CMA - Comerica: Holding Strong And Highly Liquid With 5% Dividend Yield Despite Earnings Declines

2024-01-08 06:49:26 ET

Summary

- Comerica downgraded to Hold today from its previous Strong Buy this summer.

- Nice 5% dividend yield and dividend income growth in last decade.

- Relatively flat or declining revenue, earnings, and equity growth lately while share price trading double-digits above moving average as banking sector bullish.

- Low exposure (6%) to office property loans, however longer trend of office defaults in 2024 overall remains to be seen and could impede confidence in regional banks.

Stock & Industry Snapshot

In this weekend's research note, considering that bank stocks lately have seen considerable bullishness I wanted to pick an under-covered but well-established regional US bank that I can still get for less than $60/share.

One that fits that profile is Dallas-based Comerica ( CMA ) , the parent of Comerica Bank .

For my readers less familiar with this bank, a few relevant facts are that it has been around for +174 years, boasts about its conservative lending standards, has 400 banking centers around the US with particular market penetration in its home market of Texas and the southwest but also recent expansion efforts into the southeast region.

My own experience with this banking brand was that I happened to work for another company in 2015 located in the Comerica tower in downtown Austin, Texas, and as my equities research firm is also founded in Texas this company along with Frost Bank is a common sight in the state's capital city and its growing skyline.

It also is relevant to mention it is based in a state that had experienced one of the largest influx of newcomers (and potential banking customers) and economic growth in history. In fact, a recent Newsweek article this month mentioned that Texas "registered nearly 8 percent economic growth in the third quarter of 2023, higher than the national expansion of about 5 percent."

As for my history in picking this stock, since my last rating of this stock in late August, when I called it a strong buy , by now it has gone up almost 18%.

Comerica - price since last rating (Seeking Alpha)

Recent sector performance from SA market data indicates financials have gone up +29% in 3 years and +9% in the last year. We also saw their spike in December after the recent Fed meeting as well.

Comerica - financial sector (Seeking Alpha)

I would argue that this sector has begun its road to recovery particularly after the market punished it last spring during the Silicon Valley Bank failure.

Any earnings data for Comerica will refer to the most recent FY23 Q3 results (official press release and investor presentation) that came out on Oct. 20th, while future expectations may relate to the Q4 results coming out in a few weeks on Jan. 19th.

Scoring Matrix

We use a 9-point scoring method that looks at this stock holistically and assigns a total rating score, using a score matrix. The matrix follows a logical sequence. For example, we discuss earnings and share price before discussing the price-to-earnings valuation.

{kind=link}

Today's Rating

Based on the score total in the score matrix , this stock is getting a rating of hold.

This is a downgrade from my previous strong buy rating last summer.

Compared to the consensus rating on Seeking Alpha, this time around I am agreeing with the consensus from analysts and the quant system, but am more cautious than Wall Street.

Comerica - rating consensus (Seeking Alpha)

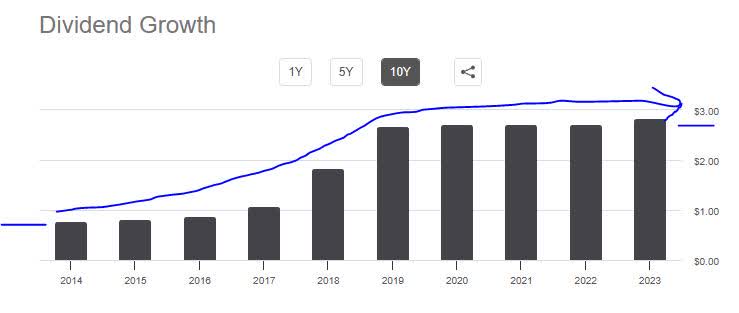

Dividend Income Growth

The first metric I care about as a dividend-income investor putting together a dividend-income portfolio, is what kind of 10 year dividend growth history this stock has and also future potential growth.

Have a look at its 10 year dividend chart :

{kind=link}

If I had added 100 shares in this stock to my portfolio, let's say, in 2014, I would have seen $0.79/share/annually ($79 annual dividend income) vs $2.84/share/annually in 2023, which is a +259% growth over 10 years.

