CMA - Comerica Is Fairly Priced Relative To Peers

2024-01-18 17:41:03 ET

Summary

- Comerica's recent rally has jacked up the firm's price-to-tangible book value multiple above its peer group average.

- Bad debt-related headwinds may prove costly to the firm's bottom line resulting from sustained interest rate hikes.

- Price target: $47 to $60.

Ahead of Comerica Incorporated's ( CMA ) newest earnings report on January 19th, I believe investors should sell the firm's shares.

My last article about Comerica, published on October 4th, argued that the bank had been unfairly beaten down following the March 2023 banking crisis. Moreover, the usage of intrinsic and extrinsic valuation methodologies confirmed the notion that Comerica was undervalued. This was confirmed following the firm's Q3 2023 earnings report where Comerica beat earnings and revenue estimates. So what has changed? The firm's shares have rallied since October 4th, posting a ~34% gain compared to the S&P 500's ~12% appreciation in value. This has altered Comerica's quantitative valuation. Moreover, the firm's underlying fundamentals are not as robust as they were in early October.

Catalysts

Comerica's current valuation is affected by the following key areas:

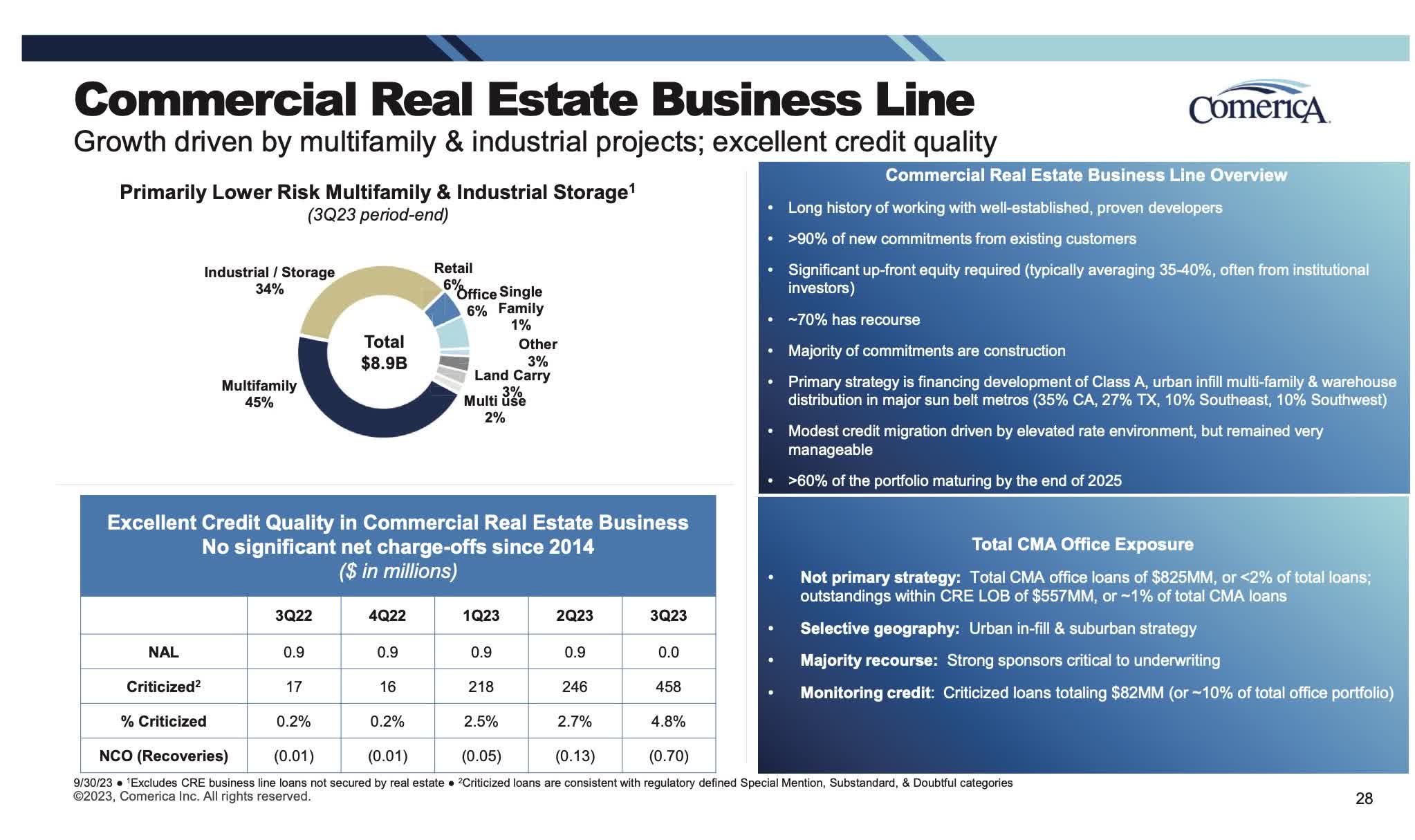

1. Commercial Real Estate Exposure

The firm's CRE exposure grew slightly between Q2 2023 and Q3 2023 from $8.5 billion to $8.9 billion. This is not bad in itself, but concern abounds when one looks at the growing number of criticized loans within Comerica's CRE portfolio. This grew to 4.8% from 2.7% over the quarter. Fortunately, Comerica's underwriters have wisely built in recourse measures to ~70% of all CRE loans. This should allow the company to recover some assets in the case of default. Moreover, the firm's lending strategy has concentrated on Class A development which tends to be less risky than other CRE loans. Comerica's Q4 report should provide more clarity into the effects of lingering CRE issues stemming from rising borrowing costs .

