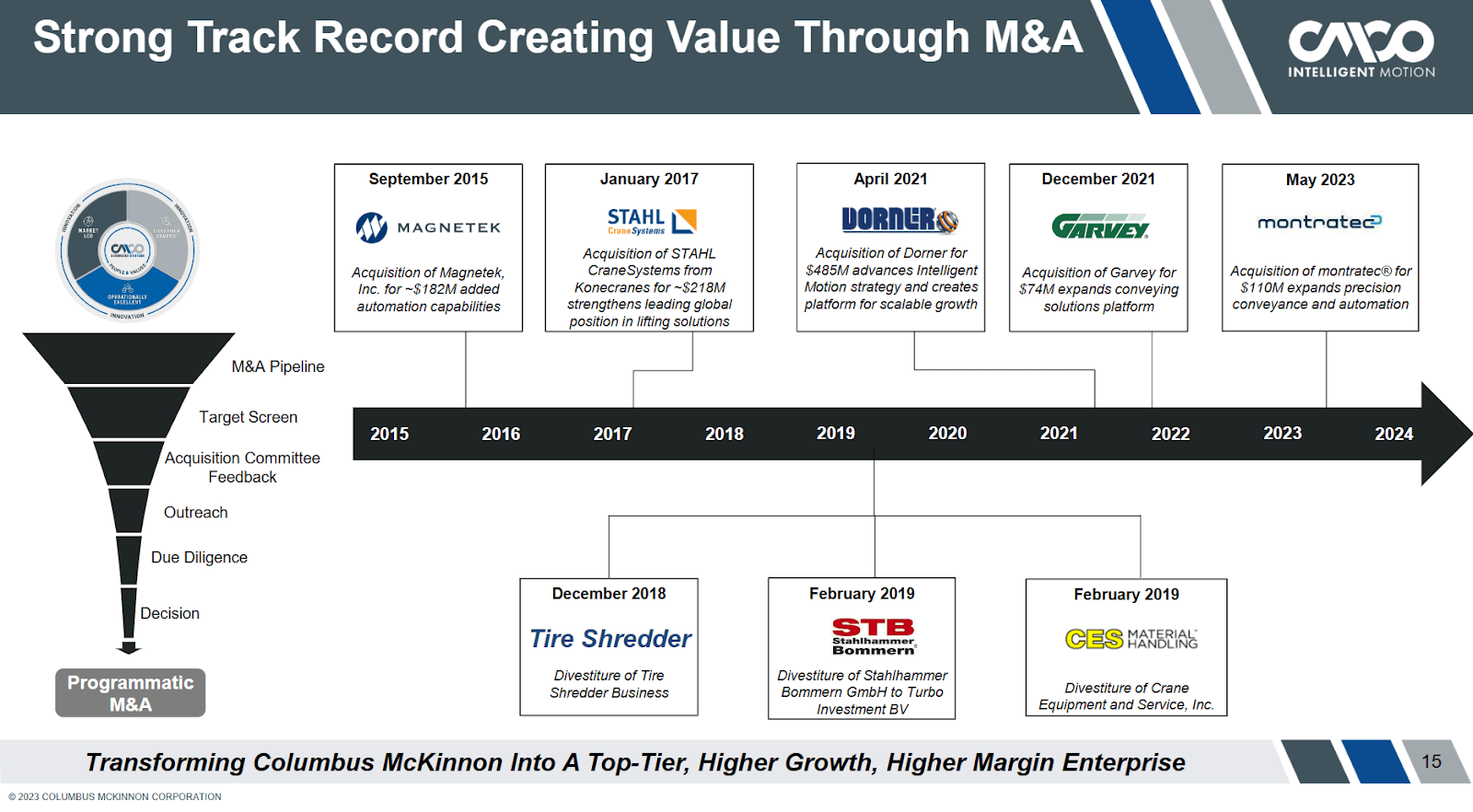

With goodwill being around $644 million, Columbus clearly has accumulated a lot of expertise in the acquisition of peers. I believe that the current state of the balance sheet will most likely allow new transitions. If new acquisitions successfully increase automation and remote monitoring, and recurrent revenue also creeps up, I would expect a lot of interest from outside investors. Besides, we could expect net sales growth and EBITDA margin increases.