Though I have not seen any announcement for 2024 dividend hikes, I will make an educated guess from the income statement showing earnings declines in the recent quarter and the cash flow statement showing negative free cash flow per share that there is a lessened probability of dividend hikes in the immediate future, though not impossible.

This is based on the assumption that growth in profits leads to a greater chance of dividend hikes and returning that profit growth back to shareholders.

Still, what favors them is the $0.71/share quarterly payout and the stable history of quarterly payouts.

Therefore, in this category I call it a buy rather than a strong buy, based on stable payouts, a relatively high payout per share, and proven 10 year growth in the triple digits, while an offsetting factor is the lower potential for dividend hikes in the near future.

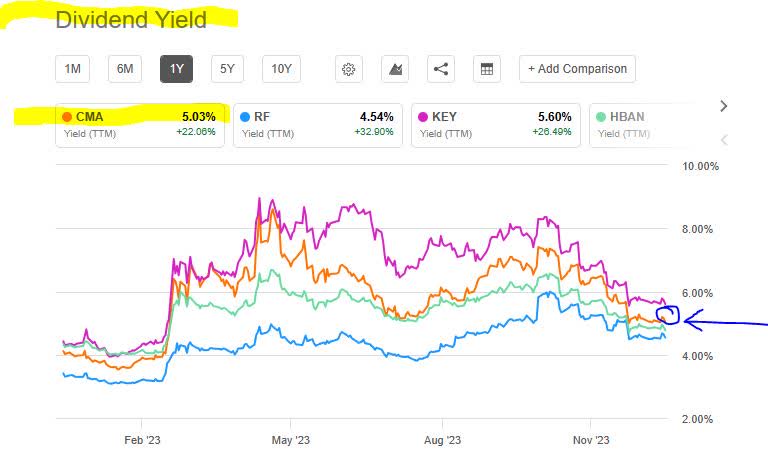

Dividend Yield vs Peers

Next, I want to turn your attention to the dividend yield comparison tool and in it I will be comparing Comerica's dividend yield against three peers in the regional banking space.

The goal is to find the best dividend yield for my capital invested at the current share price, since for example a $0.70 dividend does not mean the same for a stock trading at $50 vs a stock trading at $300. I certainly encourage you to try this tool from Seeking Alpha as it has helped me greatly in comparing similars.

{kind=link}

In this comparison, Keycorp ( KEY ) leads the pack with a yield of 5.60%, however my focus stock Comerica is not far behind at 5.03% yield.

Trailing behind are Huntington Bancshares ( HBAN ) with 4.77% and Regions Financial ( RF ) at 4.54%.

The question is whether continued share price growth will pull the yield down. I think it could, but more so because the sector itself is bullish lately. The company, however, has seen declines in both revenue and earnings in the most recent quarterly result.

So, in this category I think it still makes sense to call this stock a buy and snag the +5% yield before it drops, since 5% is a pretty solid yield in my opinion considering that the sector average is 3.35%.

Revenue Growth

That brings me to the next topic which is top-line revenue growth, and the income statement tells us a story about that.

We see that total revenue dropped to $882MM in the quarter ending September, vs $957MM in Sept 2022, a 7.8% YoY decline.

From the same income statement we can see that although non-interest income grew it seems that net interest income fell on a YoY basis. A driver of this appears to be the interest expense going up to $502MM vs $43MM in Sept. 2022, an over +1,000% YoY increase in the interest expense.

I have seen this with some banks where the net interest margin is squeeze in the current high rate environment which drives both interest income up as well as interest expense on items like consumer deposits and bank borrowing in the money markets.

In fact, the company in their Q3 results press release commented:

Net interest margin decreased 9 basis points to 2.84%, primarily reflecting higher-cost funding sources.

My outlook for the end of FY23 and first quarter of FY24 when it comes to revenue is cautious, since we are still in a high rate environment that can impact net interest income unfavorably at this bank and according to rate tracker CME Fedwatch the likelihood of a Fed rate decrease is not expected until the March meeting (a 62% probability of a rate drop).

My call here would be a hold , based on single-digit YoY revenue declines and continued expected pressure on net interest income, while non-interest income has not really made up for it.

Earnings Growth

Returning to the income statement again, now let's talk about net income (earnings).

The data tells us that earnings dropped to $251MM, vs $351MM in Sept 2022, a 28% YoY decline.

