FIX - Comfort Systems USA: Normalizing Growth And Premium Valuation

2023-11-30 06:41:05 ET

Summary

- Comfort Systems USA's revenue growth is expected to continue benefiting from a healthy backlog and demand in the industrial, technology, and manufacturing sectors.

- However, the high growth rate seen in the past year is expected to normalize, and the company's margin outlook is mixed.

- The stock is trading above historical averages, and there is little margin of safety at current levels, leading to a neutral rating.

Investment Thesis

Comfort Systems USA, Inc's (FIX) revenue growth should continue to see benefits from a healthy backlog of $4.28 billion exiting Q3 2023, and good demand in industrial, technology, and manufacturing sectors driven by medium to long-term secular trends. However, the streak of extraordinarily high growth rate that the company has been witnessing over the last year should likely end in the coming year as the growth rate is expected to normalize. On the margin front, the company's outlook is currently mixed with moderating inflation helping, but fewer price increases as well as lower margin modular business hurting.

In addition to normalizing revenue growth rate and mixed margin outlook, the valuation also seems unfavorable as FIX is trading above historical averages due to the high growth seen over the past few quarters. I believe there is little margin of safety at the current levels. Hence, I continue to have a neutral rating on the stock.

Revenue Analysis and Outlook

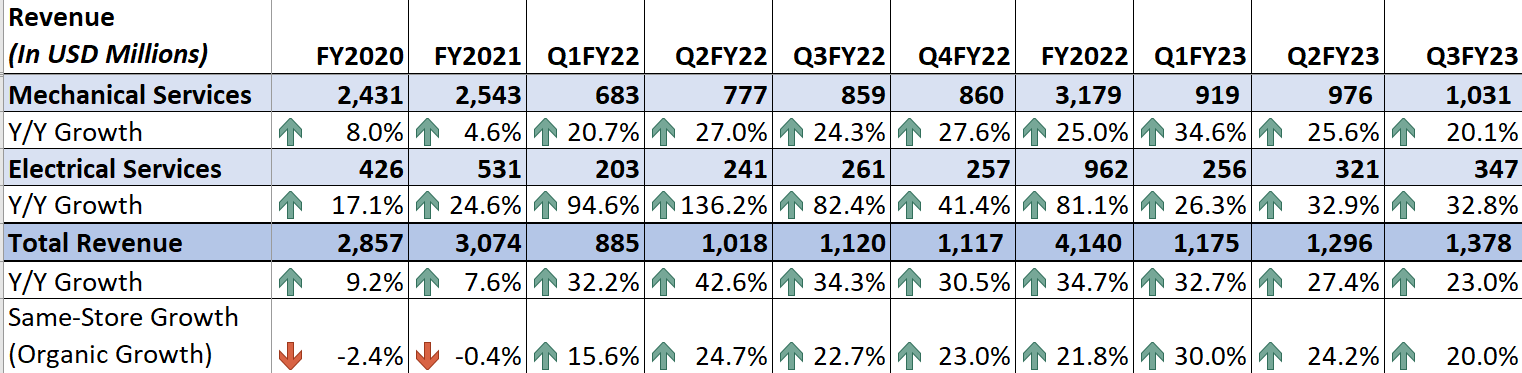

I previously covered the stock in August, where I talked about a potential slowdown in growth. The company has reported its earnings for the third quarter of 2023 since then, and while the organic growth has slowed from 24.2% Y/Y in Q2 to 20% Y/Y in Q3, it still remains at very high levels. In the third quarter of 2023, the company continued to benefit from tailwinds associated with price increases, healthy end-market demand across the segments, and good backlog execution. In addition, the Eldeco acquisition (the company acquired Eldeco in Q1 2023) further supported the top line. This resulted in a 23% Y/Y increase in revenue to $1.37 billion. The revenue growth reflects a 20% Y/Y same-store growth (organic revenue) and a 3 percentage point growth from the Eldeco acquisition. The revenue growth was broad-based across the segments with a 20.1% Y/Y increase in the Mechanical segment and a 32.8% Y/Y growth in the Electrical segment.