{kind=link}

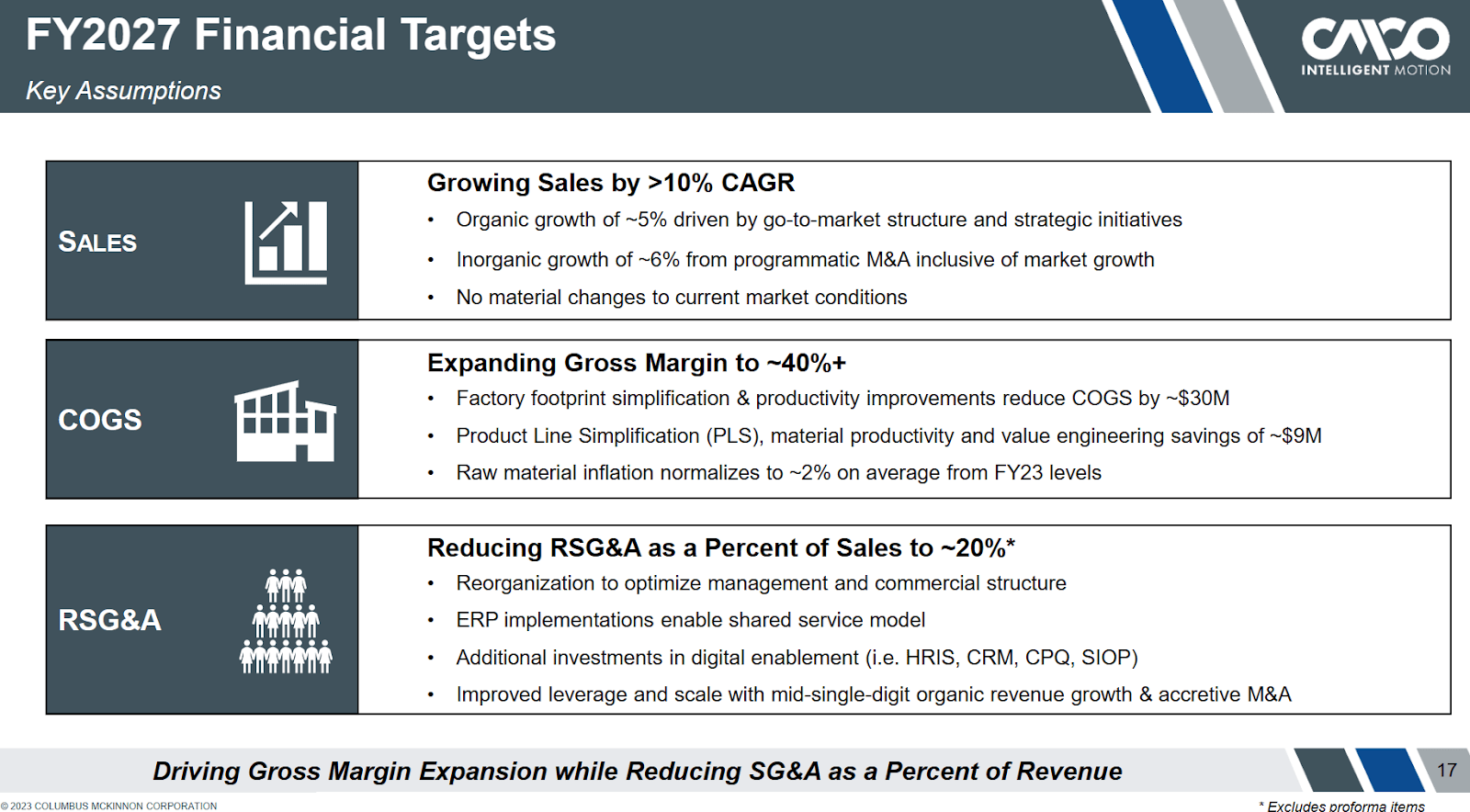

Columbus appeared to be quite optimistic in terms of future net sales growth and profit margins. The company expected growing sales by close to 10% CAGR and gross margin increasing to close to 40% as well as certain reorganization to optimize management and commercial structure. My numbers are a bit more conservative, but I also expect net sales growth from now to 2033 along with FCF margin increases.