I would point out that non-interest expenses were not a huge driver of declining earnings, as they appear to have grown just 11% YoY.

In addition, the company remarked in their Q3 presentation that "noninterest income remained robust with only a modest decline largely driven by deferred compensation."

It appears to me the key driver of weakened earnings is the decline in top-line net interest income. Looking forward to full-year 2023 results, in fact, the company in their Q3 presentation expects net interest income to grow just "+1 to 2% (vs FY22), reflecting benefit of full-year average loan growth offsetting impact of increased funding & deposit costs."

In this section I would call it a sell , on the basis of double-digit earnings declines and relatively low net interest income forecasts.

Equity Positive Growth

We can get a picture of this firm's equity (book value) from its balance sheet , which tells us that total equity fell to $4.97B vs $5.06B in Sept 2022, a YoY decline of 1.7%.

This is practically a flat growth in equity, so nothing significant either way.

Another figure I want to mention is that company long-term debt declined slightly as well, a good sign I think.

This being a bank, within this talk of assets and liabilities I also like to mention the CET1 ratio which is a Basel III regulatory item. From their Q3 presentation, we see that CET1 jumped up to 10.79% , well above regulatory minimums and the company's own target of 10%.

In addition, the company is in a strong position in terms of liquidity with +$45B liquidity capacity including +$20B in untapped funding from the Fed's discount window :

Comerica - liquidity (company q3 presentation)

In this section I would call this a hold , based on the data showing flat growth in book value, but offset by positives such as an improving CET1 ratio and really strong liquidity.

Share Price vs Moving Average

The following yChart shows the share price as of Friday's close, and its relationship vs its 200-day SMA, which is a metric I prefer as it smoothes out price volatility over a longer term, in this case 200 days.

Right now the share price is trading at a +27% premium to the 200-day SMA.

At the same time, the company saw declines in both revenue and earnings and flat equity growth, however also offers a +5% dividend yield opportunity.

I would argue that although the dividend yield is compelling, the double-digit share price growth vs its average and also +$20/share higher than its autumn lows, while revenue/earnings/equity have not grown at the same time, shows that the sector bullishness may have been pulling this stock up with it.

For that reason, I am compelled to call it a hold rather than a buy. I think the sector can pull it up some more, but it also lacks the earnings growth right now that I look for in a great buy opportunity.

Valuation: Price-to-Earnings

It is important to consider valuation data after having already discussed share price and earnings.

We can see this data tells us the forward P/E ratio is now 7.71 , about 30% less than the sector average which is close to 11x earnings.

When comparing to the share price and earnings data discussed, I think it is an OK multiple considering that earnings growth did not keep up with share price growth but rather declined by double digits.

I would not call it a great multiple, and that is the reason why, because the share price is somewhere around +60% above its autumn lows and double-digits above its moving average yet earnings did not grow.

So, I will call it a hold at this valuation, and also want to point out that it presents a much better valuation than regional banking peer KeyCorp whose forward P/E is near 15x earnings even while its earnings saw a double-digit YoY decline. That would be an example I would give of overvaluation that is not justifiable.

Valuation: Price-to-Book Value

Also from valuation data we can see the rift between share price and book value (equity).

We can see the forward P/B ratio is 1.54, only about 30% above the sector average which is trending around 1.18x book value.

It seems to me the driver of this slightly elevated multiple is the overly bullish share price, while at the same time equity growth was practically flat or on a single-digit YoY decline. This is creating this gap between price and book value here.

From the peer group, in terms of P/B ratio I would have picked Huntington Bancshares as their forward P/B multiple is only 1.16 yet also have a roughly +8% YoY growth in book value according to their balance sheet . That is a great combination I am looking for, a low price multiple and growth in equity.

In this context, I am compelled to call Comerica a hold because although their P/B multiple is not overly high it does not present a great buy right now, due to the rift between rising price growth and flat equity growth.