FIX's Historical Revenue (Company Data, GS Analytics Research)

{kind=link}

Looking forward, I believe the company should be able to continue delivering sales growth benefiting from healthy backlog levels, and good end-market demand supported by secular trends. However, I also expect the growth rate to normalize moving forward

Exiting the third quarter, the company's backlog stood at $4.28 billion, representing a growth of 31.9% YoY. This strong growth reflects same-store backlog growth (organic growth) of 26.9% YoY and ~5 percentage point contribution from the Eldeco acquisition. This growth was also broad-based across the segments with the Mechanical segment backlog increasing by 22.9% YoY and the Electrical segment backlog increasing by 63.7% YoY. The company's backlog benefited from good demand in the modular business and in the industrial sector.

However, if we look at the sequential backlog trajectory, it has been showing a flattish trend remaining between $4 billion and $4.5 billion over the last four quarters with a peak in Q1 FY23.

FIX's Order Backlog (Company Data, GS Analytics Research)

As the company laps tougher backlog comps starting Q4, I expect backlog growth to normalize. In recent years, the company's backlog has benefited from price increases due to inflation, and supply chain constraints, which were fueling a good amount of pre-bookings. However, moving forward, these benefits are expected to dissipate. The impact of price increases should decline as the company does not plan to take further pricing given moderating inflation. Additionally, as the supply chain conditions improve and project execution becomes more efficient, I anticipate the backlog should gradually return to standard levels. This should also lead to revenue growth normalization as backlog is a leading indicator of revenue growth. Moreover, the company is also facing tough revenue comparisons in the coming quarters. So, we should see the rate of growth of both backlog and revenue slowing down in 2024.

On the Q3 2023 earnings call , talking about the revenue outlook for the upcoming year, management commented:

So we're in budgeting season now. Literally, we're literally going out and getting our field view on that. The comparables get tougher and tougher. Half of the growth until this quarter was inflation. We don't expect net inflation growth, right? We don't expect inflation to reverse currently, but we don't expect it to be a big 10% portion. So I would -- I just don't see how our -- we continue to have same-store revenue growth of 20% next year."

I expect the company's organic growth to slow to low double-digit levels by next year and then single-digit range from FY25 onwards.

Margin Analysis and Outlook

In the third quarter of 2023, FIX's margin growth continued to benefit from improved execution, sales leverage, and price increases. This helped the company offset headwinds from inflationary costs. This resulted in a gross margin expansion of 200 bps YoY to 20.1%. On a segment basis, gross margin increased by 280 bps YoY in the Mechanical segment to 20.4%, while margins in the Electrical segment decreased slightly by 30 bps YoY to 19.4%. The decline in the Electrical segment was due to the lapping of benefits from litigation gains in the prior year's quarter. Consolidated Adjusted EBITDA margin increased by 230 bps YoY to 11.3%.

FIX's Historical Gross Margin and Adjusted EBITDA Margin (Company Data, GS Analytics Research)

Looking forward, the company's margin outlook is mixed. While moderating inflation should help margins, it also means fewer price increases which has supported the company's margin performance meaningfully till now. Further, the company has seen a good amount of large orders in its modular business from large hyperscale data centers and other customers in recent quarters. The orders from these customers often run into 100s of millions of dollars and while they help revenues, the margins in modular business are lower. So, as these orders start converting into revenues they should negatively impact the mix. So, I believe margin prospects are mixed.

Valuation and Conclusion

Comfort Systems USA is currently trading at a forward P/E of 19.78x FY24 consensus estimate of $9.57 which is above its historical 5-year average forward P/E of 18.73x. The company has good revenue growth prospects benefiting from a healthy backlog and secular demand trends, however, the rate of growth is expected to normalize moving forward. Moreover, the margin outlook is also mixed for the coming year. I believe, this normalizing revenue growth and mixed margin growth doesn't warrant a premium valuation and provides less margin of safety. So I would prefer to be on the sidelines and continue my neutral rating.

For further details see:

Comfort Systems USA: Normalizing Growth And Premium Valuation