{kind=link}

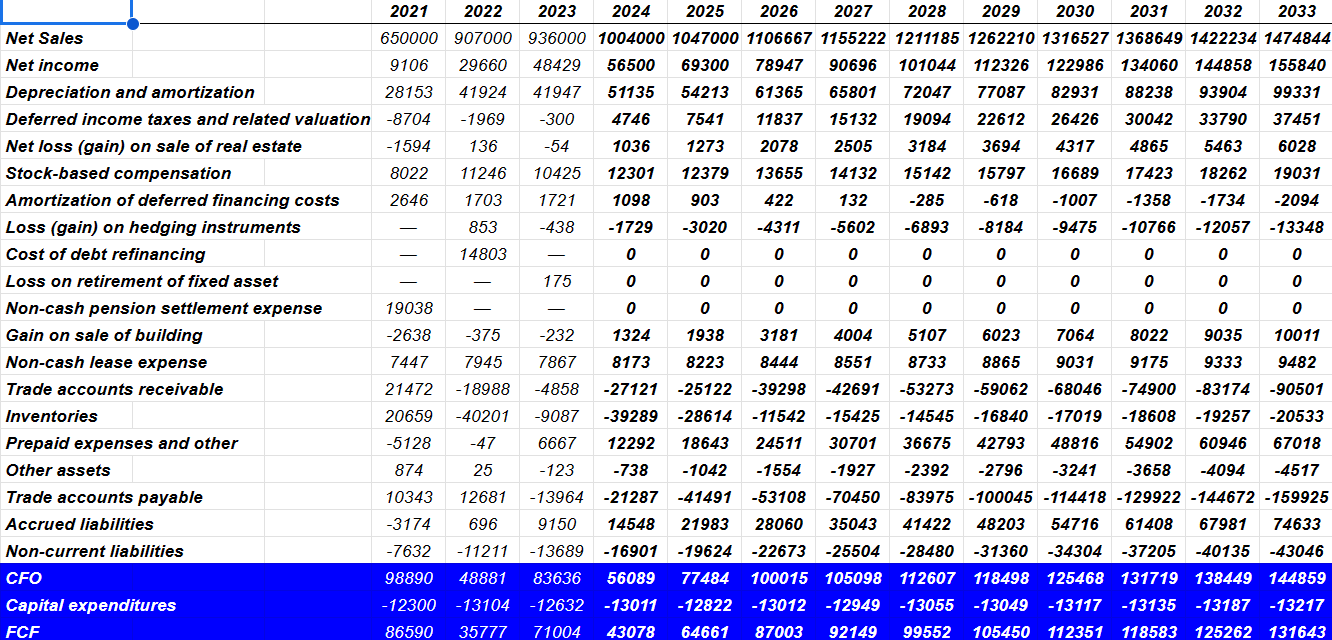

My numbers included 2033 net sales of about $1.474 billion, 2033 depreciation and amortization of about $99 million, deferred income taxes and related valuation worth $37 million, and 2033 stock-based compensation of $19 million.

Also, with 2033 changes in trade accounts receivable of about -$91 million, changes in inventories of -$21 million, and prepaid expenses of about $67 million, I also assumed 2033 changes in trade accounts payable of about -$160 million.