Comerica Q3 2023 Investor Presentation

{kind=link}

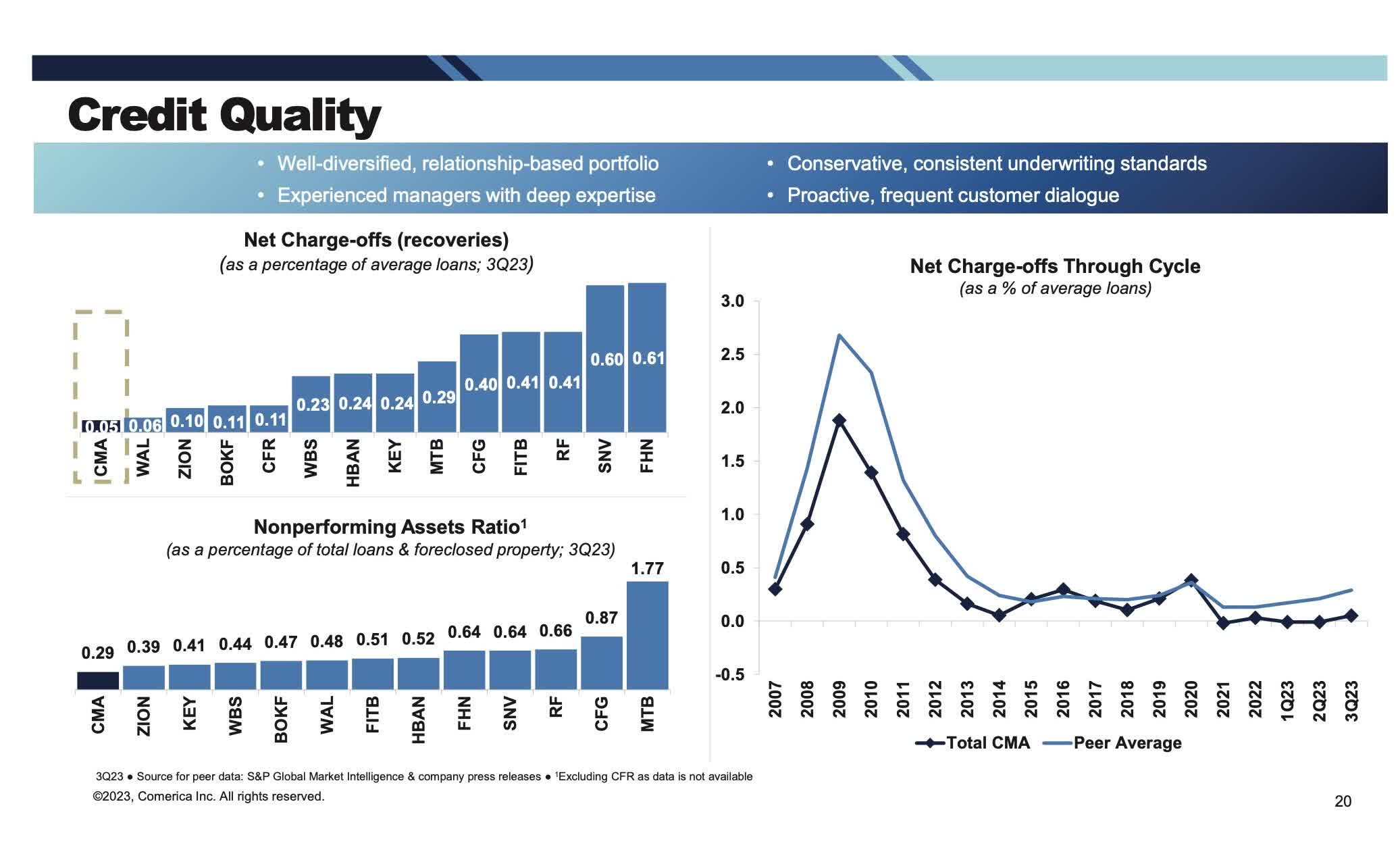

2. Net Charge-Offs

Credit quality is of increasing importance as interest rates have risen. Comerica has experienced a slight uptick in net charge-offs throughout its loan portfolios. Moreover, the firm has shown some ability to recover assets from these delinquencies. This could still become a drag on Comerica's balance sheet and will be interesting to investigate the extent of this rise during Q4 2023 and Q1 2024.