Risk Analysis

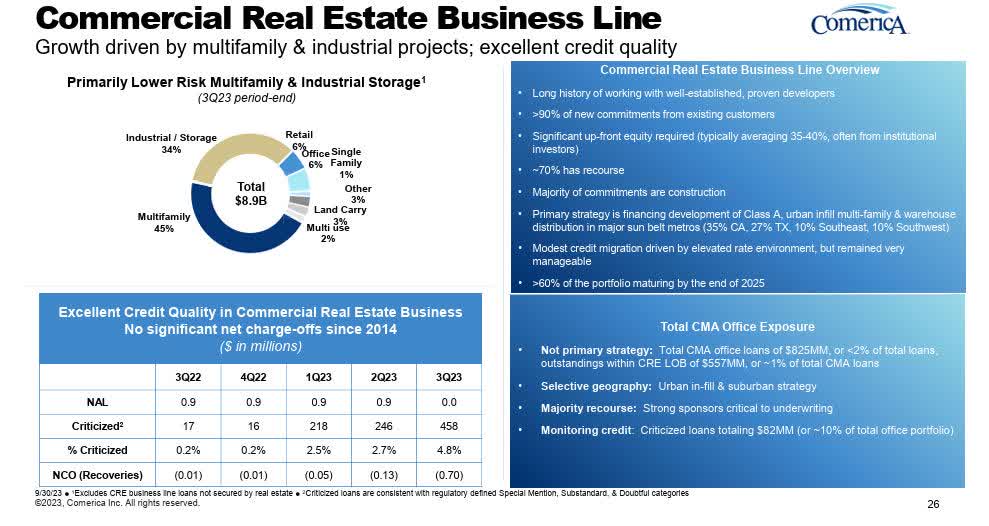

This being a regional bank, the potential risk I would focus on this time is exposure to commercial real estate.

Headlines going into 2024 include "office will continue to face the most strain" according to a January article in Fortune magazine , a piece in Business Insider from 2 weeks ago highlighting that "the commercial real estate sector is at risk of seeing its biggest crash since 2008, and that could slam US banks with up to $160 billion in losses," while at the same time the National Association of Realtors pointed out that "in 2023, the industrial sector maintained its status as the standout segment with the most robust growth among all categories within the commercial real estate market in 2023."

With that said, here is an overview of this bank's CRE exposure, according to their own Q3 presentation:

{kind=link}

We can see from the graphic that Comerica's largest CRE exposure is tied to multifamily and industrial properties, which I think favors it considering what I just mentioned about industrial property. Its exposure to office is down to just 6% of the CRE portfolio, so barely 1/10th of the CRE loan book. Any continued downturn in the office segment, therefore, should not post a systemic danger to this firm.

However, we can also see that the % of criticized loans (substandard / higher risk of loss) has jumped in Q3 to just under 5%, whereas in 3Q22 it was at 0.2%, and between these periods there is a steady increase in the criticized loans ratio.

If you look at the glass half full, though, that means that around 95% of their CRE loans are non-criticized, and therefore likely in good standing.

So, in terms of risk impact I think headwinds to the office sector will have low impact on this bank's portfolio, and in terms of risk probability it is more like moderate right now.

For that reason, in terms of this downside risk I think it is more about how the larger market perceives it and whether fear-centric selling occurs in bank stocks if several large office properties suddenly default on their loans this year, which is an open question. We saw the fear-based selloff in banks after just two regional bank failures last spring, even a selloff of perfectly good bank stocks for fear of systemic contagion.

So, this being a regional bank, I am more inclined to say hold right now than buy, as I think the regionals could be hit first with any type of panic selling if and when it occurs in 2024. Right now the offsetting factor could be the likelihood of Fed rate drops, and the cost of debt coming down but also more people returning to the office than before.

Quick Summary

To briefly summarize, in today's re-rating I'm downgrading to hold from my previous strong buy last summer.

Though a +5% dividend yield is compelling, headwinds include a bloated share price growth while earnings /revenue/equity have declined or been flat.

The bank's exposure to higher-risk real estate loans like office property is low, but there this the potential perceived risk by the market if more prominent office properties begin defaulting in 2024, which could spook investors away from bank stocks again. That is the canary in the coal mine right now, so to speak.

My portfolio strategy here would be to hold on to this stock, particularly if I had bought during the spring or autumn price dips because I am already seeing a double-digit upside right now, and if things stabilize in the office market we could see further bullishness in banks, at which point I would either continue to hold for the quarterly dividend income or would sell at a 20 to 30% capital gain at least.

For further details see:

Comerica: Holding Strong And Highly Liquid With 5% Dividend Yield, Despite Earnings Declines