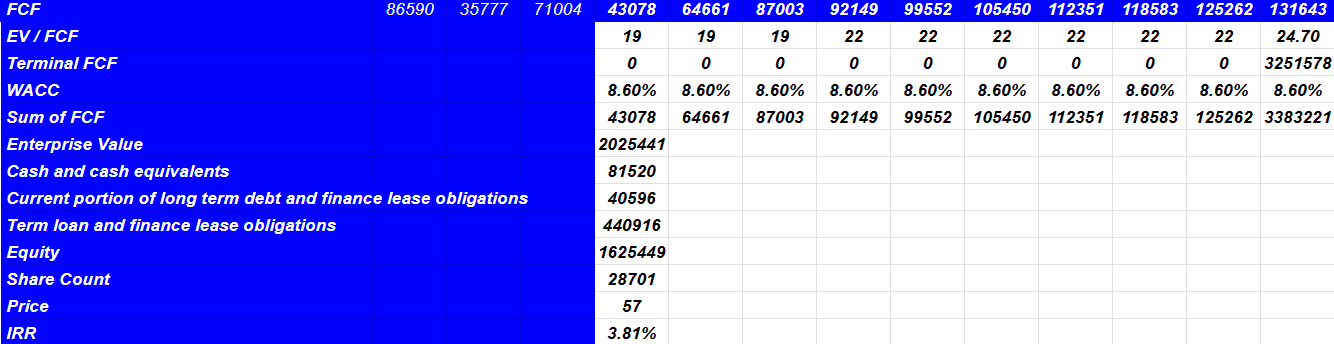

Finally, taking into account 2033 changes in accrued liabilities of $74 million, 2033 CFO would be close to $144 million, and with 2033 capital expenditures worth -$14 million, 2033 FCF would be $131 million.

{kind=link}

I also included an EV/FCF ratio of 24.7x, which implied an enterprise value of $2.025 billion. Note that the 10 years median, 5 years median, and 3 years median EV/FCF stand at about 19x-26x, so I believe that my EV/FCF multiple appears reasonable.

Source: Ycharts

If we also add cash and cash equivalents of about $81 million, and subtract current portion of long term debt and finance lease obligations of $40 million and term loan and finance lease obligations close to $440 million, the implied equity valuation would be $1.625 billion, and the implied price would be $57 per with an IRR of 3.8%.

{kind=link}

Fragmented Market

The market appears to be a fragmented market that has not been able to consolidate over the years, where there are a large number of participants at a regional, national, and international level. All of them have their own manufacturing facilities. In some cases, individual operating units of companies with greater diversification in their product offerings are added. The competition is driven mainly by the customer support, advice service, and the price and quality offer.

Some of the most renowned competitors that we can find are Konecranes (KNCRF) and Kito for cranes and hoists, Campbell Chain, Peerless Chain Company, and American Chain and Cable Company for chains, Konecranes, Power Electronics International, Inc., Cattron Holdings, Conductix-Wampfler, Control Techniques, OMRON Corporation (OMRNY), KEB GmbH, and Fujitec (FJTCY) in digital motor systems.

Risks

Columbus operates in a highly competitive market and cyclical conditions tied directly to the state of the global economy and its variations. In this sense, the scope of favorable prices at the time of sales and access to certain raw materials are risk factors in relation to the company's business model.

Many of the end-users of our products are in highly cyclical industries, such as manufacturing, power generation and distribution, commercial construction, oil and gas exploration and refining, transportation, agriculture, logging, and mining that are sensitive to changes in general economic conditions. Their demand for our products, and thus our results of operations, is cyclical and directly related to the level of production in their facilities, which changes as a result of changes in general macroeconomic conditions, including, among others, movements in interest rates, inflation, changes in currency exchange rates and higher fuel and other energy costs, and other factors beyond our control, and is vulnerable to economic downturns. Source: 10-k

Internationally, Columbus has assets located in more than 50 countries, and the bulk of the profits from countries outside the United States is considerable. In addition, the exposure to legal and regulatory conditions in each of these as well as variations in exchange rates and interest rates are also risk factors.

Ultimately, the company's operations are subject to future variations in environmental legislation as well as regulations for the markets in this sense, which may eventually mean a complication, especially in the event that this begins to change the way of conceiving industry.

In my opinion, the only extreme case that I can project is if a transformation strategy towards digital services fails to be carried out, and due to new industry trends, other companies take positions in larger markets and displace the position of the company.

Conclusion

Columbus McKinnon offers smart mobility products and impressive financial expectations for the year 2027. The company noted in the most recent annual report that the business is expected to benefit from a list of megatrends like automation and digitalization, e-commerce, and modernization of infrastructure trends. Besides, the company is also launching new products like Intelli-Connect, which I believe will most likely enhance future revenue growth. Finally, with a solid business balance sheet and a lot of expertise in the M&A markets, I would expect significant inorganic growth in the coming years. Yes, there are some risks from the competitive market, cyclical conditions, supply chain disruptions, or lack of access to certain raw materials. With that, I believe that Columbus could trade at a higher price mark.

For further details see:

Columbus McKinnon: Significant Tailwinds And Undervalued Stock