Comerica Q3 2023 Investor Presentation

{kind=link}

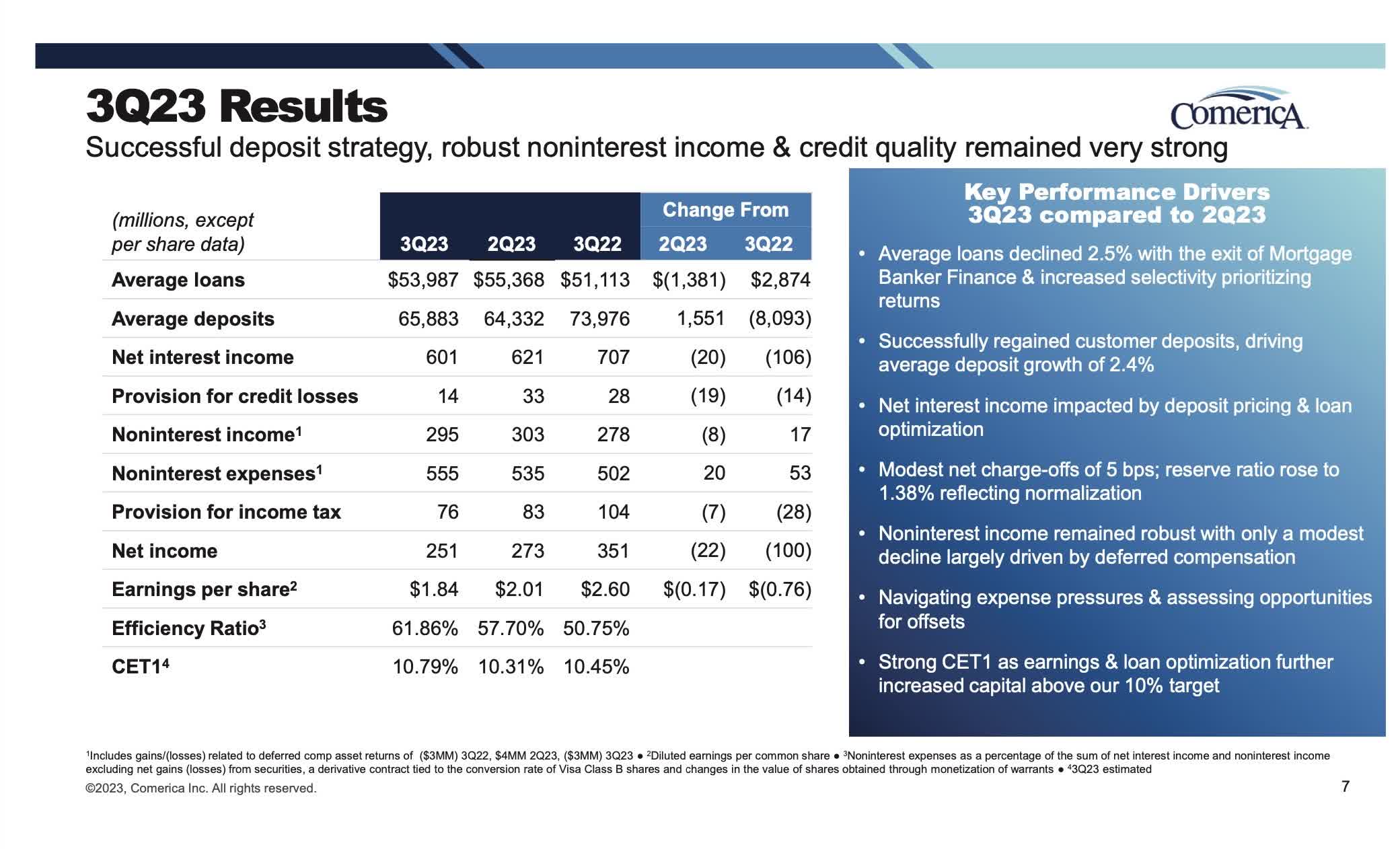

3. Loan and Deposit Growth

Comerica's aggregate loans fell slightly between Q2 2023 and Q3 2023. In addition, the firm's deposits rose slightly over the same period. Changes in loans and deposits both impact Comerica's bottom line as they are indicators of the firm's profit-generating capabilities. Unfortunately, the firm has been unable to recapture its net interest income from 3Q 2022. Much of this can be attributed to industry-wide banking headwinds, but it is reasonable to believe that Comerica may face more downside pressures in its loan and deposit growth.

Comerica Q3 2023 Investor Presentation

{kind=link}

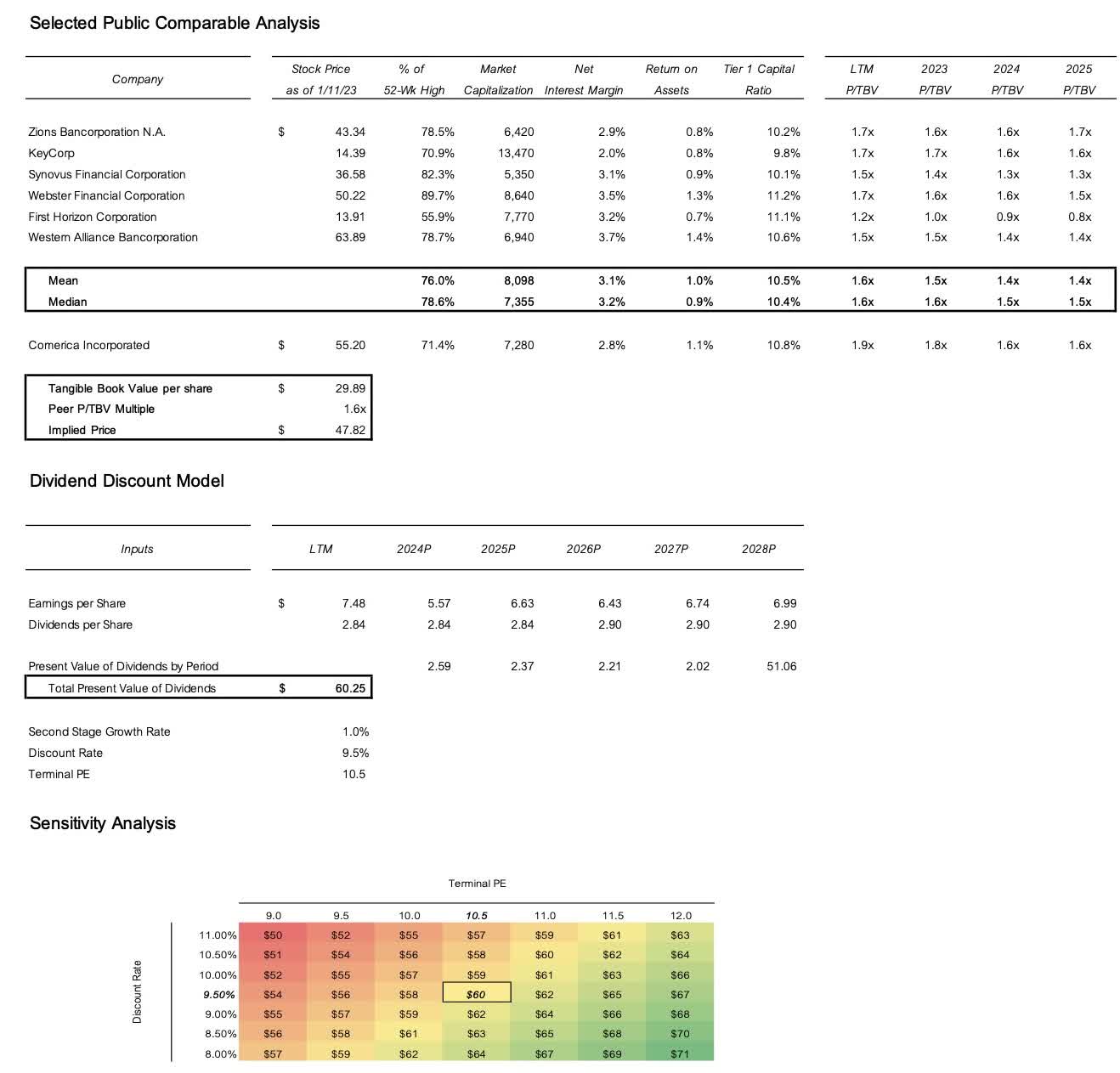

Valuation

My last Comerica valuation model is linked in my previous article about the firm. There are a few updates that are worth noting:

- The peer group of Zions Bancorporation, National Association ( ZION ), KeyCorp ( KEY ), Synovus Financial Corp. ( SNV ), Webster Financial Corporation ( WBS ), First Horizon Corporation ( FHN ), and Western Alliance Bancorporation ( WAL ) still seems appropriate. This is a result of similar market capitalizations, deposit bases, and branch networks between each firm.

- In October, Comerica's price-to-tangible book value (P/TBV) multiple was equal to the means and medians of its competitors' multiples. Small changes in TBV and price since then have yielded a higher multiple for Comerica relative to its competitors. These factors imply that Comerica is no longer cheaply priced relative to its peers.

- Comerica's valuation based on future cash flows in the form of dividends was cut to be more conservative. However, near-zero growth in dividends still implies that the firm has some upside. This is a good sign for investors who believe squarely in the merits of valuing a company according to its cash flows.

{kind=link}

Conclusion

It pains me to put a sell rating on Comerica as I still think that it has some upward movement left. Perhaps the firm even beats earnings on Friday. The bottom line is that I like the firm, just maybe not at this price. If shares trade closer to $40, I will likely suggest another buy rating because Comerica still has best-in-class fundamentals compared to competitors. It is hard to argue with the firm's unit economics, especially from a net recoveries standpoint where it is better than almost every other regional bank. Unfortunately, Comerica no longer provides an attractive margin of safety to be considered a true value pick.

For further details see:

Comerica Is Fairly Priced Relative To Peers